Codex Structural Adjustment Confirmed: APRA’s DTI Cap Displaces Systemic Risk to the Non-Bank Lending Sector

APN ANALYSIS: A-260219-AUS137522

Executive Summary

The Australian Prudential Regulation Authority’s (APRA) activation of a 20 per cent portfolio cap on high Debt-to-Income (DTI) lending for regulated banks has not resulted in a material reduction of systemic leverage. Instead, the policy has acted as a catalyst for a high-velocity migration of loan demand to the non-bank sector, displacing billions in high-DTI investor loan demand from the regulated banking sector to unregulated Non-Authorised Deposit-taking Institution (Non-ADI) lenders. This matters because while the balance sheets of major banks appear safer, the policy has inadvertently created a material systemic blind spot. The risk has not been eliminated; it has been rerouted into an opaque, rapidly expanding segment of the financial system that operates entirely outside of APRA’s purview.

For property professionals, this structural bifurcation of the credit market is a primary operational consideration. Access to capital is now split: prime, low-leverage borrowers will continue to be serviced by traditional banks, while creditworthy investors and complex borrowers requiring leverage above 6x DTI must now navigate the specialist Non-ADI sector. Mastering this new landscape, including the product suites and pricing premiums of lenders like Pepper Money, La Trobe Financial, and Liberty Financial, is no longer optional. It is essential for accurate client qualification, sophisticated deal structuring, and mitigating settlement risk in a fundamentally altered credit environment.

Background & Strategic Context

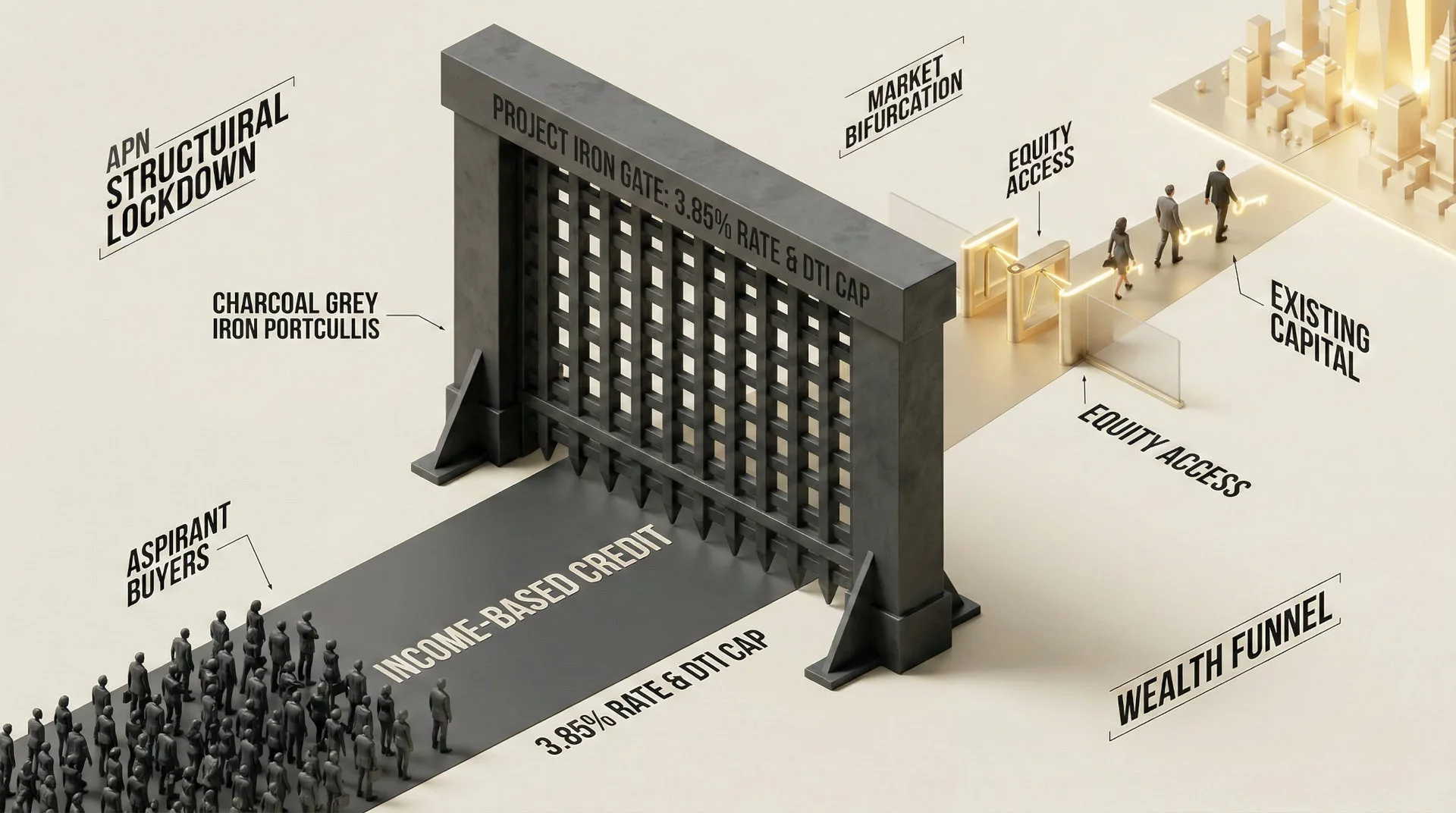

This event validates and calibrates APN’s core macro-theses, demonstrating how direct state intervention structurally reshapes market architecture and funnels activity through specific channels. The enforcement of the DTI cap is a textbook example of a regulatory ‘Iron Gate’ that, while intended to promote stability within the regulated sector, has inadvertently created a new, opaque risk channel by displacing, rather than reducing, demand for leverage.

State Intervention and the SPCI Framework (APN SPCI, 24800): APRA’s activation of the DTI cap is a direct state-level intervention that has fundamentally restructured the architecture of the Australian credit market, providing validation for the APN Sovereign Policy Composite Index™ (SPCI, 24800) framework, which posits that regulatory action is a primary driver of structural market change.

The Erection of a Regulatory Barrier (Project Iron Gate): The 20 per cent portfolio cap acts as a rigid ‘Iron Gate’, structurally decoupling creditworthy, high-income borrowers from traditional ADI capital solely based on a mathematical DTI ratio. This enforces a cashflow-based rationing system and creates a cohort of borrowers who are now algorithmically excluded from the regulated sector.

Quantifying the Market Dislocation (APN Credit Rationing Index™): The immediate rejection of investor loan applications, which already constituted over 10 per cent of new flows and were on an accelerating trajectory, provides a baseline reading for the APN Credit Rationing Index™ (24230). It measures the scale of borrowers being mathematically excluded by the new regulatory friction, providing the raw input for the observed migration to the non-bank sector.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of APRA’s macroprudential directives, quarterly ADI property exposure statistics, and real-time broker flow data. The key facts are:

- The Regulatory Mandate: Effective 1 February 2026, APRA mandated that Authorised Deposit-taking Institutions (ADIs) must limit new loans with a Debt-to-Income (DTI) ratio of six or more to just 20 per cent of their quarterly originations, applied separately to owner-occupier and investor portfolios.

- The Pre-Existing Pressure Point: Prior to the mandate, high-DTI loans to investors were already at 10.1 per cent of new lending and accelerating, forcing major banks to immediately ration credit to avoid breaching the 20 per cent cap and maintain a prudential buffer.

- The Re-Leveraging Phase: The market was in a ‘re-leveraging’ phase prior to the intervention, with aggregate high-DTI loans rising from a low of 5.0 per cent in June 2024 to 7.3 per cent by September 2025. This indicates APRA’s intervention was an abrupt policy shift in a market actively seeking more leverage, not a continuation of an organic de-risking trend.

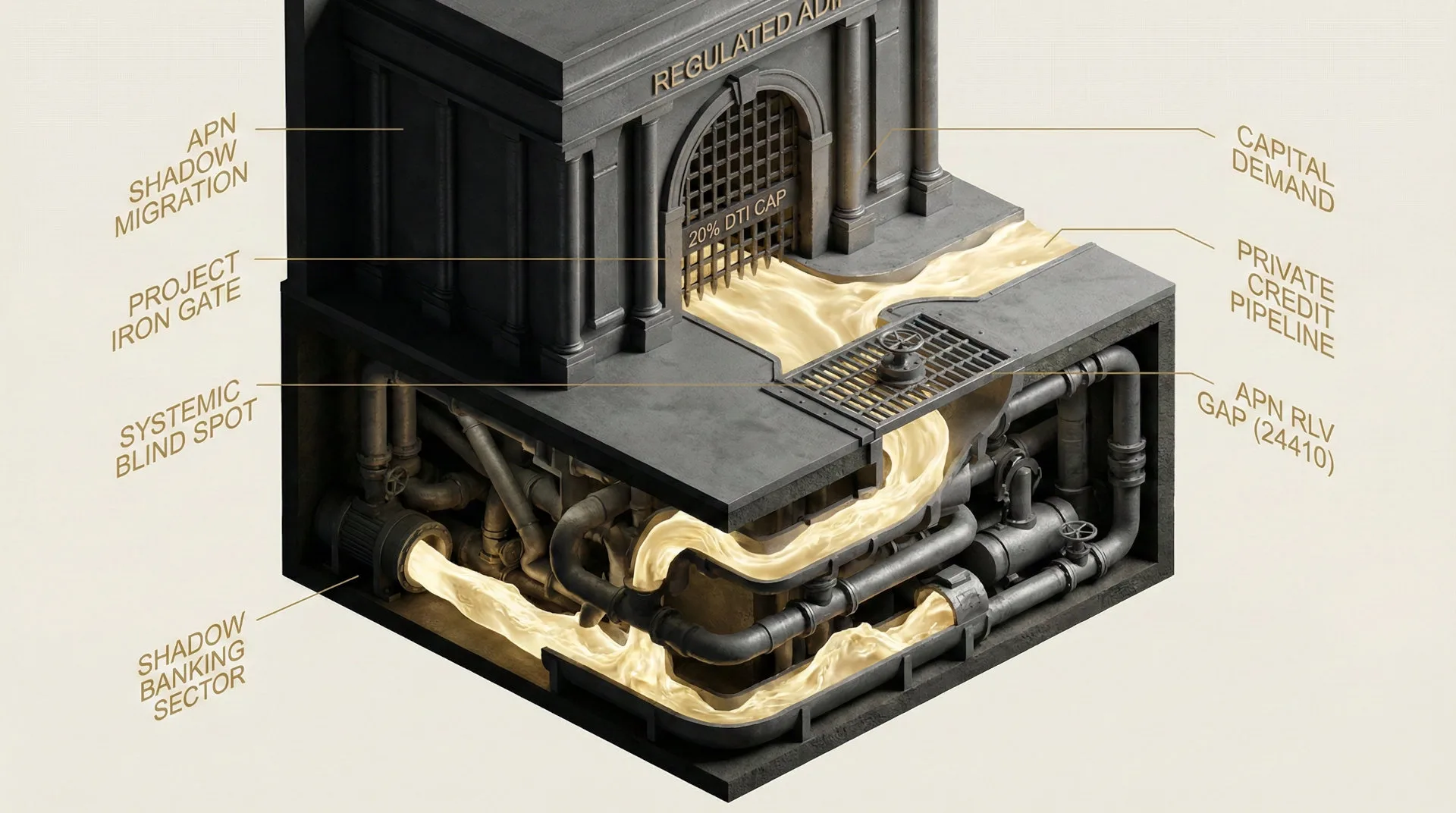

- The Non-ADI Exemption: Non-ADI lenders are not bound by APRA’s macroprudential rules and are therefore completely exempt from the 20 per cent DTI cap, creating a clear and profitable channel for regulatory arbitrage.

Critical Analysis & Balanced View

The core paradox of APRA’s policy is that in its attempt to de-risk the regulated banking system, it has increased the opacity and potential fragility of the financial system as a whole. The ‘Displaced Leverage’ hypothesis is confirmed: the risk has not been eliminated, merely moved outside of the regulatory perimeter. The primary counter-argument, that the higher cost of capital for Non-ADIs would create a natural barrier, has been empirically disproven. Elevated institutional demand for Australian Residential Mortgage-Backed Securities (RMBS) has suppressed wholesale funding costs, allowing Non-ADIs to price their products at a premium of only 13-105 basis points over ADI rates.

This narrow premium is well below the 150bps threshold APN identifies as the point of demand destruction. For property investors, particularly with negative gearing benefits, this premium is a manageable cost of doing business to secure an asset in a market where capital growth continues to outpace wage growth. Consequently, a perception of systemic safety has been created that may not reflect the total system risk. While ADI balance sheets are fortified in isolation, the broader system has imported a new dependency on wholesale funding markets and the global appetite for Australian credit risk, a dynamic that remains entirely outside the regulator’s direct control.

Strategic Implications for Property Professionals

- For Mortgage Brokers & Finance Strategists: Your role is now bifurcated. You must maintain two distinct pipelines: a ‘vanilla’ ADI channel for low-DTI clients and a specialist Non-ADI channel for high-leverage investors and complex borrowers. Failure to master the Non-ADI product suite and underwriting criteria is a direct threat to revenue and client retention.

- For Buyers’ Agents & Agents: Pre-qualification of clients is now an essential operational requirement. You must probe a client’s DTI ratio and funding strategy early in the engagement. An offer subject to finance from a high-leverage investor relying on a major bank is now a high-risk proposition; understanding their path to a Non-ADI lender is key to assessing deal certainty.

- For Developers & Project Marketers: The settlement risk on off-the-plan sales has materially increased, as your target market of investors is being directly impacted. It is essential to establish partnerships with finance specialists who have established Non-ADI channels to provide funding solutions for your purchasers, thereby de-risking your project’s settlement phase.

- For Property Investors: The cost of high leverage has structurally changed. While capital remains accessible via the Non-ADI sector, it comes at a premium of up to ~105 basis points. This premium must be factored into your feasibility analysis, but it should be viewed as a manageable cost of business required to secure an asset in a supply-constrained market.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the Project Iron Gate framework, empirically demonstrating how a regulatory cap creates a structural barrier to credit for a specific borrower cohort, forcing a migration to alternative capital sources.

- Index Calibration (APN RVM™): The APN Regulatory Velocity Multiplier™ (24210) is calibrated to track the volume and speed of displaced loan applications migrating from the ADI to the Non-ADI sector. The initial 10.1 per cent of investor loans being immediately affected establishes the baseline velocity for the index.

- Index Calibration (APN Credit Rationing Index™): The APN Credit Rationing Index™ (24230) reading is adjusted upwards. The index now measures not just the theoretical serviceability gap, but the actual, observed number of creditworthy borrowers being rejected by ADIs due to the hard DTI portfolio limit.

- Data Capture Mandate: This analysis triggers a new data capture mandate under the APN Symbiotic Intelligence Network™ (24310) to survey mortgage brokers on the percentage of high-DTI loan applications being rerouted to Non-ADI lenders and the average approval times, providing a real-time feed for the APN RVM™.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.