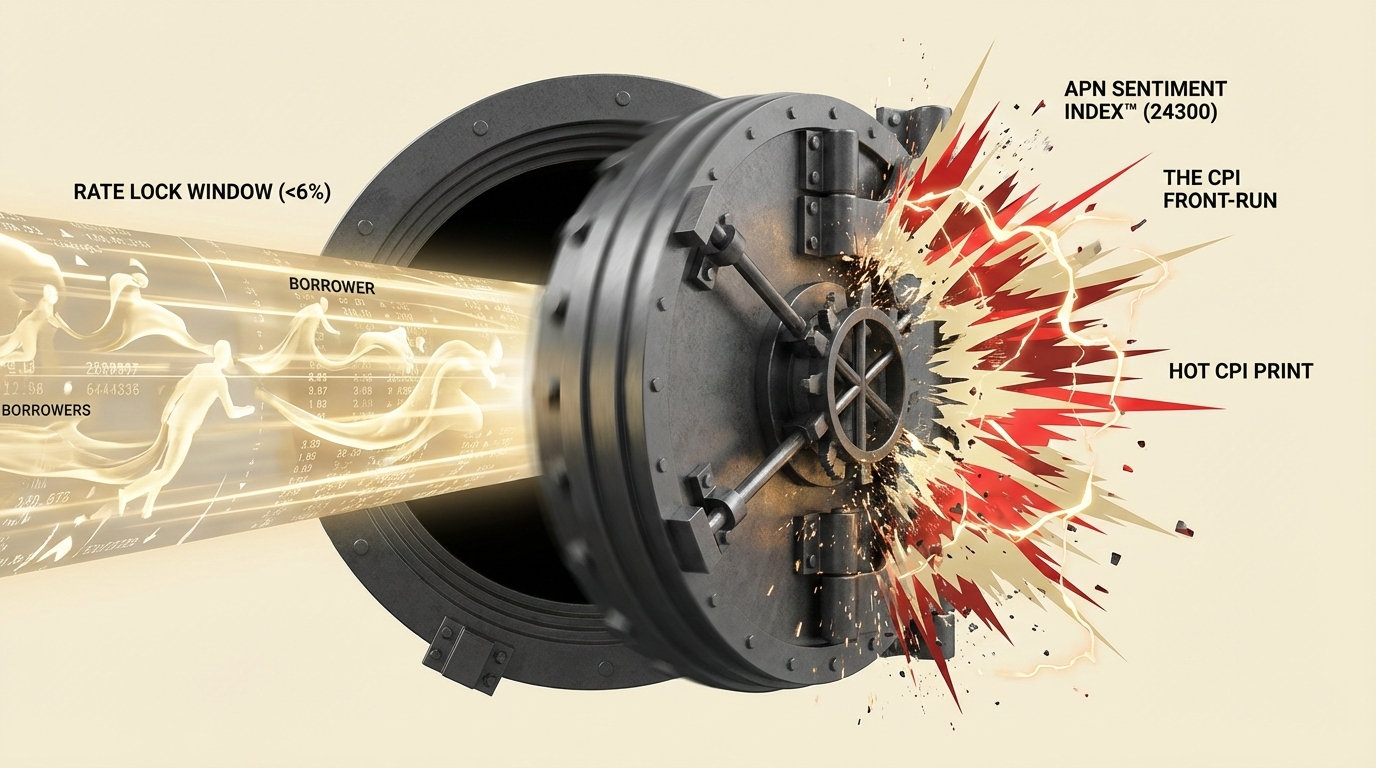

The CPI Front-Run: How Australia’s Major Banks Just Executed a De Facto Rate Hike

APN ANALYSIS: A-260125-AUS135177

Executive Summary

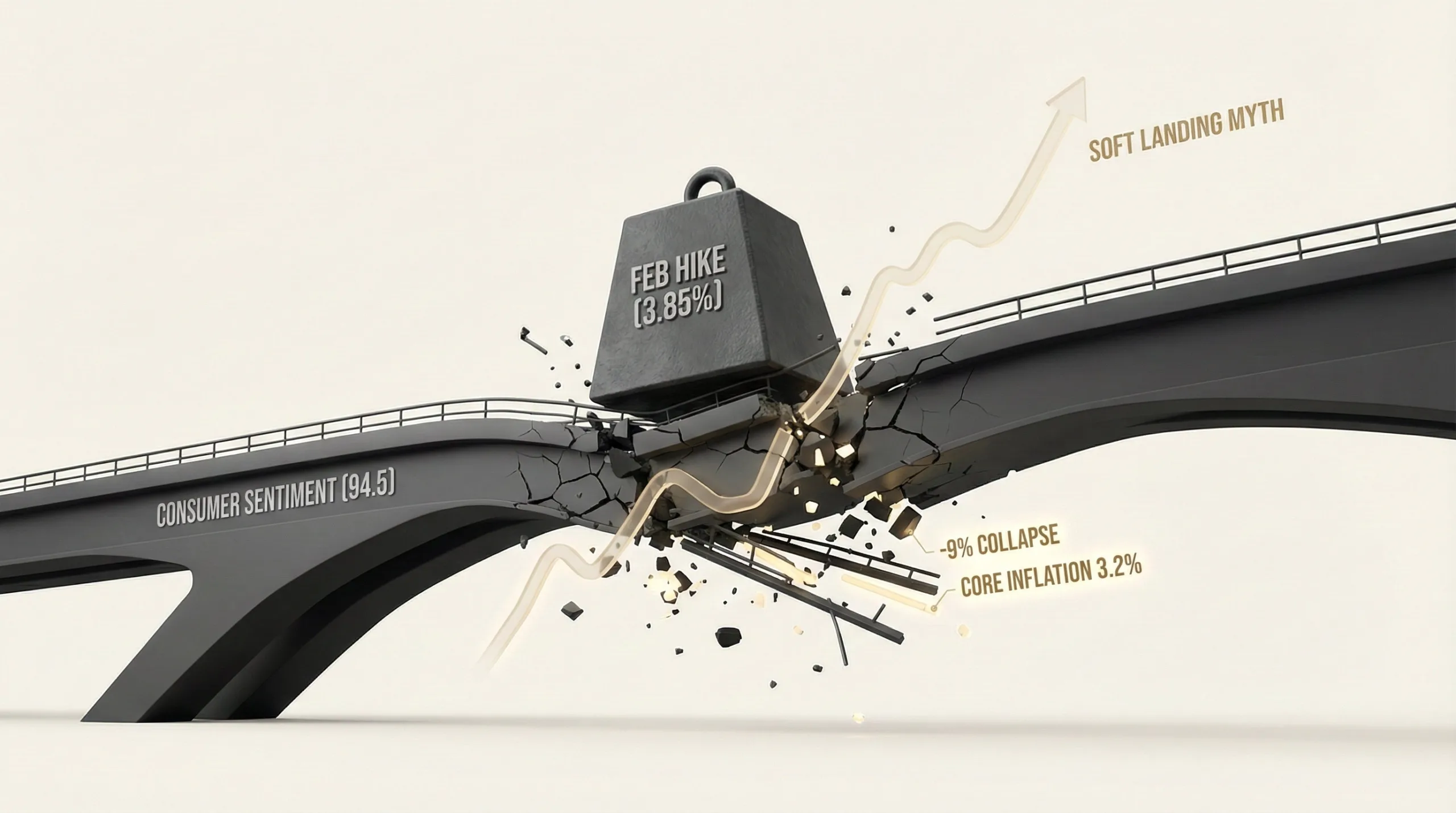

The Australian fixed income and retail banking markets have materially priced in an ‘elevated’ Q4 inflation print, pre-empting the Reserve Bank of Australia’s (RBA) February decision. Led by a substantive 70 basis point hike on 3-Year fixed rates by the Commonwealth Bank (CBA), the major banks have effectively closed the ‘rate lock’ window and established a new 6.00% floor for mortgage pricing. This ‘Codex Structural Adjustment’, the translation of wholesale market risk perception into a real-world pricing adjustment, signals that bank treasury departments, using their own real-time data, are positioning against the RBA’s neutral guidance and preparing for a ‘higher-for-longer’ interest rate environment.

For property professionals, this pre-emptive tightening by the banks is a material event that overrides the RBA’s immediate decision. The material increase in fixed rates to over 6.00% will materially impact borrowing capacity for new buyers and reduce the viability of pre-approved loans that were not rate-locked. This creates a material constraint for transaction volumes and market sentiment in Q1 2026, demanding an immediate recalibration of client advice and deal structuring.

Background & Strategic Context

This event validates and calibrates APN’s core thesis that state-level actors, in this case, the major banks acting as a proxy for monetary policy transmission, are a material factor shaping market boundaries. The ‘CPI Front-Run’ is a clear example of how institutional ‘pre-cognition’ can create structurally significant events independent of official central bank action, necessitating a structural repricing of risk across the entire economy.

A De Facto Policy Intervention (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The aligned repricing by CBA and NAB represents a de facto tightening of credit conditions. This intervention by regulated entities directly impacts the property market’s operational boundaries, effectively bypassing the formal RBA cash rate-setting process and demonstrating how structurally significant private sector actors can front-run and influence policy outcomes.

A Widening Credit Divide: This substantive repricing disproportionately benefits the banks by protecting their Net Interest Margins (NIMs) against rising funding costs. It simultaneously creates a material barrier for new market entrants and marginal borrowers, who now face higher serviceability hurdles, thereby reinforcing the economic advantage of incumbent asset holders not exposed to new credit origination.

A Contraction in Conviction (APN Professional Sentiment Index™): The substantive repricing in the bond and swap markets, which was the primary driver of the banks’ repricing, is a quantifiable manifestation of contracting professional sentiment. The 54% probability of a rate hike priced into futures markets reflects a structurally embedded lack of conviction in the RBA’s ability to contain sticky domestic inflation, a core metric tracked by the APN Professional Sentiment Index™ (24300).

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing analysing market data from January 15 to January 23, 2026. The key observations are:

- The Futures Market Pricing: The ASX 30-Day Interbank Cash Rate Futures for February 2026 closed with an implied yield of 3.735%, pricing in a 54% probability of a 25 basis point RBA rate hike at its February 3 meeting.

- The Sovereign Bond Yield Escalation: The Australian 3-Year Government Bond yield materially escalated to 4.27%, a 37 basis point increase in under a month, signalling a structural repricing of medium-term interest rate expectations away from a ‘managed economic deceleration’ scenario.

- The Retail Banking Catalyst: On January 15, Commonwealth Bank (CBA) hiked its 3-Year Fixed Rate mortgage by a material 70 basis points to 6.04%, a pre-emptive adjustment executed two weeks before the official CPI data release.

- Systemic Confirmation: National Australia Bank (NAB) followed on January 23, hiking its fixed rates by up to 40 basis points. This confirmed the move was a systemic banking sector response to funding pressures, not an isolated institutional decision.

- The US Divergence: The spread between the Australian and US 10-Year government bond yields widened to over 54 basis points, confirming the sell-off was driven by idiosyncratic risk perception regarding domestic inflation, not just imported volatility from the US.

Critical Analysis & Balanced View

The market behaviour suggests not ‘insider trading’ in the legal sense, but ‘defensive pre-cognition’ by the major banks. With access to vast, real-time transaction data, bank treasury departments possess an analytical edge over the market and even the RBA, which relies on lagging official statistics. CBA’s decision to hike rates so substantively implies their internal data models were already signalling an ‘elevated’ inflation print, incentivising them to protect their balance sheet by ‘front-running’ the official data release.

The critical insight is the ‘Codex Structural Adjustment’: the moment when esoteric bond-market signals translate into real-world pricing adjustments. While the physical 3-Year bond yield did not breach the 4.50% valuation threshold, the underlying swap rates that banks use for funding almost certainly did. This validates the ‘yield escalation’ thesis in the funding market that matters most to the real economy. The key paradox is that the RBA’s influence over monetary conditions has been materially diminished before its meeting. The banks have tightened policy on their behalf, creating a complex decision matrix: hiking now validates the elevated market anxiety, but pausing risks a ‘dovish adjustment’ and being seen as operating with an elevated lag to market conditions.

Strategic Implications for Property Professionals

- For Agents & Buyers’ Agents: Immediately contact all clients with active pre-approvals. Verify if a ‘Rate Lock’ fee was paid. If not, their borrowing capacity has likely been materially reduced, requiring an urgent reassessment of their purchasing power and target properties before the pre-approval expires.

- For Mortgage Brokers: Triage your application pipeline. Prioritise clients who can still meet serviceability at rates above 6.00% (which test at over 9.00% under APRA’s buffer). Prepare for an elevated volume of application rework and proactively communicate the closure of the sub-6% fixed-rate window to manage client expectations.

- For Developers: Re-run feasibility studies for all current and pipeline projects. The escalation in funding costs and the contraction in buyer borrowing capacity will directly impact end-sales velocity and Gross Realisation Values (GRVs). Off-the-plan marketing strategies must now account for a more constrained and uncertain credit environment.

- For Valuers & Asset Managers: The 6.00% fixed-rate floor acts as a new valuation benchmark. This de facto tightening of credit will put downward pressure on transaction volumes and, potentially, on asset prices in the short term, particularly for secondary-grade assets or locations with greater interest-rate sensitivity.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the sensitivity of the APN Professional Sentiment Index™ (24300), as the substantive repricing in futures and swap markets represents a quantifiable contraction in institutional confidence ahead of official data.

- Index Calibration: The APN Risk & Compliance Index™ (24200) is calibrated to recognise this ‘Codex Structural Adjustment’ event. The banks’ pre-emptive repricing serves as a form of private-sector regulatory action, increasing operational risk across all credit-dependent activities and demonstrating a key tenet of the APN Risk & Compliance Index™ (24200).

- Data Capture: This event triggers a new data capture mandate for the APN Symbiotic Intelligence Network™ (24310) to track the spread between major bank fixed-rate mortgage pricing and the 3-Year swap rate, quantifying the ‘risk premium’ being applied in the retail credit market.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.