Australian Real Estate Sector Navigates Structural Overservice Amidst Constrained Transaction Volumes

APN ANALYSIS: A-260629-AUS140102

Executive Summary

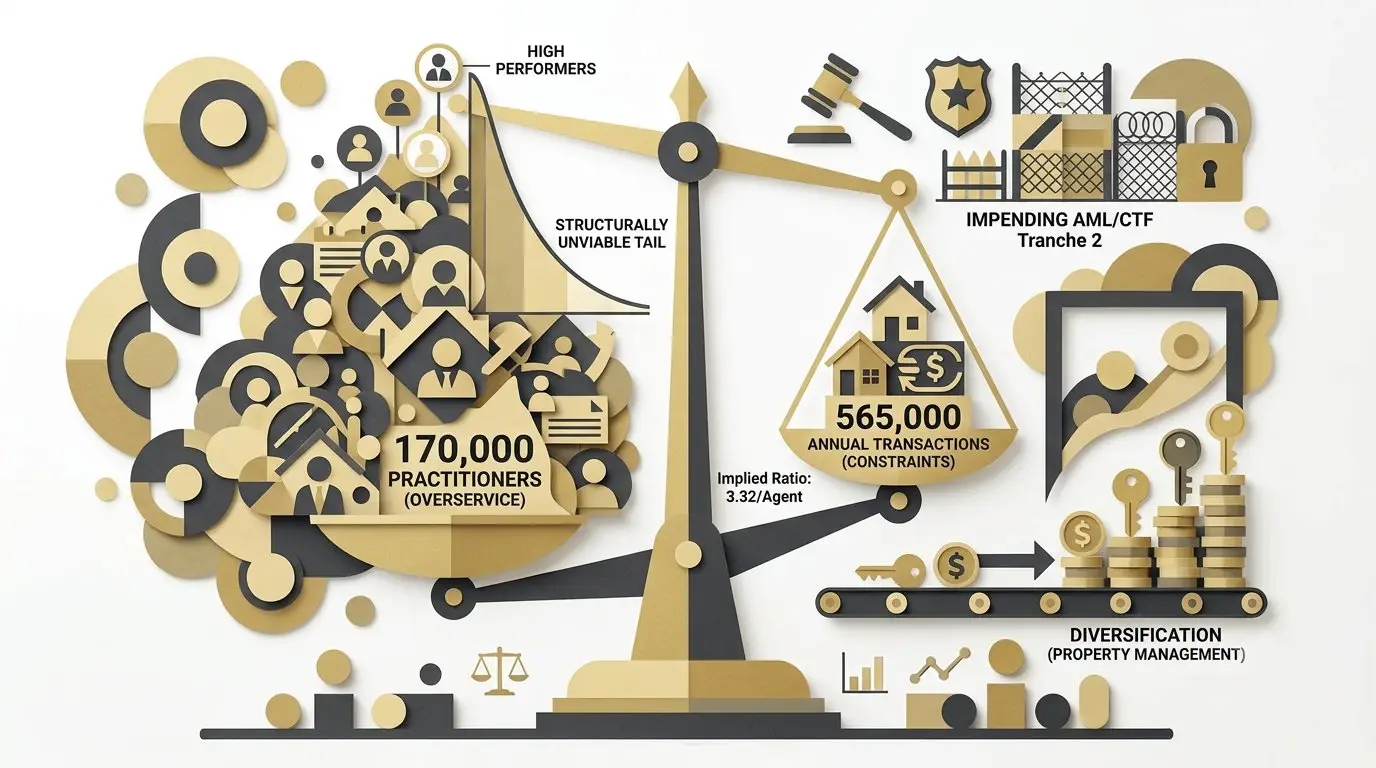

The Australian residential real estate sales sector is characterised by a material structural overservice, with an estimated 170,000 practitioners competing for a constrained pool of approximately 565,000 annual transactions. This misalignment, driven by workforce expansion during the 2020–21 cyclical peak and subsequent transaction volume contraction, is creating significant operational friction, including commission compression and margin pressure on agency businesses.

For property professionals, this environment necessitates a strategic shift towards operational efficiency, revenue diversification through services like property management, and rigorous compliance readiness for impending AML/CTF Tranche 2 legislation. The data indicates a period of industry consolidation where scale, capitalisation, and non-transactional revenue streams will be critical for sustained viability.

Background & Strategic Context

This analysis validates and calibrates APN’s core thesis on market friction and regulatory velocity. The divergence between human capital supply and transactional demand within the real estate services sector provides a clear empirical case study of how macroeconomic shifts, when filtered through regulatory frameworks, create systemic stress. The analysis specifically quantifies the mechanisms tracked by the APN Risk & Compliance Index™ (24200), demonstrating how financial pressure translates into compliance risk and forced consolidation.

A Lagging Indicator of Cyclical Exuberance (Market Psychology & Herd Behaviour (21620)): The expansion of the licensed agent workforce to an estimated 170,000 practitioners was a direct response to the asset accumulation momentum and hyper-liquidity of the 2020–2021 zero-bound interest rate environment, demonstrating how market sentiment drives human capital allocation.

The Credit Exclusion Mechanism (APN Credit Rationing Index™ (24230)): The sustained monetary tightening cycle, amplified by APRA’s 3.00 per cent serviceability buffer, structurally constrained borrowing capacity, leading to a material contraction in transaction volumes from a peak of approximately 650,000 in 2021 to 565,073 in 2025.

The Turnover Trap (APN Replacement Cost Gap™ (24450)): While asset valuations remain elevated, insulating incumbent owners from forced sales, high replacement costs and debt-to-income constraints suppress physical transaction velocity. This traps liquidity and limits the total addressable market for agents.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of statutory licensing registers across five major Australian states and national property transaction data from official and institutional sources. The key facts are:

- Practitioner Headcount Expansion: The national real estate sales workforce is estimated at approximately 170,000 active practitioners, a figure expanded during the 2020–2021 market peak. Major jurisdictions including New South Wales (>64,000), Queensland (51,447), and Victoria (33,945) show significant human capital accumulation against pre-pandemic baselines.

- Transaction Volume Contraction: National residential transactions contracted from a cyclical peak of approximately 650,175 in 2021 to 531,573 in 2024, before a marginal recovery to 565,073 in 2025. This represents a sustained reduction in the total pool of commission-generating events.

- Implied Agent-to-Transaction Ratio: The current market structure yields an implied national average of 3.32 transactions per agent per annum (565,073 transactions / 170,000 agents), a mathematically unsustainable level for a significant portion of the licensed cohort.

- Escalating Regulatory Velocity: State authorities, notably NSW Fair Trading, have intensified enforcement, issuing $1.58 million in fines and cancelling or suspending 84 licences in the 2024–2025 period, targeting trust account and compliance failures exacerbated by financial pressure.

- Impending Legislative Burden: The Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) Tranche 2 reforms, commencing 1 July 2026, will reclassify real estate agents as “gatekeepers,” imposing significant new compliance, reporting, and administrative overheads on approximately 70,000 businesses.

Critical Analysis & Balanced View

The low average agent-to-transaction ratio of 3.32 does not imply an even distribution of work. The data confirms a pareto-distribution is in effect, where a small percentage of high-performing agents and large networks captures a disproportionate share of transaction volume. This creates a vast, structurally unviable “tail” of licensed practitioners who are functionally inactive or operating at a net loss. This dynamic explains the intense competition and commission compression, as the marginal agent is forced to compete aggressively on price to secure any market share.

A key paradox defines the current market: high nominal property values coexist with deteriorating agency profit margins. Externally, vendors leverage the hyper-competitive environment to negotiate lower commission rates. Internally, agencies must offer high commission splits (often 50–60 per cent) to retain top-performing agents, who possess the primary leverage in a low-volume market. This dynamic means that even with high-value sales, the net profit to the agency entity is materially constrained, driving the strategic imperative for consolidation and the acquisition of recurring-revenue rent rolls.

The escalating regulatory velocity from state bodies and the impending AML/CTF legislation are not merely compliance hurdles; they function as catalysts for industry consolidation. The capital and operational cost of maintaining robust compliance infrastructure creates a structural barrier for smaller, low-volume agencies. This regulatory friction will accelerate the exit of marginal operators and the absorption of their market share by larger, better-capitalised entities.

Strategic Implications for Property Professionals

- For Independent & Boutique Agencies: The primary strategic focus must be on defending profit margins and diversifying revenue. This involves resisting commission compression through superior value propositions and actively seeking to build or acquire property management portfolios to create a stable, non-transactional revenue base.

- For Large Networks & Franchise Groups: The current market conditions create a strategic opportunity for consolidation. Acquiring the rent rolls of distressed or exiting competitors is a capital-efficient method to achieve scale, increase market share, and hedge against sales volume volatility.

- For Individual Sales Agents: Demonstrating consistent high performance is critical to command favourable commission splits. For mid-tier agents, the environment necessitates a focus on building a defensible niche or geographic specialisation to avoid being commoditised in a hyper-competitive market.

- For All Practitioners: Proactive preparation for the AML/CTF Tranche 2 reforms is non-negotiable. This requires immediate investment in understanding the obligations, establishing compliance programs, and budgeting for the associated administrative and potential technology costs. Failure to prepare represents a significant business continuity risk post-July 2026.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Risk & Compliance Index™ (24200) by empirically demonstrating how macroeconomic pressure (constrained transaction volumes) directly translates into elevated regulatory risk, evidenced by the surge in enforcement actions by NSW Fair Trading against financially stressed agencies.

- Index Calibration: The APN Regulatory Velocity Multiplier™ (24210) is calibrated to reflect the increased intensity and financial impact of state-level enforcement actions, weighting trust account compliance failures more heavily as a leading indicator of agency distress.

- Data Capture: This triggers a new data capture mandate for the APN Risk & Compliance Index™ (24200) to systematically track agency insolvencies and the rate of rent roll acquisitions as primary metrics for industry consolidation velocity ahead of the AML/CTF Tranche 2 implementation.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.