Structural Decoupling in Australian Property: Professional Sentiment Diverges from Consumer Constraint Amid Policy Intervention

APN ANALYSIS: A-260511-AUS139205

Executive Summary

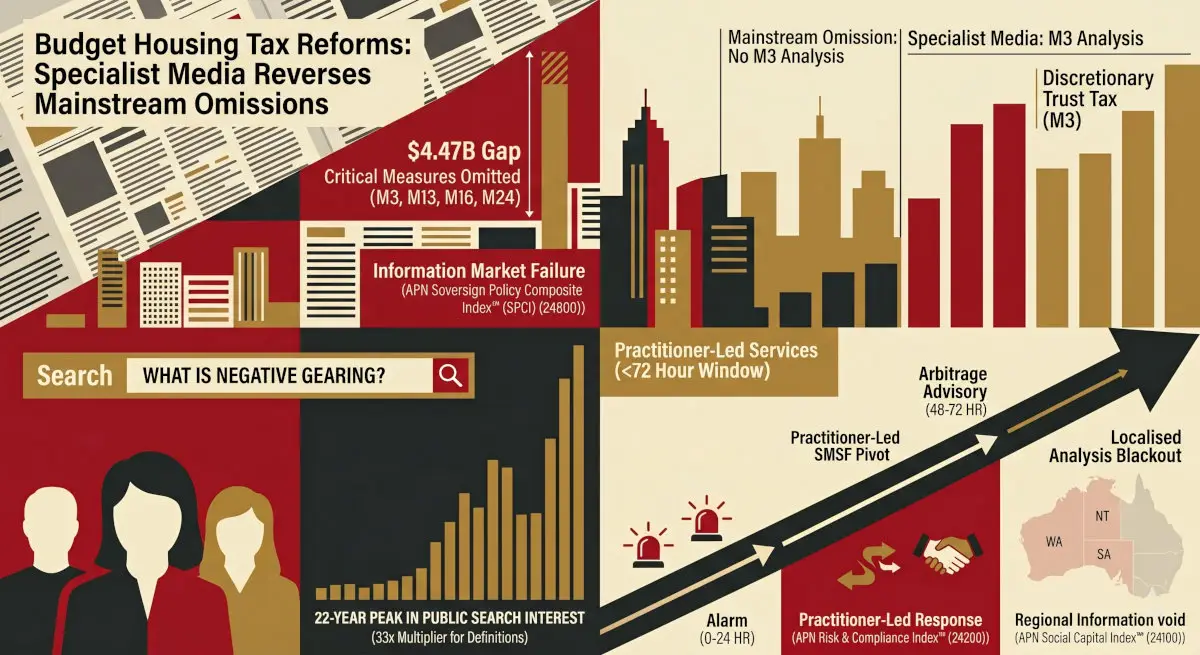

As of May 2026, the Australian property market is defined by a structural decoupling between professional sentiment and consumer capacity. While the ANZ-Roy Morgan Consumer Confidence Index has registered its lowest reading since commencement and the Official Cash Rate sits at a restrictive 4.35%, investment housing credit is expanding at 8.5% year-on-year — its highest trajectory in contemporary data. This divergence is not a cyclical anomaly but a structural condition, sustained by a national housing supply deficit and the ability of equity-rich investors to operate independently of the credit constraints affecting wage-earning consumers. The 2026–27 Federal Budget directly intervenes into this environment, with measures targeting negative gearing, capital gains tax, and housing support schemes generating distinct sentiment responses across state jurisdictions.

For property professionals, this national decoupling translates into three distinct state-level operating environments. Queensland exhibits a rationally bullish posture, underpinned by demographic capacity and supply deficits. New South Wales presents an asymmetric market, bifurcated between optimistic professionals servicing high-equity investors and defensive practitioners in mortgage-belt corridors. Victoria functions as a structural outlier, with a defensive professional sentiment shaped by a unique combination of state fiscal friction, localised socio-economic vulnerability, and a perceived amenity discount in its capital core. Navigating these divergent state-level fundamentals is now critical for effective capital allocation, risk management, and service delivery across the national property ecosystem.

Background & Strategic Context

This analysis validates and calibrates APN’s core ‘Asset-Wage Divergence’ macro-thesis. This thesis posits that as physical asset values escalate at a rate materially exceeding nominal wage growth, capital flows progressively decouple from the macroeconomic constraints binding the median wage-earning consumer. The May 2026 market condition provides a clear empirical demonstration of this construct, where professional sentiment, driven by equity-backed capital, operates on a fundamentally different plane from consumer sentiment, which is anchored to wage-based borrowing capacity. The event is analytically significant as it quantifies the magnitude of this divergence at the convergence point of restrictive monetary policy and targeted federal fiscal intervention.

Structural Decoupling Signal (APN Professional Sentiment Index™ 24300): The gap between the operational optimism of property professionals—evidenced by the 8.5% growth in investor credit—and the empirical constraint on consumers—evidenced by record-low confidence and a 4.35% OCR—has reached a historically anomalous magnitude. This is not a cyclical variation but a structural discontinuity in market behaviour.

State-Level Fiscal Friction (APN Risk & Compliance Index™ 24200): Victoria’s elevated property tax burden, including a Windfall Gains Tax and augmented land tax thresholds, is generating documented regulatory friction. This acts as a material suppressor on development viability and investor sentiment, creating a clear point of differentiation from the less onerous fiscal environments in Queensland and New South Wales and driving capital reallocation.

Localised Vulnerability Convergence (APN Acute Vulnerability Index™ 24126): The formal invocation of this index for the Melbourne West SA4 demonstrates how national macroeconomic pressures are concentrating into specific geographic pockets of stress. The convergence of elevated unemployment, constrained housing delivery, and high mortgage stress in outer-suburban corridors creates a localised risk profile that is not apparent in national-level data.

Amenity Perception Discount (APN Sentinel™ 24120): The invocation of this index for the Melbourne City SA4 confirms that non-financial factors, such as the sustained media and political salience of public safety, can generate a measurable amenity discount. This impacts asset values and capital allocation independently of traditional credit or fiscal drivers, highlighting a more complex valuation landscape.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of institutional data, proprietary indices, and federal policy announcements as of May 2026. The key facts are:

- Credit Market Divergence: Investment housing credit recorded an 8.5% year-on-year expansion as of March 2026, the highest in contemporary APRA data, despite the Reserve Bank of Australia lifting the Official Cash Rate to 4.35% in May 2026.

- Consumer Sentiment Contraction: The ANZ-Roy Morgan Consumer Confidence Index registered 63.1 in March 2026, its lowest reading since the index began in 1972, directly following an OCR increase.

- Federal Budget Intervention: The 2026–27 Federal Budget confirms structural changes, including restricting negative gearing deductions to new builds (with grandfathering), transitioning the CGT discount to an indexation model, and launching the ‘Help to Buy’ shared equity scheme.

- Jurisdictional Divergence: Professional sentiment varies materially by state. Queensland is characterised by bullish decoupling, New South Wales by asymmetric decoupling, and Victoria by defensive convergence, each reflecting rational responses to distinct local fundamentals.

- Structural Supply Deficit: A projected 204,000-dwelling shortfall against the National Housing Accord’s 1.2 million home target by 2029, coupled with a 48.6% increase in construction costs since 2020, underpins secondary market asset values.

Critical Analysis & Balanced View

The primary second-order insight is the rationality of the observed sentiment divergence. The decoupling measured by the APN Professional Sentiment Index™ (24300) is not evidence of sentiment operating beyond rational empirical bounds among property professionals. Rather, it is a logical reflection of a bifurcated market. Practitioners are accurately responding to the segment of the market that remains liquid and active: incumbent asset holders and investors with significant equity reserves who are insulated from the serviceability constraints binding wage-dependent borrowers. This cohort is driving the 8.5% expansion in investor credit. Professional optimism is therefore an accurate pricing of where capital is flowing, validating the ‘Asset-Wage Divergence’ construct where market activity has structurally detached from the median consumer’s economic reality.

A further critical insight is the ‘Triple-Suppressor Mechanism’ unique to Victoria, which explains its structural underperformance. This is not a simple cyclical downturn but the result of three distinct, non-overlapping pressures. First, state-level fiscal friction, measured by the APN Risk & Compliance Index™ (24200), applies systemic yield compression across the entire jurisdiction. Second, the convergence of localised socio-economic stress in outer-suburban mortgage belts, formally invoked via the APN Acute Vulnerability Index™ (24126) in Melbourne West, creates a geographic pressure point. Third, a crime perception amenity discount in the metropolitan core, invoked via the APN Sentinel™ (24120) in Melbourne City, degrades value independently of fiscal or credit factors. The concurrent operation of these three suppressors provides a rational basis for the defensive sentiment and capital reallocation observed among Victorian property professionals.

Strategic Implications for Property Professionals

- For Capital Allocators & Investors: The pronounced interstate divergence signals a clear opportunity for jurisdictional arbitrage. A data-grounded assessment is required to weigh the structural tailwinds in Queensland against the high-friction environment in Victoria and the asymmetric, high-cost market in New South Wales.

- For Development Professionals: The Federal Budget’s focus on new-build negative gearing and build-to-rent incentives provides a strong policy signal. However, this must be assessed against state-level supply chain constraints and the ‘Replacement Cost Floor’, where high construction costs make new builds unviable below existing market prices, favouring institutional-scale projects.

- For Mortgage Brokers & Financial Advisors: The market has bifurcated into two distinct client streams. One segment, concentrated in mortgage-belt corridors, requires sophisticated advice on debt restructuring and delinquency mitigation. The other, comprising equity-rich investors, requires strategic guidance on acquisition, portfolio optimisation, and navigating the new CGT landscape.

- For Valuers & Asset Managers: The formal invocation of the APN Sentinel™ (24120) and APN Acute Vulnerability Index™ (24126) confirms that non-financial and hyper-localised factors are now quantifiable pricing risks. Valuations in affected zones must now incorporate specific discounts for perceived amenity and concentrated socio-economic stress to remain accurate.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Professional Sentiment Index™ (24300) by demonstrating a quantifiable, historically anomalous decoupling between the professional optimism driven by investor credit and the material constraint on consumer capacity.

- Validation: This analysis validates the APN Risk & Compliance Index™ (24200) by evidencing how Victoria’s state-based fiscal interventions are functioning as a material suppressor on investment sentiment and a direct driver of interstate capital reallocation.

- Index Calibration: The APN Acute Vulnerability Index™ (24126) is formally invoked for the Melbourne West SA4. The index is calibrated to the evidenced convergence of elevated local unemployment (5.2%), constrained housing delivery, and concentrated mortgage stress in this specific geographic corridor.

- Index Calibration: The APN Sentinel™ (24120) is formally invoked for the Melbourne City SA4. The index is calibrated to the measurable amenity discount driven by a sustained negative perception of public safety, which is impacting capital allocation and asset values independently of fiscal or credit factors.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.