Site Silence: The Structural Contraction of Australia’s Mid-Tier Construction Sector

APN ANALYSIS: A-260226-AUS137722

Executive Summary

The Australian mid-tier residential construction sector is experiencing a state of structural contraction, not a cyclical downturn. A sustained liquidity constraint, catalysed by the Reserve Bank of Australia’s February 2026 cash rate hike to 3.85%, has converged with hyper-inflated material costs, the systemic withdrawal of trade credit insurance, and a substantive ATO debt recovery campaign. This has materially deteriorated the financial viability of the high-volume, low-margin builders who form the core of the nation’s housing supply pipeline, triggering an industry-wide ‘Site Silence’ phase.

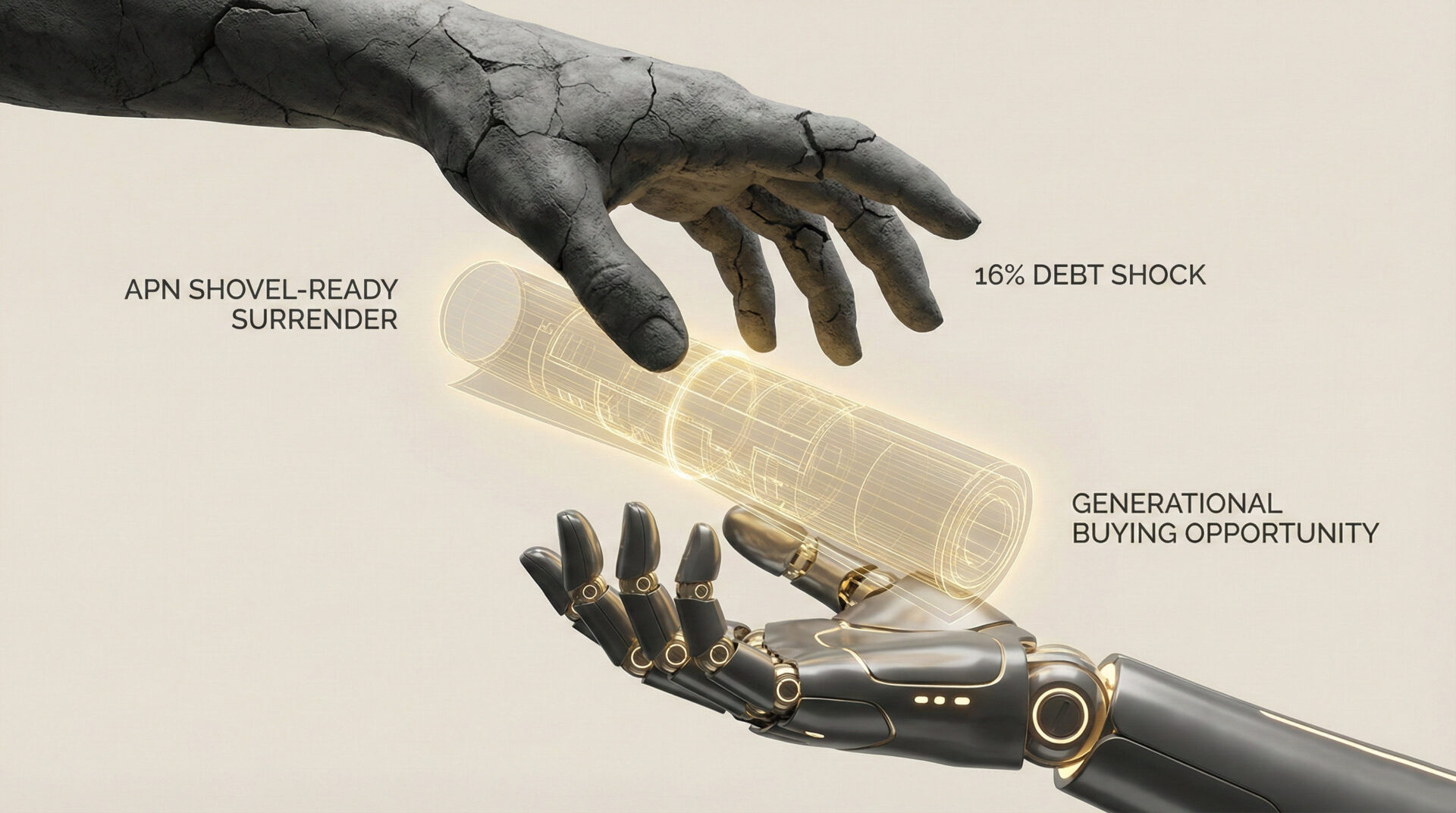

For property professionals, this marks the end of the speculative, high-leverage development model that has defined the last decade. The analysis indicates that project viability can no longer be assumed, and counterparty risk—specifically builder solvency—has superseded all other variables in project due diligence. The market’s foundational risk profile has inverted, shifting from the contractor’s corporate balance sheet to the consumer’s unsecured capital. The risk of total deposit loss for off-the-plan buyers is now systemic, not isolated, fundamentally altering the conditions of engagement for developers, lenders, and buyers alike.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses, particularly The Supply Illusion and The Glass House (Net State Position™). The sustained contraction of the mid-tier construction sector provides empirical evidence that government housing targets are disconnected from physical delivery capacity and that the market’s financial architecture structurally transfers risk from corporate ‘Extractors’ to consumer ‘Hosts’. The convergence of multiple distress vectors has materially deteriorated the notional solvency upon which the mid-market development model was built.

Defining the Paradox (The Supply Illusion): The divergence between government policy, targeting 1.2 million new homes, and the physical reality of a contracting delivery pipeline has never been wider. This analysis indicates that approvals on paper do not translate to physical assets when the entities contracted to build them are insolvent, rendering state and federal housing targets mathematically impossible to achieve.

Mapping the Vulnerability (The Glass House (Net State Position™)): The structural pressure point illustrates the structurally sensitive dependency between the Tier 2 Extractors (mid-tier builders) and the Tier 4 Hosts (off-the-plan buyers). The financial contraction of the Extractors, under the weight of macroeconomic pressures, directly and materially deteriorates the Hosts’ financial security, whose deposits are predicated on the builder’s now-notional solvency.

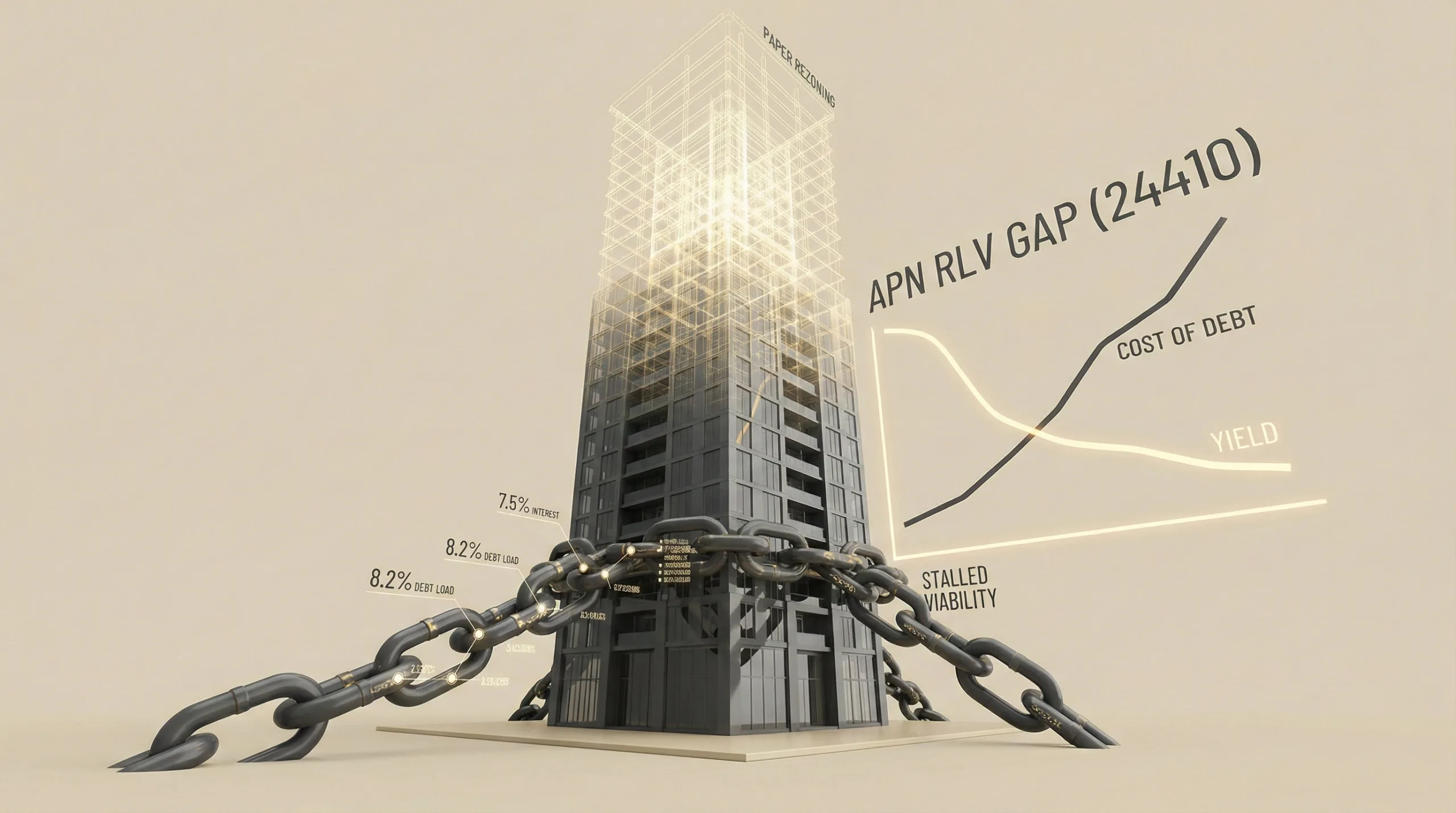

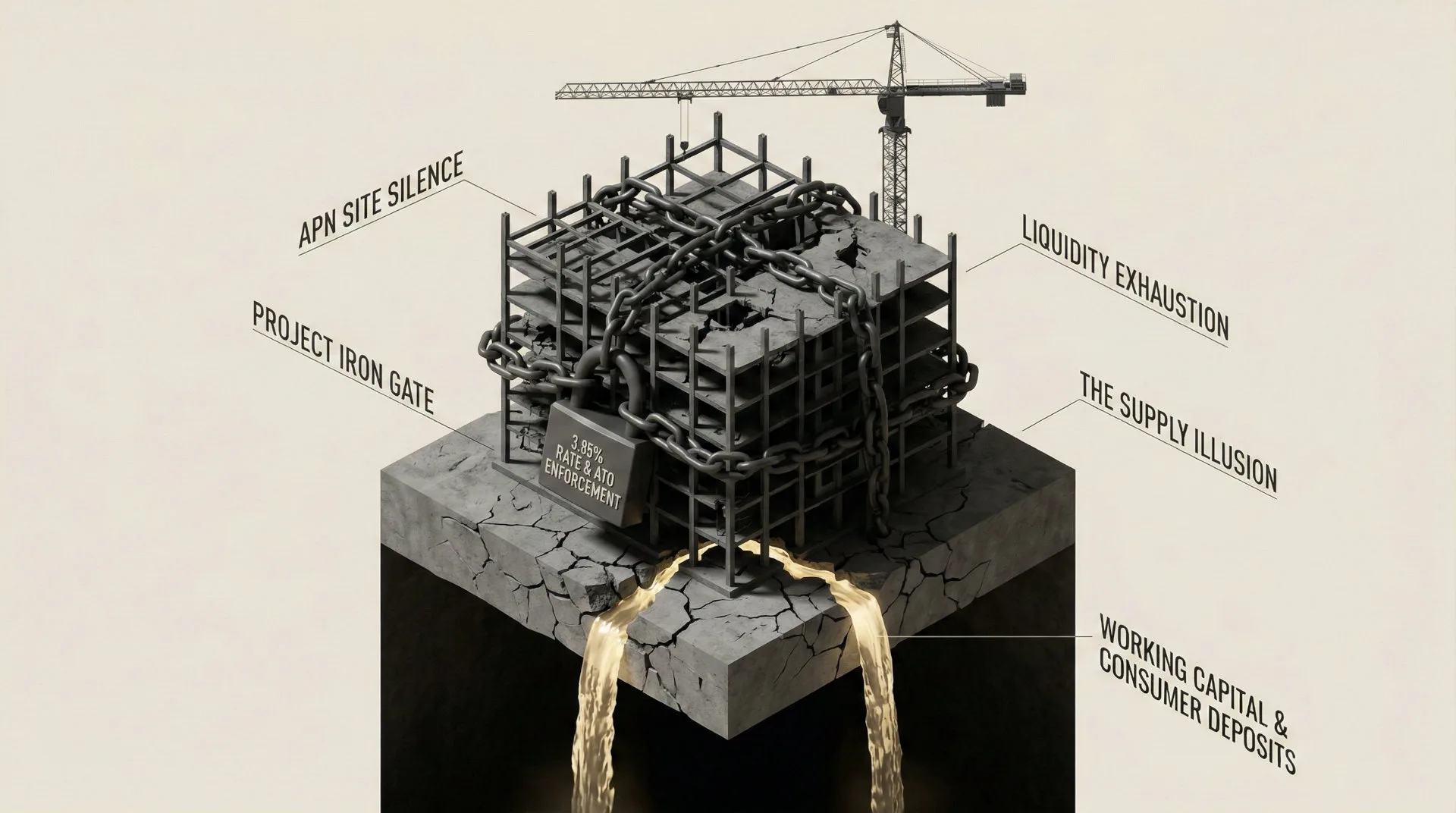

Quantifying the Trigger (Project Iron Gate): The RBA’s hike to a 3.85% cash rate acted as a monetary ‘Iron Gate’, materially restricting the construction sector’s access to the cheap, continuous working capital it requires for survival. This event demonstrates the core thesis that in a tightened credit environment, cash flow—not collateral—is the ultimate determinant of survival.

Measuring the Enforcement Impact (APN Risk & Compliance Index™ (24200)): The ATO’s substantive application of Director Penalty Notices to recover $4.3 billion in tax debt from the construction sector is a clear example of regulatory velocity creating a sustained liquidity event. This enforcement action acts as the final catalyst, forcing already-constrained firms into immediate liquidation and formalising the ‘Site Silence’ phase.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of macroeconomic data from the RBA, corporate insolvency filings from ASIC, and proprietary intelligence on supply chain and credit market conditions. The key facts are:

- Monetary Policy Impact: In February 2026, the RBA lifted the official cash rate to 3.85%, citing persistent inflationary pressures. This immediately increased debt servicing costs for highly geared builders, contracting working capital and materially reducing margins on fixed-price contracts.

- B2B Default Acceleration: The rate hike triggered a material acceleration in business-to-business invoice defaults. CreditorWatch data confirms the construction sector is the highest single contributor to national insolvencies, accounting for approximately 24% of all corporate failures.

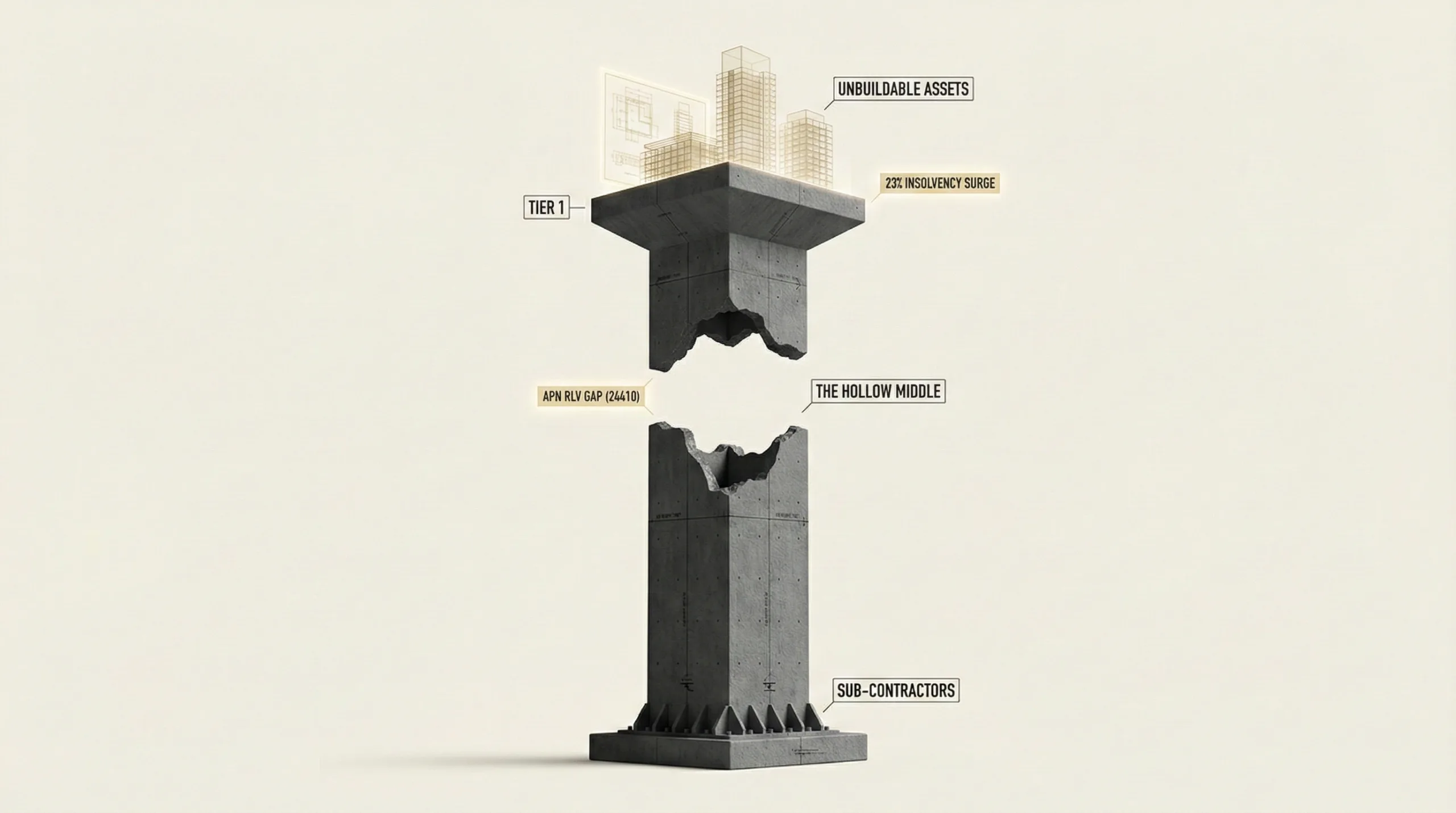

- Structural Insolvency Volume: ASIC data shows a new, elevated baseline of 1,200-1,300 monthly corporate insolvencies across the economy. Within this, 2,142 construction firms entered external administration in the financial year to early February 2026, indicating a structural contraction, not a cyclical adjustment.

- Supply Chain Structural Adjustment: An accelerated growth in global copper prices in Q4 2025, a critical late-stage material, eliminated profitability on projects priced months or years earlier. This demonstrates how time itself has become a lethal cost multiplier for delayed projects.

- Regulatory Friction & Credit Withdrawal: The ATO is actively pursuing $4.3 billion in collectable debt from the construction sector, primarily using Director Penalty Notices. Simultaneously, trade credit insurers have withdrawn coverage from the sector, forcing suppliers to demand cash on delivery and creating a sustained ‘Liquidity Exhaustion Point’ for builders.

- Labour Market Displacement: A substantive pipeline of Tier 1 infrastructure and renewable energy projects, backed by over $37 billion in capital, is actively ‘crowding out’ the residential sector by absorbing the finite pool of skilled trades with higher wages and superior payment security.

Critical Analysis & Balanced View

The current structural pressure point is not the result of a single factor, but a material, interconnected sequence of events. The monetary policy intended to curb demand-side inflation has had the unintended consequence of exhausting the housing market’s supply-side capacity. This creates a structural paradox: by trying to solve today’s inflation, policymakers have created the conditions for a future housing shortage and the material rental and price inflation that will accompany it. The failure of a Tier 2 builder is no longer an isolated commercial event; it is a systemic pressure that travels through the entire supply chain and capital stack, with the final impact absorbed by the unsecured consumer deposit.

The analysis reveals a complete breakdown in the traditional risk-sharing model of property development. The ‘selective underwriting’ by trade credit insurers and the ‘firmer and faster actions’ of the ATO are not independent events but coordinated responses to the same underlying data showing structurally significant balance sheet fragility. This tri-party sustained friction between the builder, their suppliers, and the regulator is structurally unavoidable. The ‘Site Silence’ phase is therefore not a temporary pause but a structural state, representing a lasting void in the market’s capacity to deliver medium- to high-density housing.

Strategic Implications for Property Professionals

- For Developers: Immediately re-evaluate all counterparty risk. Builder solvency is now the primary project risk, superseding site acquisition and sales velocity. Existing fixed-price contracts are likely unviable; prepare for re-negotiation, significant cost escalation, or contractor failure. Future projects require higher contingency budgets and procurement models that de-risk supply chain exposure.

- For Lenders & Financiers: Stress-test all construction loan books against cascading builder failure scenarios. The value of pre-sales as a risk mitigant is materially diminished when the contracted builder is insolvent. Expect a material volume of projects requiring receiver appointments and prepare for mortgagee-in-possession sales in a market with few viable replacement builders.

- For Agents & Buyers’ Agents: You have a duty to advise clients of the elevated systemic risk in the off-the-plan market. The security of deposits is now structurally uncertain. Your advice must shift focus to established properties or projects delivered by Tier 1 entities with highly resilient balance sheets. Due diligence must now extend beyond the developer to the builder’s financial health and project exposure.

- For Investors & Off-the-Plan Buyers: The risk of total deposit loss, or elevated opportunity cost via sunset clause cancellations, is at a cyclical high. Avoid any development where the builder is a mid-tier entity with high gearing and low public visibility. The ‘Glass House’ is structurally degrading, and as a Tier 4 Host, your capital is the most exposed.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides empirical validation for the core theses of The Supply Illusion and The Glass House (Net State Position™). It indicates a structurally significant expansion in the APN Residual Land Value (RLV) Gap™ (24410) for the entire mid-tier sector, confirming the core mechanism of the APN Future Development Pipeline Index™ (24400).

- Index Calibration: The APN Regulatory Velocity Multiplier™ (24210) is calibrated upwards to reflect the ATO’s substantive use of Director Penalty Notices as a primary catalyst for corporate failure. The APN Supply Chain Strain Index™ (a component of 24400) is recalibrated to more heavily weight the temporal risk of late-stage material cost escalations, such as copper.

- Data Capture: This analysis triggers a new data capture mandate to track the ratio of court-ordered winding-up applications versus voluntary administrations within the construction sector. This ratio will serve as a real-time proxy for the extent of balance-sheet deterioration and the declining viability of corporate rescue attempts.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24600) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.