RBA Policy Failure Confirmed: ‘Wealth Funnel’ Inflation Forces End of Easing Cycle, Trapping Developers

APN ANALYSIS: A-251115-AUS130469

Executive Summary

The Reserve Bank of Australia’s decision to hold the cash rate at 3.60% on November 4, 2025, marks the end of the 2025 monetary easing cycle. This policy inflection was not discretionary; it was necessitated by a September quarter inflation print that the RBA itself described as “materially higher than expected,” with its preferred underlying measure breaching the 2-3% target band. Critically, APN analysis confirms the RBA’s own statements validate that its recent rate cuts directly fuelled this inflation by over-stimulating the housing market, a mechanism APN identifies as The Wealth Funnel. The central bank has been forced to abandon its easing stance because its own policy became a primary driver of the inflation it is mandated to control.

For property professionals, this is not a temporary pause but the establishment of a new, structurally higher interest rate environment. The market’s consensus pivot to a “higher-for-longer” reality invalidates development feasibility and funding models predicated on a terminal cash rate below 3.60%. This policy failure has triggered a stagflationary feedback loop: higher rates suppress new supply, which in turn exacerbates the housing-led inflation that prevents the RBA from cutting rates. This creates a period of profound uncertainty, directly impacting developer sentiment, project viability, and risk pricing across the entire sector.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses, demonstrating how state-level intervention directly shapes market outcomes and creates systemic risk. The RBA’s policy pivot is a textbook example of a primary actor being forced to react to the second-order consequences of its own decisions, confirming the causal frameworks APN uses to analyse the Australian property market.

The State as Primary Actor (Project Overlord): The RBA’s monetary policy, first the 2025 easing cycle, then the abrupt November hold, is the single most dominant force shaping market conditions. This event proves that state-level decisions, not organic market forces, are setting the boundaries for capital costs, asset valuation, and development feasibility, validating the core tenet of Project Overlord.

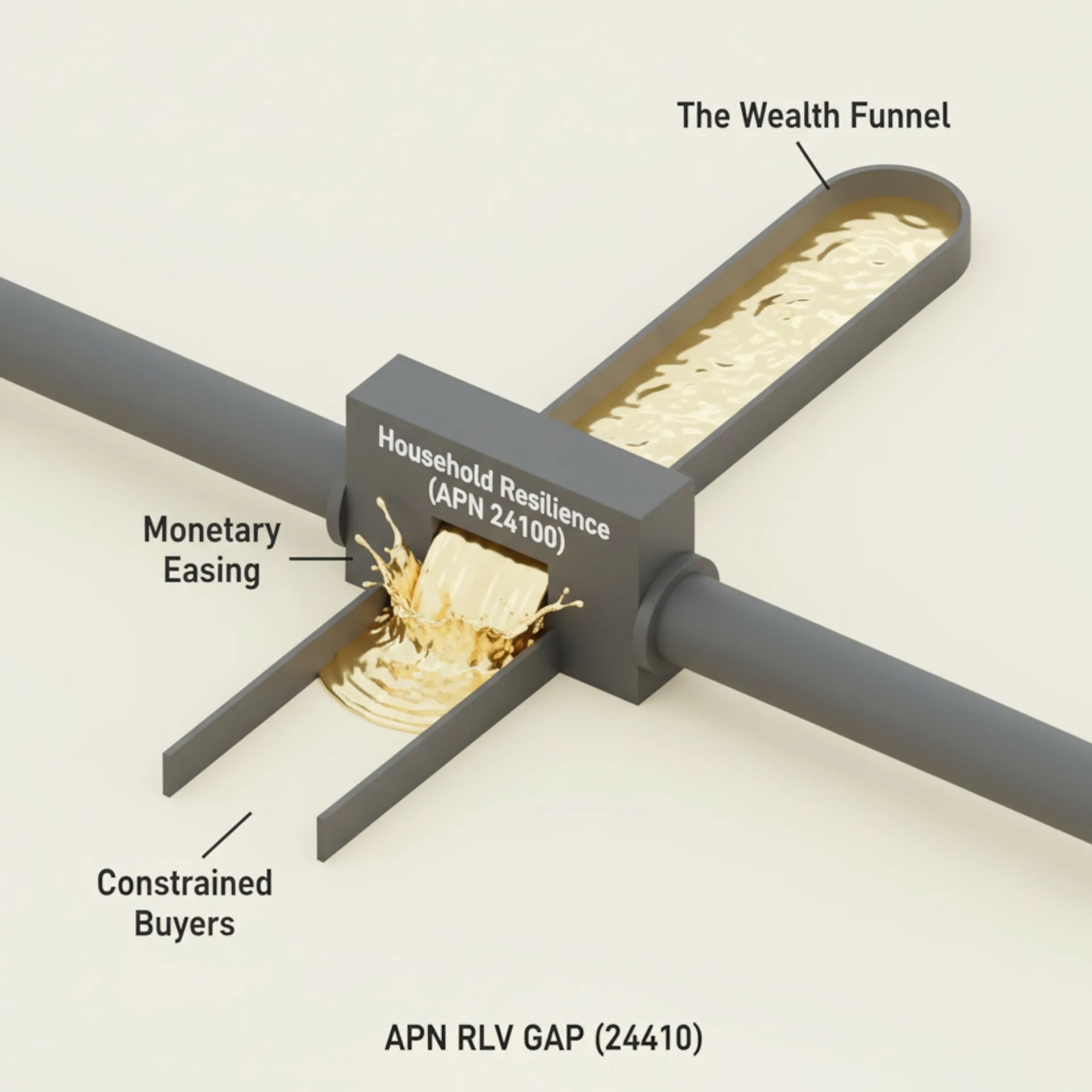

Validating the Inflation Mechanism (The Wealth Funnel): The RBA’s own statement provides a verbatim admission of The Wealth Funnel mechanism. It draws a direct causal link from its “recent interest rate reductions” to a “strengthening” housing market, which in turn caused “Housing prices” and “dwelling construction costs” to rise, feeding the very inflation that forced the policy reversal.

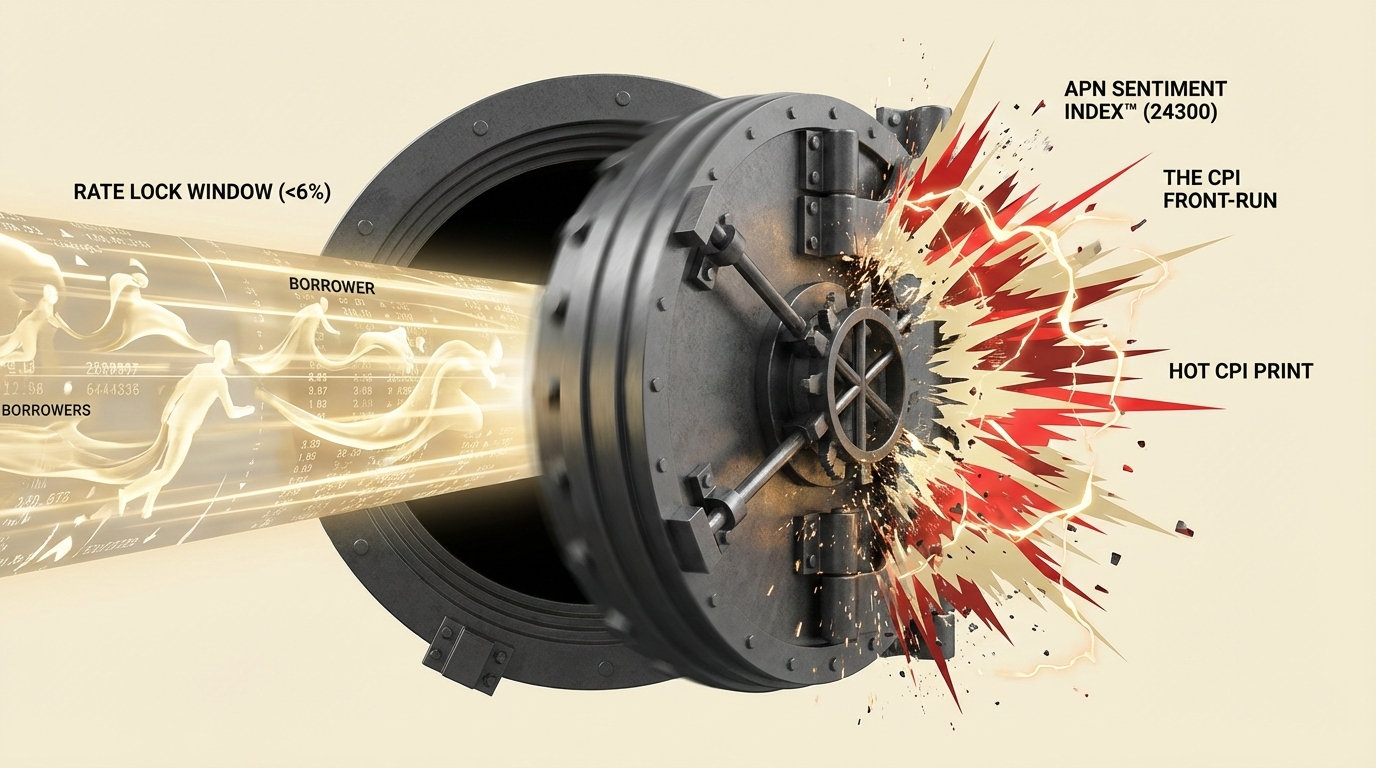

Quantifying the Sentiment Shock (APN Professional Sentiment Index™): The policy inflection triggered an immediate and quantifiable collapse in professional confidence, as market expectations for further rate cuts were “wiped out” and replaced with the new risk of a hike. This validates the APN Professional Sentiment Index™ (24300) as a real-time leading indicator of the “animal spirits” that drive investment and development decisions.

Exposing the Viability Gap (APN Future Development Pipeline Index™): The new “higher-for-longer” rate environment is a direct economic friction applied to all development projects. This widens the Residual Land Value (RLV) Gap by increasing the cost of capital, rendering previously viable projects unfeasible. This event demonstrates the core function of the APN Future Development Pipeline Index™ (24400), which filters economically unviable “Paper Rezonings” from the genuine supply pipeline.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Reserve Bank of Australia’s November 4, 2025, policy statements, associated publications, and the subsequent market reaction. The key facts are:

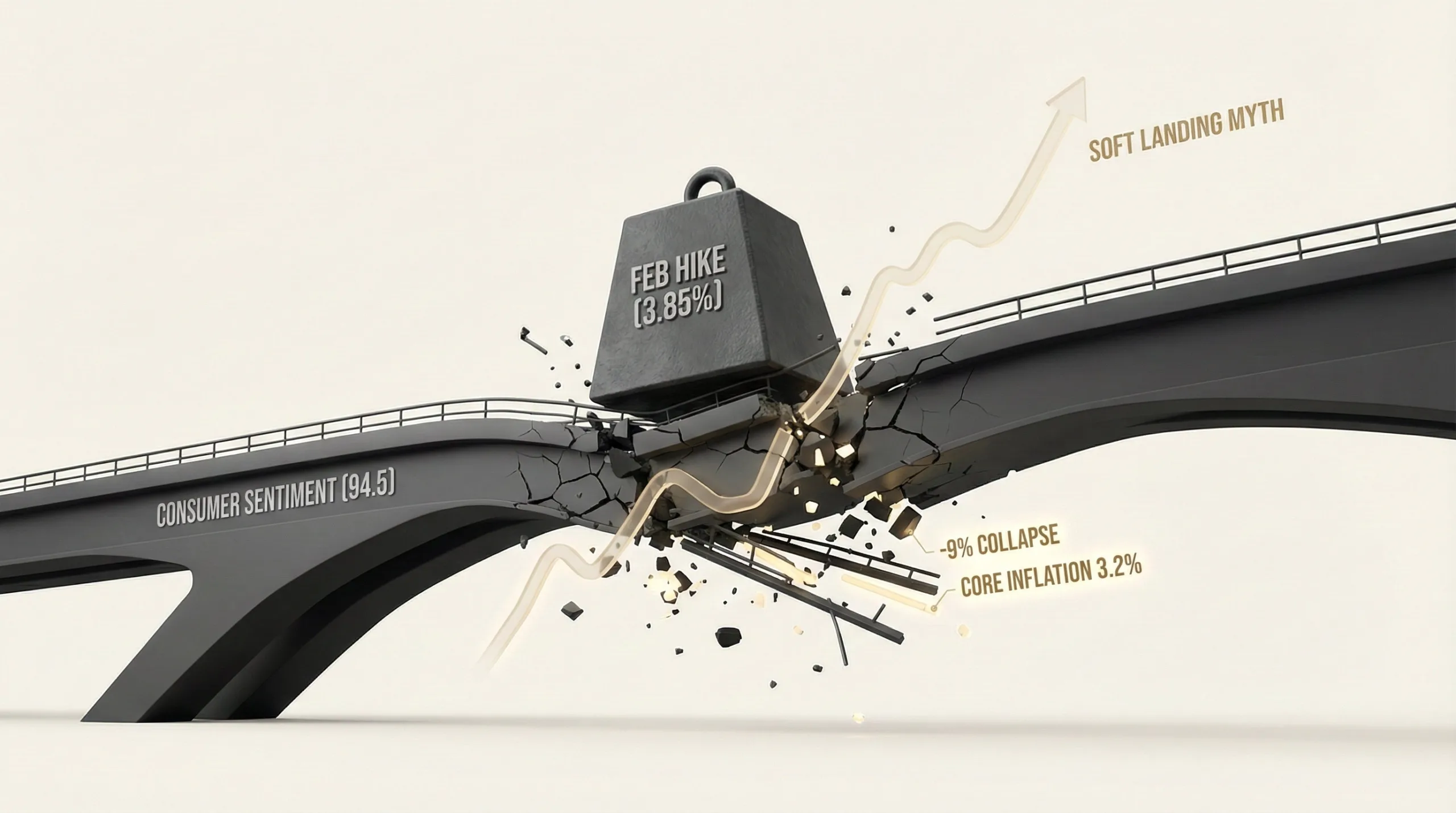

- Policy Inflection: The RBA held the cash rate at 3.60%, officially terminating the 2025 easing cycle which had seen three prior cuts. This was a forced “hawkish hold” in response to new data.

- Inflation Breach: The decision was driven by September quarter trimmed mean inflation hitting 1.0% for the quarter and 3.0% annually, breaching the RBA’s 2-3% target band. The RBA admitted this was “materially higher than expected.”

- ‘Wealth Funnel’ Admission: In its official statement, the RBA explicitly linked its “recent interest rate reductions” to the “effect” of a “strengthening” housing market, which in turn was causing “Housing prices” to rise and “dwelling construction costs” to “increase again.”

- Market Expectation Collapse: Market-priced probability of a 2025 rate cut “collapsed to near zero” following the inflation data and RBA hold. All four major Australian banks retracted or delayed forecasts for further cuts, cementing 3.60% as the new terminal rate for the cycle.

- Emergence of Hike Risk: The policy pivot introduced a new negative optionality into the market. Analysts began “raising the risk of another hike,” a scenario that was considered negligible during the easing cycle, confirmed by Governor Bullock’s admission that the board “did not consider cutting rates.”

Critical Analysis & Balanced View

The RBA’s communication strategy around the November 4 hold reveals a deeper policy paradox. In its official statement, the bank practices a form of “semantic shielding” by structurally separating the paragraph on “materially higher” inflation from the paragraph discussing the housing boom. It avoids making the explicit connection that the rising housing and construction costs it is stimulating are a core domestic driver of the inflation it is fighting. This is a deliberate communication tactic to de-link its policy (easing) from its negative consequence (housing-led inflation).

This exposes the RBA’s conflicting mandates. The easing cycle was intended to support the labour market, but it has instead over-stimulated The Wealth Funnel, forcing the inflation-targeting mandate to take precedence. Furthermore, a critical contradiction exists between the RBA’s formal modelling and its real policy signal. The official Statement on Monetary Policy contains a “technical assumption” of a future rate cut to achieve its 2027 inflation target, yet Governor Bullock’s press conference guidance dismissed this possibility. The market correctly interpreted the Governor’s hawkish verbal signal as the true policy, rendering the official forecast a dovish fiction designed to soften the market’s reaction.

The synthesis of this analysis reveals a structural “stagflation doom loop.” RBA easing fuelled The Wealth Funnel, causing housing inflation. This forced the RBA to halt easing, creating a “higher-for-longer” rate environment. This damages developer feasibility, constraining new housing supply. The resulting undersupply ensures housing costs and rents remain elevated, feeding back into the inflation that prevents the RBA from delivering the rate cuts the sector needs. The negative sentiment is therefore not a reaction to a single rate decision, but a realisation of this structural trap.

Strategic Implications for Property Professionals

- For Developers: The “higher-for-longer” rate environment is the new baseline. Funding models predicated on a sub-3.60% terminal rate are now invalid. Immediately stress-test project feasibilities against a widened Residual Land Value (RLV) Gap, persistent high construction costs, and the increased probability of settlement risk.

- For Investors & Asset Managers: The Wealth Funnel mechanism will continue to support incumbent asset values (especially established housing) in the short-term due to constrained new supply. However, the emergence of “Stagflation Risk” is a primary threat to real returns and will cap capital growth prospects in the medium term. A flight to quality is the logical portfolio response.

- For Agents & Buyers’ Agents: Market psychology has pivoted from optimism to uncertainty. Prepare for a bifurcated market where marginal buyers are sidelined and A-grade assets command a premium. Client education is critical: the easing cycle is over, and near-term mortgage relief is highly unlikely, fundamentally altering buyer capacity.

- For Lenders & Financiers: The credit risk profile for the property sector has materially shifted. The removal of expected rate cuts increases settlement risk for off-the-plan developments and default risk for highly leveraged borrowers. Re-evaluate serviceability buffers and loan-to-value ratios for both commercial and residential lending, particularly for secondary assets or fringe projects.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation (Codex 24300): This analysis provides definitive validation for the APN Professional Sentiment Index™ (24300). The immediate collapse in rate cut expectations, the unanimous pivot from bank economists, and the emergence of “Stagflation Risk” in analyst commentary directly correlate with the negative sentiment captured from developers and peak bodies.

- Validation (The Wealth Funnel): The RBA’s explicit admission of the causal chain, from its own rate cuts to rising housing and construction costs, provides primary source validation for The Wealth Funnel as a core APN analytical framework for understanding market mechanics.

- Index Calibration (Codex 24400): The APN Future Development Pipeline Index™ (24400) is recalibrated to reflect the increased cost of capital. The new “higher-for-longer” rate environment functions as a significant economic friction filter, widening the Residual Land Value (RLV) Gap and increasing the index’s weighting towards a higher probability of “Paper Rezonings.”

- Data Capture Mandate (Codex 24300): This event triggers a new data capture mandate for the APN Professional Sentiment Index™. The mandate is to track and quantify the divergence between the RBA’s official published forecasts and the Governor’s discretionary verbal guidance, treating this gap as a key metric of policy credibility and a driver of professional uncertainty.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness.

Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down.

Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.