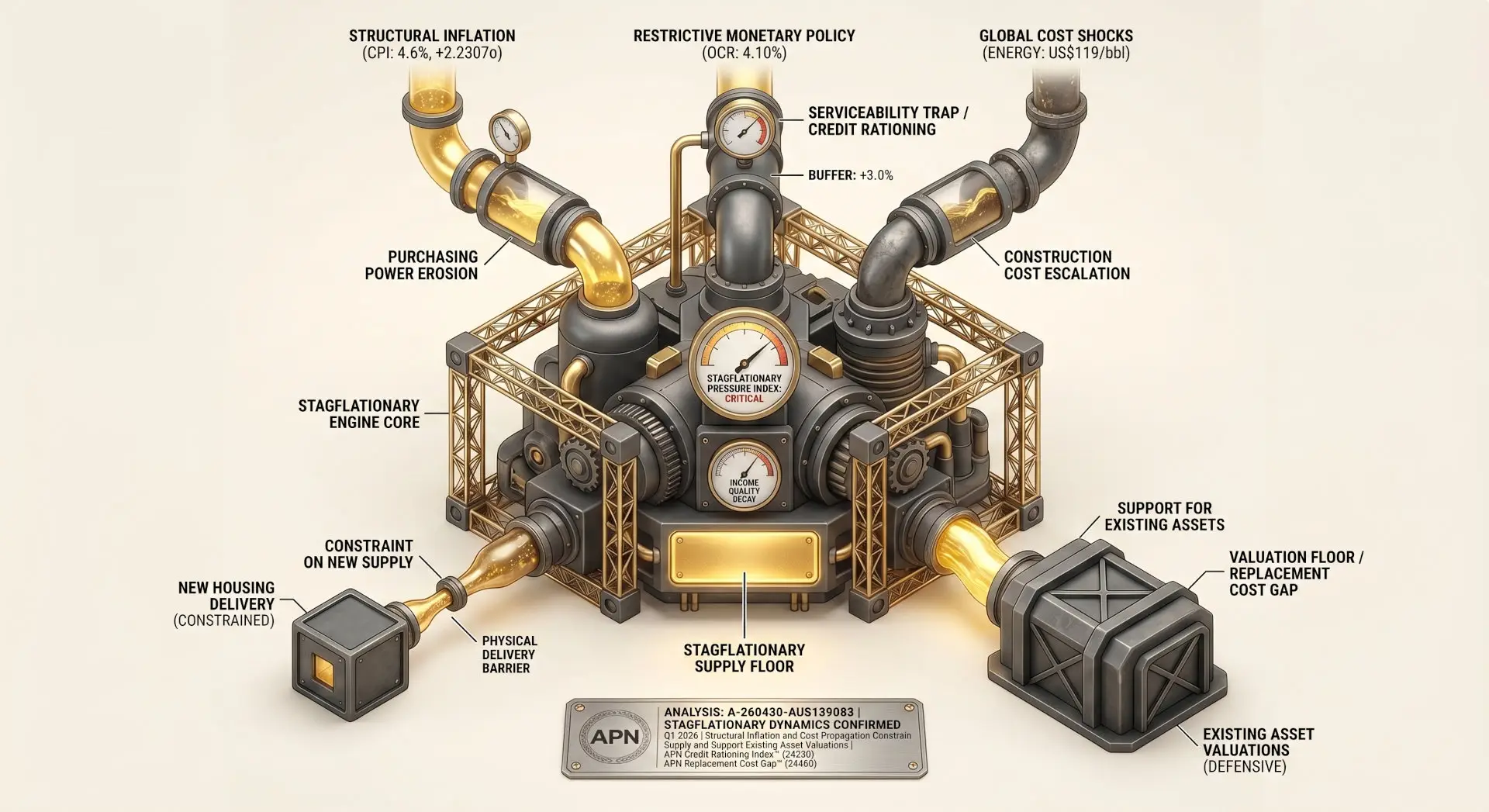

Stagflationary Dynamics Confirmed: Structural Inflation and Cost Propagation Constrain Supply and Support Existing Asset Valuations

APN ANALYSIS: A-260430-AUS139083

Executive Summary

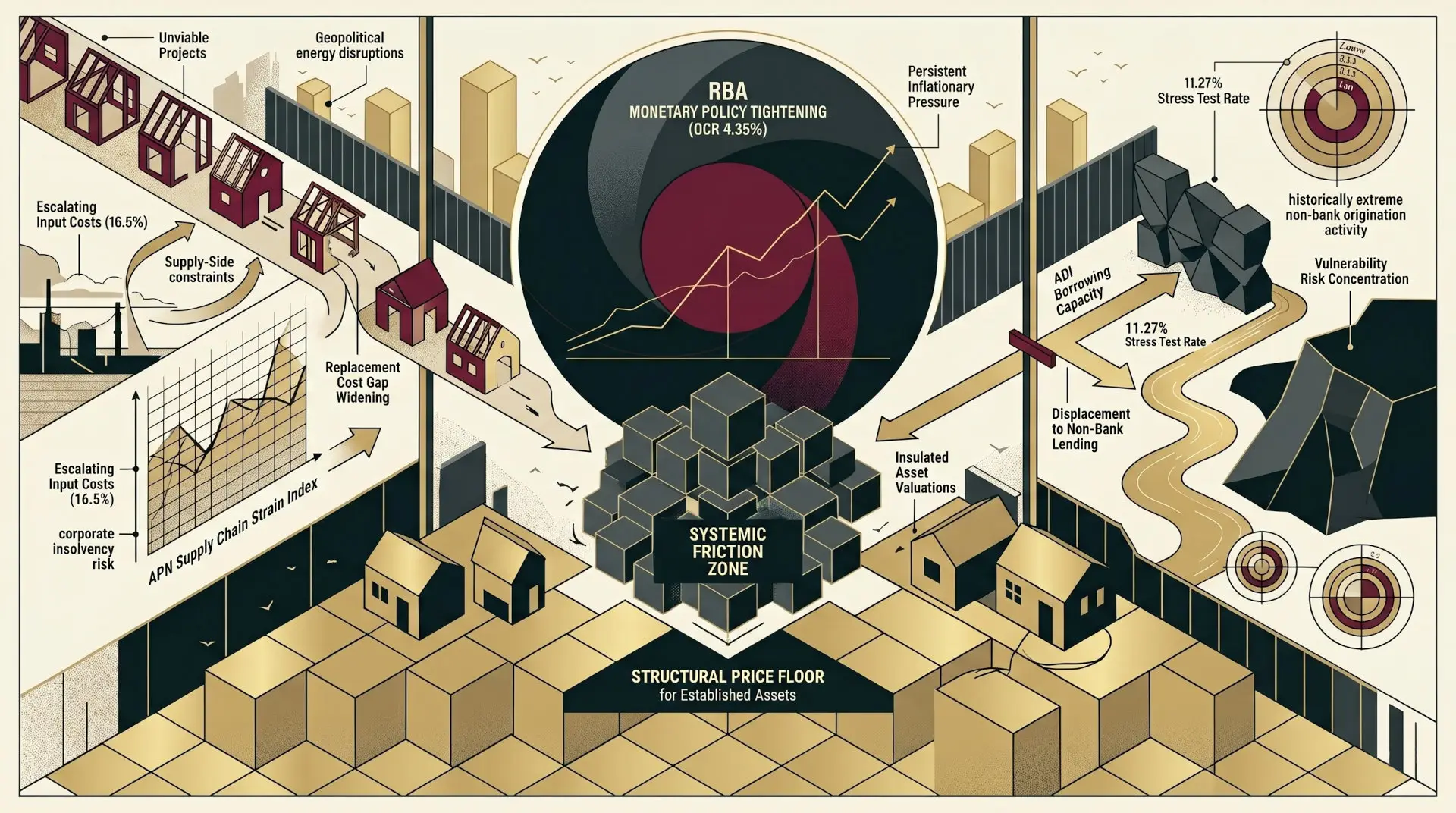

The March Quarter 2026 macroeconomic data confirms a period of elevated structural pressure, defined by a Two Standard Deviation inflation event (4.6% Headline CPI) and a 4.10% Official Cash Rate. This combination of persistent inflation and restrictive monetary policy is driving structural cost propagation through the economy, most notably in the construction sector, where energy price shocks are materially escalating project costs. This dynamic constrains the delivery of new housing supply while simultaneously eroding household purchasing power and tightening credit availability.

For property professionals, this analysis validates the Stagflationary Supply Floor thesis. The widening gap between the cost to construct new dwellings and the value of existing stock establishes a hard floor under asset prices, rendering established properties highly defensive. Concurrently, the ‘Serviceability Trap’—created by the interaction of high inflation with restrictive macroprudential lending rules—will suppress transaction volumes in the regulated sector and displace credit demand toward higher-cost, non-bank channels. Navigating this environment requires a focus on the economic viability of new supply and the bifurcated nature of the credit market.

Background & Strategic Context

This analysis validates and calibrates the APN Stagflationary Supply Floor thesis. The convergence of elevated inflation, rising input costs, and constrained credit availability creates a physical and economic barrier to the generation of new housing supply. This structural constraint insulates the valuation of incumbent assets from the downward pressure typically associated with deteriorating consumer sentiment and constrained household incomes. The March 2026 data provides a clear, empirical confirmation of this dynamic in action.

Persistent Inflationary Pressure (Inflation 21220): The confirmation of a 4.6% Headline CPI print, representing a statistical deviation of +2.2307σ from the 15-year mean, marks a formal Two Standard Deviation Event. This classifies the current inflationary environment as a structural condition rather than a transient cyclical fluctuation, fundamentally altering the baseline assumptions for holding costs and asset yields.

Systemic Cost Propagation (Construction Costs & Supply Chain 21260): The escalation of global energy prices to US$119/bbl is functioning as a non-linear multiplier on construction inputs. The resulting margin erosion on fixed-price contracts is accelerating B2B invoice defaults and creating a physical delivery constraint on new housing, a mechanism tracked via B2B Invoice Default Velocity (21280).

Mechanical Credit Rationing (Banking & Lending Regulation 21350): The persistence of a +3.0 percentage point serviceability buffer, layered on top of a 4.10% OCR and new Debt-to-Income ratio caps, has created a material credit rationing environment. This structurally constrains borrowing capacity for a significant cohort of the market, a dynamic measured by the APN Credit Rationing Index™ (24230).

Degrading Income Quality (Employment & GDP 21230): An unemployment rate of 4.3% masks a compositional decay in the labour market, characterised by a shift from full-time to part-time employment. This trend degrades the organic income growth capacity of households, further pressuring their ability to service debt under elevated inflation and interest rates.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the March Quarter 2026 macroeconomic data release and its interaction with prevailing regulatory settings. The key facts are:

- Inflationary Deviation: Headline CPI registered 4.6%, translating to a Z-score of +2.2307σ against the 15-year baseline, formally constituting a Two Standard Deviation Event. Housing-specific CPI outpaced the headline rate at 6.5%.

- Monetary Policy Stance: The RBA Official Cash Rate was adjusted to, and remains at, 4.10%, establishing a high cost of capital for the domestic credit system.

- Structural Cost Driver: A peak in Brent Crude at US$119/bbl, against a new baseline of US$105/bbl, triggered a material escalation in construction costs exceeding 16.5% for key inputs like copper and freight.

- Credit Assessment Constraint: The combination of the 4.10% OCR, standard bank margins, and the +3.0 percentage point APRA serviceability buffer results in a theoretical mortgage stress test rate approaching 11.02% for new borrowers.

- Labour Market Condition: The 4.3% unemployment rate is analytically classified as compositional decay, reflecting a degradation in the quality and security of employment, which limits household income growth.

Critical Analysis & Balanced View

Two critical second-order insights emerge from this analysis. The first is the paradox of the Serviceability Trap. Macroprudential rules, specifically the +3.0% serviceability buffer, were designed to enhance systemic stability. However, when combined with high inflation and a restrictive OCR, they now function as a primary source of market friction. The mechanism traps financially sound households in existing loan structures by making it mathematically impossible for them to pass serviceability tests for refinancing or upgrading. This suppresses transaction velocity and displaces credit demand toward less-regulated, higher-cost non-bank lenders, shifting systemic risk rather than eliminating it.

The second insight is the structural decoupling of asset prices from consumer sentiment. The Stagflationary Supply Floor thesis is validated by the market’s response to record-low Consumer & Business Sentiment (21640). Ordinarily, such low sentiment would signal downward pressure on prices. Instead, the high and rising cost of new construction, measured by the APN Replacement Cost Gap™ (24450), creates a powerful counter-force. Buyers are transacting not from a position of confidence, but from a rational calculation that the cost to build a new asset is prohibitive. This makes existing stock the only viable option, insulating its value and overriding traditional sentiment-based forecasting models.

Strategic Implications for Property Professionals

- For Developers: The widening APN Replacement Cost Gap™ (24450) renders speculative, fixed-price contracts commercially unviable. Strategic focus must shift to cost-plus models, securing supply chains in advance, or land banking until input cost volatility subsides.

- For Investors: Established residential assets in supply-constrained locations now function as highly defensive holdings. The structural supply floor provides a significant buffer against valuation declines, though rising holding costs will pressure net yields and require active management.

- For Mortgage Brokers & Lenders: The market is bifurcating. Expect continued contraction in the prime ADI mortgage market due to the Serviceability Trap. Material growth opportunities now exist in servicing cohorts displaced to non-bank lenders and structuring complex refinancing solutions for credit-worthy but constrained borrowers.

- For Valuers & Planners: Valuation methodologies must now assign a greater weight to replacement cost as a primary determinant of value, even where it contradicts negative sentiment indicators. Planning frameworks must acknowledge the economic non-viability of delivering affordable supply under the current cost structure, as zoning allowances alone cannot overcome this barrier.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Replacement Cost Gap™ (24450) by demonstrating how elevated construction costs (21260), driven by energy price shocks, create a structural price floor for existing assets.

- Validation: This analysis validates the APN Credit Rationing Index™ (24230) by confirming that suppressed credit velocity is a mechanical consequence of regulatory rule-setting (21350), not a fundamental contraction in borrower demand.

- Index Calibration: The APN Acute Vulnerability Index™ (24126) is calibrated to reflect the simultaneous convergence of all five pressure vectors (Interest Rates, Inflation, Employment, Construction Costs, Sentiment), increasing its sensitivity to demographic displacement signals at the lower quartiles of the market.

- Data Capture: This triggers a new data capture mandate for Real-Time Credit Velocity (21270) to differentiate between ADI and Non-Bank Financial Intermediation flows, allowing for the precise quantification of capital displacement.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.