The Resilience Trap: RBA Confirms Household Buffers are Sustaining Higher Rates and Contributing to Accelerated Capital Asymmetry

APN ANALYSIS: A-251117-AUS130602

Executive Summary

Analysis of the Reserve Bank of Australia’s October-November 2025 data confirms the ‘Resilience Trap’ is now an active market mechanism. The RBA’s own Financial Stability Review has certified the material financial resilience of the household sector, which possesses material liquidity and equity buffers. This strength has created a policy paradox: the RBA is now unable to cut interest rates due to the perceived risk that this ‘resilient’ majority will immediately re-leverage into the housing market and amplify systemic risk. This forced ‘higher-for-longer’ pause, publicly justified by inflation-distorted spending data, has been validated by major bank economists, who have pushed rate cut expectations out to mid-2026.

For property professionals, this establishes a 6-9 month period of accelerated capital asymmetry. The extended period of elevated interest rates functions as a significant barrier to entry for new buyers and places sustained pressure on highly-leveraged, non-incumbent investors. This environment disproportionately benefits asset-rich incumbents who possess the very financial buffers that created the structural constraint, protecting their asset values and creating opportunities to acquire assets from constrained sellers. The market will now materially segment between capital-rich and capital-constrained participants, accelerating wealth divergence.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses, demonstrating how state-level intervention is the primary force shaping market boundaries and socio-economic outcomes. The RBA’s policy constraint is not a passive market event; it is an active intervention that creates a predictable, two-tiered market structure for the foreseeable future.

Confirming the Primacy of State Intervention (APN Sovereign Policy Composite Index™): The RBA’s decision to maintain a restrictive policy stance, despite expectations of easing, is a direct state-level intervention. This action overrides conventional market cycles, proving that regulatory and central bank policy—the core of the APN Sovereign Policy Composite Index™ (SPCI, 24800) framework—remains the primary determinant of market access, credit availability, and ultimately, asset valuation.

Illustrating a Capital Concentration Mechanism: The outcome of the RBA’s ‘Resilience Trap’ illustrates how the policy pause disproportionately benefits incumbent asset holders by maintaining high entry barriers for competitors and protecting existing asset values from the deflationary effects of a broader downturn. This functions as a mechanism that transfers economic advantage to a specific cohort.

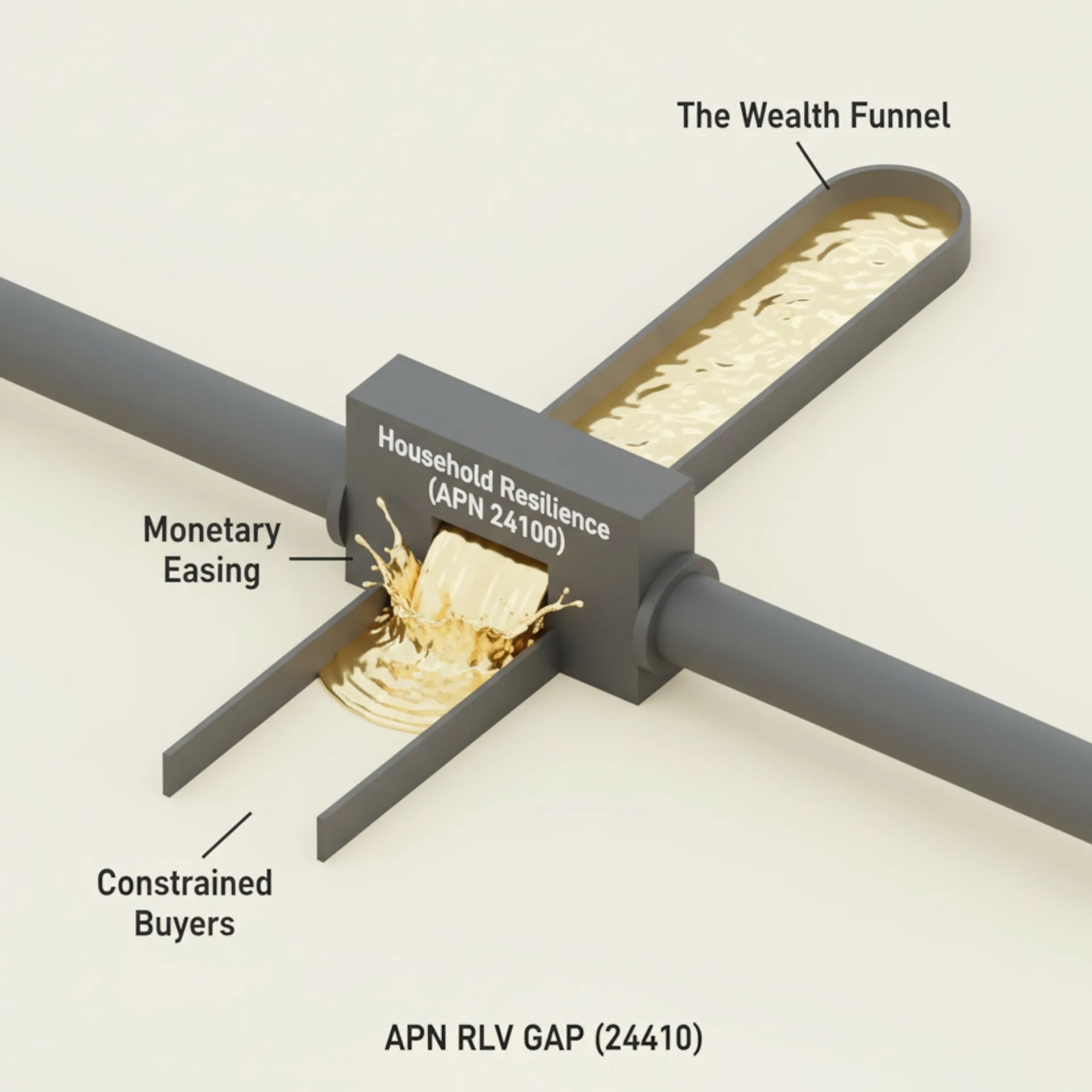

Quantifying the Paradox of Resilience (APN Social Capital Index™): The household buffers identified by the RBA are a key input for the financial stability metrics within our APN Social Capital Index™ (24100). This analysis reveals an elevated paradox: while high household financial resilience is positive for social cohesion and stability (Project Bedrock), it simultaneously blunts the effectiveness of monetary policy, creating a negative feedback loop that produces adverse outcomes for other sectors of the economy and increases structural capital asymmetry.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Reserve Bank of Australia’s October 2025 Financial Stability Review, Commonwealth Bank’s October 2025 HSI data, and subsequent market analysis from November 2025. The key facts are:

- RBA Confirms Elevated Household Resilience: The RBA’s October FSR certified that ‘Most mortgagors have maintained material liquidity and equity buffers’. Quantified data showed the median variable-rate owner-occupier holds prepayment buffers equivalent to ~2 years of repayments, while less than 1% of mortgagors are in negative equity.

- RBA Identifies Resilience as a Systemic Risk: The FSR explicitly stated that in an easing cycle, rate cuts could ‘amplify macro-financial vulnerabilities’ by fuelling ‘riskier forms of lending’. This perceived risk of re-leveraging by resilient households forces the RBA to avoid easing.

- Inflation Data Provides a Public Pretext: The CommBank HSI Index reported a ‘thirteenth straight month of growth’ in household spending. However, CBA’s own chief economist confirmed this strength did not reflect underlying volumes, and was ‘likely being driven partially by price increases’ (inflation) rather than consumption volumes, complicating the RBA’s reading of the economy.

- Monetary Policy Transmission is Diminished: Analysis from the e61 Institute, co-authored by a former RBA senior researcher, confirmed that large household savings buffers have ‘diminished the usual cash flow effects of monetary policy’, making it ‘weaker and slower’ to take effect.

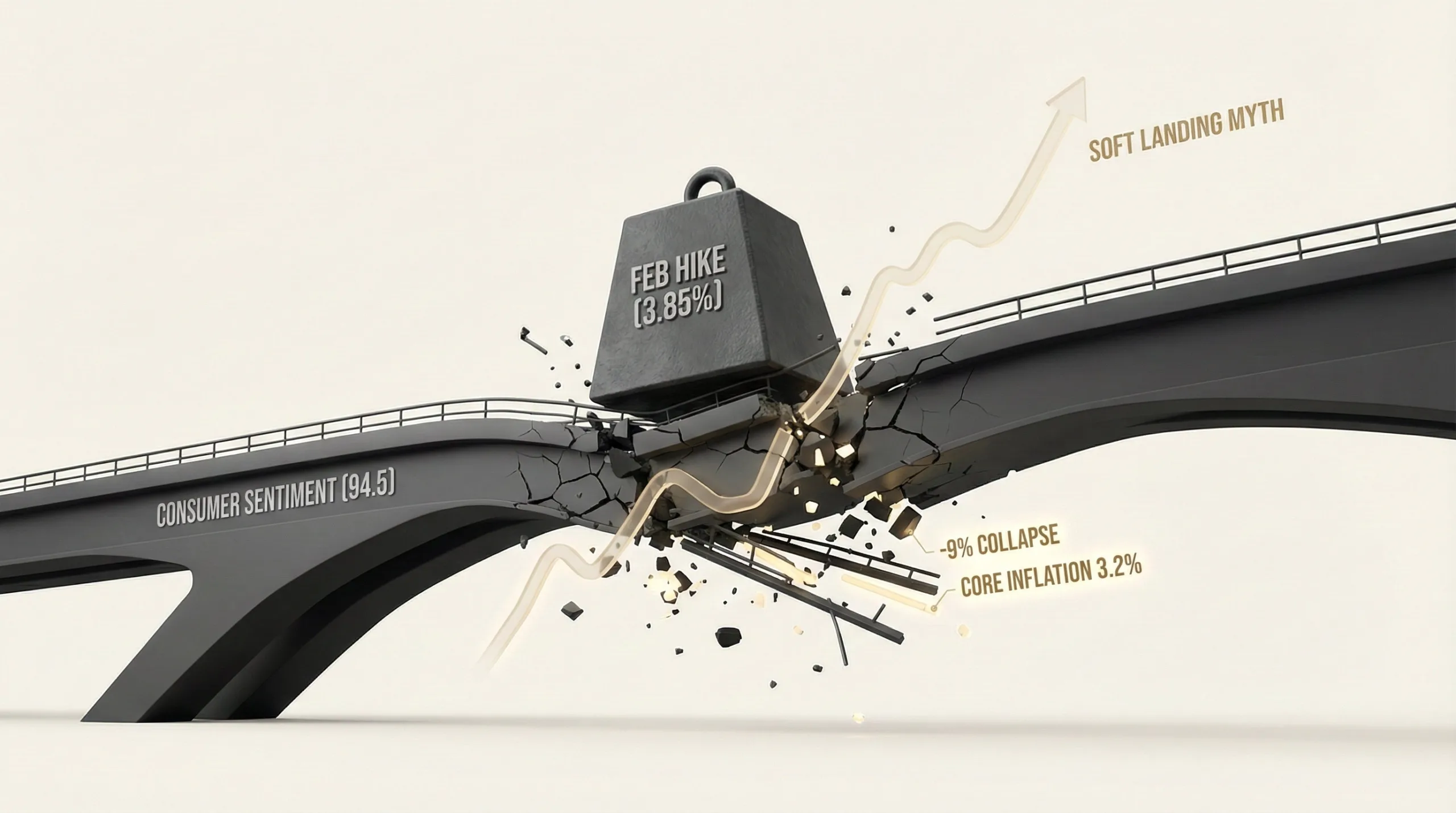

- Market Quantifies the Period of Restrictive Policy: In response to the RBA’s pause and the underlying data, major bank economists (ANZ, NAB) pushed their forecasts for the first rate cut from November 2025 out to February or May 2026, confirming a 6-9 month period of unexpectedly restrictive policy.

Critical Analysis & Balanced View

The core insight from this analysis is the structural policy paradox now facing the Reserve Bank. The RBA is effectively constrained by the very financial stability it sought to engineer. The strength of incumbent household balance sheets has rendered its primary policy tool—the cash rate—an ineffective instrument for providing targeted economic relief. Any attempt to support the ~2% of borrowers in genuine stress would provide a material volume of lower-cost capital to the ‘resilient’ 98%, which the RBA perceives would initiate another speculative valuation premium.

This compels the RBA to adopt a policy of relative constraint: maintaining a restrictive ‘higher-for-longer’ stance. While this policy protects the financial system from the ‘macro-financial vulnerabilities’ of a speculative boom, it comes at a material cost. It reduces market dynamism, entrenches barriers to entry for new participants, and applies financial pressure to households and businesses without large cash buffers. The underlying risk is a policy error; if the aggregate resilience data masks concentrated areas of stress in specific demographics or regions, this prolonged restrictive stance could trigger a more accelerated, segmented downturn than the RBA anticipates.

Strategic Implications for Property Professionals

- For Developers: The extended period of high borrowing costs will widen the Residual Land Value (RLV) Gap, rendering marginal projects unviable and increasing financing risk. Focus on de-risking existing pipelines and securing funding commitments now. Prepare for acquisition opportunities of sites from over-leveraged smaller entities to emerge in mid-to-late 2026.

- For Agents & Buyers’ Agents: The market will bifurcate. A-grade stock held by ‘incumbent’ owners will hold its value, while secondary assets and vendor-constrained properties will face downward price pressure. Client qualification is essential; segment your database into ‘buffered’ (with material liquidity and equity) and ‘constrained’ (reliant on finance) cohorts. The buffered group is your primary addressable market for the next 6-9 months.

- For Investors: The current policy environment explicitly favours existing, well-capitalised portfolios. This is a period for consolidation and optimisation, not serial, leveraged expansion. Stress-test portfolios against a ‘higher-for-longer’ scenario extending to H2 2026 and build liquidity reserves. The primary opportunity will be acquiring quality assets from ‘non-incumbent’ holders who lack financial buffers.

- For Mortgage Brokers: This policy environment complicates serviceability calculations and extends approval timelines. Proactively communicate the ‘higher-for-longer’ reality to clients to manage expectations and prevent deal failure. The strategic focus shifts to helping buffered clients refinance and build liquidity, while preparing pre-approval pipelines for a potential for accelerated growth in new buyer activity once the RBA signals the start of an easing cycle in mid-2026.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core tenets of the APN Sovereign Policy Composite Index™ (SPCI, 24800), demonstrating how a state-level actor’s policy (the RBA’s pause) directly creates predictable market segmentation and accelerates wealth divergence.

- Index Calibration: The APN Social Capital Index™ (24100) is calibrated to recognise that while high aggregate household liquidity is a positive indicator for social stability (Project Bedrock), it can act as a negative feedback loop on monetary policy effectiveness. This ‘Resilience Paradox’ is now weighted as a factor that increases the probability of prolonged, restrictive policy settings.

- Data Capture: This triggers a new data capture mandate for the APN Future Development Pipeline Index™ (24400). The model will now incorporate a 6-9 month delay in expected rate cuts to more accurately calculate the impact on the Residual Land Value (RLV) Gap for projects in pre-construction and financing phases.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.