Divergence in Economic Sentiment: APN Analysis Indicates a February Rate Hike to 3.85% as the Base Case

APN ANALYSIS: A-260109-AUS134164

Executive Summary

The Australian economy is experiencing a ‘Sentiment-Expectation Divergence’, a material divergence between positive market expectations and the more restrictive policy outlook being forecast by major institutions. Despite a recorded fall in headline inflation to 3.4%, APN’s analysis indicates the Reserve Bank of Australia has sufficient justification to deliver a 25-basis-point rate hike in February 2026. This is driven by persistently elevated ‘core’ inflation (3.2%), driven by structural pressures in services, housing, and a 19.7% electricity price increase. The substantive shift by CBA and NAB to forecast a 3.85% cash rate is no longer a tail risk but a central probability, materially eroding the consumer sentiment recovery observed in late 2025.

For property professionals, this analysis signals an immediate end to the ‘wait-and-see’ approach. The rapid repricing of rate expectations is already acting as a tightening mechanism, evidenced by a 9% material contraction in consumer confidence. This ‘risk perception of a rate increase’ will translate into a measurable slowdown in discretionary spending and transaction volumes in Q1 2026, regardless of the RBA’s final decision. The key strategic imperative is to hedge for a 3.85% cash rate, stress-test project feasibilities against a 4.10% higher-risk scenario, and prepare for a market where buyer borrowing capacity, not sentiment, becomes the primary constraint on price growth.

Background & Strategic Context

This concentrated divergence in monetary policy expectations validates and calibrates APN’s core macro-theses on how state intervention and market sentiment shape the Australian property landscape. The RBA’s position, balancing accelerating domestic growth and slowing global trends, places it in a position where decisive, and potentially materially restrictive, action becomes the path of least regret. This creates an elevated volatility environment where our proprietary frameworks are instrumental for assessing uncertainty.

The Primacy of State Intervention (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The RBA’s potential hike is an action consistent with the SPCI framework, where a state-level actor must intervene to manage economic boundaries, in this case, to materially constrain persistent domestic inflation. The analysis shows the RBA is isolated, unable to rely on a global recession to cool the economy, forcing its hand and demonstrating that monetary policy remains the primary factor shaping asset values in the short-to-medium term.

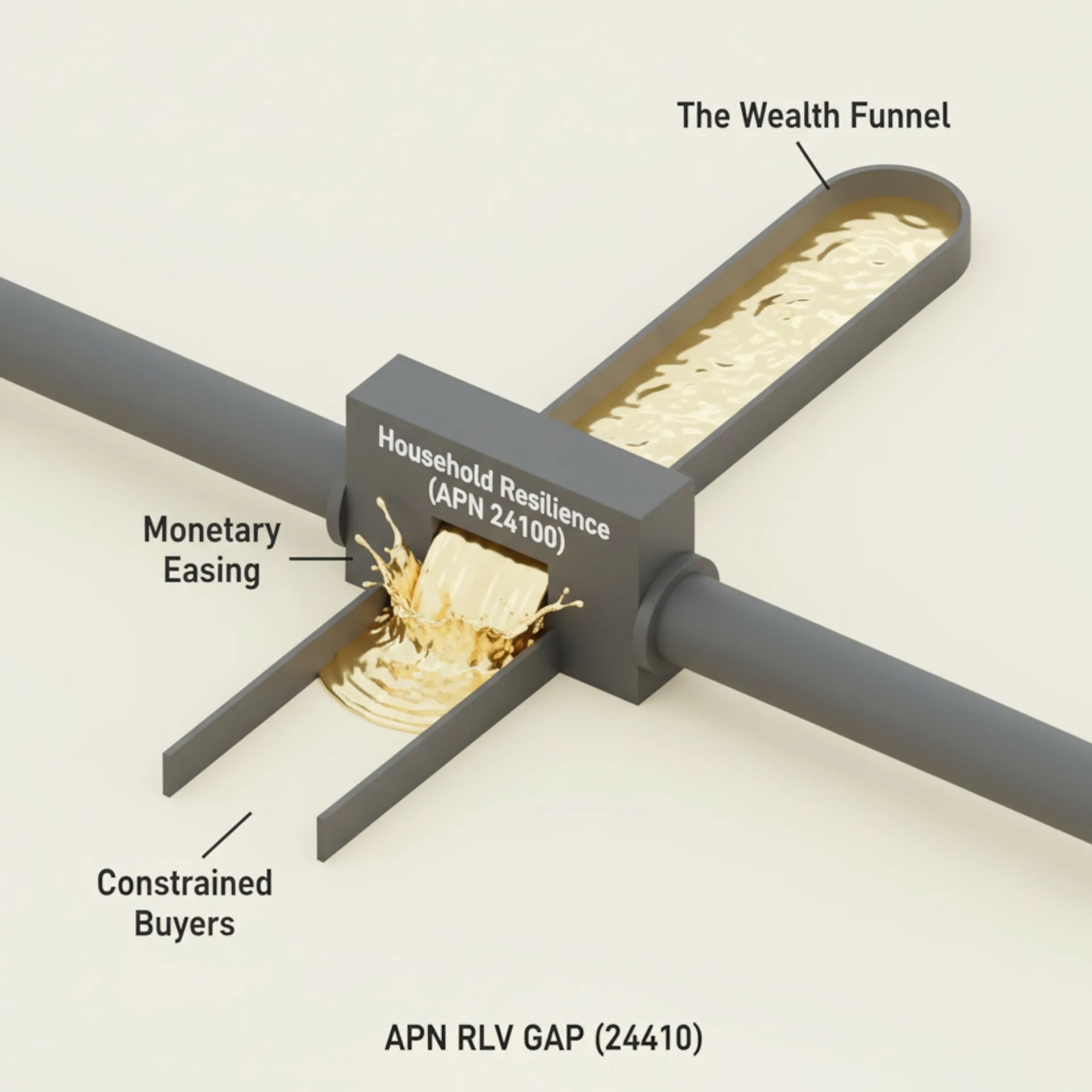

The Widening Socio-Economic Divergence: The data reveals a bifurcated economy. Resilient housing prices, coupled with an expanding ‘experience economy’, demonstrate that incumbent asset holders and those with secure, high incomes are insulated from rate signals. Meanwhile, the 9% material contraction in sentiment among mortgaged households shows that the adverse impact is concentrated on the leveraged consumer, increasing the divergence between asset-holding and credit-dependent cohorts.

The Amplification of Uncertainty (APN Regulatory Velocity Multiplier™): The ‘Sentiment-Expectation Divergence’ is a clear illustration of an elevated RVM environment. The rapid repricing of rate expectations by CBA and NAB, creating a 100-basis-point spread with Westpac’s forecast, has materially increased the ‘velocity’ of policy uncertainty. This uncertainty is not benign; it is actively constraining capital expenditure and incentivising households to reduce spending, amplifying the economic impact beyond the potential effect of the rate increase itself.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the January 2026 macroeconomic data set, including the ABS Monthly CPI Indicator, major bank economic updates, and consumer sentiment surveys. The key facts are:

- Institutional Pivot: CBA and NAB have solidified forecasts for a February 2026 cash rate hike to 3.85%. NAB’s position is notably substantive, flagging a potential second hike to a terminal rate of 4.10% by May 2026, in direct contrast to the market’s prior easing bias.

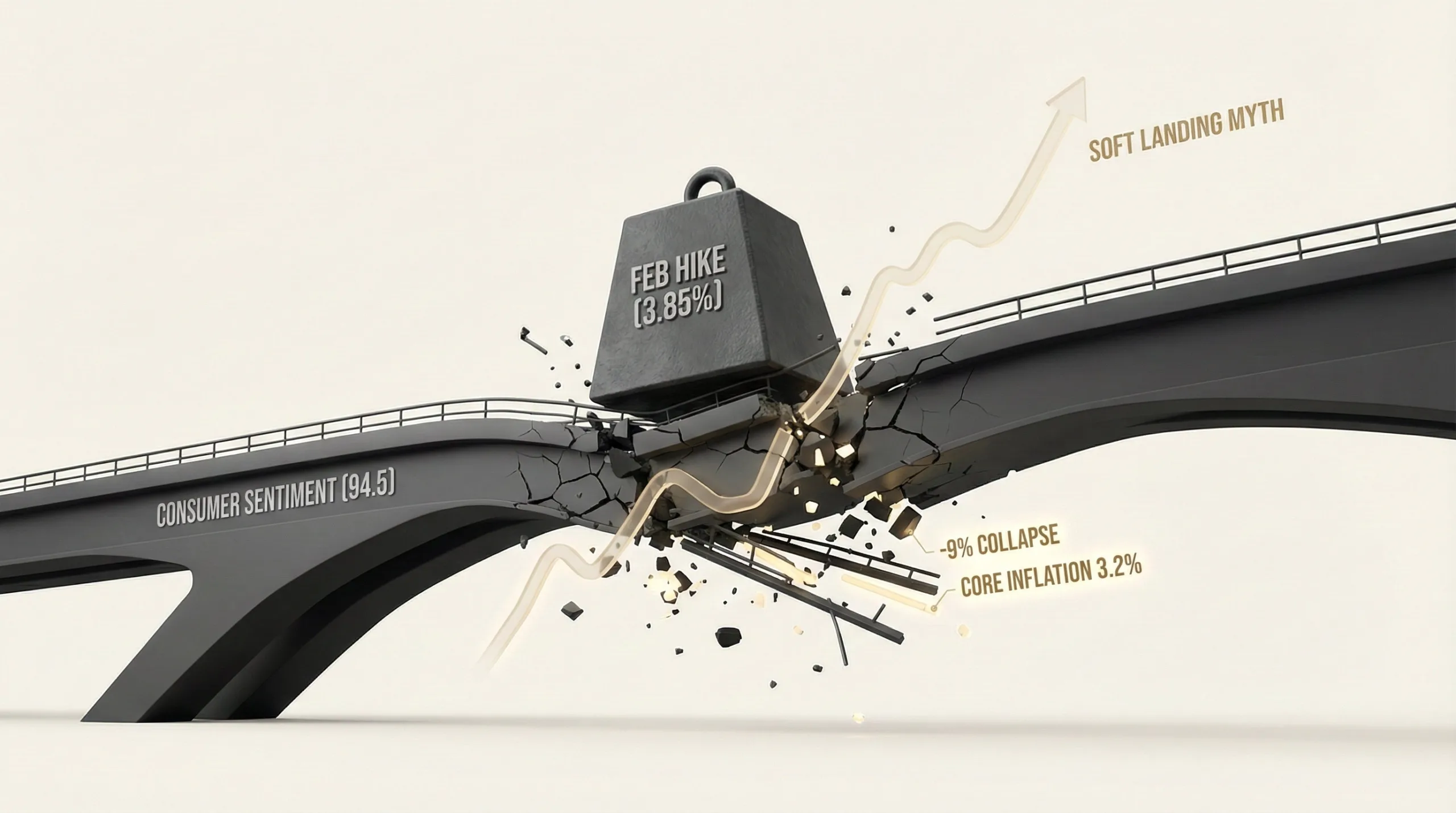

- Inflationary Data Interpretation: The headline CPI for November 2025 fell to 3.4%, but this does not fully represent a more elevated underlying condition. The RBA’s preferred ‘Trimmed Mean’ measure of underlying inflation remains persistently elevated at 3.2%, well outside the 2-3% target band and showing little downward momentum.

- Core Inflation Drivers: The persistence of inflation is not broad-based but concentrated in non-tradable, interest-rate-insensitive sectors. This includes a statistically significant 19.7% year-on-year increase in electricity prices and a 4.0% rise in rents, which monetary policy has limited direct influence over.

- Sentiment Contraction: The Westpac-Melbourne Institute Consumer Sentiment Index contracted by 9% in a single month, falling from a moderately positive 103.8 to a materially negative 94.5. This was driven by a sharp reversal in mortgage rate expectations from ‘cuts’ to ‘hikes’.

- Retail Distortion: A 4.6% YoY rise in November retail spending was indicative of distortion rather than underlying strength. It was driven by consumers delaying purchases for Black Friday sales (goods) and accelerated growth in the ‘experience economy’ (concerts, sport), a services category demonstrably less sensitive to interest rate signals.

Critical Analysis & Balanced View

The current economic environment is defined by a series of substantive paradoxes that complicate the RBA’s decision-making and elevate risk for property professionals. Firstly, we are witnessing a ‘Two-Speed Inflation’ dynamic. While global supply chains have helped cool goods inflation, domestic services inflation remains persistently elevated. The RBA’s blunt instrument—the cash rate—cannot target one without materially constraining the other, meaning it may need to accept the risk of a retail sector contraction to tame the services sector.

Secondly, there is a material ‘Sentiment-Spending Disconnect’. Consumers report materially negative sentiment and risk perception of rate hikes, yet their behaviour, particularly the accelerated growth in spending on entertainment and experiences, suggests a pattern of immediate consumption supported by a still-tight labour market. This complicates the RBA’s objective of demand destruction, as consumers are cutting back on goods but not on services, the very sector generating inflationary pressure.

Finally, the ‘Market-Reality Disconnect’ presents a significant structural risk. The ASX 200 is pricing in a ‘managed economic deceleration’ scenario, buoyed by forecasts of accelerating GDP growth. This optimism is materially diverged from the consumer sentiment contraction and the more restrictive outlooks from major banks. This divergence creates a vulnerability where a non-consensus hike could trigger a material repricing not just in bond markets, but across equity and asset values as the market realigns with the more constrained economic outlook.

Strategic Implications for Property Professionals

- For Developers & Financiers: The 100-basis-point divergence between NAB’s and Westpac’s forecasts creates elevated uncertainty for project feasibility. Assume a higher cost of capital (base case 3.85%) for H2 2026 and stress-test projects against NAB’s 4.10% scenario. This elevated RVM environment justifies delaying new capital-intensive commitments until after the February RBA decision provides clarity.

- For Commercial Landlords (Retail & Office): The analysis reveals a bifurcated consumer base. While ‘experience’ spending is resilient, traditional goods retail is exposed. Landlords with tenants in the discretionary goods sector (e.g., department stores, fashion) should factor increased vacancy risk and pressure on rents. Conversely, assets tied to the ‘experience economy’ (e.g., entertainment precincts) show short-term resilience.

- For Agents & Buyers’ Agents: The material contraction in consumer sentiment to 94.5 is a strong leading indicator of a slowdown in transaction volumes. While prices are currently holding up due to supply constraints, buyer borrowing capacity will be directly impacted by a hike. Prepare clients for a market where finance approvals become the primary constraint, and the ‘accelerated acquisition phase’ is replaced by the ‘risk perception of overvaluation’.

- For Asset & Portfolio Managers: The ‘Sentiment-Expectation Divergence’ necessitates a portfolio review to identify assets vulnerable to an abrupt contraction in consumer spending. Underweight consumer discretionary-exposed assets. The 19.7% electricity price increase is a direct input cost for all businesses and a political risk; monitor for government intervention (e.g., rebates) in the May budget, which could distort inflation signals and complicate the RBA’s path.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the elevated sensitivity of the APN Regulatory Velocity Multiplier™ (APN RVM™) (24210). The rapid 9% contraction in consumer sentiment following bank forecast changes confirms the model’s premise that the velocity of policy expectation shifts can generate economic friction comparable to an actual policy change.

- Index Calibration: The APN Sentinel™ (24120) index is calibrated to reflect the material decoupling between consumer sentiment (negative) and business confidence (resilient but falling). The 9-point drop in the Westpac index against a more moderate fall in the NAB business survey provides a new calibration point for sentiment divergence.

- Data Capture: This event triggers a new data capture mandate for the APN Agora™ (24140). The distinction between ‘goods-based’ retail (Black Friday) and ‘experience-based’ consumption (concerts, sport) must be tracked as separate sub-components to more accurately measure the drivers of local economic activity and their respective sensitivity to monetary policy.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.