APRA’s DTI Exemption Validates ‘Two-Tier Distortion,’ Directing Capital into New Builds While Materially Restricting Established Market

APN ANALYSIS: A-251201-AUS131425

Executive Summary

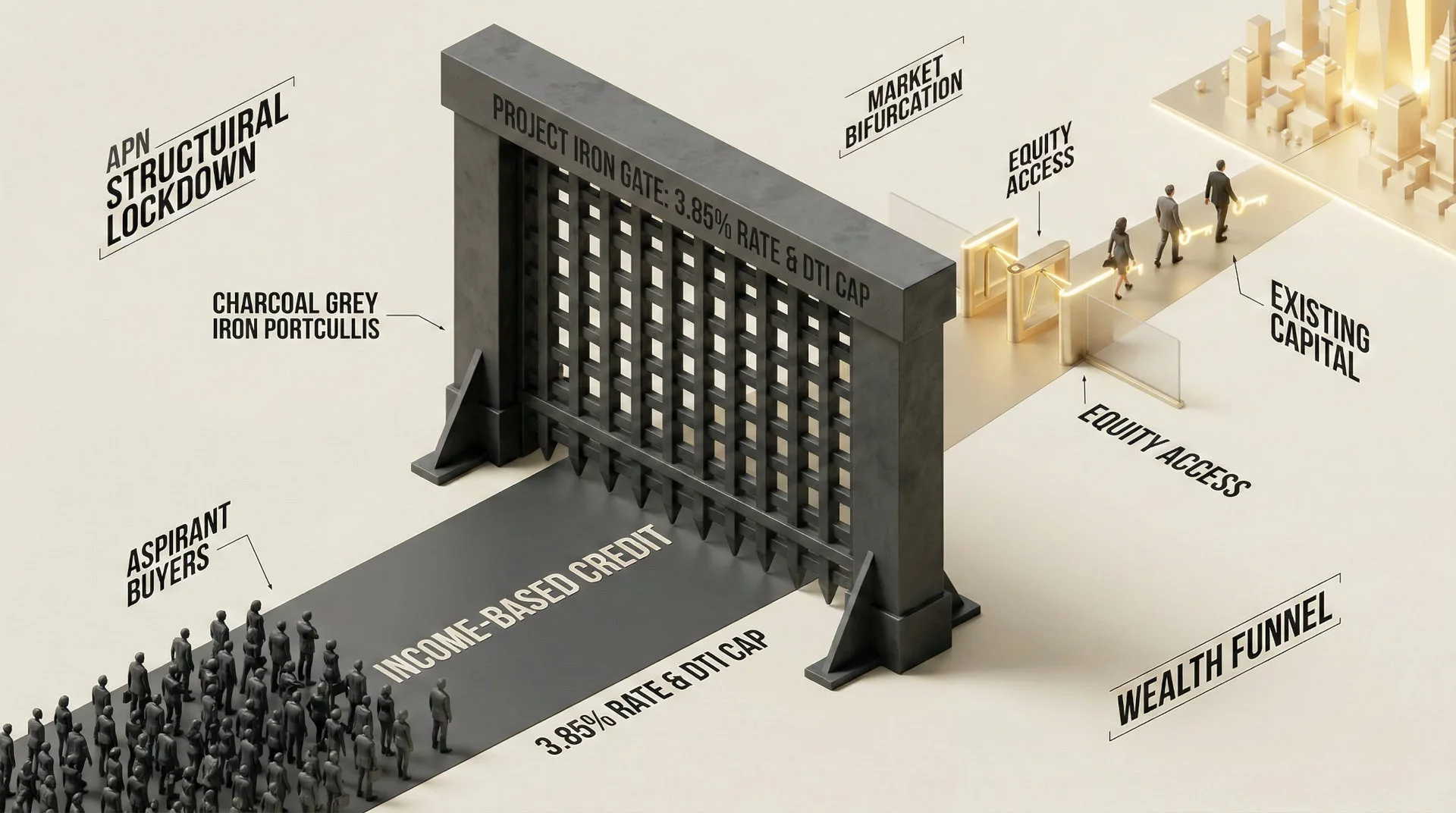

The confirmation of an explicit regulatory exemption for “new dwellings” within APRA’s incoming Debt-to-Income (DTI) cap validates the “Two-Tier Distortion” thesis. Our analysis confirms that this policy engineers a structural capital funnel, providing unlimited leverage for new construction while imposing a material liquidity restriction on the established property market. Effective February 1, 2026, high-DTI loans greater than or equal to 6x for established stock are capped at 20% of flow, while new builds are exempt.

For property professionals, this creates a bifurcated market. The established market faces an immediate “liquidity trap,” forcing investors who cannot refinance to sell, while capital is forcibly migrated toward developers. With major banks already near the cap (19% flow), a “Shadow Cap” is now operational, triggering credit rationing well before the deadline and granting monopoly-like pricing power to unleveraged landlords in a rental market with constrained supply.

Background & Strategic Context

This analysis identifies a definitive regulatory intervention that splits the residential property market into two distinct asset classes based on financing liquidity, validating core APN theses on market distortion and capital flow.

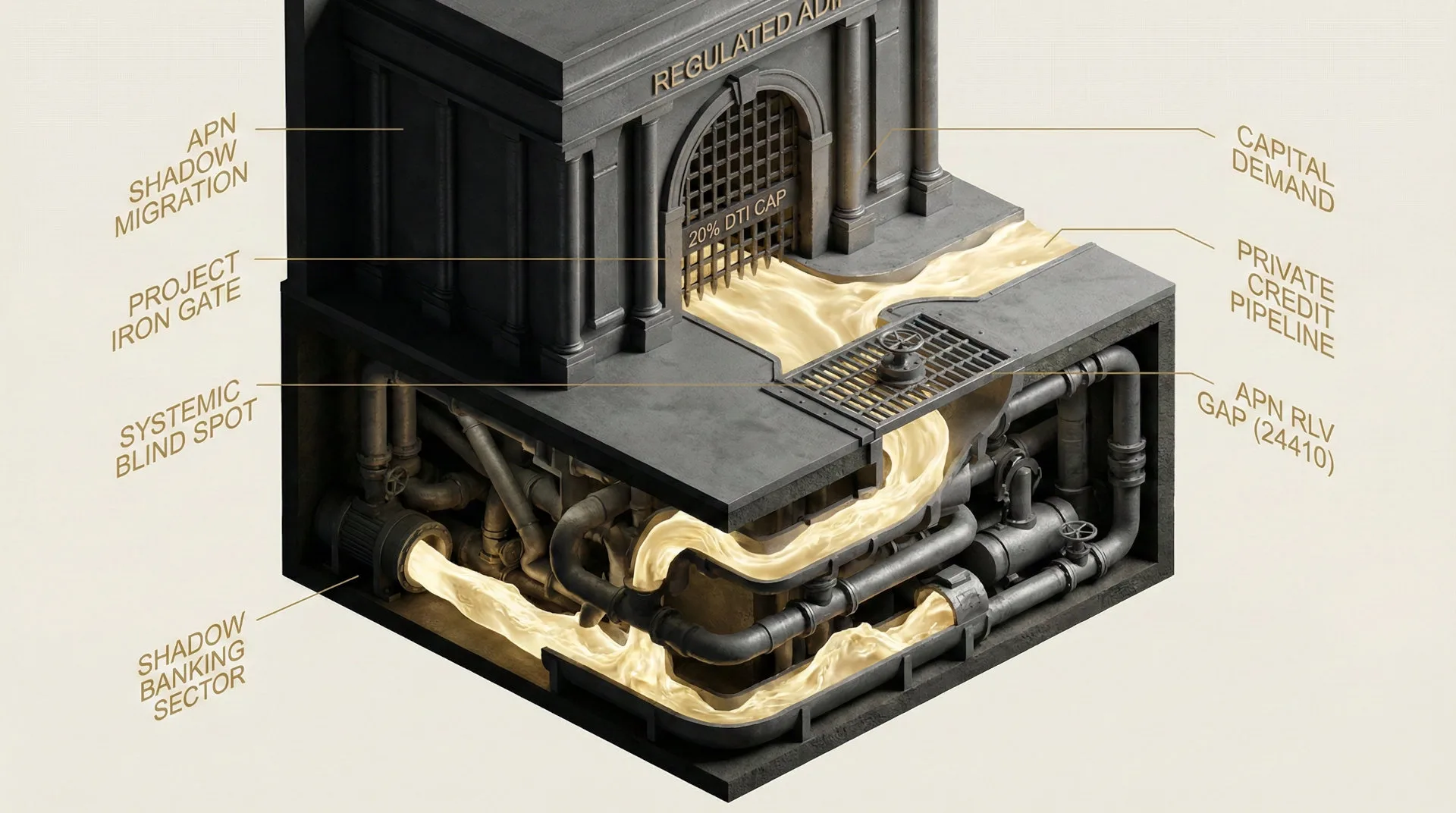

- Two-Tier Capital Structure (APN Risk & Compliance Index™): The policy explicitly differentiates collateral based on age, not risk. This creates a “Two-Tier Distortion” where “new dwellings” enjoy a permanent financing advantage (unlimited high-DTI capacity) while “established dwellings” are subject to a hard liquidity cap. This validates the APN Risk & Compliance Index™ (24200) thesis that regulatory intervention is now the primary driver of asset liquidity.

- The Developer Funnel (APN Future Development Pipeline Index™): The exemption is a state-sponsored sales channel. By exempting new construction, the regulator has effectively deputised mortgage brokers to direct high-leverage clients away from the secondary market and directly into the APN Future Development Pipeline Index™ (24400). This deployment of credit policy provides a non-market demand floor for developers.

- The Rental Shock (APN Sentinel™): The policy acts as a catalyst for a “Rental Shock,” relevant to APN Sentinel™ (24120). By capacity-constraining investor acquisition of established rentals now (via the cap) while incentivising new supply that won’t exist for 12-24 months, it creates an immediate “supply gap.” This structural exit of investors from the established market will drive rents higher, exacerbating social friction.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing. The key facts are:

- The Regulation: Effective February 1, 2026, ADIs must limit new mortgages with a DTI ratio greater than or equal to 6x to 20% of total quarterly flows.

- The Exemption: The limit explicitly does not apply to “loans for the purchase or construction of new dwellings.”

- The Constraint: Major Banks are currently at ~19% high-DTI flow, leaving a negligible 1% buffer. Challenger banks (e.g., Bendigo) are at ~23% and must contract by >300bps.

- The Segregation: Limits apply to owner-occupier and investor portfolios separately, preventing cross-subsidisation.

- The Context: National vacancy rates are at historic lows (~1.1%), and rents consume a record one-third of household income.

Critical Analysis & Balanced View

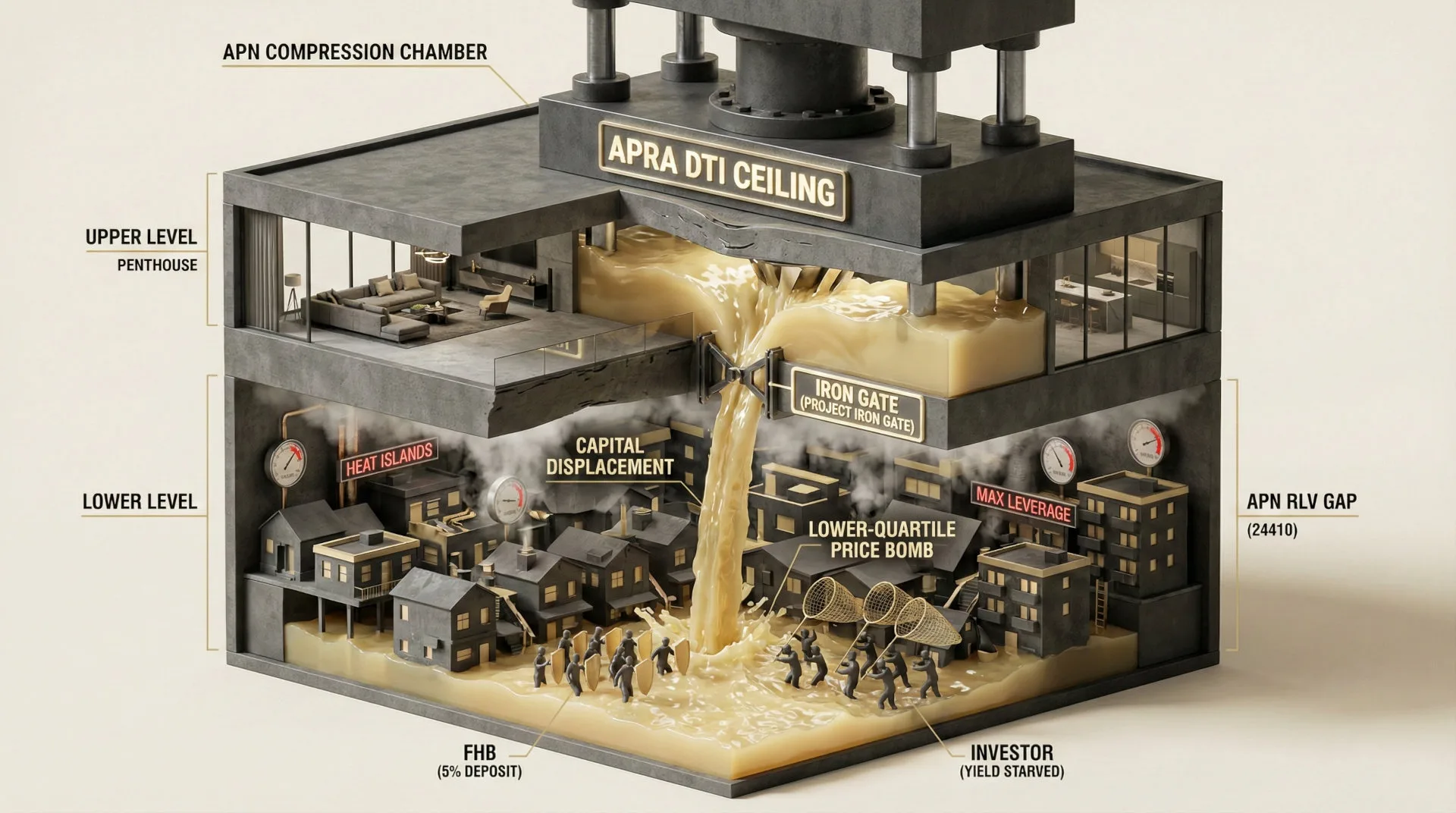

The central observation pertains to evidence of regulatory arbitrage. The policy is not a prudent credit measure; it is an industrial subsidy. By exempting new builds, the regulator is acknowledging that the objective is not solely financial stability (as a high-DTI loan is risky regardless of the asset’s age) but rather to stimulate construction activity at the expense of the secondary market.

The most critical operational insight is the “Quantifiable Squeeze.” With major banks already at 19% exposure against a 20% cap, the effective “Shadow Cap” is operational today. Banks cannot risk breaching the limit, so they will begin rationing credit immediately to build a buffer. This means the window for high-leverage financing in the established market has effectively already closed for many borrowers.

This creates a “Liquidity Trap” for incumbents. Existing investors with high-DTI loans in the established market are now constrained. They cannot refinance to another lender because they would be classified as a “new” high-DTI origination under the cap. This lack of mobility strips them of negotiating power and, if rates rise or circumstances change, forces them to sell, feeding the “investor exit” dynamic. Meanwhile, the “rental shock” is projected: investors are being forced out of the only stock available for rent today (established homes), while the replacement stock (new builds) is years away.

Strategic Implications for Property Professionals

- For Mortgage Brokers: You must pivot high-leverage clients immediately. The “new build” exemption is the only viable path for DTI greater than or equal to 6x approval. This requires new partnerships with developers to secure stock that fits this financing window.

- For Developers: This policy provides a demand assurance. Market your stock explicitly as “High-DTI Exempt.” This is a powerful unique selling proposition (USP) for investors and first-home buyers stretching their capacity.

- For Investors (Established): You are entering a rental market scenario characterised by elevated competition. If you can hold (are unleveraged), you will gain monopoly-like pricing power as your leveraged competitors are forced to sell. Expect yields to materially escalate as rental supply contracts further.

- For Agents: Prepare for an elevated activity during the accelerated acquisition phase in Dec 2025/Jan 2026 as buyers rush to meet the Feb 1 deadline, followed by a sharp liquidity withdrawal and a difficult sales environment for investment-grade established stock.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides high-confidence validation of the “Two-Tier Distortion” thesis. It confirms that the regulator has engineered a structural separation of the market, where “new” and “established” assets operate under different liquidity regimes.

- Index Calibration (24200): The APN Risk & Compliance Index™ (24200) is calibrated to include “Asset Age” as a primary liquidity variable. Established assets now carry a “Regulatory Liquidity Discount” due to the DTI cap.

- Index Calibration (24400): The APN Future Development Pipeline Index™ (24400) is updated to weight the “DTI Exemption” as a positive demand driver, effectively placing a “regulatory floor” under developer presales.

- Data Capture (24310): The APN Symbiotic Intelligence Network™ (24310) is tasked to monitor the spread between “New Build” and “Established” mortgage interest rates and approval times, as banks may begin to price the scarcity of high-DTI capacity in the established sector.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.