Capital Realignment: Forced Sale of Permitted Sites Presents a Strategic Acquisition Window

APN ANALYSIS: A-260205-AUS136758

Executive Summary

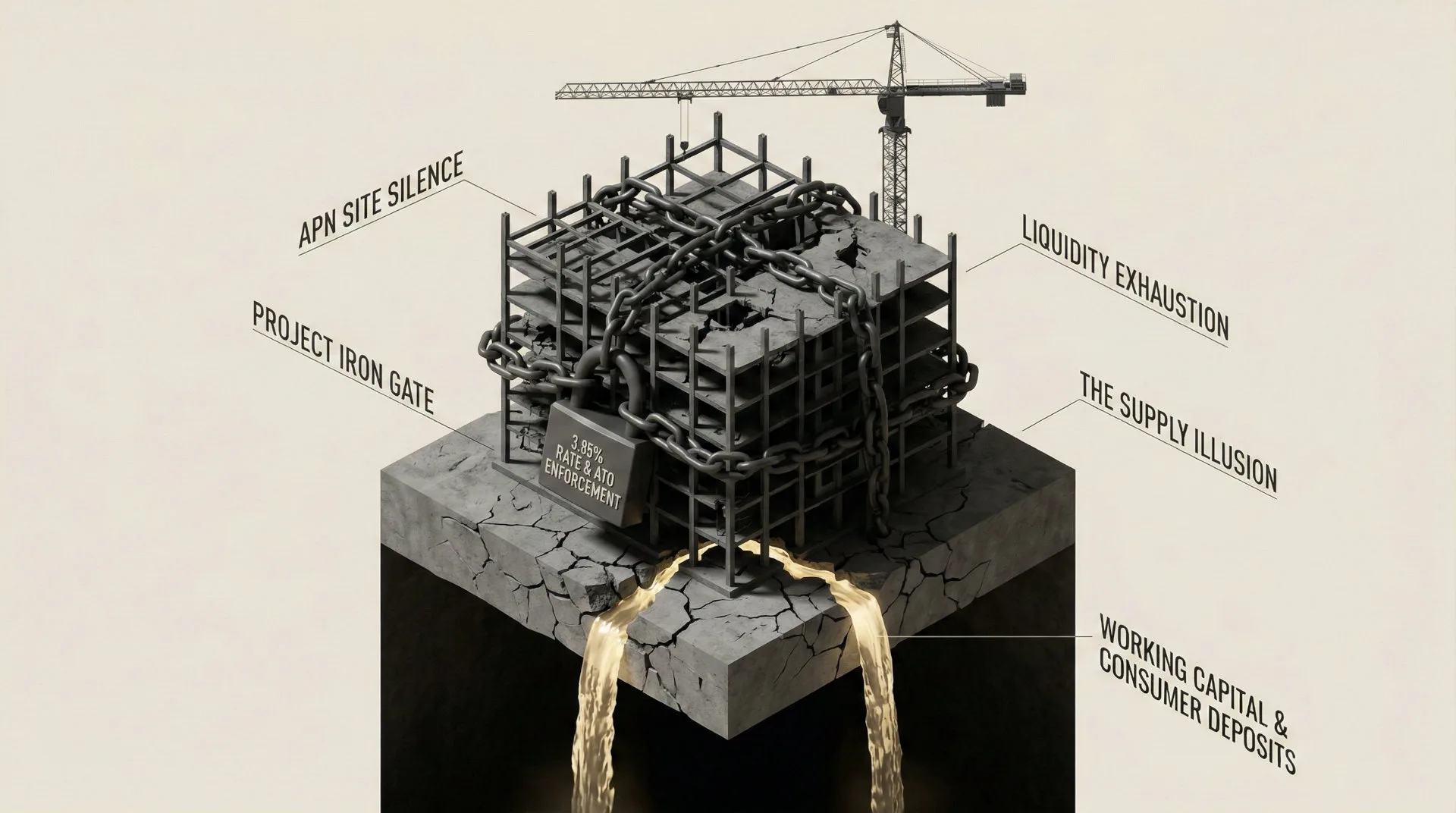

The Australian residential development sector has entered a sustained phase of capital realignment, a structural correction driven by unsustainable holding costs. The February 2026 RBA cash rate hike to 3.85% has acted as a primary catalyst, shifting the source of developer pressure from input cost volatility to a material increase in debt servicing pressure. This has pushed mezzanine finance rates for mid-tier developers to 14-22%, with risk-adjusted tranches frequently breaching the 20% threshold, causing a 24% increase in debt servicing costs. Consequently, the APN Residual Land Value (RLV) Gap™, the disparity between a vendor’s book value and a developer’s ability to pay, has structurally adjusted, forcing the liquidation of fully permitted, ‘shovel-ready’ development sites.

For property professionals, this is not a cyclical downturn but a structural reset of the development market. The forced sale of permitted sites signifies the material deterioration of the mid-tier developer capital stack, creating a finite acquisition window for well-capitalised investors, funds, and institutional players. The appearance of ‘Mortgagee in Possession’ sales confirms the price reset is underway, allowing for the acquisition of de-risked assets at a significant discount to 2024 valuations. The concurrent 29.8% contraction in multi-unit approvals guarantees a material supply deficit in 2027-28, creating ideal market conditions for projects acquired today.

Background & Strategic Context

This market event validates and calibrates APN’s core theses on market intervention and capital flow, demonstrating how monetary policy, as measured by the APN Sovereign Policy Composite Index™ (SPCI, 24800), can be deployed as an instrument on the cost of capital and induce structural attrition in the development pipeline. The forced sale of permitted sites is the physical manifestation of a structural pressure point within the mid-tier development sector, driven by a confluence of factors that our frameworks are designed to track.

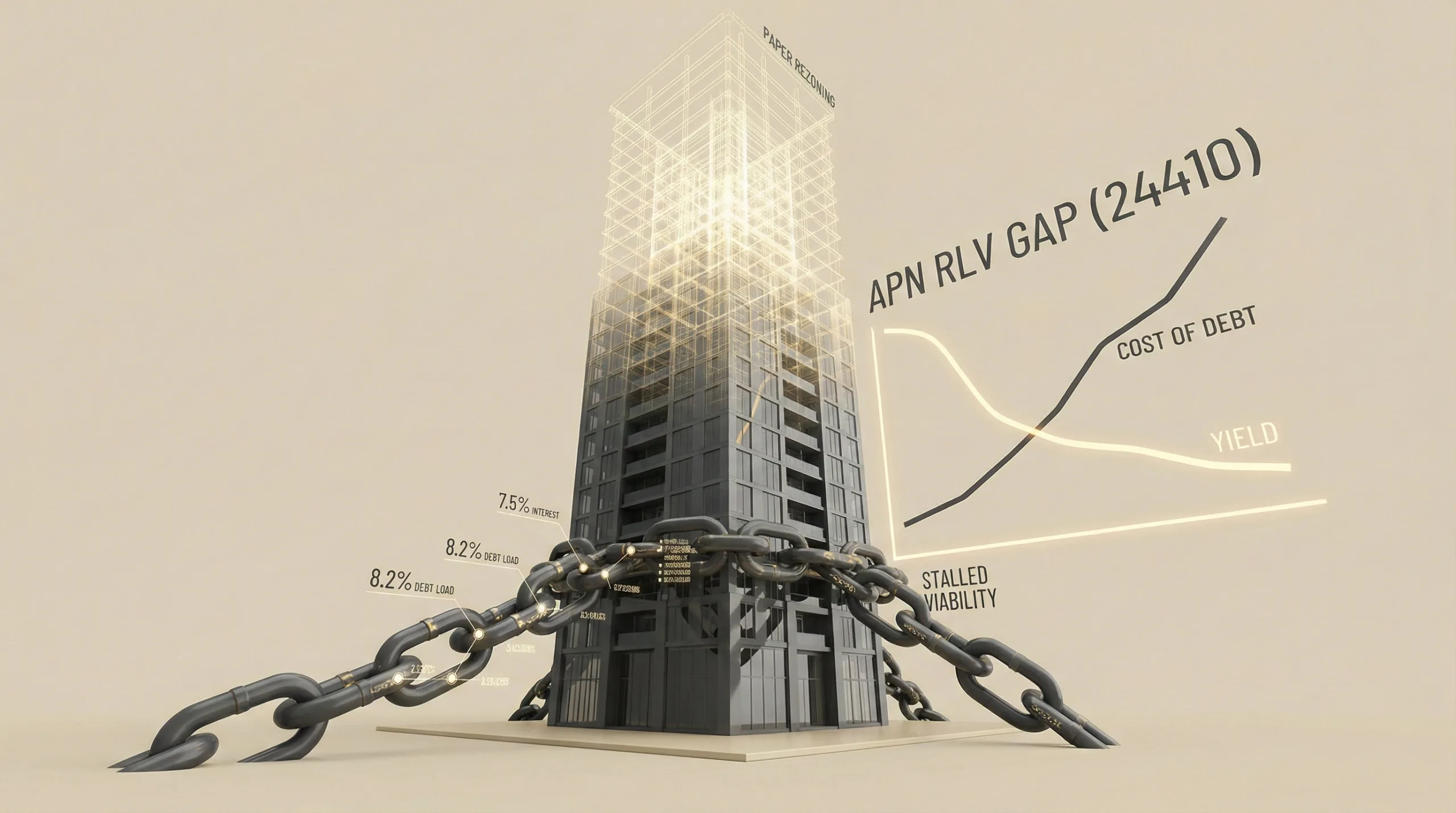

The Widening Viability Chasm (APN Residual Land Value (RLV) Gap™): The RBA’s rate hike has been deployed as an instrument to influence the ‘Finance Costs’ variable in the RLV calculation. This has not merely compressed the residual land value; for highly leveraged assets, it has pushed it into negative territory. The resulting gap between vendor expectations and developer capacity is now being resolved not by negotiation, but by foreclosure, as confirmed by mortgagee sales.

The Capital Access Decoupling (Project Iron Gate): While Project Iron Gate primarily focuses on retail credit, its principles are clearly visible here. The ‘Mezzanine Spike’ to 14-16% acts as a commercial ‘Iron Gate’, decoupling mid-tier developers from the viable capital needed to hold assets. This enforces a materially adverse ‘cashflow-primary’ environment, where a strong balance sheet, not just a viable project, is the key to operational continuity.

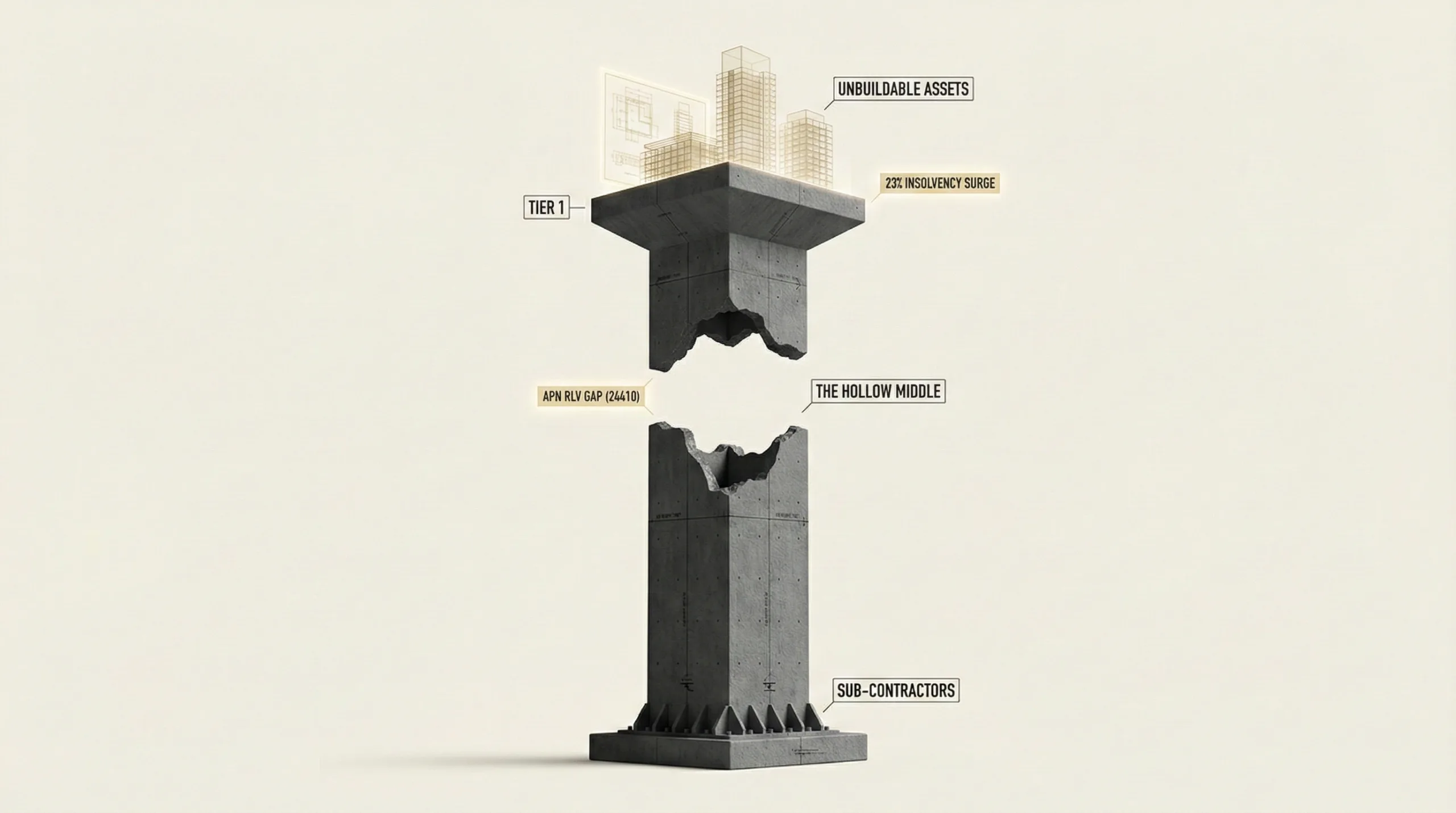

The Phantom Pipeline Manifests (APN Future Development Pipeline Index™): The 29.8% contraction in multi-unit approvals is the statistical confirmation of this index’s core function, filtering economically unviable ‘Paper Rezonings’ from the genuine supply pipeline. The material increase in debt servicing pressure has turned a vast swathe of the theoretical future supply pipeline into economically unviable projects, as they become financially unfeasible before construction commences.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of Australian Bureau of Statistics (ABS) data, RBA statements, and live distressed asset listings from February 2026. The key facts are:

- The RBA Trigger: The Reserve Bank of Australia lifted the official cash rate by 25 basis points to 3.85% on 3 February 2026, citing persistent inflation. This contradicted market expectations for a policy pivot and rendered the ‘hold until 2025’ strategy financially unviable for many developers.

- The Approvals Decline: National approvals for ‘private sector dwellings excluding houses’ (apartments and townhouses) contracted by 29.8% in December 2025. Victoria recorded 3,514 total approvals in December 2025, a 32.2% monthly decline that represents the state’s lowest recorded level since June 2013.

- The Debt Servicing Pressure: The cost of mezzanine finance and preferred equity, which is structurally important for mid-tier developers, has increased to the 14-16% per annum range. This represents a circa 24% increase in holding costs for a typical leveraged land bank, making it mathematically unsustainable.

- The Asset Liquidation: ‘Mortgagee in Possession’ sales of permit-approved sites, such as the 68-lot subdivision in Rockbank, have appeared on the market. Concurrently, institutional players like Mirvac have confirmed acquiring similar de-risked sites’ at a discount to the vendor’s carrying value.

Critical Analysis & Balanced View

The central paradox of the 2026 market is that just as construction feasibility improves with stabilised input costs, financial feasibility has materially contracted. The very policy tool used to address the 2022-24 supply chain inflation—rate hikes—has induced a new structural pressure point in the capital stack. This represents not a structural planning deficit, but a structural financing constraint. The market has bifurcated into two distinct camps: the distressed mid-tier, burdened by high-cost project finance, and the opportunistic institutional tier, which is leveraging its superior balance sheet and lower cost of capital to consolidate assets. This counter-cyclical consolidation aggregates fragmented, distressed land holdings into large, institutional-grade portfolios. The latent risk for acquirers is timing; however, the structurally significant contraction in the approvals pipeline provides a clear, data-backed timeline for a future supply deficit, significantly de-risking the medium-term hold for those who can enter the market now.

Strategic Implications for Property Professionals

- For Developers & Private Equity: The acquisition window for de-risked, permit-approved sites is now open. Identify assets held by distressed mid-tier players and focus negotiations on the unsustainable holding costs as the primary lever. Prioritise ‘shovel-ready’ assets where planning risk is eliminated and avoid raw land until the cost of capital stabilises.

- For Lenders & Financiers: Immediately stress-test loan books exposed to mid-tier developer land banks. Expect an increase in loan-to-value (LVR) covenant breaches as valuers begin pricing in mortgagee sale comparables. An opportunity exists for specialist distressed debt funds to provide rescue finance or acquire loan tranches at a discount.

- For Valuers & Consultants: The primary valuation benchmark has shifted. Historical sales data is now less relevant than distressed listings and mortgagee sales. The APN RLV Gap™ is the forward-looking metric of elevated importance; valuations must now be heavily weighted towards a project’s mathematically derived RLV based on current finance costs, not historical vendor expectations.

- For Agents & Buyers’ Agents: A new client category is emerging: institutional counter-cyclical capital seeking distressed assets. Position your deal flow to service these cash-rich, decisive buyers. For residential clients, explain that the current development halt guarantees a concentrated housing deficit in 2027-28, underpinning medium-term price growth for established stock.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the APN Residual Land Value (RLV) Gap™ (24410), demonstrating its shift from a theoretical constraint to the primary mechanism of structural market adjustment. It also validates the application of the APN Credit Rationing Index™ (24230) in the commercial development space via the ‘Mezzanine Spike’.

- Index Calibration: The APN Future Development Pipeline Index™ (24400) is recalibrated to reflect the 29.8% contraction in multi-unit approvals, significantly increasing the ‘economic friction filter’ for projects requiring mezzanine debt. The calculated 24.2% increase in holding costs becomes a new input variable for assessing project viability.

- Data Capture: This triggers a new data capture mandate to systematically track and categorise ‘Mortgagee in Possession’ and ‘Receiver Appointed’ listings for development sites nationally. This data will now feed directly into the real-time calibration of the APN RLV Gap™, providing a real-time indicator of market pressure.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.