The SEQ Liquidity Trap: How Uninsurability is Constraining the Property Market

APN ANALYSIS: A-260120-AUS134918

Executive Summary

A convergence of structurally significant hailstorms, a material failure in federal policy, and unique Queensland conveyancing laws has precipitated a structural “Liquidity Trap” in the South-East Queensland residential property market. This is not a structural pressure point of demand, but of transaction mechanics. The inability of the insurance market to price or provide continuous coverage in the wake of CAT 255 has created semi-permanent “uninsurable zones,” primarily in the Logan-Bayside corridor and Gold Coast Hinterland. This manifests as operational embargoes during weather events and “technical embargoes” via prohibitive premiums, which have been observed reaching $6,200, nearly double the state average. The result is a localised but material market constraint, where assets cannot be financed or settled, causing transactions to be terminated and exposing buyers to significant legal and financial risk.

For property professionals, this is a paradigm shift, not a cyclical weather event. The inability to secure insurance has moved from a fringe administrative hurdle to a primary driver of transaction failure and asset devaluation. Professionals must now treat “insurability risk” as a core component of due diligence, on par with building and pest inspections. The financial viability of a transaction and the underlying value of an asset are now directly tethered to the postcode’s rating within an insurer’s risk model. Ignoring this new reality exposes clients to structurally significant settlement failure and agents to significant professional liability.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses on the primacy of state intervention and the financialisation of physical risk. The emergence of an “Uninsurable Zone” is not an organic market failure but a direct consequence of a legislative framework ill-equipped for meteorological reality. It provides a powerful, real-world case study of how policy gaps create market distortions and devalue assets.

A Failure of State Intervention (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The analysis confirms that the legislative design of the Cyclone Reinsurance Pool (CRP) is the central catalyst for the structural pressure point. By narrowly defining its remit to “Cyclone Events,” this federal intervention has failed to cover SEQ’s primary peril, Severe Convective Storms (hail). This policy gap has created a two-tier market, where cyclone risk is subsidised by the government while hail risk is borne entirely by the private market, leading to the observed material premium adjustments in SEQ.

The Physical Risk Becomes Financial (APN Substrate™ 24150): The events of the 2025/26 season are a physical manifestation of the climate and material weather risks this index is designed to quantify. The market is no longer treating these as abstract, long-term possibilities. The $6,200 premium is the market’s mechanism for pricing the high probability of roof and property damage in the “Hail Alley,” moving the risk from a theoretical rating to a tangible, immediate financial cost that directly impacts household budgets and asset viability.

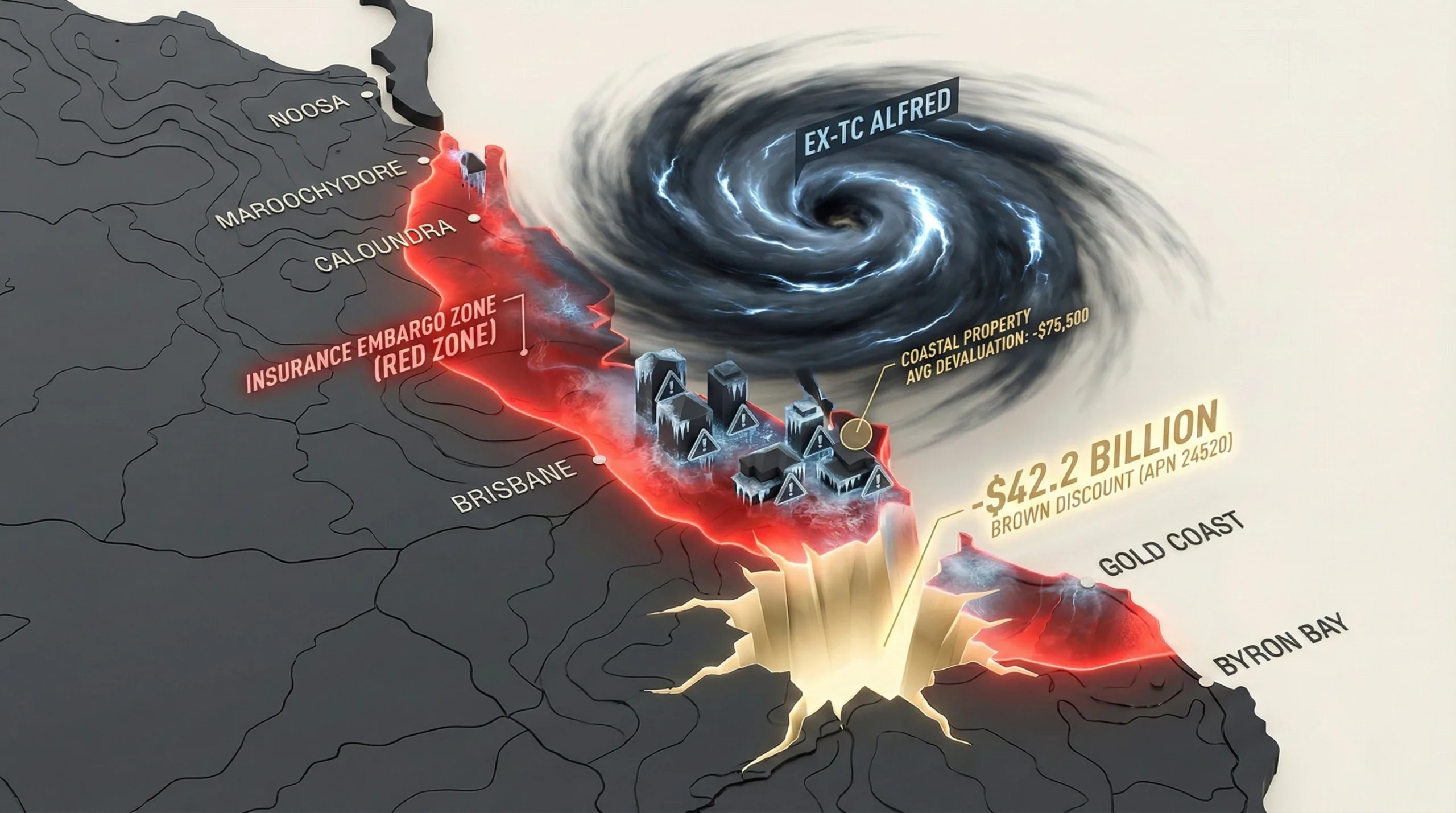

The Emergence of a “Brown Discount” (APN Climate-Risk Asset Devaluation Index™ 24500): The prohibitive premiums and withdrawal of coverage in specific postcodes represent the first wave of a quantifiable `APN Brown Discount™ (24520)`. Assets located in the “Uninsurable Zone” are being financially penalised for their high physical risk exposure. This is no longer an ESG reporting metric; it is a direct impact on an asset’s net yield, borrowing capacity, and, ultimately, its market value.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of insurance industry declarations, meteorological data, and insurer financial disclosures following the 2025/26 severe weather season. The key facts are:

- The Trigger Event: The primary capital erosion event was CAT 255, a non-cyclonic giant hail event on 23-24 November 2025, which produced hail exceeding 11cm in a corridor from the Gold Coast Hinterland to Brisbane’s Bayside. This event, not a cyclone, is the driver of the current insurance structural pressure point in SEQ.

- The Geographic Footprint: The “Uninsurable Zone” is not random; it precisely maps the “supercell highway” that characterises SEQ’s climatology. The core zones are the Logan “Hail Alley” (4127, 4129), the Bayside Corridor (4179, 4154), and the Gold Coast Hinterland (4272).

- The Insurance Response: Insurers have deployed a two-pronged retreat. “Operational Embargoes” temporarily freeze new policies during active storms like Ex-TC Koji in January 2026. More critically, “Technical Embargoes” use prohibitive pricing (premiums >$6,000) and impossible underwriting conditions (e.g., requiring certified roof integrity on damaged properties) to effectively redline these zones.

- The Legal Vulnerability: Queensland’s “Risk at Contract” conveyancing standard (REIQ contracts) is a critical vulnerability. It passes all risk for the property to the buyer at 5:00 PM the next business day after signing, exposing them to material financial loss if a storm hits or an embargo is enacted before they can secure insurance.

- The Policy Failure: The Federal Cyclone Reinsurance Pool (CRP) is legislatively barred from covering damage from Severe Convective Storms (hail). As CAT 255 was not a cyclone, insurers had to absorb the full billion-dollar-plus loss on their private balance sheets, forcing them to materially raise premiums in SEQ to recover capital.

Critical Analysis & Balanced View

The SEQ property market is experiencing a paradox created by well-intentioned government intervention with structural limitations. The Cyclone Reinsurance Pool, designed to enhance affordability in North Queensland, has inadvertently concentrated private reinsurance pricing power on the remaining perils in South-East Queensland. This has created the anomalous condition where insuring against hail in Logan can be more expensive than insuring against cyclones in Cairns, simply because one risk is government-backed and the other is exposed to a volatile global market.

The “Settlement Trap” represents a dormant systemic vulnerability in Queensland’s legal framework, now activated by insurance market illiquidity. This procedural failure disproportionately impacts the most financially fragile market participants, such as First Home Buyers using low-deposit schemes, who lack the cash reserves to navigate premium shocks or settlement delays. The “Technical Embargo” is a sophisticated form of de-risking by insurers; by pricing coverage at a level that materially constrains mortgage serviceability, they effectively withdraw from a market without facing the regulatory and political consequences of a formal exit.

This is not merely an insurance problem; it is a market structure problem. The inability to transfer risk via insurance breaks a fundamental link in the chain of property transactions. Without a policy solution to address the “hail gap” in the CRP, these “Uninsurable Zones” are likely to become entrenched, leading to a permanent bifurcation in asset values between insurable and uninsurable postcodes.

Strategic Implications for Property Professionals

- For Agents & Buyers’ Agents: Contract management is now a primary risk mitigation tool. A “subject to satisfactory insurance” clause is no longer optional but essential for protecting buyers in any area with elevated storm risk. You must advise clients that finance clauses do not protect against insurance issues arising late in the contract period and manage settlement timelines to avoid known high-risk periods like the Christmas shutdown.

- For Valuers & Lenders: Asset valuation and credit assessment models require immediate recalibration. The annual insurance premium is a direct input to net yield for investors and debt serviceability for owner-occupiers. A property with a $6,000 premium has a lower net value and supports a smaller loan than an identical property with a $3,000 premium. The inability to obtain a Certificate of Currency is a primary indicator of a compromised security.

- For Developers: Granular climate risk analysis is now a critical component of site acquisition due diligence. The viability of a project is no longer just about construction costs and sales values; it is now also dependent on the insurability of the end product for purchasers. Developing within a known “Hail Alley” or a postcode near its insurer accumulation limit introduces significant settlement risk that can stall project sell-downs.

- For Strata & Property Managers: Proactive asset hardening is the most effective defence. A building’s insurance profile is now a key determinant of its value and appeal. Advocating for capital works funds to be directed towards roof upgrades, impact-resistant solar panels, and building envelope improvements can generate a significant return on investment through lower premiums and improved insurability, creating a competitive advantage in the market.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the APN Sovereign Policy Composite Index™ (SPCI, 24800) thesis, demonstrating how a specific legislative gap, the Cyclone Reinsurance Pool’s exclusion of hail, is the primary driver of market dislocation and reduction in asset value in SEQ. It also validates the predictive power of the `APN Substrate™ (24150)` index, which flagged these zones for high severe weather risk.

- Index Calibration: The `APN Climate-Risk Asset Devaluation Index™ (24500)` is now calibrated to classify prohibitive insurance premiums (defined as >150% of the state average) as a direct financial signal triggering an `APN Brown Discount™ (24520)`. The `APN Financial Climate Sensitivity™ (24510)` rating for postcodes 4127, 4129, and 4272 is immediately elevated to “Extreme”.

- Data Capture: This event triggers a new data capture mandate for the `APN Symbiotic Intelligence Network™ (24310)`. The system will now actively track and quantify (a) insurance quote denial rates by postcode, (b) average quoted premiums for a benchmark property in high-risk zones, and (c) the prevalence of “subject to insurance” clauses in contracts as leading indicators of market liquidity and settlement friction.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.