Catchment Capitalism: How School Zones Became Australia’s Newest Asset Class

APN ANALYSIS: A-260125-AUS135173

Executive Summary

The Australian residential property market has entered a period of structural bifurcation, heralding the emergence of what APN has designated ‘Catchment Capitalism’. As the broader market stagnates under the weight of the 2024-2025 interest rate cycle, a distinct ‘Two-Speed’ economy has formed, driven not by traditional economic levers but by access to high-performance public education. High-performance public school catchment zones have effectively decoupled from the credit cycle, with suburbs like Cherrybrook (NSW) and McKinnon (VIC) recording demand intensity and capital value retention that significantly outperforms their capital city averages. This divergence is a rational capital rotation by upper-middle-class families, triggered by the historic inflation of private school fees, which have been directly exacerbated by Victoria’s 2025 payroll tax reforms. Households are now choosing to arbitrage the materially escalating, non-recoverable cost of private education by capitalising it into a mortgage premium on a catchment-zoned property, transforming a lifestyle expense into a tax-privileged, appreciating asset.

For property professionals, this structural shift redefines asset valuation in key metropolitan enclaves. The ‘education premium’ is no longer a soft preference but a hard, quantifiable financial arbitrage, creating defensive assets with non-traditional demand drivers that are decoupled from the credit cycle. Understanding, pricing, and advising on the risks and opportunities of this regulatory asset, including the elevated risk of ‘Capacity Lockout’ from strict enrolment management plans, is now essential for advising clients on acquisition, valuation, and portfolio strategy in 2026 and beyond.

Background & Strategic Context

This event provides a textbook validation of APN’s core macro-thesis, the APN Sovereign Policy Composite Index™ (SPCI, 24800), demonstrating how state-level fiscal policy, in this case, Victoria’s payroll tax reform, can act as the primary catalyst for re-routing capital flows and creating new asset classes within the residential market. The resulting ‘Catchment Capitalism’ is a direct manifestation of how regulatory changes create distinct cohorts with differing outcomes.

A State-Level Intervention (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The Victorian Government’s removal of the payroll tax exemption for high-fee non-government schools has served as the primary macro-fiscal trigger. This policy directly altered the cost base of the private education sector, necessitating a pass-through of costs that has priced out a significant segment of the market and redirected capital towards public school catchment zones.

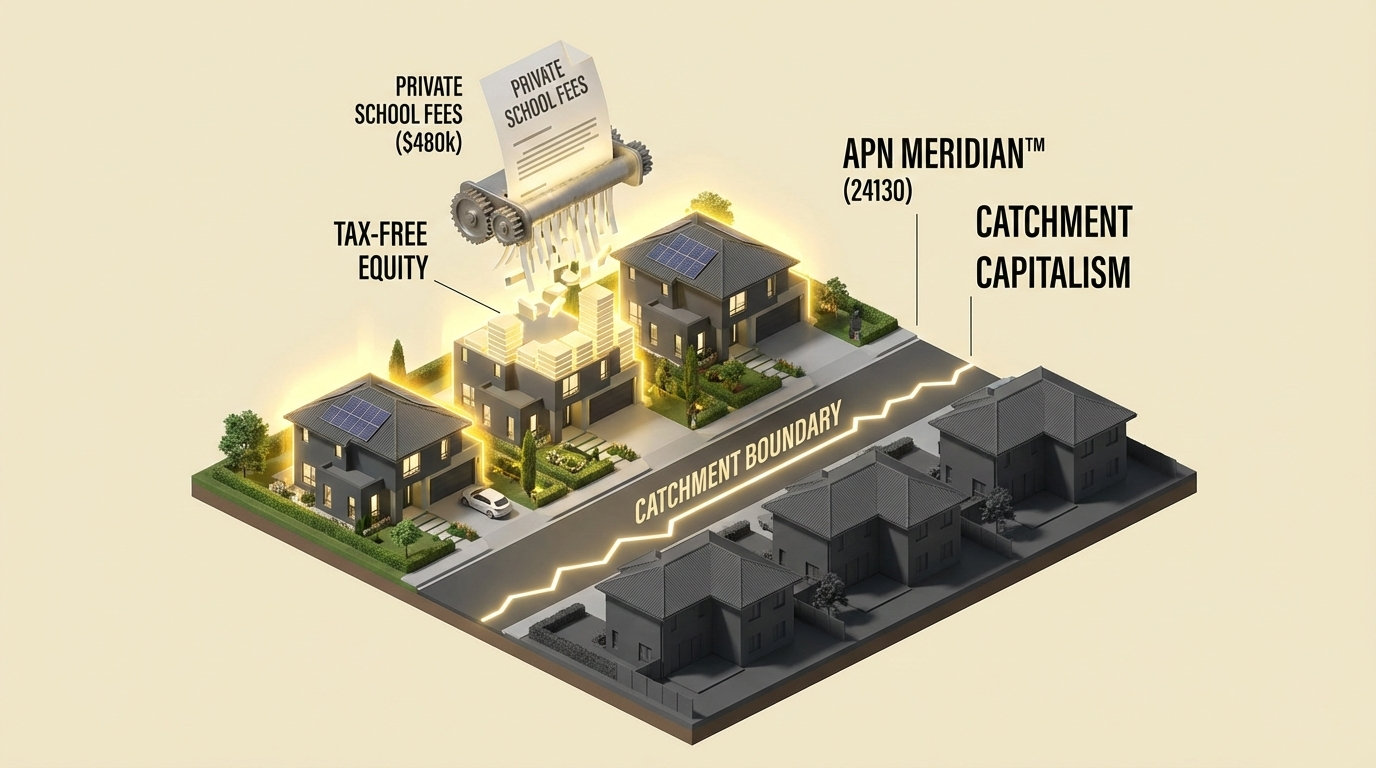

The Capitalisation of Education Value (APN Meridian™): The market is now explicitly pricing the perceived quality and accessibility of Tier 1 public schools. The ‘education premium’ seen in zones like McKinnon and Cherrybrook is a direct capitalisation of the value proposition tracked by our Education Value Index (24130), transforming a public good into a tradable, mortgage-backed asset.

An Amenity & Access Arbitrage (APN Agora™): While the school is the primary driver, the outperformance is amplified by the strong underlying amenity scores of these suburbs. Families are not just buying a school place but a complete ‘life stage’ solution with strong connectivity, retail services, and public spaces, creating a powerful, multi-layered value proposition that our Amenity & Access Index (24140) measures.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of market data and policy impacts for the January 2026 reporting period. The key facts are:

- The Market Bifurcation: A ‘Two-Speed’ property market has emerged. While broader capital city markets show flat or low single-digit growth, specific public school catchments are experiencing accelerated growth.

- The Payroll Tax Trigger: The removal of the payroll tax exemption for many Victorian private schools from 1 July 2024 has led to significant fee hikes of 6-10% (and higher in total costs) for the 2026 academic year, making private education unaffordable for a larger cohort of families.

- The ‘Catchment Premium’ Quantified: The market has assigned a clear monetary value to school zone access. In Cherrybrook (NSW), this has driven a 12.4% increase in the median house price to $2,400,000. In McKinnon (VIC), the premium for an in-zone property remains structurally firm at approximately $240,000 to $300,000 over comparable out-of-zone properties.

- The Financial Arbitrage: Households are making a rational choice to avoid a sunk cost of ~$480,000 in post-tax private school fees for two children. Instead, they are investing in a catchment property, where the ‘cost’ is limited to the interest on the premium (e.g., ~$126,000 over six years), while the principal is preserved as tax-free equity in their main residence.

- The Capacity Lockout Risk: The value of this asset is not guaranteed. Schools at capacity, like Mansfield State High School (QLD), are enforcing strict Enrolment Management Plans (EMPs), creating a risk that a family can buy into a zone but be denied enrolment, negating the premium paid.

Critical Analysis & Balanced View

The phenomenon of ‘Catchment Capitalism’ presents a paradox: the more rational it becomes for an individual family to pursue this strategy, the more fragile and inequitable the system becomes as a whole. High-performing public schools are effectively being privatised by proxy, with the material mortgage premium substituting for the tuition fee. Access is no longer determined by locality in its purest sense, but by the capital capacity to pay a $300,000 entry fee, fundamentally structurally degrading the social contract of public education.

Furthermore, the ‘education premium’ is an inherently fragile asset. Its value is not derived from the land or the dwelling, but from a regulatory line on a map, what APN terms a ‘Codex Structural Adjustment’. This value is exposed to two significant, under-priced risks. The first is administrative risk, or ‘Capacity Lockout’, where a school principal’s interpretation of an EMP can nullify the asset’s utility. The second is legislative risk, where a Department of Education decision to redraw a catchment boundary could rapidly erase hundreds of thousands of dollars in property value. This makes the premium a high-beta asset contingent on bureaucratic discretion, a risk profile that standard valuation models fail to capture.

The third-order consequence is a physical and demographic divergence of the streetscape itself. As capital flows into the ‘in-zone’ side of a boundary street, it fuels a higher velocity of renovation and gentrification. Over time, this creates two distinct communities on the same road, one populated by high-income professionals and the other retaining a more traditional, mixed-income demographic. This deepens social stratification and presents long-term challenges for local government planning and social cohesion.

Strategic Implications for Property Professionals

- For Agents & Buyers’ Agents: Your due diligence process must now include a detailed review of a school’s Enrolment Management Plan (EMP). Simply being ‘in the zone’ is no longer sufficient; you must advise clients on the specific residency requirements, historical enforcement, and the risk of ‘Capacity Lockout’ to protect them from acquiring a non-performing asset.

- For Valuers: Standard hedonic valuation models are no longer structurally viable in these micro-markets. The ‘Education Premium’ must be isolated and quantified as a separate regulatory asset. Valuations must now include a risk assessment based on the school’s capacity and the potential for boundary changes, as this represents a significant, previously unpriced legislative risk to the asset’s value.

- For Developers: The ‘ripple effect’ from saturated Tier 1 zones presents a demonstrable opportunity. Identifying and acquiring sites within ‘Tier 2’ school catchments—those with good reputations and existing capacity—offers significant uplift potential as demand is redirected. Focus on family-friendly townhouse and medium-density projects in zones like Vermont Secondary College (VIC) or Castle Hill High (NSW).

- For Mortgage Brokers & Financial Planners: Clients are no longer just buying a home; they are making a strategic financial decision to arbitrage education costs. Frame the ‘catchment premium’ as a capital investment, not an expense. Model the total cost comparison between private fees (a sunk cost) and the mortgage premium (a capital-preserved investment) to demonstrate the wealth creation and tax advantages of this strategy.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the APN Meridian™ (24130), confirming that the market assigns a quantifiable capital value to educational access. It also validates the APN Sovereign Policy Composite Index™ (SPCI, 24800), as a state-level tax policy is the primary causal driver of the market bifurcation.

- Index Calibration (APN Meridian™): The Education Value Index is recalibrated to increase the weighting of ‘enrolment capacity’ and ‘EMP strictness’ as key risk factors. The index will now differentiate between the ‘Theoretical Premium’ (value based on zone boundary) and the ‘Realised Premium’ (value adjusted for lockout risk).

- Index Calibration (APN RVM™): The Regulatory Velocity Multiplier™ (24210) will be applied to Department of Education boundary reviews and EMP updates. A high RVM™ score on a catchment boundary review will now trigger a ‘Legislative Risk’ flag for properties on the fringe of that zone.

- Data Capture (APN Symbiotic Intelligence Network™): This analysis triggers a new data capture mandate via the Symbiotic Intelligence Network™ (24310) to track agent and buyer sentiment specifically related to EMP enforcement and perceived boundary stability in Tier 1 and Tier 2 school zones.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.