BTR Viability Reassessment: Financial Recalibration Evident as Developers Defer Loss Recognition

APN ANALYSIS: A-260112-AUS134220

Executive Summary

A systematic investigation into the Australian Build-to-Rent (BTR) sector has disproven the hypothesis that major domestic developers are preparing an imminent, widespread “Strata Exit” by filing for subdivision. APN’s audit of planning portals for major assets from Lendlease and Mirvac returned no such applications. However, the analysis confirms a more subtle but significant “Financial Recalibration” is underway. This is evidenced by the exit of founding institutional capital from Mirvac’s BTR fund and a material yield inversion, where the cost of debt now exceeds the yield on development cost. The public commitment to the BTR model coincides with a private, operational recalibration driven by unsustainable project economics.

For property professionals, this signals an elevated divergence in the market. The immediate risk is not an elevated volume of BTR stock hitting the for-sale market, but a prolonged period of commercially unviable projects and a capital constraint for listed Australian developers. While the domestic BTR pipeline is effectively constrained by an unworkable cost structure, the continued activity of foreign capital, such as Greystar, highlights a bifurcation of the sector. This creates a clear strategic advantage for operators with access to a lower cost of capital or more efficient, standardised delivery models, who can capitalise on the constraint of their domestic competitors.

Background & Strategic Context

This analysis validates and calibrates several of APN’s core macro-theses, revealing a market shaped by the interplay of state intervention, capital flows, and fundamental economic viability. The BTR sector has become a primary area of structural interaction where these forces are most visible, determining which projects proceed from paper approvals to physical construction.

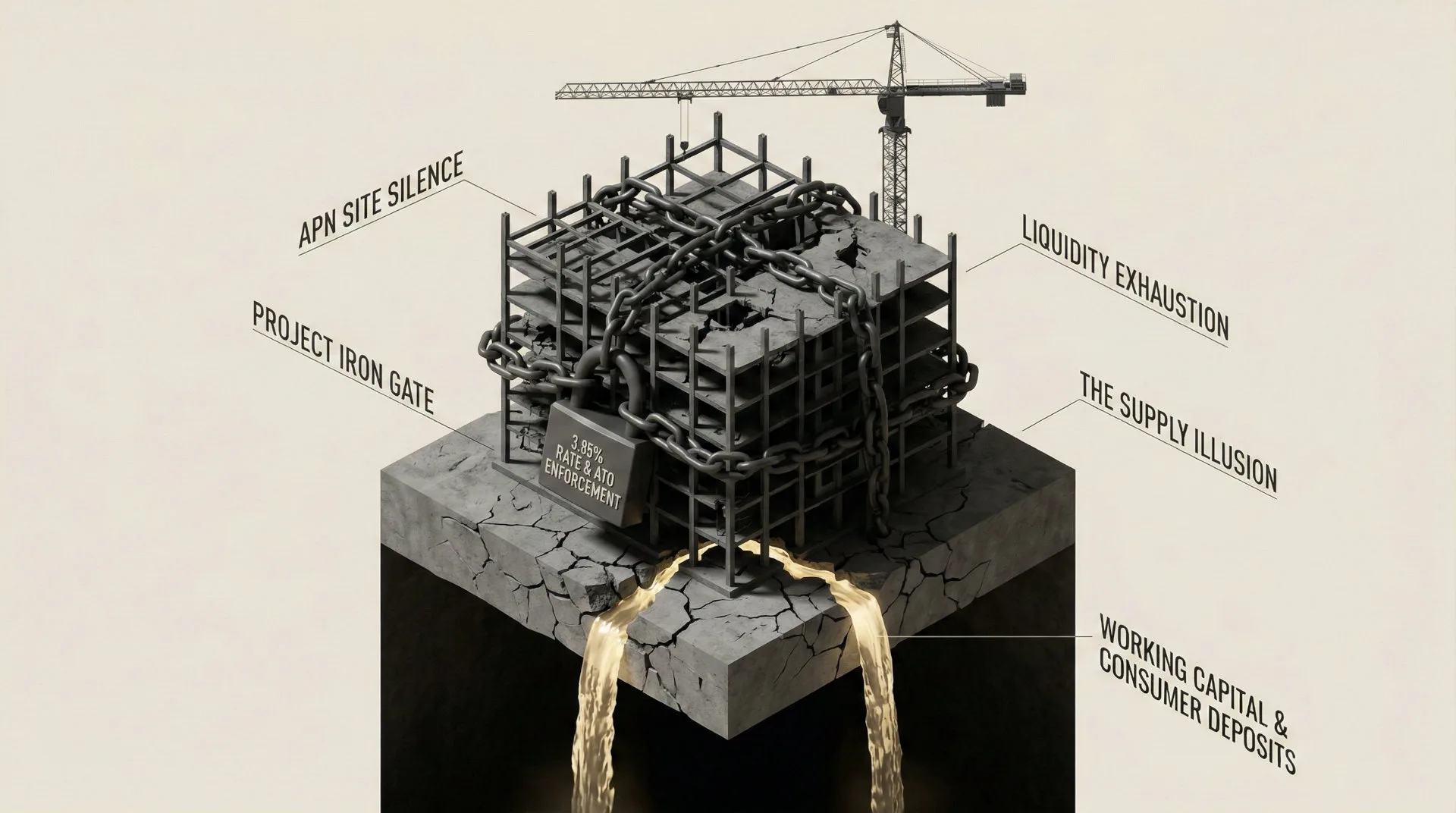

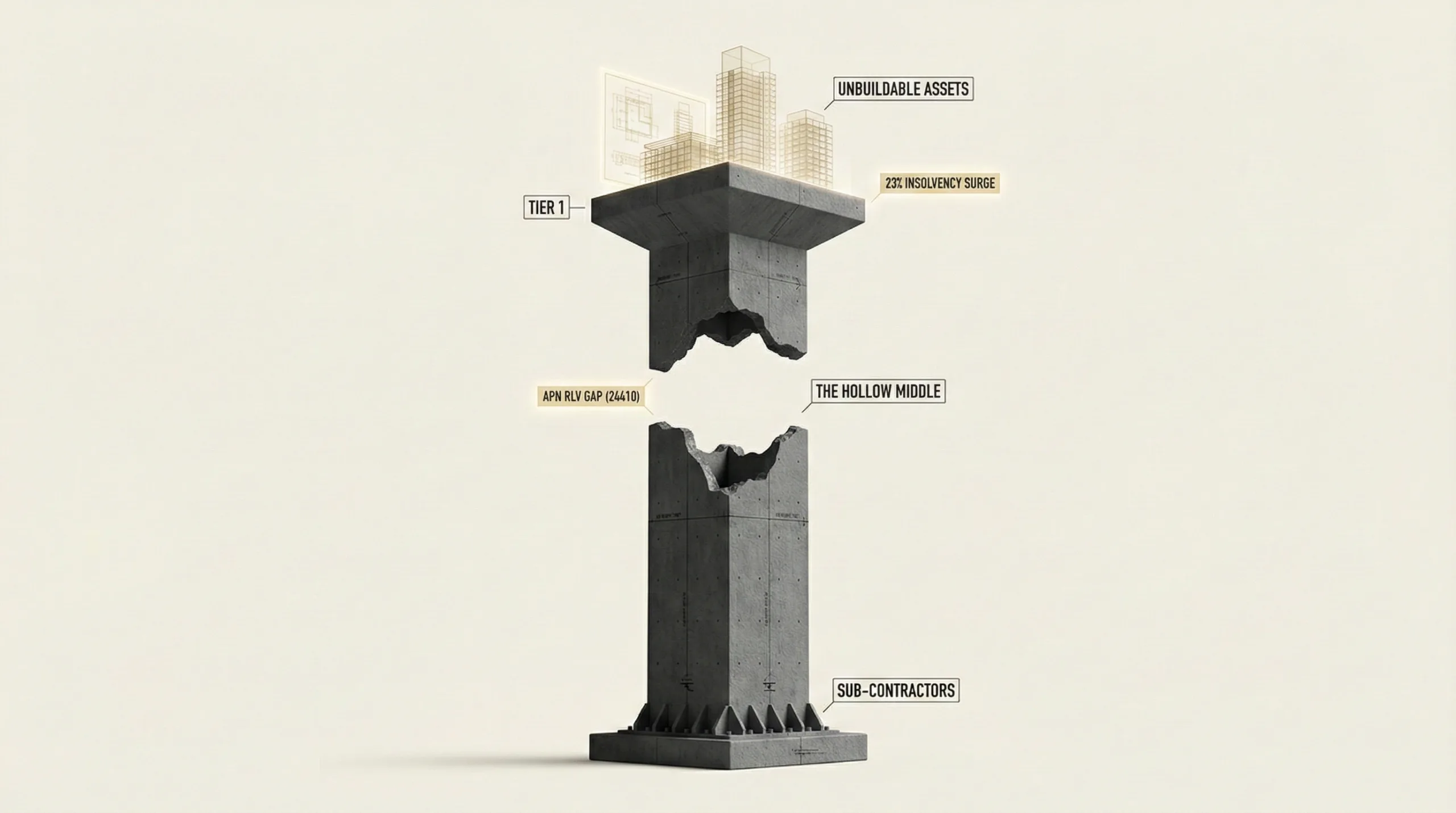

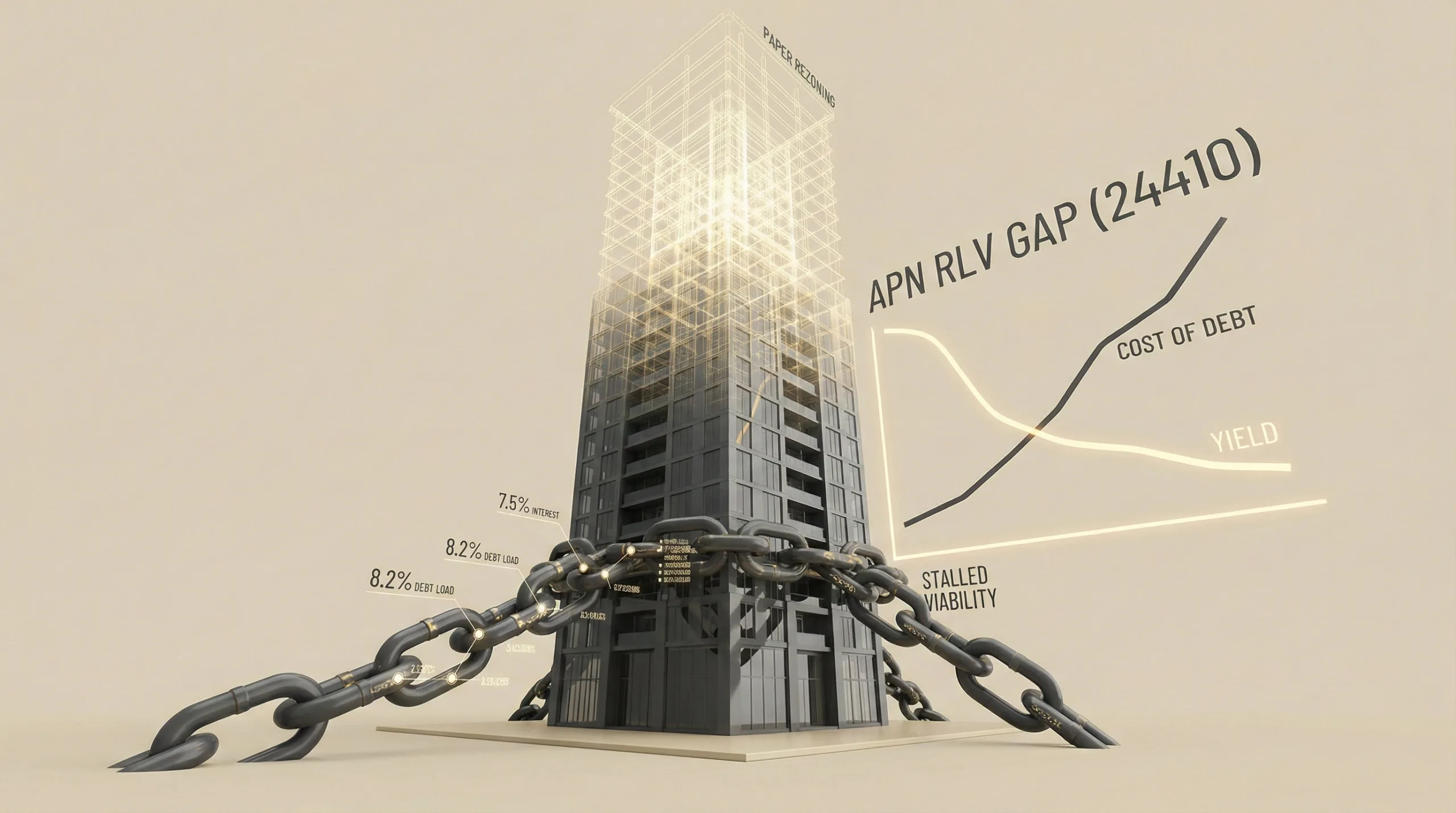

The Viability Impasse (APN RLV Gap™): The core of the structural pressure point is the negative spread between the achievable development yield on new projects (estimated at ~3.8%) and the prevailing cost of debt (~5.5%). This creates a significant APN Residual Land Value (RLV) Gap™, rendering new projects financially unviable from inception and turning thousands of approved apartments into dormant “Paper Rezonings”.

The Regulatory Anchor (APN Risk & Compliance Index™): State-level intervention, exemplified by the Queensland Government’s affordability covenants on Mirvac’s LIV Anura project, acts as a structural impediment. These contractual obligations create a formidable barrier to a “Strata Exit”, effectively sustaining the asset in a rental tenure and demonstrating how regulatory frameworks under the APN Risk & Compliance Index™ (24200) can dictate asset-level strategy and constrain commercial optionality.

The Capital Structure Arbitrage: The transaction seeing Mitsubishi Estate (foreign commercial capital) exit Mirvac’s BTR fund, to be replaced by Australian Retirement Trust (domestic superannuation capital), represents a shift from shorter-term, higher-return-seeking capital to long-dated, lower-yield-accepting domestic capital. This capital structure adjustment serves to stabilise the asset and prevent a forced liquidation, protecting incumbent valuations while highlighting the pressure on the original investment thesis.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing, synthesising systematic audits of state planning portals, ASX announcements, and financial reporting data from Q4 2025 to January 2026. The key facts are:

- ‘Stealth DA’ Hypothesis Disproven: A comprehensive systematic search of planning registers for Lendlease’s Melbourne Quarter West Tower and Mirvac’s LIV Anura and LIV Aston assets returned a NIL result for any strata subdivision applications lodged within the target window.

- Founding Capital Exit: In December 2025, Australian Retirement Trust (ART) acquired a 48.5 per cent stake in Mirvac’s $1.7 billion BTR fund. This stake was sold by a founding investor, confirmed by market intelligence to be Mitsubishi Estate, whose exit after an anomalously short hold period signals a reassessment of the asset class’s near-term performance outlook.

- Yield Inversion Confirmed: Analysis of Mirvac’s FY25 financial data confirms an average cost of debt between 5.4% and 5.6%. This is materially contrasted with the estimated Net Development Yield of ~3.8% for new projects, creating a negative carry of -1.7%. Even on operational assets, the book capitalisation rate of ~5.75% provides a negligible 15 basis point spread over debt, indicating material cash flow pressure.

- US Capital Divergence: In material contrast to the domestic slowdown, US-based major BTR operator Greystar broke ground on its $360 million “Haiku” project in Kensington, Melbourne, in September 2025. This demonstrates that the BTR model remains viable for operators with a different cost of capital and a more efficient, standardised delivery model.

Critical Analysis & Balanced View

The investigation reveals a sector in a state of deferring loss recognition. The absence of strata subdivision applications is not a sign of robust health, but a strategic decision to avoid crystallising a valuation loss. By recapitalising with more stable domestic superannuation capital, developers like Mirvac can extend the holding period, hoping that accelerated rental growth will eventually close the gap with the high cost of debt. This avoids a forced liquidation but validates the financial pressure that forced the original capital partner to retreat.

The “Strata Optionality” designed into these premium towers remains a material dormant risk. The high-quality finishes and extensive amenity packages mean these assets can be easily pivoted to a for-sale product if required. The lack of a DA today is a function of current partnership agreements, not a permanent strategic commitment. Should the yield inversion persist and rental growth falter, these capital partners may re-evaluate their strategic commitment, making the strata exit the most logical path to liquidity.

Finally, the Greystar counter-narrative is materially instructive. It demonstrates the BTR asset class itself is not structurally unviable in Australia. Rather, the specific high-cost, bespoke architectural model favoured by listed domestic developers is what has become unviable in the current capital environment. The future of the sector may be increasingly dominated by vertically integrated global players who can leverage scale, standardisation, and a lower cost of capital to navigate the RLV Gap™.

Strategic Implications for Property Professionals

- For Developers: The APN RLV Gap™ is now the defining constraint for the BTR sector. New projects are unfeasible without materially discounted land, significant government subsidies, or access to a capital structure with a cost of debt well below the market rate for listed entities. The Greystar model of product standardisation and mid-market positioning offers a more resilient pathway than the premium, high-OpEx model.

- For Capital Allocators & Fund Managers: The Mitsubishi/ART transaction is a material signal of a capital pivot. Opportunities now exist to acquire stakes in funds under pressure or partner with developers needing to recapitalise. However, underwriting must be focused on the real cash-on-cash return after debt service and factor in a long-term hold, as near-term yield compression is structural.

- For Valuers & Financiers: Book valuations based on a ~5.75% capitalisation rate are under elevated pressure when the cost of debt is ~5.6%. Valuations must now more heavily weight the negative carry on new developments and the thin cash-flow spread on operational assets. The “Strata Optionality” should be assessed as a potential exit, but its value is contingent on the health of the retail apartment market at the time of a future pivot.

- For Agents & Buyers’ Agents: A large-scale “Strata Exit” is a medium-term risk, not an immediate market event. Do not expect an elevated volume of high-quality BTR stock to hit the for-sale market in 2026. However, major assets like LIV Aston and Melbourne Quarter West Tower should be monitored closely for any future subdivision applications, as this would be a leading indicator of a market shift and a significant release of new apartment supply.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core mechanism of the APN Residual Land Value (RLV) Gap™ (24410), confirming that a negative spread between development yield and debt cost is the primary force constraining the BTR pipeline. It also validates the application of the APN Risk & Compliance Index™ (24200) in identifying how regulatory covenants act as structural impediments that constrain asset-level exit strategies.

- Index Calibration: The APN Future Development Pipeline Index™ (24400) will be calibrated to more heavily weight the cost of debt as a primary friction filter for project viability. The confirmed negative carry of -1.7% on new BTR starts provides a new, sector-specific benchmark for identifying “Paper Rezonings”.

- Data Capture: This analysis triggers a new data capture mandate for the APN Symbiotic Intelligence Network™ (24310). The network will now systematically track the capital structure of major BTR projects, specifically monitoring the weighted average cost of capital (WACC) and the origin of equity (e.g., domestic superannuation vs. foreign commercial) as a leading indicator of project viability and developer pressure.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.