Buyers’ Agent Sector Structurally Overserved Following Disproportionate Expansion and Credit Tightening

APN ANALYSIS: A-260629-AUS140106

Executive Summary

The Australian buyers’ agent sector is undergoing a significant structural correction. Following a period of rapid expansion between 2016 and 2026 that saw practitioner headcount more than double to over 1,000, the market is now defined by structural oversupply. This growth occurred within a regulatory void, resulting in a market where over 85 per cent of participants operate without peak-body accreditation. This rapid inflation of service providers has converged with a material contraction in the buyer pool, driven by persistent macroprudential constraints—notably APRA’s 3.00 percentage point serviceability buffer—and a higher interest rate environment. The resulting decline in transaction velocity and mortgage conversion rates has rendered many high-volume, low-margin business models commercially unviable.

For property professionals, this analysis signals an impending market consolidation and a flight to quality. The current environment will be characterised by continued fee compression for undifferentiated services, an increase in corporate insolvencies among less-capitalised firms, and a reallocation of client capital towards experienced, accredited professionals. The key differentiator for sustainable practice is now the demonstrated ability to provide complex, quantifiable value—such as navigating regulatory hurdles and executing strategic off-market acquisitions—that transcends basic property search functions. Due diligence on a service provider’s credentials and business model is now as critical as due diligence on an asset.

Background & Strategic Context

This analysis validates and calibrates APN’s core thesis regarding the sensitivity of professional service industries to credit cycle dynamics. The buyers’ agent sector provides a clear case study of how rapid expansion during a period of accessible credit becomes unsustainable when monetary and macroprudential policies tighten. The divergence between practitioner headcount and executable transaction volume demonstrates how regulatory friction can structurally reshape a market, separating institutional-grade operators from a commoditised lower tier.

A Manifestation of Herd Behaviour (Market Psychology & Herd Behaviour (21620)): The influx of new practitioners into the buyer’s agent sector during the 2020–2022 accelerated acquisition cycle was a direct manifestation of herd behaviour, driven by the perception of high yields and low operational complexity. The resulting ‘accreditation gap’, where over 85% of practitioners operate outside peak-body oversight, illustrates a structural decoupling of market participation from established professional standards.

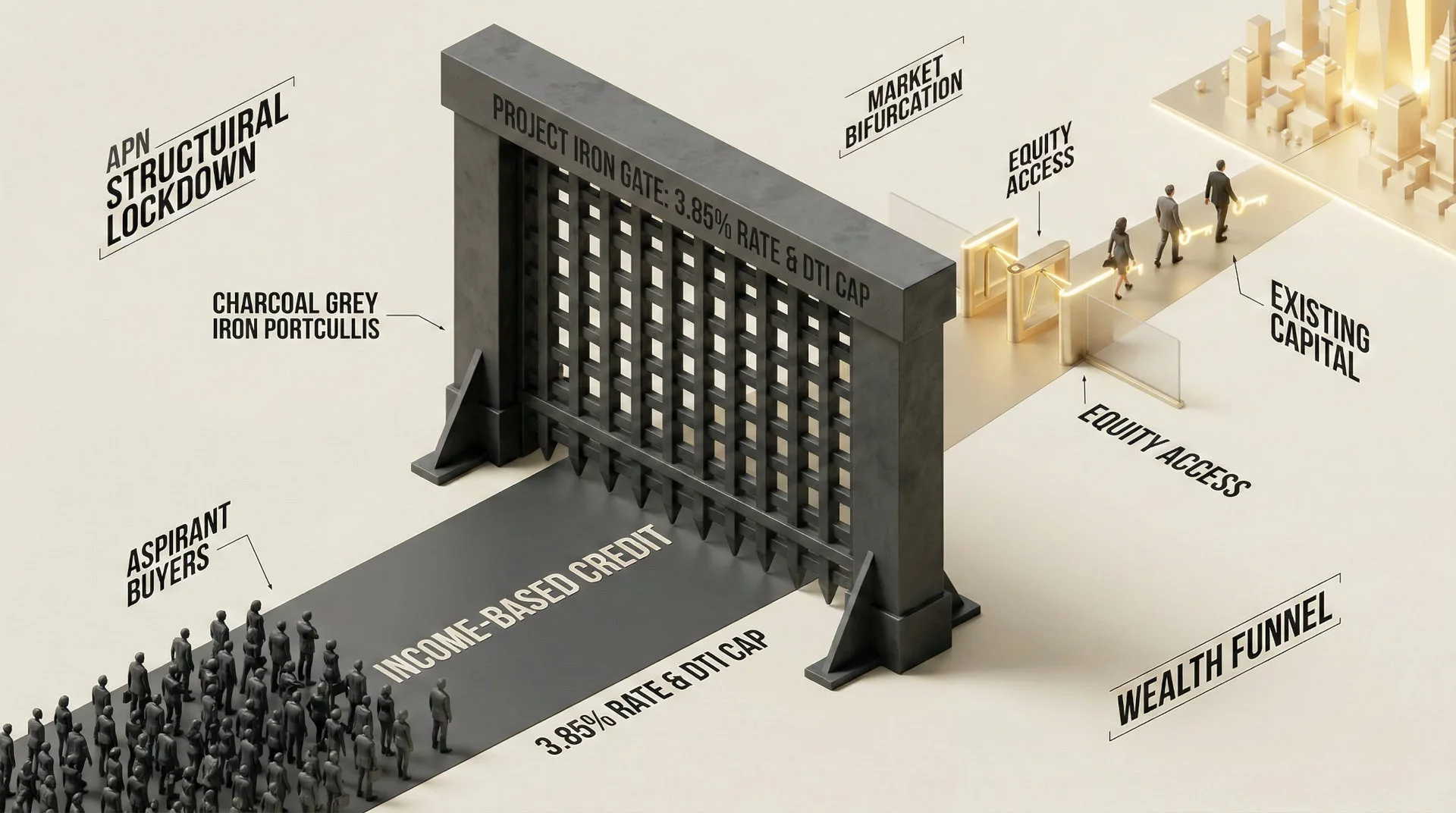

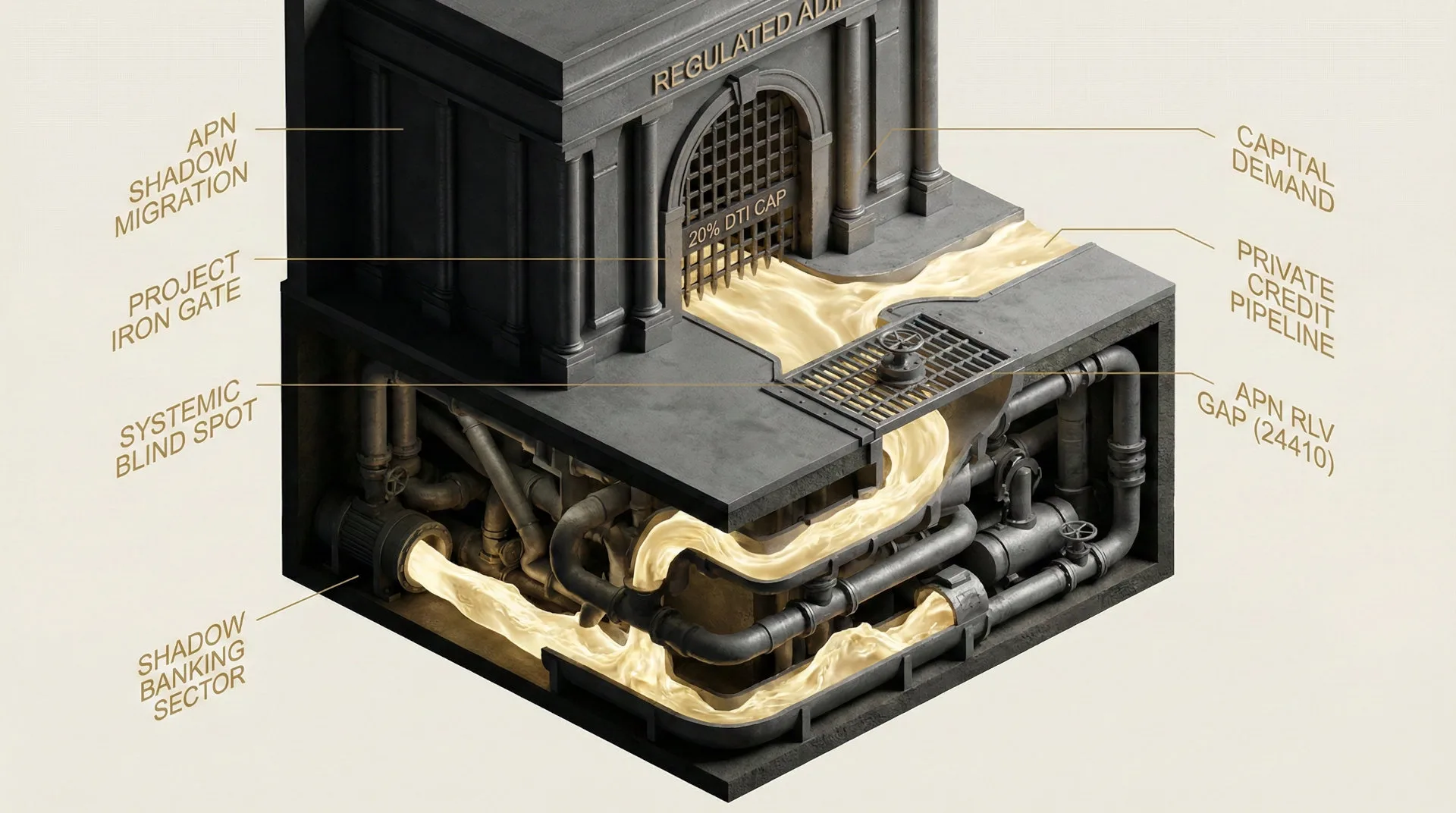

An Operative Credit Exclusion Mechanism (APN Credit Rationing Index™ (24230)): The sustained application of the Australian Prudential Regulation Authority’s (APRA) 3.00 percentage point serviceability buffer is functioning as a primary credit rationing mechanism. By mathematically suppressing maximum borrowing capacity, this policy directly reduces the addressable client pool for buyer’s agents, empirically validating how sovereign policy choices constrain market depth irrespective of underlying consumer demand.

A Signal of Decoupling Sentiment (APN Professional Sentiment Index™ (24300)): The measurable fee compression being initiated by new market entrants is a key negative indicator captured by the index. This trend signifies a structural decoupling between the asset optimism of incumbent professionals, who maintain premium fee structures, and the operational reality confronting newer participants in a volume-constrained environment.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of sovereign regulatory data, peak industry body reporting, and financial market metrics from the 2018–2026 period. The key facts are:

- Disproportionate Headcount Expansion: The number of active buyers agents in Australia more than doubled from approximately 500 in 2016 to over 1,000 by 2026, with growth concentrated in a regulatory environment lacking a specific licensing category for buyer-exclusive agents.

- The Measured Accreditation Gap: With the leading peak body, REBAA, holding approximately 140 accredited members, the empirical data confirms that over 85 per cent of practitioners operate without formal accreditation or peer-group oversight.

- Contracting Transactional Liquidity: The buyer pool has materially contracted. The mortgage conversion rate fell 11.2 percentage points (from a peak of 87.3% to 76.1%) between 2022 and late 2024, while the average number of registered bidders at auction has declined by nearly 40% from the 2021 cycle peak.

- Sustained Macroprudential Constraints: APRA has maintained its 3.00 percentage point loan serviceability buffer through 2026. Independent modelling indicates this policy mathematically excludes approximately 270,000 potential buyers from securing a median home loan.

- Material Signal of Sector Insolvency: The May 2026 liquidation of high-volume advisory firm Dashdot, which ceased operations with a stated $16.57 million creditor deficiency including over $10.5 million owed to retail clients for prepaid services, serves as a leading indicator of systemic stress within the sector.

Critical Analysis & Balanced View

The data reveals a critical bifurcation in the buyer’s agent sector, driven by two distinct and competing business models. The first insight is that the failure of high-volume firms like Dashdot is not an anomaly but a structural consequence of a business model predicated on perpetual market expansion and high transaction velocity. These models, often dependent on aggressive digital marketing and large upfront fees to cover high operational overheads, are fundamentally incompatible with a high-interest-rate, constrained-credit environment. Their failure is a market correction, weeding out operators who structured their businesses on the assumption that the accommodative credit conditions of 2020–2022 were permanent.

The second-order insight relates to the value proposition of off-market access. The analysis confirms that top-tier agents justify premium fees by securing off-market properties. However, the critical mechanism is not access to ‘secret’ listings but a strategic arbitrage of vendor friction. Professional agents capitalise on a vendor’s desire to avoid upfront advertising costs (e.g., ~$9,000 in Sydney) and campaign uncertainty, securing assets for their clients at a statistically significant discount (averaging 4.3%, or ~$60,000 in Sydney) that far outweighs the avoided marketing expense. This demonstrates that the value of an elite agent lies in exploiting market inefficiencies, a skill set the commoditised, price-focused tier of the market cannot replicate. This bifurcation between institutional-grade strategists and commoditised search agents will define the sector’s consolidation phase.

Strategic Implications for Property Professionals

- For Buyers Agents: Survival and growth will depend on differentiating service offerings beyond commoditised search functions. Focus must shift to complex due diligence, navigating regulatory frameworks, and demonstrating quantifiable value through strategic execution, particularly in the off-market space. Business models reliant on high volume and low margins face significant viability risk.

- For Real Estate Agencies: The documented 4.3% average financial penalty for vendors selling off-market is a powerful data point to justify investment in public marketing campaigns. Use this evidence to counter vendor reluctance, framing advertising expenditure as a necessary investment to maximise price discovery and avoid a much larger potential loss on the final sale price.

- For Mortgage Brokers & Lenders: The material decline in loan conversion rates necessitates more rigorous upfront qualification protocols. Filtering applicants against the 3.00pp serviceability buffer stress test at the earliest possible stage is critical to reduce wasted operational resources and improve the efficiency of the lending pipeline.

- For Property Investors & Home Buyers: The ‘accreditation gap’ represents a material consumer risk. Due diligence on a buyer’s agent’s credentials is now as critical as due diligence on a property. Verify REBAA accreditation, professional indemnity insurance, and a track record of performance through multiple market cycles. Be wary of models demanding exceptionally large upfront fees or promoting unrealistic ‘market-beating’ performance guarantees.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Credit Rationing Index™ (24230) by demonstrating how a persistent macroprudential policy (the 3.00pp serviceability buffer) directly reduces the addressable client pool for a professional services sector, causing structural oversupply.

- Validation: This analysis validates the APN Professional Sentiment Index™ (24300) by identifying fee compression among new market entrants as a negative sentiment signal, contrasting with the pricing power retained by established professionals.

- Index Calibration: The APN Professional Sentiment Index™ (24300) is calibrated to weight the ‘accreditation gap’—the ratio of accredited to unaccredited practitioners in a given professional services sector—as a negative indicator for overall sector health and systemic consumer risk.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.