H1 2025 Data Validates $42.2 Billion ‘Brown Discount’ as Insurance Embargoes Create Uninsurable Coastal Assets

APN ANALYSIS: A-251124-AUS131033

Executive Summary

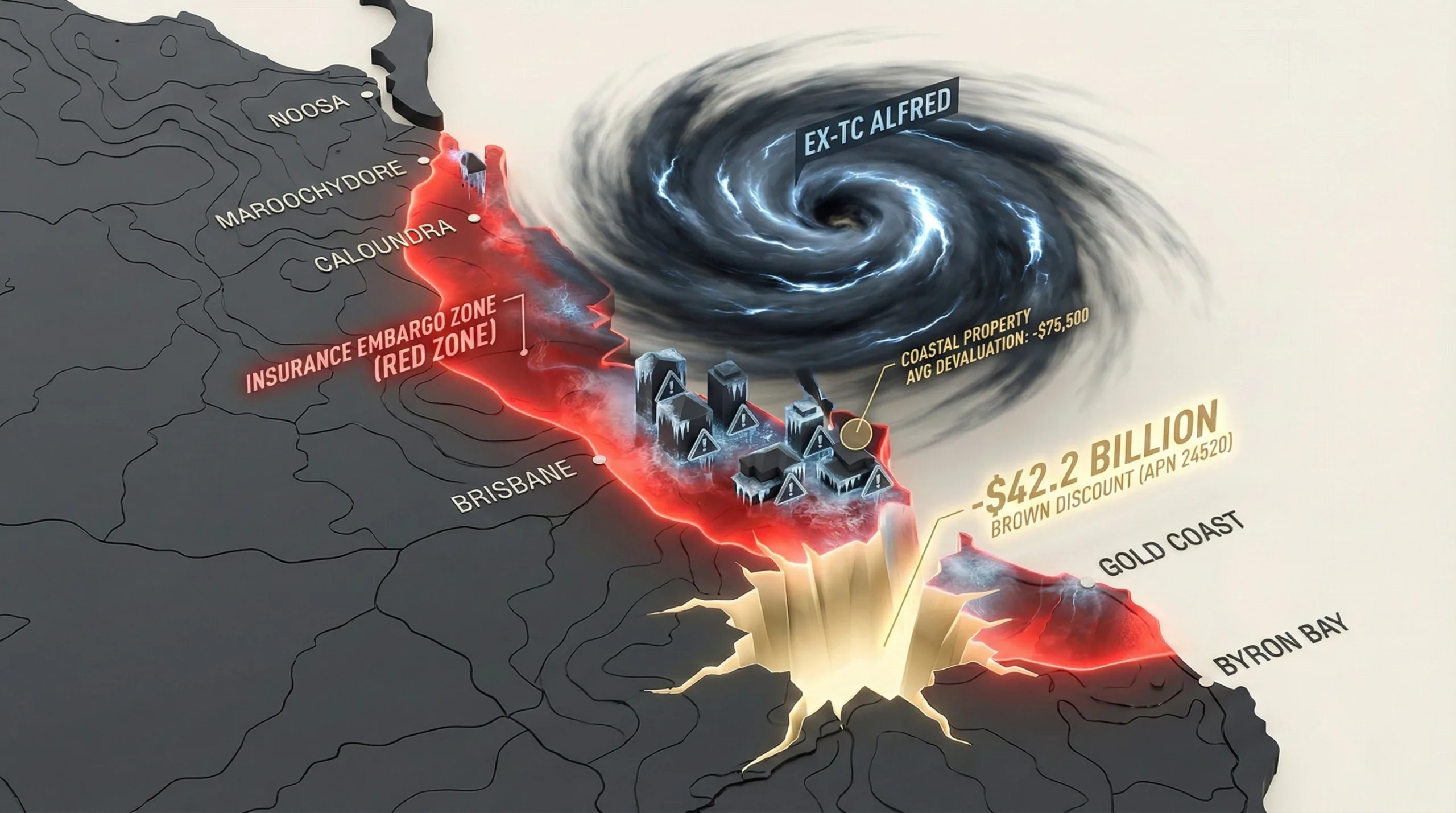

The H1 2025 material adverse event season, dominated by the financial and meteorological impact of Ex-Tropical Cyclone Alfred, has empirically validated the structural repricing of Australian coastal assets due to climate risk. This represents a shift from a forecast to a realised $42.2 billion devaluation, termed the “Brown Discount,” which is now embedded in the transactional history of the national property market. This market dislocation has been accelerated by the activation of contiguous “Red Zones”, most notably the Noosa to Byron Bay corridor, which experienced total insurance embargoes, constraining capital liquidity and creating a new, structurally exposed class of uninsurable properties.

For property professionals, this market dislocation creates both elevated peril and distinct opportunity. The confirmation of a $75,500 average devaluation for at-risk properties necessitates an immediate recalibration of valuation models to avoid professional negligence. Furthermore, the emergence of “meteorological settlement risk”, where deals collapse due to short-notice insurance embargoes, demands a fundamental overhaul of conveyancing due diligence and contract structuring to mitigate structurally significant losses for buyers and their agents.

Background & Strategic Context

This analysis validates and calibrates APN’s core macro-theses on market intervention and risk. The H1 2025 data provides empirical evidence that state-level actions and regulatory frameworks are the primary drivers shaping the boundaries of asset viability, creating a material divergence between climate-exposed and climate-resilient markets.

The State as the Ultimate Arbiter of Value (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The establishment of the Cyclone Reinsurance Pool (CRP) versus the un-pooled risk of pluvial flooding is a textbook example of state intervention creating market structural adjustments. The government’s decision to cover cyclonic wind but not the subsequent “soak” event directly led to the insurance “coverage gap” and the premium volatility observed, demonstrating that state policy, not just weather, defines asset risk.

Quantifying Financial Vulnerability (APN Climate-Risk Asset Devaluation Index™ – 24500): The $42.2 billion devaluation figure moves climate risk from an abstract concept to a quantifiable financial metric. The analysis confirms the existence of a material APN Brown Discount™ (24520), which is now being priced into transactions, validating the core purpose of the index: to calculate the APN Financial Climate Sensitivity™ (24510) of assets.

The Insurability Structural Pressure Point as a Systemic Condition: The “Noosa to Byron Bay” embargo zone demonstrates the inability of the private insurance market to function as a risk transfer mechanism in high-exposure corridors. This systemic condition shifts the ultimate liability from private capital to the taxpayer via disaster relief payments, creating a long-term fiscal burden and validating this core thesis.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Insurance Council of Australia’s H1 2025 data, the PropTrack/Climate Council “Property Value Flood Risk Report,” and insurer communications during Ex-Tropical Cyclone Alfred. The key facts are:

- Total H1 2025 Insured Loss: The total insured cost of elevated weather events reached over $1.8 billion from 148,437 claims, establishing a new, sustained baseline of attrition for the insurance sector.

- Dominance of Ex-TC Alfred: This single “hybrid” weather event was responsible for $1.36 billion (75.5%) of the total loss from over 125,000 claims, highlighting the market’s vulnerability to complex cyclone-trough systems that blur the lines of insurance coverage.

- The “Brown Discount” Quantified: A national-scale analysis empirically confirmed a $42.2 billion aggregate loss in residential property values due to flood risk, with an average devaluation of $75,500 for an at-risk three-bedroom home.

- The “Red Zone” Validated: A contiguous insurance embargo zone was activated from Noosa to Byron Bay, structurally constraining property transactions and creating a “conveyancing structural pressure point” for buyers who were unable to secure insurance cover post-contract and pre-settlement.

- The Premium Paradox: Despite official reports of premium reductions due to the Cyclone Reinsurance Pool, the effective “total cost of risk” for property owners, particularly in strata complexes, has increased by 15-25% due to increases in non-cyclone perils like flood and rising construction costs.

Critical Analysis & Balanced View

The primary insight from this analysis is the “Pool Illusion.” The Cyclone Reinsurance Pool (CRP) has created an inaccurate perception of comprehensive risk mitigation by addressing only one component (cyclone wind) of a multi-faceted risk profile. Insurers, having paid out $1.36 billion for Ex-TC Alfred’s “hybrid” flood damage, are now systematically re-pricing the un-pooled water risk, leading to the 15-25% premium increases experienced by property owners. This explains the paradox between the ACCC’s reported premium decreases and the commercial reality of higher renewal costs.

Furthermore, the ~$500 million discrepancy between initial loss estimates and final insured payouts represents a direct cost transfer from insurer balance sheets to household balance sheets. This “deductible gap” is not a saving; it is a progressive reduction of household equity that directly contributes to the $42.2 billion Brown Discount. This devaluation is most material in absolute dollar terms in prestige suburbs like Chelmer in Brisbane ($303,000 average loss) and Pitt Town in Sydney ($363,500 average loss), indicating that climate risk is a significant factor in wealth reduction in the upper quartiles of the market, creating a progressive structural deterioration of state government fiscal positions as their stamp duty revenue base erodes.

Strategic Implications for Property Professionals

- For Valuers & Lenders: Valuation models must be immediately updated to incorporate the empirically validated APN Brown Discount™ (24520), starting with the $75,500 baseline. Relying on historical comparable sales in at-risk zones without explicit climate-risk adjustment now constitutes a significant professional liability risk.

- For Agents & Conveyancers: The “uninsurable settlement constraint” is a new and material risk. The insertion of “subject to insurance” clauses into contracts of sale for properties within or near potential embargo zones is now indicated as a necessary risk-mitigation strategy. Due diligence must now include monitoring meteorological forecasts and insurer embargo statuses in the 7-14 day settlement window.

- For Developers & Planners: The “Noosa to Byron” embargo serves as a market-defined boundary for unviable development. Future projects within these “Red Zones” face elevated financing and insurance hurdles. The focus must shift to demonstrating resilience through design (improving the APN Substrate™ rating) to secure capital and future insurability.

- For Strata & Asset Managers: Budgeting for insurance renewals at CPI is no longer viable. Portfolios with coastal exposure must forecast premium increases of 15-25% annually as a baseline. Proactive investment in property-level resilience measures is now critical to mitigate premium increases and maintain asset yield.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides empirical validation for the APN Climate-Risk Asset Devaluation Index™ (24500). The $42.2 billion devaluation figure confirms the existence and scale of the APN Brown Discount™ (24520), while the “Noosa to Byron” embargo map provides a real-world geofence for high APN Financial Climate Sensitivity™ (24510) zones.

- Index Calibration: The APN Brown Discount™ (24520) metric is now calibrated with a national baseline of -$75,500 for a standard residential asset in a flood-risk zone, with higher weightings for prestige riverfront and coastal postcodes. The APN Substrate™ (24150) rating will be weighted more heavily based on the demonstrated link between flood mapping and insurance embargo activation.

- Data Capture: This event triggers a new data capture mandate for the APN Symbiotic Intelligence Network™ (24310) to track insurer embargo notices (binding suspensions) in real-time. This data will be used to dynamically map “Red Zones” and provide leading indicators of asset illiquidity for subscribers.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.