Regulatory Velocity: How the Insurance Industry’s Climate Unintegrated Risk Assessment is Initiating State Intervention

APN ANALYSIS: A-251126-AUS131172

Executive Summary

The Australian general insurance sector is exhibiting a material and structurally adverse disconnect between sentiment and reality. A landmark 2025 industry survey reveals that insurers have demoted ‘Climate Change’ from a top-three concern to a low-priority #10 risk, despite escalating physical losses. This is not a sign of successful adaptation but of concentrated desensitisation to risk and a strategic distraction by technological threats like AI and cyber crime. Concurrently, ‘Political Risk’ has accelerated growth to become the #4 concern, driven by the threat of restrictive government intervention in the insurance market. This substantive reordering of priorities matters because the industry’s attempt to price-in climate risk through material escalation in premiums has exceeded the public’s acceptance threshold, initiating the very political regulatory intervention it now anticipates structural pressure from. The sector has functionally externalised climate liability to the state, but in doing so, has invited material systemic regulatory pressure that threatens its fundamental business model.

For property professionals, this shift from a physical risk environment to a political risk environment is a paradigm change. The primary threat to asset value and development feasibility is no longer just a flood or fire, but an Act of Parliament. The potential for the government to expand its reinsurance pool to cover all perils, impose price caps, or declare development moratoriums introduces a substantive new layer of uncertainty. Valuations, due diligence, and risk modelling must now account for ‘regulatory climate risk’, where an asset’s future is determined as much by decisions made in Canberra as by its exposure to the elements.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses, demonstrating that state-level intervention is a primary determinant of market outcomes. The dynamic confirms that when private market mechanisms collide with public affordability, **APN Sovereign Policy Composite Index™ (SPCI, 24800)** is activated to redraw market boundaries. The entire feedback loop, from premium hikes to political action, is a characteristic instance of the **APN Climate-Risk Asset Devaluation Index™ (24500)** in motion, proving that regulatory response is a primary component of climate-related financial risk.

- The APN Sovereign Policy Composite Index™ (SPCI, 24800) Manifestation: The accelerated growth of ‘Political Risk’ to the #4 rank is a direct market signal that the industry anticipates a significant **APN Sovereign Policy Composite Index™ (SPCI, 24800)** event. The anticipation is no longer of routine compliance but of structurally significant intervention, where the government moves from being a regulator to a market nationaliser, fundamentally altering the rules of property insurance.

- The Exceedance of APN Financial Climate Sensitivity™ (APN Financial Climate Sensitivity™ (24510)): The entire dynamic is catalysed by exceeding the threshold of **APN Financial Climate Sensitivity™**. The ACCC’s finding that premiums ‘remain very high and are generally rising’ even after interventions confirms that the affordability threshold for a critical mass of voters has been crossed, forcing a political reaction and validating the core mechanism of our index.

- The Velocity Indicator (APN Regulatory Velocity Multiplier™ (APN RVM™) (24210)): The material inversion of risk rankings, Climate Change falling 7 places as Political Risk rises 4, is a quantifiable measure of an accelerating **APN RVM™**. The industry correctly perceives that the velocity of regulatory threats (Treasury reviews, Senate inquiries) is now a more immediate and significant force than the velocity of physical climate change, a core tenet of our **APN Risk & Compliance Index™ (24200)** framework.

- The Complacency Metric (APN Professional Sentiment Index™ (24300)): The PwC survey data provides a critical input, revealing a structurally adverse ‘Sentiment/Reality Decoupling’. The 6.6% ‘Preparedness Gap’ and the downgrading of climate risk amidst real-time material adverse events like CAT 255 are psychometric indicators of sub-optimal risk integration and resource allocation, which the index is designed to capture as a leading indicator of systemic vulnerability.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the PwC Insurance Banana Skins 2025 report (Australian Chapter) and corroborating government and industry data from Q3/Q4 2025. The key facts are:

- The Substantive Reordering of Priorities: In the Australian insurance industry’s risk hierarchy, ‘Climate Change’ materially contracted from the #3 concern in 2023 to #10 in 2025. Simultaneously, ‘Political Risk’ accelerated growth from #8 to #4, indicating a fundamental shift in perceived threats.

- The Technological Distraction: The top three risks are now dominated by technology, with ‘Cyber Crime’ at #1, ‘Technology’ at #2, and ‘Artificial Intelligence’ making a notable advancement to #3 (from #11), consuming executive attention and resources.

- The Preparedness Gap: Australian insurers scored 6.6% lower on the Preparedness Index than their global counterparts, revealing a significant challenge to their assessment confidence in their ability to manage the risks they have identified as most pressing.

- The Regulatory Trigger: The material escalation in ‘Political Risk’ is a direct response to specific government actions in late 2025, primarily the Treasury’s statutory review of the Cyclone Reinsurance Pool and explicit considerations to expand it to cover all natural disasters nationwide.

- The Sentiment/Reality Decoupling: At the exact time the industry was finalising its low ranking for climate risk, ‘Catastrophe 255’ was declared for severe hailstorms in South East Queensland, generating over 16,000 claims in 48 hours and exposing a structurally adverse unintegrated risk assessment between executive sentiment and physical reality.

Critical Analysis & Balanced View

The Australian insurance industry faces a self-generated paradox. Its primary strategy for managing climate risk—material escalation in premiums—has successfully protected balance sheets in the short term but has structurally significantly failed in the long term by initiating its primary anticipated structural pressure: political intervention. The downgrading of climate risk to #10 is not strategic foresight; it is a psychological phenomenon of ‘risk fatigue’ and the ‘normalisation of deviance’, where billion-dollar material adverse events are now considered business as usual.

This has created a structurally adverse ‘attentional displacement’. The C-suite is rationally focused on the high-velocity operational risks of AI and cybercrime, but this has resulted in a lack of focus on the more fundamental, structurally significant threat posed by regulation. They are meticulously fortifying digital security protocols while the government is drafting legislation to fundamentally reconfigure the operational parameters of the industry. The industry’s belief that it has ‘priced in’ climate risk is a fallacy; it has merely transformed a physical risk it can model into a political risk it cannot control.

The balanced view is that insurers are constrained. Escalating global reinsurance costs and climate volatility necessitate higher premiums, yet the government, facing an electorate materially affected by cost-of-living pressures, cannot tolerate the socio-economic consequences of mass uninsurability. The industry’s current path is unsustainable, leading directly to a materially constraining regulatory outcome. The only way forward is to pivot from a strategy of risk transfer (pricing) to one of proactive risk reduction and constructive engagement with the government on solutions like the ‘All Perils’ pool, lest a solution be imposed upon them.

Strategic Implications for Property Professionals

- For Developers & Planners: Your risk modelling must now include a ‘Regulatory Intervention’ variable. The threat of an ‘All Perils’ government reinsurance pool could rapidly render previously uninsurable areas viable, while also bringing the risk of government-imposed development moratoriums in those same ‘elevated risk localities’. Feasibility studies based solely on physical climate risk are now structurally incomplete.

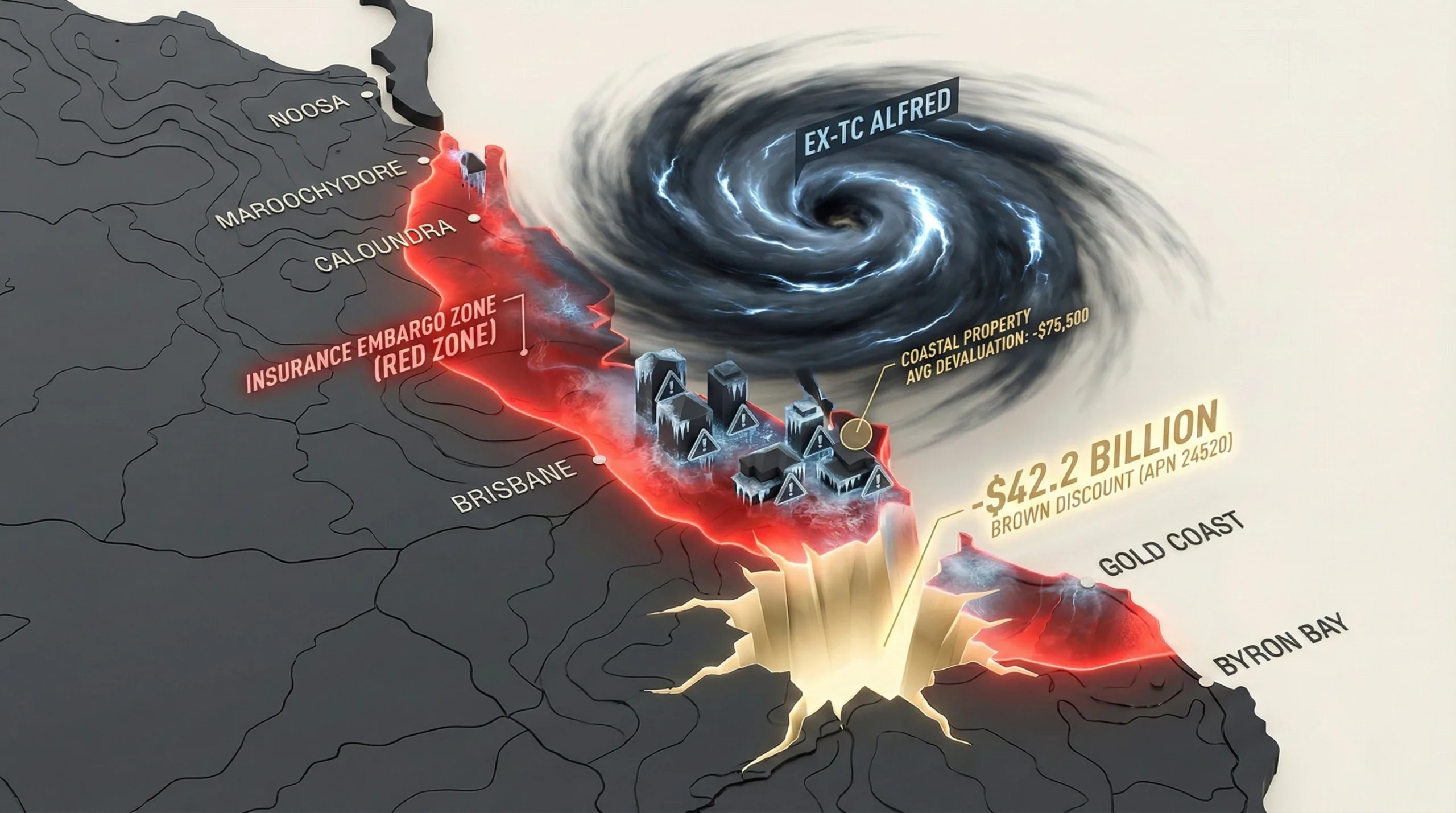

- For Valuers & Lenders: Asset valuation must incorporate a ‘Political Risk’ discount, particularly in climate-vulnerable postcodes. An asset’s insurability is no longer a given. Scrutinise not just the current premium, but the area’s vulnerability to being identified by future government schemes, price caps, or insurance embargoes. The potential for market reconfiguration akin to that observed in Florida, with state intervention dictating terms, could initiate rapid and material valuation disturbances.

- For Agents & Buyers’ Agents: Client advisory must evolve beyond physical risk disclosure. The critical question is now, ‘Is this postcode on Canberra’s radar for regulatory intervention?’. Disclosing the political and regulatory risks associated with insurance affordability and availability is a new, essential component of due diligence and fiduciary duty to protect your clients from future financial constraint.

- For Asset & Portfolio Managers: The ‘Brown Discount’ on climate-exposed assets is accelerating, driven more by regulatory threat than immediate physical risk. Portfolios with high concentrations in vulnerable regions face concurrent risk factors: the physical event and the subsequent political regulatory intervention. De-risking strategies must now prioritise assets in locations with demonstrable adaptive capacity (**APN Substrate™**) and a lower political profile.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core mechanism of **APN Sovereign Policy Composite Index™ (SPCI, 24800)**, confirming that the threat of state intervention is a primary market-shaping force. It also validates the direct causal link between **APN Financial Climate Sensitivity™ (24510)** reaching a critical threshold and the activation of regulatory risk tracked by **APN Risk & Compliance Index™ (24200)**.

- Index Calibration: The **APN Regulatory Velocity Multiplier™ (APN RVM™) (24210)** is calibrated upwards for the general insurance and property finance sectors, reflecting the accelerated pace of government reviews and legislative threats. The **APN Climate-Risk Asset Devaluation Index™ (24500)** is adjusted to increase the weighting of ‘Political Intervention Risk’ as a key component of an asset’s overall risk profile.

- Data Capture: This analysis triggers a new data capture mandate under the **APN Symbiotic Intelligence Network™ (24310)** to specifically track and quantify industry and political sentiment regarding the ‘All Perils’ pool expansion. This involves monitoring submissions to the Treasury review and statements from key stakeholders to provide a leading indicator of the likely regulatory outcome.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.