‘Valuation Air-Gap’ of 10-15% Creates Systemic ‘Settlement Trap’ for Off-the-Plan Buyers

APN ANALYSIS: A-260120-AUS134899

Executive Summary

A systemic ‘Valuation Air-Gap’ has opened for off-the-plan properties settling in Q1 2026, with major lenders de-rating assets in the high-density and greenfield corridors of Western Sydney and Melbourne’s North by 10-15% against their 2024-2025 contract prices. This material shift from a benign -2% historical variance is a structured defensive response by the banking sector to insulate their balance sheets from a perceived market correction. The de-rating has created a ‘Settlement Trap’, transferring the entire liquidity risk to the most leveraged market participants: First Home Buyers (FHBs) utilising 5% deposit schemes.

For property professionals, this is an elevated structural adjustment. The valuation gap is triggering cash calls of $60,000 to over $90,000, sums that present a material coverage challenge for the average FHB, leading to a high probability of a material volume of settlement failures. While developers are attempting to plug this gap with significant rebates of up to $30,000, this is an unsustainable, temporary fix. This ‘subsidised settlement’ model confirms the underlying structural deficiency and creates elevated counterparty risk for developers, deal flow risk for brokers, and liability risk for agents advising on these assets. The off-the-plan sector in these key growth corridors is now operating under elevated structural pressure, with systemic risk being obscured by developer distress incentives.

Background & Strategic Context

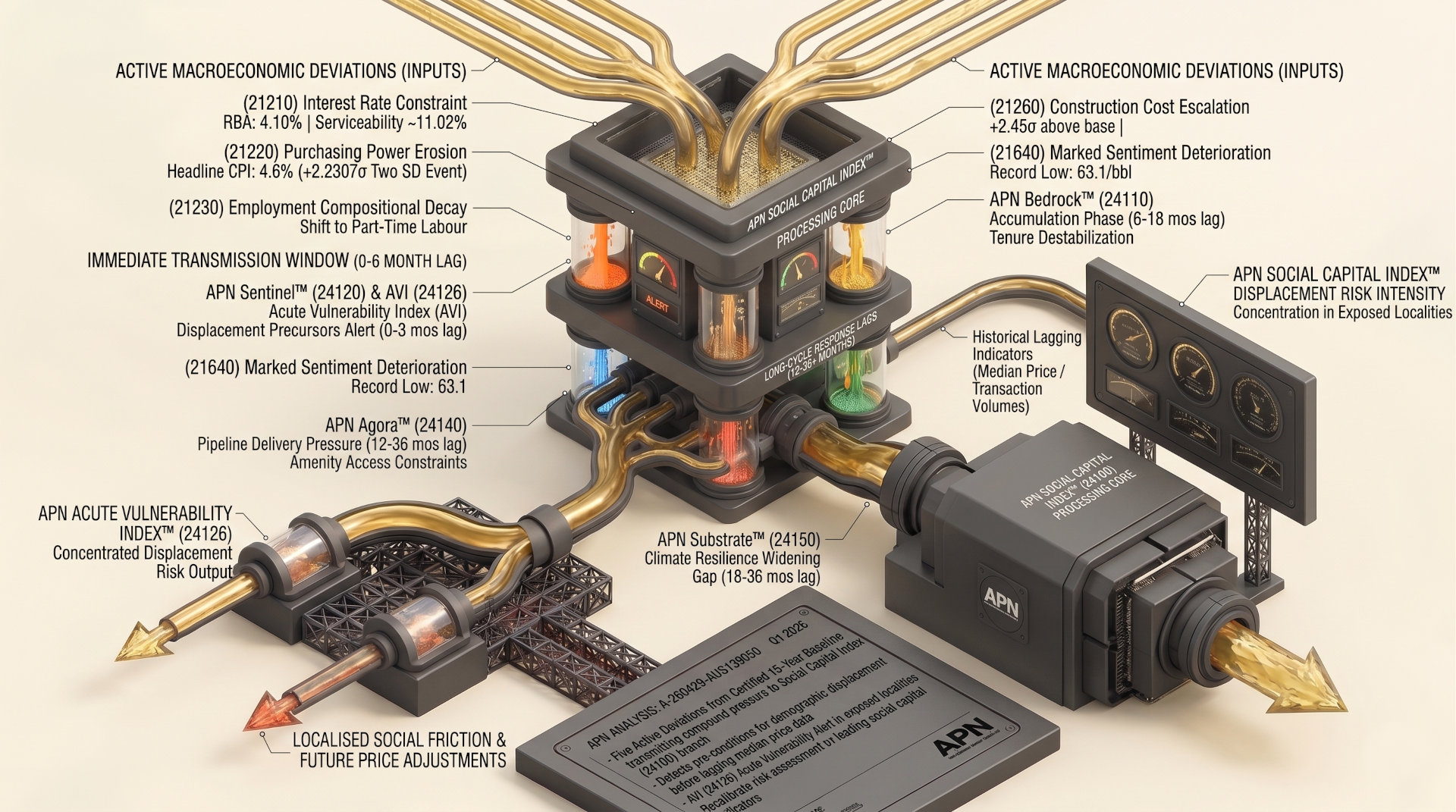

This event validates and calibrates APN’s core macro-thesis that state-level intervention is the primary force shaping market boundaries and outcomes. The Federal Government’s expansion of low-deposit schemes, intended as a stimulus, has intersected with the banking sector’s risk aversion in a decelerating market, creating a structural constraint for the cohort the policy was designed to help.

A clear example of state-led market distortion (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The expansion of the 5% First Home Guarantee Scheme acted as a substantive demand-side stimulus, encouraging buyers into the market with minimal equity. This government intervention created the conditions for the ‘Settlement Trap’ by enabling high-leverage purchases that lacked the cash buffers to withstand the expected valuation conservatism of a decelerating market.

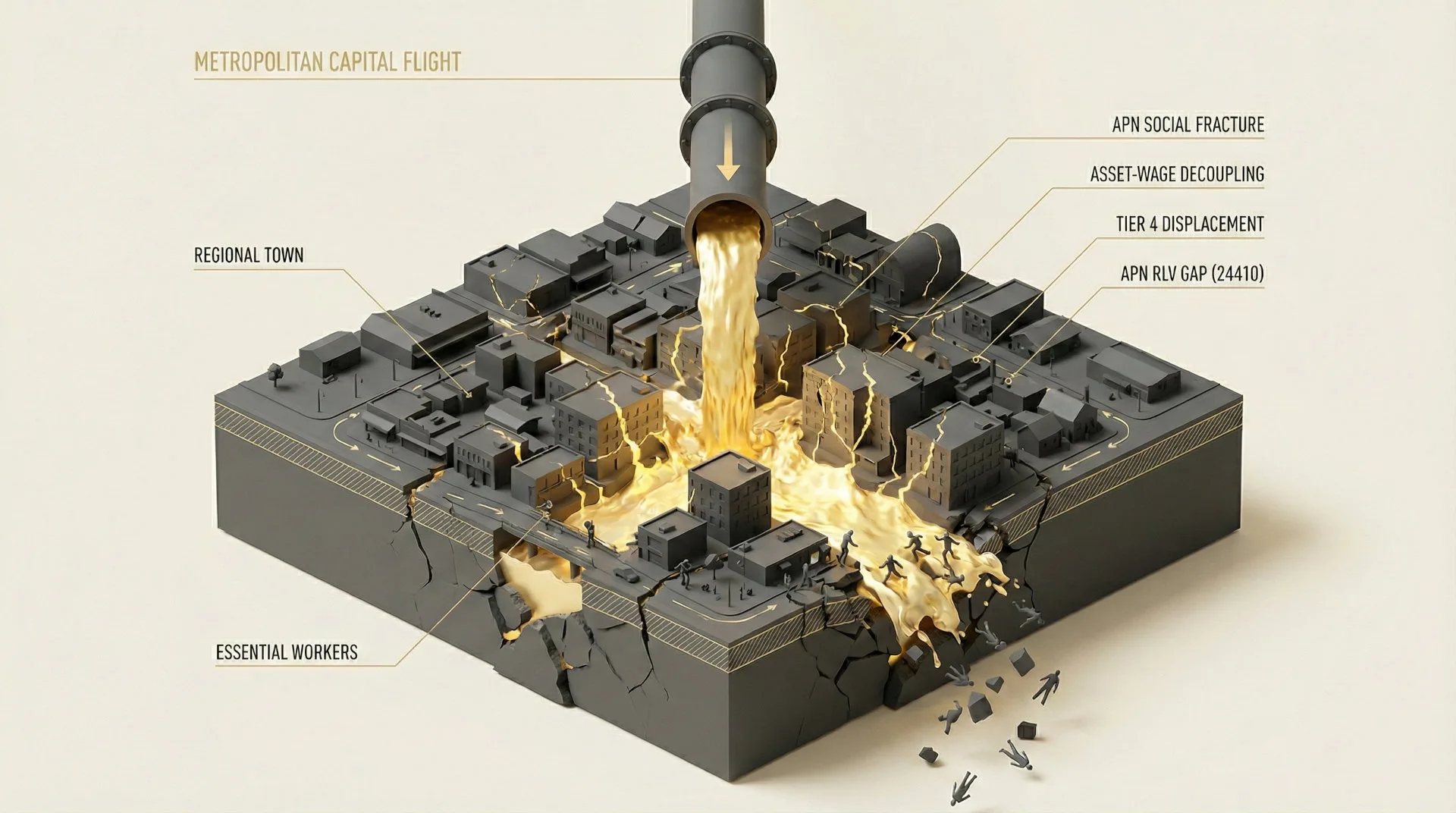

The transfer of risk to the most leveraged cohort: The ‘Valuation Air-Gap’ is a clear manifestation of the mechanism by which risk is transferred from institutional balance sheets (the banks) to the most financially exposed participants (5% deposit FHBs). While incumbent asset holders remain insulated by undersupply in the established market, new entrants are bearing a disproportionate financial impact of the market correction, facing potential insolvency before even taking possession.

A deficiency in supply-side planning (APN Future Development Pipeline Index™ – 24400): The geographic concentration of this structural pressure point in Western Sydney and Melbourne’s North highlights an elevated deficiency in matching supply with sustainable demand. These corridors, flagged by the APN Index as having a high volume of stock coming to completion, have become localities of concentrated risk. The oversupply of generic stock has materially eroded the ‘new build premium’ and given valuers the justification to de-rate assets substantively.

The regulatory gatekeepers respond (APN Risk & Compliance Index™ (24200)): The banking sector’s defensive posture, executed through their panel valuation networks, is a direct manifestation of a tightening risk and compliance environment. Lenders and valuers are acting as the market’s risk gatekeepers, responding to the ‘paradox’ of ineffective rate cuts and softening sub-markets by reverting to conservative, backward-looking valuation methodologies that prioritise the protection of their loan books over the validation of developer-set contract prices.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing synthesising real-time credit velocity data, valuation variance statistics, and developer marketing active in January 2026. The key facts are:

- Valuation De-Rating Quantified: The variance between contract price and settlement valuation has structurally adjusted from a historical baseline of -2% to a systemic de-rating of -10% to -15% for off-the-plan assets in high-supply corridors. This is driven by valuers removing the ‘new build premium’ and using softening comparable sales data.

- Macroeconomic Paradox: Despite a 75-basis point RBA cash rate cut to 3.60%, asset prices in the target sub-markets have failed to respond. Cotality data shows a -0.1% decline in Sydney and Melbourne values in December 2025, creating an adverse market environment for assets contracted 12-24 months prior.

- The ‘Settlement Trap’ Mechanism: For a typical $800,000 off-the-plan purchase with a 5% ($40,000) deposit, a 12% valuation shortfall ($704,000 valuation) results in the bank reducing its loan amount, creating an immediate cash call for the buyer of over $91,000 to complete the purchase.

- Developer Response: Major developers, including Rawson Communities and Metricon, are openly advertising settlement rebates of up to $30,000. This is an implicit acknowledgement of the valuation gap and an attempt to provide buyers with the equity needed to prevent widespread contract rescissions.

Critical Analysis & Balanced View

The ‘Settlement Trap’ represents a fundamental paradox: a government policy designed to improve housing accessibility has become a mechanism for financial distress. The 5% deposit scheme, while successful in boosting origination volumes, has created a cohort of buyers with elevated vulnerability to valuation volatility. The scheme’s architecture fails to account for the ‘exit risk’ at settlement in a market that is no longer uniformly rising.

The developer rebates are an elevated, second-order effect. While they appear as a marketing incentive, they are indicators of structural pressure that function as a form of non-standard vendor finance. By subsidising the buyer’s equity shortfall, developers are protecting the headline contract price to avoid adversely affecting the comparable sales data for their remaining stock. This practice obscures the true market clearing price, creating a temporary support level and delaying a more transparent market correction. However, this ‘Vendor Finance Plug’ is a finite solution. A valuation gap that exceeds the rebate amount (e.g., a 15% / $120,000 shortfall on an $800,000 asset) will still result in settlement failure, as the buyer cannot bridge the remaining gap.

This creates a self-reinforcing structural condition. Initial valuation shortfalls force developers to offer rebates. These rebated sales, if correctly interpreted by valuers as a net price reduction, then become the new, lower comparable sales data. This new data is then used to justify even lower valuations on the next tranche of settlements, widening the air-gap and increasing the pressure on the entire development pipeline. The capital reallocation toward lower-risk assets noted by valuation firms further exacerbates this, constraining their access to the liquidity needed to stabilise.

Strategic Implications for Property Professionals

- For Developers: Immediately stress-test your settlement pipeline against a minimum 15% valuation shortfall scenario. Proactively engage with your financiers and purchasers in high-risk corridors. Factor rebate strategies and the potential cost of rescissions into project feasibility and cash flow forecasting for all future projects.

- For Mortgage Brokers & Lenders: Your duty of care has escalated. Flag all clients with low-deposit, off-the-plan loans settling in the next 6-12 months as high-risk. You must proactively communicate the potential for a material cash shortfall at settlement and explore contingency options, rather than awaiting an adverse valuation outcome.

- For Agents & Buyers’ Agents: Your professional indemnity risk has increased. Mandate elevated due diligence for any client considering an off-the-plan purchase, particularly in greenfield or high-density areas. Your advice must now include a quantified analysis of the ‘Settlement Trap’ risk, and you must ensure clients have cash buffers significantly exceeding the minimum deposit requirement.

- For Valuers: Maintain your conservative stance. The de-rating is a necessary and defensible market correction. Your primary duty is to the lender. Ensure meticulous documentation of comparable sales, including any evidence of rebates or incentives that affect the net sale price, to defend your assessments against expected pressure from developers.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the APN Sovereign Policy Composite Index™ (SPCI, 24800), demonstrating how state-led stimulus (5% deposit schemes) can create material, unintended market distortions. It also confirms the mechanics by which systemic risk is transferred to the most leveraged, least-resourced market participants.

- Index Calibration: The APN Future Development Pipeline Index™ (24400) is recalibrated for Western Sydney and Melbourne’s North to increase the risk weighting for projects with high exposure to the FHB cohort. The APN RLV Gap™ (24410) is widened to explicitly model ‘developer rebates’ as a mandatory project cost line item in these corridors, reducing the viability of future supply.

- Data Capture: This analysis triggers a new data capture mandate under the APN Symbiotic Intelligence Network™ (24310). The mandate is to systematically track the volume, value, and geographic concentration of developer rebates and ‘nomination sales’ as a primary leading indicator of settlement pipeline stress and market liquidity structural adjustments.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.