IAG Data Validates APN Sovereign Policy Composite Index™ (SPCI, 24800) as Insurers Acknowledge State Dependency to Maintain Commercial Viability

APN ANALYSIS: A-251124-AUS130996

Executive Summary

Insurance Australia Group’s (IAG) latest climate report provides empirical evidence that the Australian insurance sector has crossed a financial rubicon. The report confirms a 67% increase in insured costs from elevated-severity weather over the preceding five years, totalling $22.5 billion. This is not a statistical anomaly but the direct financial consequence of climate change-driven “compound events” that are disproportionate to traditional actuarial models. Notably, the report identifies Australia’s economic heartland—the Brisbane-Sydney-Melbourne (BSM) corridor—as the new primary locus for escalating hail and flood risk, rendering the historical “safe harbour” narrative for southern capitals no longer structurally viable. This structural dislocation validates APN’s thesis that the private insurance market can no longer function without direct state intervention, forcing a strategic pivot to reliance on government-funded mitigation to maintain commercial viability.

For property professionals, this is a signal that climate risk has transitioned from a theoretical ESG concern to a primary driver of asset value and financial liability. The data confirms that asset values in previously ‘blue-chip’ metropolitan zones are now directly contingent on public spending and political will, introducing a new, complex layer of risk to every portfolio. The widening “protection gap,” where up to 80% of high-risk properties are uninsured for key perils, means a significant portion of the market consists of “hollow assets”, valuable on paper but with zero recovery value in a structural dislocation. Understanding this new dynamic is no longer optional; it is fundamental to valuation, development, and advisory in the Australian market.

Background & Strategic Context

The release of IAG’s third “Severe Weather in a Changing Climate” report is a material validation event, providing the empirical data required to calibrate APN’s core macro-theses on the Australian property market. The report’s findings move the conversation from academic modelling to commercial reality, confirming that state intervention is now the central pillar of market stability and risk management, a direct manifestation of the forces tracked by APN’s proprietary frameworks.

The State as Insurer of Last Resort (APN Sovereign Policy Composite Index™ (SPCI, 24800)): IAG’s explicit endorsement of the Federal Government’s $350 million Disaster Ready Fund is a public acknowledgement that the private insurance market’s solvency is now contingent on public capital. By linking insurance affordability directly to taxpayer-funded mitigation projects like levees and seawalls, the industry confirms the core thesis of the APN Sovereign Policy Composite Index™ (SPCI, 24800): state action, not market forces, now defines the boundaries of insurability and, by extension, property value.

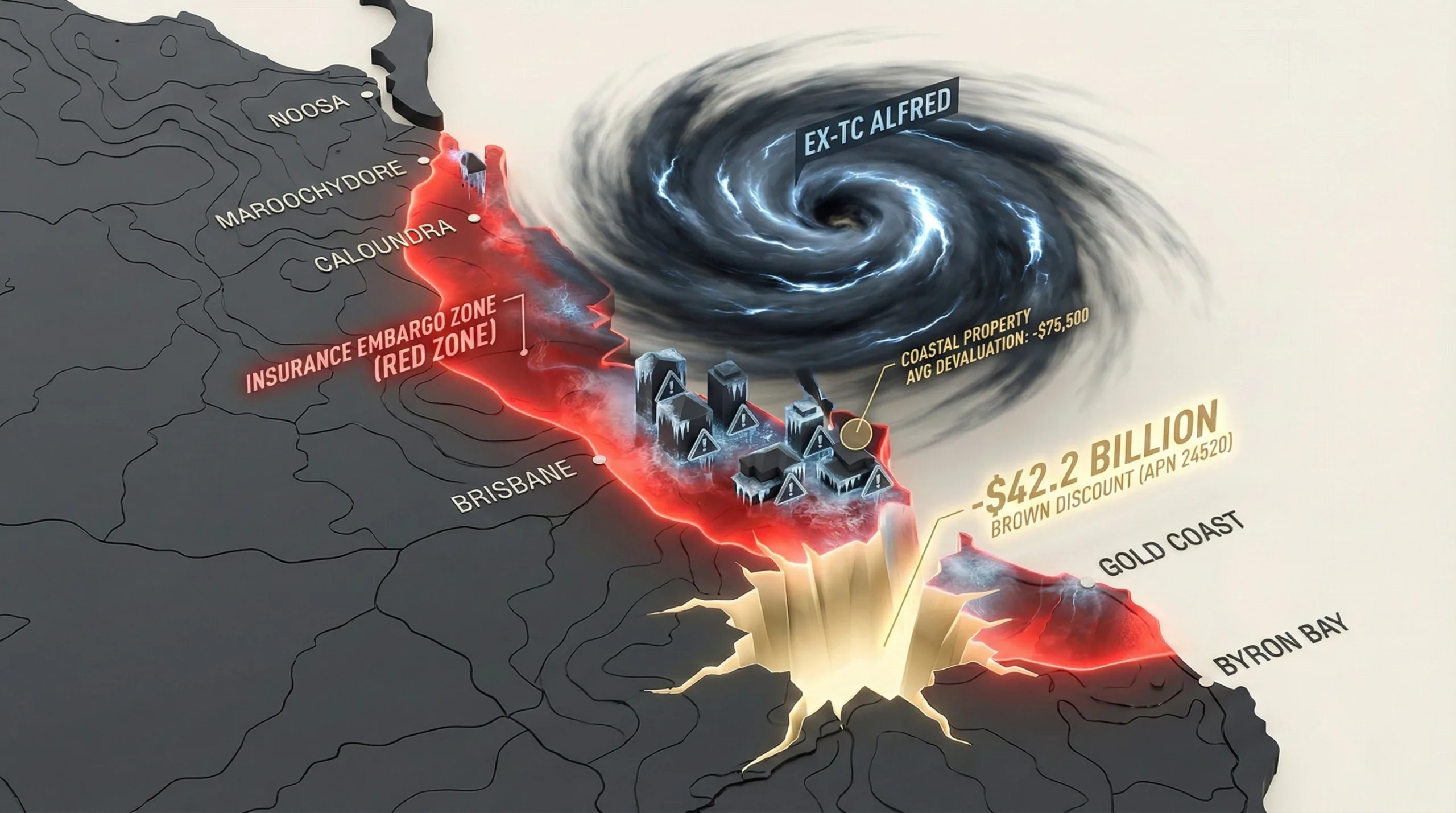

The Financialisation of Physical Risk (APN Climate-Risk Asset Devaluation Index™ 24500): The 67% cost increase and the identification of the BSM corridor as a new hail risk primary locus provide the financial and geographic inputs for the APN Brown Discount™. This is no longer a future projection; it is a quantifiable, escalating financial liability. Assets within these zones, previously considered low-risk, now carry a measurable risk premium that will erode capital value and place pressure on lending serviceability.

The Erosion of Foundational Resilience (APN Substrate™ 24150): The structurally significant “protection gap,” with 80% of high-risk flood properties effectively uninsured, represents a market failure that directly degrades community-level resilience. This erosion of the financial safety net that underpins property value is a material negative input for the APN Substrate™ rating. It signals that in the event of a structural dislocation, the economic shock will not be absorbed by insurers but will fall directly on households, lenders, and ultimately the taxpayer, presenting a risk to the stability of entire postcodes.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of Insurance Australia Group’s (IAG) third “Severe Weather in a Changing Climate” report, released November 2025, in conjunction with associated CEO statements, regulatory filings, and industry data. The key facts are:

- $22.5 Billion Cost Escalation: The insurance industry paid $22.5 billion in insured costs for elevated-severity weather events over the past five years, a 67% increase on the previous quinquennial period. This acceleration far outstrips inflation and is driven by event frequency and severity.

- Geographic Risk Inversion: The Brisbane-Sydney-Melbourne (BSM) corridor, Australia’s most populated region, is now experiencing the fastest increase in large-to-giant hailstone risk, inverting historical models that focused on tropical northern Australia.

- State Dependency Confirmed: IAG’s CEO publicly linked future insurance affordability and availability to government spending via the $350 million Disaster Ready Fund, formalising the industry’s reliance on taxpayer-funded mitigation infrastructure.

- Structurally Significant Protection Gap: Industry data confirms up to 80% of homes in high-risk flood zones lack flood insurance. Furthermore, 80% of the broader market is underinsured for total replacement cost, exposing the economy to material contingent liabilities.

- Reinsurance Capital Retreat: Global reinsurers have resulted in structural changes to IAG’s 2025 catastrophe program, including the non-renewal of “aggregate drop-down” covers. This signals a retreat of capital from covering frequent, mid-sized Australian weather events, shifting more risk back to primary insurers and their customers.

Critical Analysis & Balanced View

The convergence of these data points reveals a structural paradox at the heart of the Australian property market: as physical risk escalates, the primary mechanism for managing that risk, private insurance, is systematically retreating. This creates a class of “hollow assets” that are traded at market values, which fail to account for their uninsurable status and near-total loss potential. The IAG report is less a forecast and more a lagging indicator of a market that has already undergone a structural adjustment.

The further insight lies in the dynamic of reactive mitigation. The government’s Disaster Ready Fund is an attempt to de-risk the built environment, but the report’s focus on “compound events” and new perils like “fire tornadoes” suggests the climate baseline is shifting faster than mitigation infrastructure can be funded and built. This positions the government not as a temporary backstop, but as a permanent, non-discretionary subsidiser of the property and insurance sectors. The primary question for investors is no longer just ‘what is the physical risk?’, but ‘what is the political risk that this government subsidy will be withdrawn or prove insufficient?’. The private market’s viability is now a contingent variable of public policy.

Strategic Implications for Property Professionals

- For Developers & Planners: The viability of future projects is now directly tied to their alignment with government mitigation spending under the APN Sovereign Policy Composite Index™ (SPCI, 24800). Greenfield sites in high-risk zones without planned public infrastructure investment are effectively unbankable and carry a commercially unviable risk profile. Due diligence must now include a forward-looking assessment of state and federal mitigation pipelines.

- For Valuers & Lenders: The APN Brown Discount™ must now be systematically applied to assets within the BSM corridor, particularly those at the urban-bushland interface or in flood plains. The insurability status of a property is a material fact that must be reflected in valuations and lending security assessments, as an “uninsured” asset has a recovery value approaching zero in a material adverse event.

- For Agents & Buyers’ Agents: Disclosure of climate risk and insurability status has transitioned from best practice to a core fiduciary duty. Professionals must be prepared to advise clients on the escalating long-term holding costs (premiums, levies) and capital risks associated with properties in newly identified high-risk zones, as this now directly impacts an asset’s investment potential.

- For Asset & Portfolio Managers: Portfolio diversification must now incorporate granular, peril-based climate risk analysis. A portfolio with a high allocation to the BSM corridor, previously considered a low-risk allocation, now has a concentrated and rapidly escalating risk profile that requires active management, hedging, or strategic divestment.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the APN Climate-Risk Asset Devaluation Index™ (24500), confirming the direct financial impact of physical climate risk and its geographic concentration in the BSM corridor. It also provides primary evidence for the core thesis of the APN Sovereign Policy Composite Index™ (SPCI, 24800), confirming state dependency is now an explicit industry strategy.

- Index Calibration: The APN Brown Discount™ (24520) will be calibrated using the 67% insurance cost increase as a risk velocity metric. The geographic boundaries of the discount will be redrawn to reflect the BSM corridor’s status as a high-risk zone. The APN Substrate™ (24150) rating will be immediately downgraded for postcodes with a confirmed flood insurance protection gap exceeding 50%.

- Data Capture: This event triggers a new data capture mandate under the APN Symbiotic Intelligence Network™ (24310) to track insurance premium fluctuations, changes in policy deductibles and exclusions, and uninsured property sales data within the BSM corridor. This will serve as a high-frequency leading indicator of market pressure and capital retreat.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.