Structural Bifurcation of the NEM Validated: Prioritisation of Data Centres Over Industrial Loads

APN ANALYSIS: A-260111-AUS134203

Executive Summary

A confluence of a material heatwave and elevated transmission failures between January 8-11, 2026, served as a stress test for the Australian National Electricity Market (NEM). The event validated the hypothesis of a structural bifurcation in the grid: the market has structurally bifurcated, creating two distinct tiers of energy users. It now systematically prioritises ‘Light Zones’, capital-intensive digital infrastructure like data centres, while treating ‘Dark Zones’, the traditional industrial base, as curtailable loads to maintain grid stability. This represents a fundamental and structurally significant shift in the social contract of energy reliability, moving from a universal standard to a tiered system based on an asset’s ability to pay for protection.

For property professionals, this event codifies a new, elevated layer of location-based risk and opportunity. The financial viability and underlying value of industrial assets are now directly tied to their position in this new energy hierarchy. Assets located in ‘Dark Zones’ face material operational risks from both physical curtailment and elevated price volatility, impacting their valuation, insurability, and operational continuity. Conversely, assets co-located with or serving the protected ‘Light Zones’ benefit from a ‘reliability premium’ and new commercial opportunities in energy infrastructure, fundamentally redrawing the map for industrial investment and development.

Background & Strategic Context

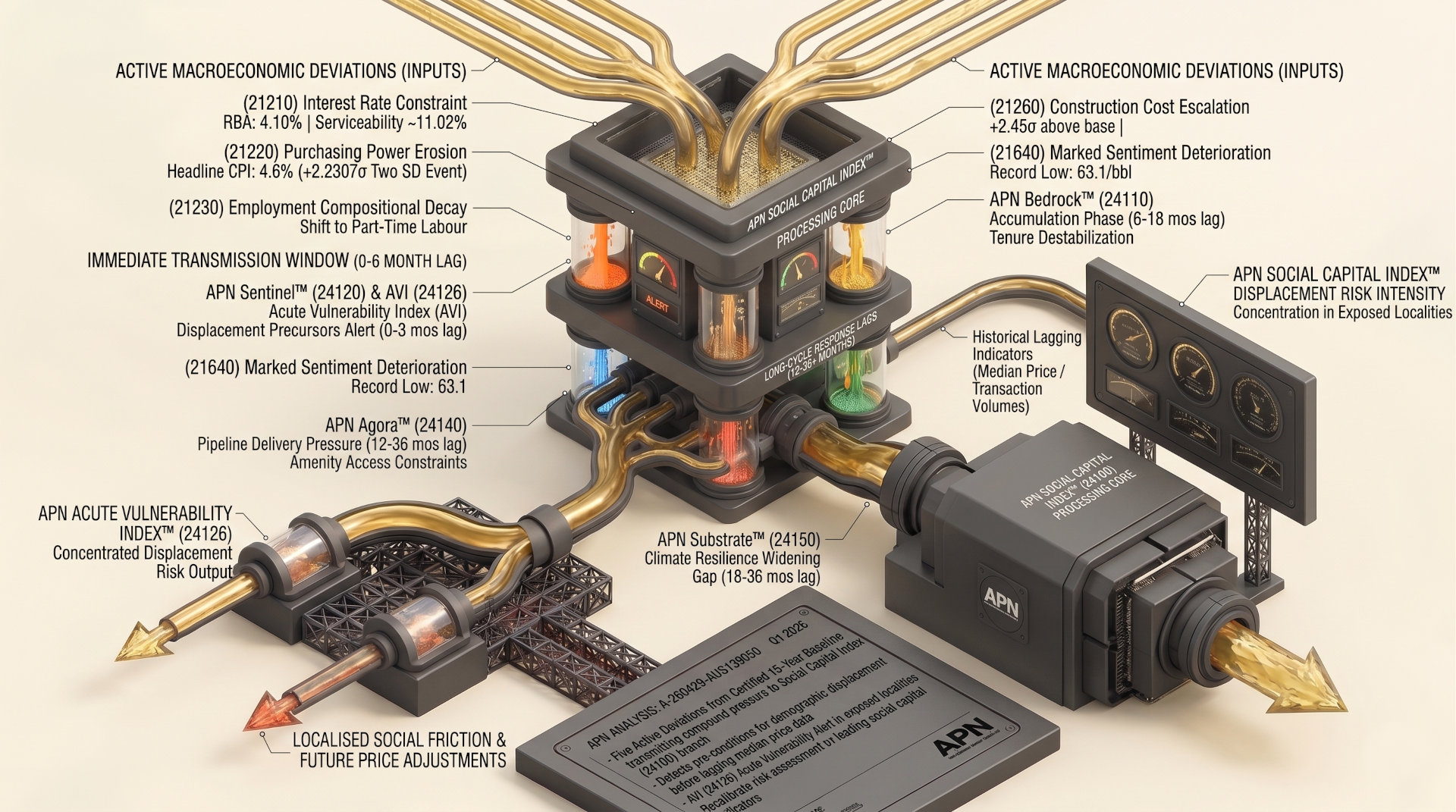

This event validates and calibrates APN’s core macro-theses, demonstrating how state-level market design, as measured by the APN Sovereign Policy Composite Index™ (SPCI, 24800), creates a tiered system that results in a reallocation of capital and operational security toward a specific cohort of assets. The structural pressure point was not a simple market failure but the logical outcome of a system designed to manage volatility through financial mechanisms that favour new, flexible digital assets over the incumbent physical economy.

The State as the Primary Actor (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The design of market mechanisms like the System Integrity Protection Scheme (SIPS) and the classification of emergency reserves (RERT) are state-level interventions by the Australian Energy Market Operator (AEMO). These rules are not neutral; they explicitly dictate who receives power during an elevated systemic condition and who is curtailed. This is not a free market outcome; it is a market architected to produce this exact bifurcation.

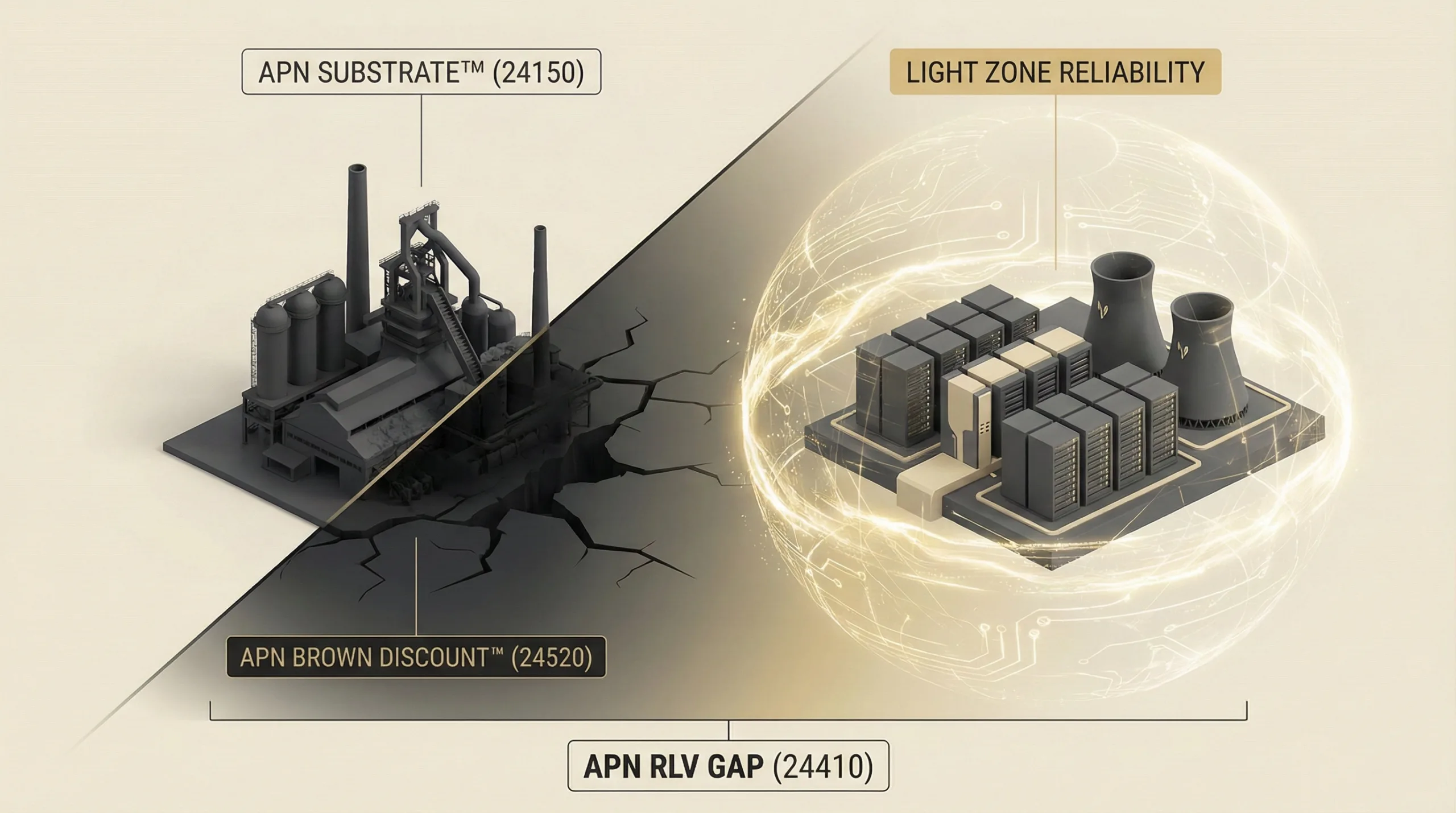

The Erosion of the Physical Layer (APN Substrate™): The analysis maps the ‘Dark Zones’ directly onto the APN Substrate™ (24150) – the nation’s industrial bedrock of steel, aluminium, and manufacturing. The events of January 2026 demonstrate a structurally significant failure of this substrate’s adaptive capacity, with assets like Tomago Aluminium and BlueScope Steel being treated as grid stabilisers first and productive enterprises second.

The Emergence of a Quantifiable ‘Brown Discount’ (APN Financial Climate Sensitivity™): The elevated price volatility and curtailment risk facing heavy industry represent a tangible financial liability. This event allows us to quantify the APN Brown Discount™ (24520) for assets in these ‘Dark Zones’, as their energy insecurity directly devalues their operational viability and corporate worth, a risk factor now visible in BlueScope’s contested takeover valuation.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of Australian Energy Market Operator (AEMO) market notices and operational data from the elevated energy system events of January 8-11, 2026. The key facts are:

- The Trigger Event: A material heatwave across South Australia and Victoria drove record electricity demand while simultaneously derating the thermal capacity of elevated-risk transmission lines.

- The Primary System Failure: On January 9, 2026, the unplanned outage of two key 330kV transmission lines into Melbourne (Dederang–South Morang No. 2 and Dederang–Murray No. 67) created a double contingency (N-2) event, placing the Victorian grid at risk of systemic contraction.

- The ‘Dark Zone’ Response: AEMO’s immediate response relied on curtailing large industrial loads to preserve system frequency. Tomago Aluminium in NSW was required to function as a ‘virtual battery’, shedding an estimated 600 MW, while BlueScope Steel at Port Kembla was exposed to price spikes near the market cap of ~$16,600/MWh.

- The ‘Light Zone’ Shield: Simultaneously, the Victoria Big Battery (VBB) was activated under its System Integrity Protection Scheme (SIPS) contract, injecting 250 MW to stabilise voltage in the Melbourne metropolitan area. This action effectively shielded the city’s data centres and residential loads from the rolling blackouts threatening industry.

- The Financial Outcome: A net capital reallocation occurred. Industrial assets incurred financial losses from lost production and elevated price exposure, while flexible assets like the VBB and Virtual Power Plant (VPP) aggregators profited from SIPS activation payments and arbitrage opportunities created by the elevated systemic condition.

Critical Analysis & Balanced View

This tiered reliability dynamic is not the result of structural incentive alignment but an emergent, structural property of a market that has prioritised financialisation over universal service. The paradox is that the very solutions meant to manage renewable intermittency—batteries and demand response—are creating a new, material form of energy inequality. The application of the term ‘demand response’ to industrial loads is functionally distinct from its application to other market participants. The investigation shows it is effectively non-discretionary curtailment to prevent systemic contraction, with compensation that does not consistently cover the resulting financial losses. In contrast, ‘demand response’ from VPPs and data centres is a voluntary, profit-seeking arbitrage activity.

The system is now designed to reward capital-intensive, flexible digital assets that can monetise volatility, while structurally constraining capital-intensive, inflexible industrial assets that require stability. The elevated long-term risk is the permanent deindustrialisation of the APN Substrate™, leaving Australia’s economy structurally reliant on a digital layer that itself depends on a functioning physical world for its inputs and security. The grid’s structure has produced cohorts with differing viability. Without intervention, commercially unviable cohorts face structural displacement.

Strategic Implications for Property Professionals

- For Industrial Asset Owners & Investors: Energy security is now a primary due diligence item. Proximity to constrained transmission nodes is a quantifiable liability. Valuations must now incorporate an ‘energy risk discount’ based on an asset’s classification as a curtailable Tier 3 load. Investment in on-site firming (e.g., solar with battery storage, gas) is no longer optional but essential for operational viability.

- For Developers (Industrial & Commercial): The ‘Light Zones’ (e.g., Western Sydney, Western Melbourne) are becoming de-risked enclaves for development. Significant opportunities exist in co-locating new industrial and logistics facilities with energy infrastructure like large-scale batteries and data centres to benefit from the ‘reliability halo’ and potentially participate in VPP revenue streams.

- For Valuers & Risk Assessors: The traditional valuation model for industrial property is now no longer structurally viable. A new tiered reliability overlay must be applied, mapping assets against the Dark/Light Zone geography. The APN Substrate™ (24150) rating for an industrial precinct is now a primary indicator of its long-term value, insurability, and financial viability.

- For Agents & Buyers’ Agents: Marketing material for industrial properties must now explicitly address energy resilience. Properties with secured, long-term firm power contracts, on-site generation, or a location within a designated ‘Light Zone’ command a significant and justifiable premium. Conversely, assets exposed to spot prices in ‘Dark Zones’ must be marketed with full disclosure of this fundamental operational risk.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides high-confidence validation for the APN Substrate™ (24150) as a primary indicator of physical economic resilience. The direct correlation between the identified ‘Dark Zones’ and the nation’s industrial base confirms the index’s core premise that physical infrastructure underpins sovereign capability.

- Index Calibration: The APN Financial Climate Sensitivity™ (24510) will be calibrated to incorporate ‘Grid Reliability Volatility’ as a key input. The frequency of curtailment events and exposure to prices above a specified threshold (e.g., $5,000/MWh) will now be weighted factors in calculating the APN Brown Discount™ (24520) for affected industrial assets.

- Data Capture: This event triggers a new data capture mandate for the APN Agora™ (24140) index. We will now track and map the location of high-voltage substations and SIPS-enabled battery assets as primary ‘digital connectivity’ infrastructure, distinct from and superior to standard utility provision.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.