Monetary Policy Tightening Converges with Supply-Side Constraints, Elevating Systemic Friction

APN ANALYSIS: A-260505-AUS139151

This analysis is produced by Australian Property Network, an independent property intelligence platform with no commercial affiliations, no advertiser relationships, and no industry body funding. All findings are derived from verified Tier-1 institutional data sources — principally the Reserve Bank of Australia, the Australian Bureau of Statistics, and the Australian Prudential Regulation Authority — and from certified APN Codex node telemetry. The full institutional research brief for this analysis is published at APN Research.

Executive Summary

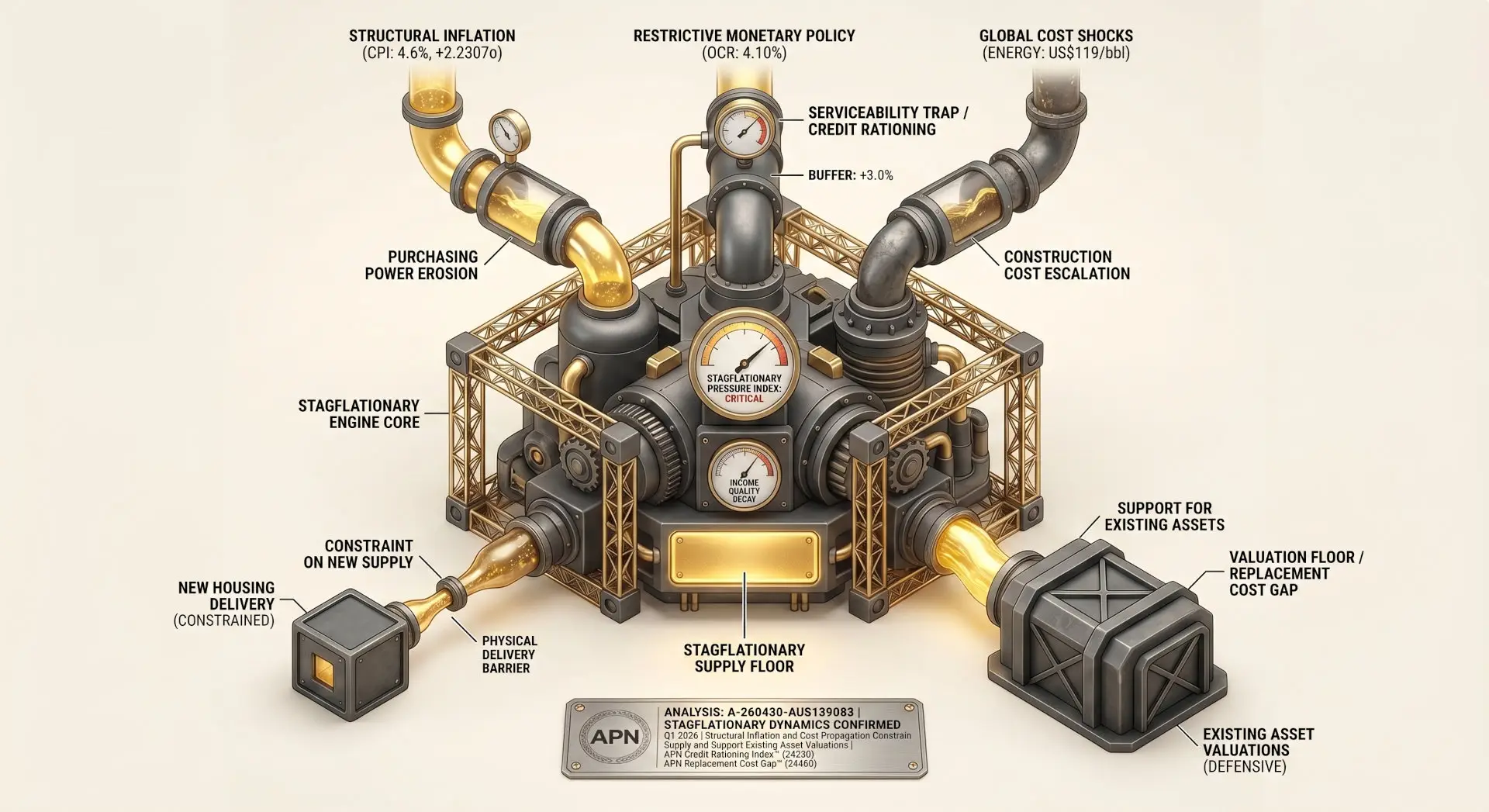

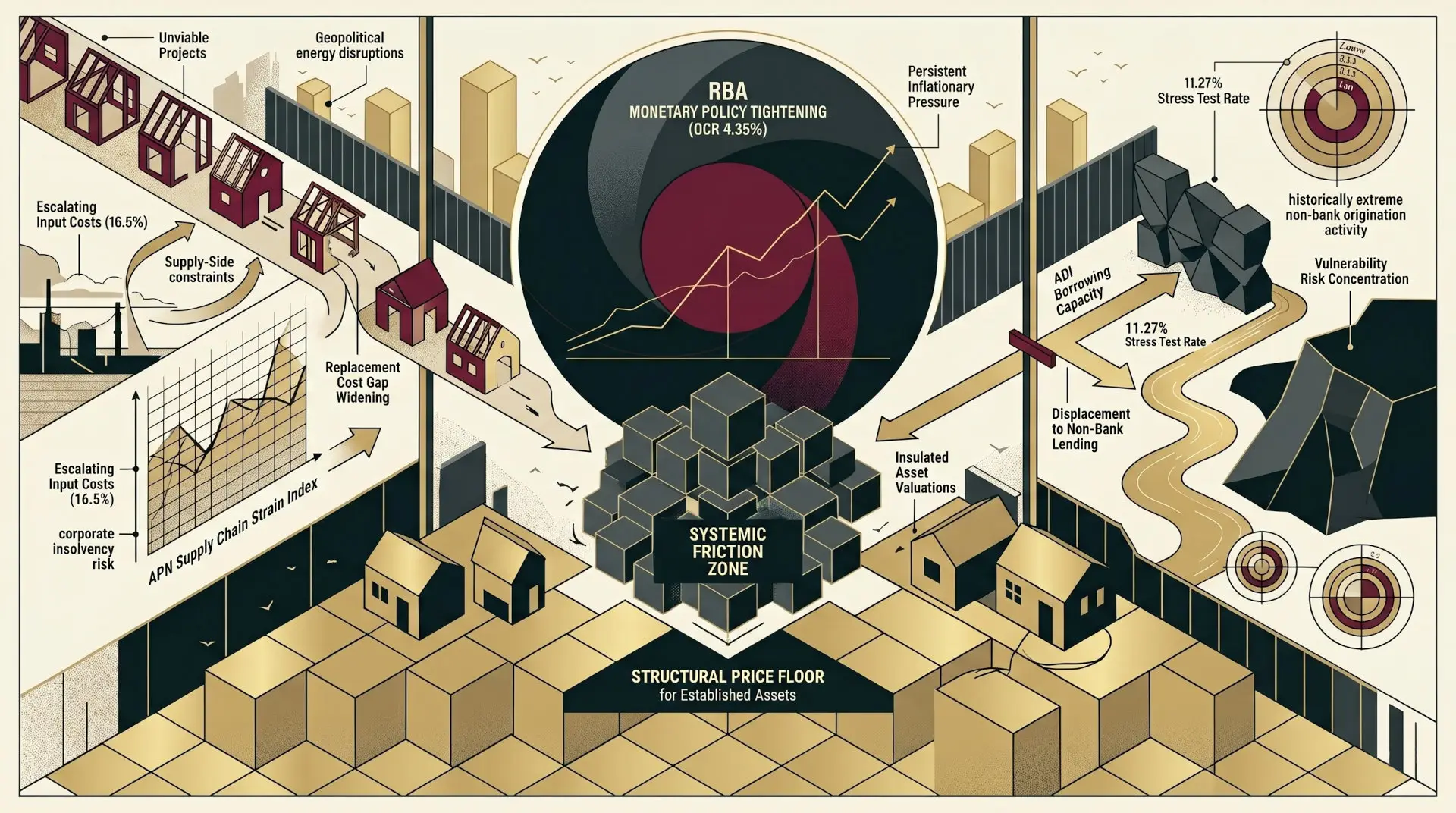

The Reserve Bank of Australia (RBA) has increased the Official Cash Rate (OCR) by 25 basis points to 4.35%, responding to persistent inflationary pressures exacerbated by geopolitical energy disruptions. This adjustment operates within an environment of static macroprudential settings and escalating supply-side cost conditions. The material impact is a dual-front constraint on the property market: a material reduction in borrowing capacity for households and a simultaneous increase in the cost of delivering new housing supply.

The convergence of these factors generates a theoretical mortgage stress test rate of 11.27% within the regulated banking system, structurally excluding a material cohort of prospective buyers and displacing capital demand to the non-bank lending sector, which operates outside the direct APRA supervisory perimeter. Concurrently, escalating material and freight costs are widening the gap between new construction costs and the value of existing properties, rendering many new projects financially unviable. This dynamic constricts the future supply pipeline, creating a structural price floor for established assets even as demand-side serviceability constraints intensify.

This environment requires practitioners to distinguish between markets primarily exposed to serviceability constraints and those insulated by structural supply limitations. Solvency risk within the construction sector and the growing concentration of credit risk in the non-bank lending sector are material analytical considerations for all participants operating in the current environment.

Background & Strategic Context

This analysis contextualises the RBA’s May 2026 decision within the broader structural conditions documented across the APN Codex 21000 Series. The decision is not an isolated event but a catalyst that amplifies pre-existing structural pressures. Its analytical significance lies in how it interacts with these conditions, confirming that the transmission of monetary policy operates through a compound structural architecture rather than as an isolated variable. The convergence of serviceability limits, construction viability gaps, and capital displacement creates a compound system where traditional policy levers produce compound structural effects.

The APN Sovereign Policy Composite Index™ (SPCI) (24800): The impact of the OCR increase is magnified by its interaction with static macroprudential policy. APRA’s 3.0 percentage point serviceability buffer, while fixed, combines with the higher OCR to generate a theoretical 11.27% assessment rate. This interaction, measured by the SPCI, quantifies the cumulative drag on credit availability and transactional velocity originating from the sovereign regulatory architecture.

The APN Replacement Cost Gap™ (24450): Geopolitical energy shocks have translated into a material escalation in construction input costs. This widens the APN Replacement Cost Gap™, which measures the divergence between the cost of constructing a new asset and the market value of an equivalent existing one. As this gap expands, the financial viability of new development contracts, insulating the value of existing assets by making their replacement prohibitively expensive.

The APN Supply Chain Strain Index™ (24430): The combination of rising input costs, elevated holding costs from higher interest rates, and tight labour market conditions creates a margin contraction condition for builders operating under fixed-price contracts. This pressure is a leading indicator of corporate insolvency within the construction sector, threatening to constrict the future housing supply pipeline through project delays and cancellations.

The APN Acute Vulnerability Index™ (24126): The convergence of eroding purchasing power from inflation, reduced borrowing capacity from monetary and macroprudential policy, and rising rental costs from constrained supply places material pressure on lower and median-income households. This index tracks the resulting socio-economic stress, which acts as a leading indicator for demographic displacement and housing insecurity.

Deconstruction of the Source Event

This analysis is based on APN’s assessment of the Reserve Bank of Australia’s Statement on Monetary Policy (5 May 2026) and associated institutional data. The key certified facts are:

- Monetary Policy Adjustment: The RBA increased the Official Cash Rate (OCR) target by 25 basis points to 4.35%.

- Node 21210 Z-Score: Against certified calibration constants (μ = 2.3609%, σ = 1.4535, N = 3,795 daily observations), the 4.35% OCR produces a Node 21210 Z-score of +1.37σ — a meaningfully elevated but not historically extreme cost-of-capital position relative to the 15-year mean.

- Serviceability Assessment Rate: The combination of the 4.35% OCR, an estimated 3.92% institutional margin, and the static 3.0% APRA buffer results in a theoretical mortgage stress test rate of 11.27% for regulated lenders.

- Revised Inflation Outlook: The RBA projects headline CPI inflation to peak at 4.8% in mid-2026. Trimmed mean inflation is forecast to remain above the 2–3% target band until late 2027, indicating a prolonged period of monetary constraint.

- External Inflationary Pressure: Geopolitical disruptions in the Middle East were cited as contributing 0.8 percentage points to Australia’s March 2026 headline inflation of 4.6%, primarily through higher fuel prices.

- Construction Sector Cost Escalation: The energy price shock contributed to a 16.5% material escalation in key inputs, specifically copper and freight, in early 2026, directly affecting construction viability.

- Labour Market Conditions: The labour market continues to operate near systemic capacity, with unemployment at 4.3% (March 2026) and a high employment-to-population ratio of 64.0%. This limits the capacity for productivity gains to offset rising input costs in the construction sector.

Critical Analysis & Balanced View

The primary structural finding of this analysis is the compound interaction between monetary tightening and supply-side cost escalation. While monetary tightening is intended to suppress demand and reduce inflation, its interaction with global supply shocks generates a structural insulating effect for incumbent asset holders. The same inflationary pressures that justify rate increases are simultaneously driving up construction costs. This expands the APN Replacement Cost Gap™ (24450), rendering new development financially unviable in many locations. The resulting supply pipeline attrition establishes a structural price floor beneath existing assets, partially insulating them from the full impact of reduced borrowing capacity. The market is therefore not experiencing a uniform demand-side contraction — it is subject to two structurally opposed conditions operating concurrently, producing divergent conditions between the new supply market and the established asset market.

A further structural implication is the displacement of credit risk. The 11.27% serviceability threshold does not eliminate housing demand; it redirects it. Prospective borrowers who are creditworthy but cannot meet the assessment criteria of regulated Authorised Deposit-taking Institutions (ADIs) are accessing the non-bank lending sector, as measured by APN’s Real-Time Credit Velocity (21270), which recorded a terminal Z-score of +2.761σ at Q4 2025 — a historically extreme level of non-bank origination activity against the certified 6-year baseline — a historically extreme level of non-bank origination activity. While this provides a funding corridor for excluded cohorts, it does so at a higher cost of capital, concentrating financial vulnerability in segments of the market that operate outside the direct APRA supervisory perimeter and are more exposed to future economic shocks.

Strategic Implications for Property Professionals

For Developers: Project feasibility requires reassessment against materially higher input costs and constrained end-buyer financing. Fixed-price contracts carry material risk. Business models with cost flexibility and secured funding lines are better positioned to navigate the current feasibility environment. The viability of projects is now heavily dependent on location-specific supply-demand imbalances.

For Investors: Divergent market conditions are forming. Established properties in areas with high barriers to new supply are insulated by the structural price floor established by the APN Replacement Cost Gap™ (24450). Greenfield and high-supply corridors carry material exposure to serviceability-driven value erosion where the replacement cost floor is absent or narrow.

For Lenders & Brokers: The displacement of capital toward the non-bank sector presents a clear opportunity for participants in that space. However, assessing borrower serviceability outside the APRA regulatory framework necessitates more rigorous, individualised risk assessment to avoid concentrating default risk within non-bank portfolios.

For Valuers & Asset Managers: The elevated Sovereign Friction Coefficient, driven by policy constraints and quantified through the APN Sovereign Policy Composite Index™ (SPCI) (24800), indicates that transactional liquidity will remain suppressed. Valuations must increasingly account for the widening divergence between the cost to build and market value, as this now operates as a primary determinant of price stability for existing assets.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.