The Structural Yield Rotation: Macquarie Swaps Agricultural Risk for State-Guaranteed Energy Annuities

APN ANALYSIS: A-251127-AUS131247

Executive Summary

Macquarie Asset Management (MAM) is executing a structurally significant A$3 billion capital rotation, divesting its mature Paraway Pastoral agricultural portfolio to fund its new renewable energy platform, Aula Energy. This is not a simple sector pivot; it is a structural arbitrage between risk profiles. MAM is exiting the volatile, weather-dependent, and low-yielding business of operational farming for the stable, state-underwritten, and higher-yielding returns of renewable infrastructure. The move confirms that institutional capital now views assets backed by government revenue floors, like those in the Capacity Investment Scheme (CIS), as financially superior to unsubsidised commodity-producing assets, fundamentally reshaping the valuation of Australian land.

For property professionals, this event establishes a new valuation paradigm for rural and regional land. The ‘highest and best use’ of a broadacre property is no longer solely defined by its agricultural productivity. Its value is now materially linked to its potential to host state-backed energy infrastructure. This ‘Electron Rotation’ creates a clear bifurcation in the market: land with access to the grid commands a significant ‘Infrastructure Uplift’ premium, while land without it is increasingly exposed to the combined risks of climate volatility and capital reallocation. This redefines risk and opportunity for valuers, developers, and investors in the non-urban property sector.

Background & Strategic Context

This event validates and calibrates APN’s core thesis that state-level intervention is the primary factor shaping property market boundaries and asset class viability. Macquarie’s multi-billion-dollar decision was not driven by a change in commodity forecasts, but by a change in federal government policy that created a mathematically superior investment vehicle. The ‘Electron Rotation’ is a direct consequence of a deliberate state action to de-risk private capital in pursuit of national energy objectives.

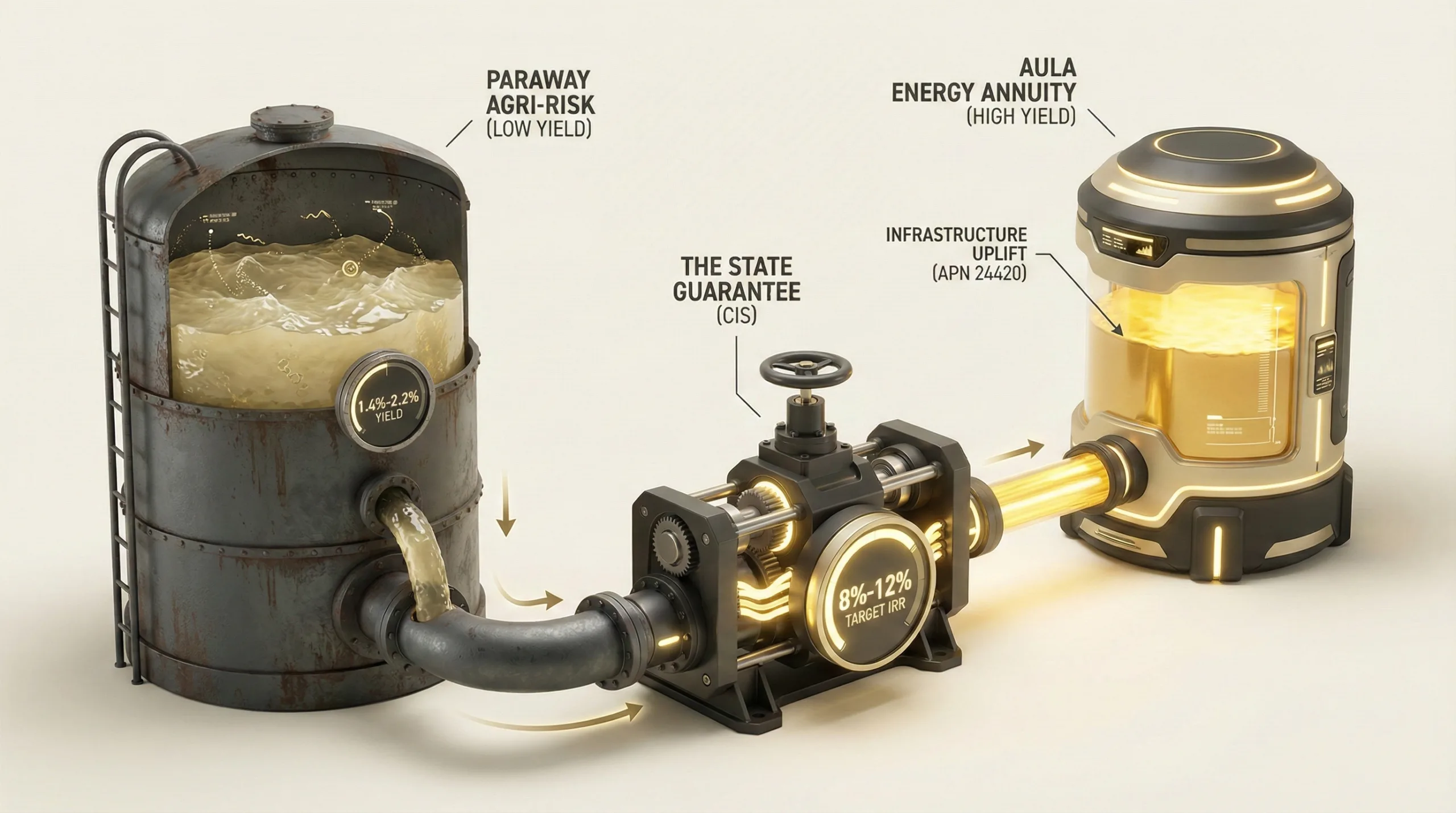

The State as Prime Mover: The APN Sovereign Policy Composite Index™ (SPCI, 24800): The Commonwealth’s Capacity Investment Scheme (CIS) is a primary example of state intervention creating an entirely new investment logic. By providing a revenue floor for renewable energy projects, the government has structured a class of ‘quasi-government bonds’ that displaces traditional, unsubsidised assets like operational agriculture in the institutional risk-return matrix. This is not a market-led evolution; it is a state-directed reconstruction of the infrastructure asset class.

Quantifying the State’s Influence (APN Infrastructure Uplift Multiplier™): The financial core of this rotation is the ‘Infrastructure Uplift’. The CIS acts as the codex, or mechanism, that applies a multiplier to the value of land suitable for energy generation. A hectare of grazing land producing a ~2% yield is financially inferior to a hectare hosting a wind turbine with a state-guaranteed 8-12% IRR target. The A$3 billion capital rotation is the physical manifestation of this multiplier effect in action, as capital flows towards the state-underwritten asset.

Pricing Climate Volatility (APN Financial Climate Sensitivity™): Macquarie’s exit from Paraway is a sophisticated de-risking of its portfolio’s financial sensitivity to climate. Paraway’s earnings are a high-beta derivative on weather patterns and commodity cycles. Aula Energy’s earnings are underwritten by the Commonwealth Treasury. This rotation demonstrates institutional capital’s move to price ‘weather risk’ by divesting exposed assets and acquiring assets where climate transition policy (i.e., the CIS) provides a direct financial shield.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of Macquarie Asset Management’s strategic capital rotation from its agricultural fund to its energy transition platform. The key facts are:

- The Paraway Divestment: Macquarie has officially commenced the sale process for Paraway Pastoral Company, an agricultural portfolio spanning 4.4 million hectares. Verified market intelligence places the valuation between A$2.5 billion and A$3.0 billion, a significant upward revision from earlier estimates.

- The Aula Energy Capitalisation: Concurrent with the Paraway sale, Macquarie has launched and is actively funding Aula Energy, its onshore renewable energy platform. This includes funding the construction of assets like the Boulder Creek Wind Farm, a capital-intensive phase requiring substantial liquidity.

- The Liquidity Bridge: The A$2.5B+ capital release from the Paraway exit provides the ‘dry powder’ necessary to fund the heavy construction and development pipeline of Aula Energy, creating a direct and logical link between the two transactions.

- The State Guarantee (‘The Codex’): Aula Energy’s Carmody’s Hill Wind Farm was a successful bidder in the Commonwealth’s Capacity Investment Scheme (CIS) Tender 4. This successful bid is the structurally significant de-risking event, securing a government-backed revenue floor for the asset and transforming it from a speculative development into a stable, infrastructure-grade annuity.

Critical Analysis & Balanced View

The strategic driver of this rotation is the ‘Volatility Spread’—the arbitrage opportunity between the uncertain, weather-dependent returns of agriculture and the guaranteed returns of state-backed energy. Our analysis shows Paraway Pastoral’s operating yield has compressed to 1.4% to 2.2% on its current multi-billion-dollar valuation. In a high-interest-rate environment, this represents a negative risk premium for the operational and climatic risks involved. In contrast, renewable projects under the CIS target IRRs of 8% to 12%, with downside revenue risk explicitly removed by the taxpayer.

This is a sophisticated application of financial engineering. Macquarie is divesting a mature, 18-year-old agricultural fund at the peak of the land appreciation cycle to redeploy the capital into the nascent, de-risked growth phase of the energy transition. The timing is precise, monetising the ‘beta’ of land value growth before a forecast softening in the rural market, and reinvesting into an asset class where the government has just created an ‘alpha’ support mechanism.

However, it is analytically inaccurate to view this as an exit from ‘Natural Capital’. Rather, Macquarie is refining its exposure by decoupling ‘Land Ownership’ from ‘Operational Farming’. By selling the high-opex, labour-intensive farming entity (Paraway) while simultaneously building funds focused on carbon and biodiversity, MAM is shifting from a ‘production’ model (selling beef) to a ‘rent-seeking’ model (collecting carbon credits or energy lease payments). The ‘Electron’ has mathematically displaced the ‘Protein’ as the preferred unit of value because it comes with a sovereign guarantee.

Strategic Implications for Property Professionals

- For Rural & Agribusiness Valuers: The valuation of broadacre land can no longer be based solely on its productive capacity (stocking rates, crop yields). Proximity to transmission infrastructure and suitability for renewable generation are now primary value drivers. A new ‘highest and best use’ calculation is required, factoring in the potential for a ‘state-alpha’ revenue stream, which may eclipse the land’s agricultural value.

- For Developers & Land Bankers: The primary strategy for large-scale land acquisition in regional Australia is now geared towards energy infrastructure. Securing parcels within designated Renewable Energy Zones (REZs) or near major grid connection points is paramount. The strategic land acquisition model is no longer for future residential subdivision but for securing long-term lease agreements with energy platforms like Aula Energy.

- For Agents & Buyers’ Agents: The rural property market will bifurcate. Properties with no infrastructure potential will be valued on traditional metrics and face headwinds from capital rotating out of the sector. Conversely, properties with the potential for a passive wind or solar lease income will command a significant ‘energy annuity’ premium, attracting a new class of investor seeking de-risked, inflation-linked returns.

- For Institutional Investors & Fund Managers: Macquarie’s strategy is the new model for managing climate and commodity risk. The model of rotating from assets with high ‘weather beta’ (agriculture, tourism) to assets with ‘state alpha’ (underwritten renewables, social infrastructure) will be replicated. This will create acquisition opportunities for mature, unsubsidised asset portfolios and intensify competition for development sites that benefit from government de-risking schemes.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides a validation of the APN Sovereign Policy Composite Index™ (SPCI, 24800) thesis, where direct state intervention (the CIS) fundamentally alters asset class viability and triggers multi-billion-dollar capital flows. It serves as a primary case study for the APN Infrastructure Uplift Multiplier™ (24420), demonstrating how a government guarantee mechanism creates a quantifiable value premium for specific land assets.

- Index Calibration: The APN Financial Climate Sensitivity™ (24510) index is recalibrated to quantify the ‘Volatility Spread’ between unsubsidised, climate-exposed assets (Paraway) and state-underwritten climate solutions (Aula). The ‘Brown Discount’ for pure-play agricultural operations without infrastructure potential is now benchmarked against the ‘Green Premium’ for energy-hosting land, which is demonstrably attracting institutional capital.

- Data Capture: This event triggers a new data capture mandate under the APN Symbiotic Intelligence Network™ (24310). The network will now actively track and analyse all rural land transactions within a 50-kilometre radius of announced CIS projects and major transmission lines to monitor for, and quantify, the leading edge of the APN Infrastructure Uplift Multiplier™ as it is priced into the market.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.