The Volt-Split Structural Adjustment: How NSW Energy Policy is Creating a Two-Tier Rural Property Market

APN ANALYSIS: A-251127-AUS131231

Executive Summary

A material structural adjustment is bifurcating the rural property market within the New South Wales Central-West Orana Renewable Energy Zone (REZ). State-led energy infrastructure procurement has bifurcated land values, creating two distinct asset classes. The first, “Power Hosts,” are properties hosting transmission lines or generation assets. They benefit from state-guaranteed, inflation-indexed “Energy Annuities” that capitalise into significant valuation premiums. The second, “Amenity-Affected Properties,” are neighbouring properties that suffer uncompensated valuation drag and liquidity constraint due to their proximity to this critical infrastructure. This phenomenon, which APN terms the “Volt-Split Structural Adjustment,” is not a cyclical adjustment but a permanent, policy-driven re-rating of rural assets.

For property professionals, this analysis is of elevated importance. The traditional metrics of agricultural productivity are no longer sufficient for valuing land within the REZ footprint. The existence of an “Energy Annuity” introduces an infrastructure-grade, low-risk income stream that demands a lower capitalisation rate, justifying premiums of 15-30%. Conversely, the material reduction in amenity in high-value lifestyle markets like Mudgee is creating real-term discounts of up to 40% relative to the strongly appreciating baseline market. Understanding the legislative architecture that enforces this divide is now essential for accurate valuation, risk assessment, and client advisory in affected regions.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses on how state intervention fundamentally reshapes property markets. The creation of the REZ and its associated compensation framework is a direct act of market structuring, with predictable and highly divergent outcomes for asset owners.

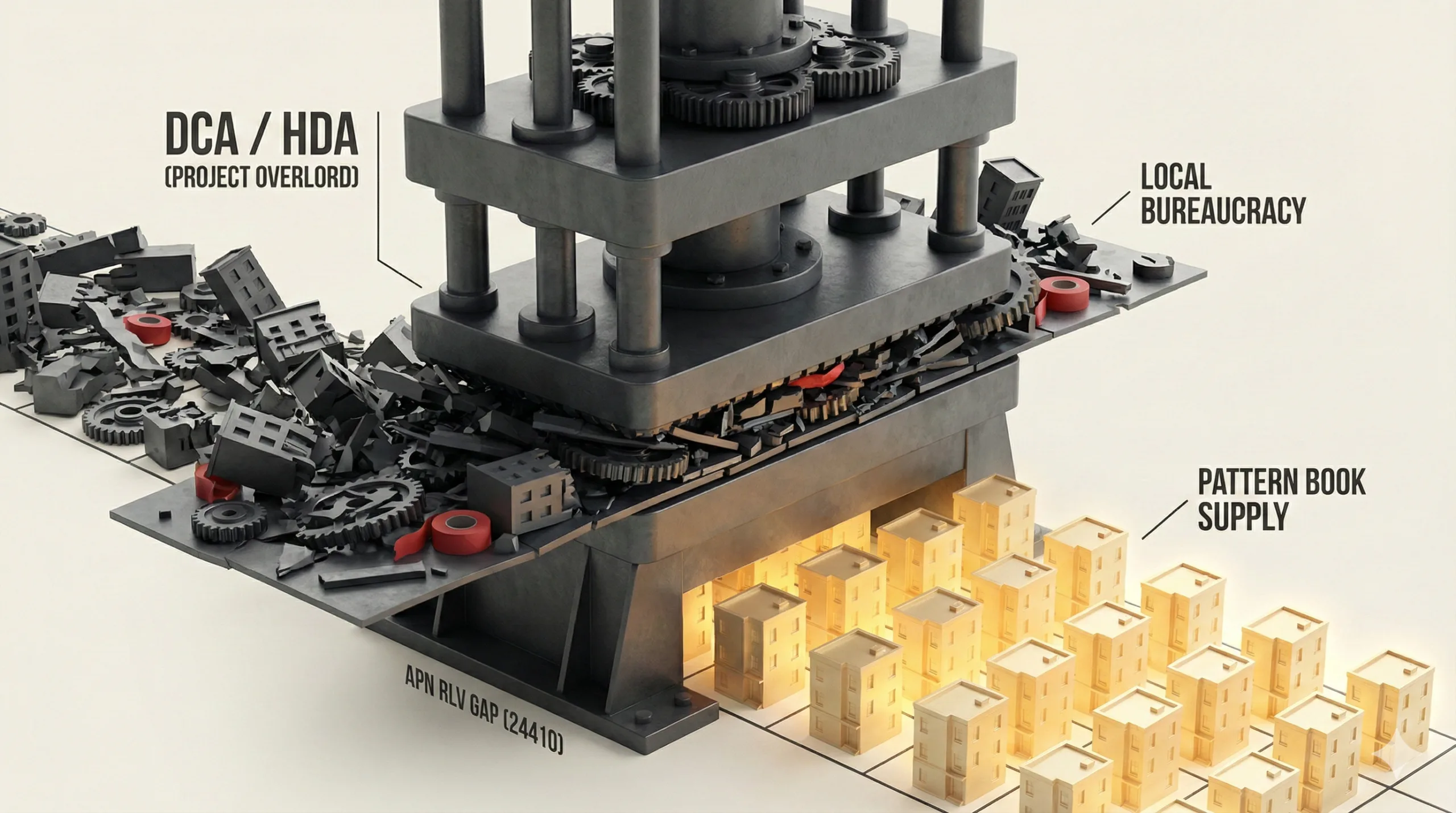

A Case Study in State-Level Intervention (APN SPCI, 24800): The establishment of the REZ, the declaration of infrastructure as CSSI (Critical State Significant Infrastructure), and the design of the Strategic Benefit Payments (SBP) scheme are direct, top-down interventions by the NSW Government. These actions override local planning and create new property rights (the right to an energy annuity) and uncompensated externalities, demonstrating that state policy is the primary driver of value creation and destruction in this market.

A Policy-Driven Divergence of Outcomes: The compensation framework is explicitly designed to channel financial benefits exclusively to “Power Hosts” while legally shielding operators from claims by neighbours. This legislative design actively reallocates financial benefits to a select group of landowners, re-classifying their assets into institutional-grade investments, while leaving adjacent properties to absorb the negative externalities, widening the gap between incumbent asset holders.

Quantifying the Premium (APN Infrastructure Uplift Multiplier™): The combination of the SBP annuity, “Just Terms” compensation, and private incentives creates a multi-layered financial benefit that can be measured by the APN IUM™. The analysis confirms that this uplift is not merely theoretical; it is a bankable, indexed income stream that fundamentally re-rates the asset from pure agriculture to a hybrid ‘Agri-Infra’ class, justifying a significant valuation premium.

Measuring the Discount (APN Agora™ Amenity & Access Index): The devaluation of “Amenity-Affected Properties” is a direct consequence of a negative shock to the APN Agora™ index. The imposition of 70-metre-high transmission towers materially degrades the “view shed” and introduces industrial characteristics into a rural landscape. In lifestyle-driven markets like Mudgee, where amenity is a primary value component, this negative shock is structurally significant for market value and liquidity.

Deconstruction of the Source Event

This deconstruction is based on APN’s synthesis of market data from Herron Todd White and Rabobank, NSW Valuer General reports, and the legislative architecture of the REZ compensation schemes. The key facts are:

- The Appreciating Baseline Market: The underlying Central-West Orana market is experiencing a period of material capital appreciation, decoupling from national trends. Key sub-markets recorded material year-on-year median land value growth in 2025, including Dubbo (+12.7%) and the Mudgee-Lithgow corridor (+109%).

- The “Power Host” Premium: Host landholders receive a multi-layered “Energy Annuity.” This includes a Strategic Benefit Payment (SBP) of $200,000 per kilometre of transmission line, paid as an indexed annuity of $10,000/km/year for 20 years, in addition to upfront capital compensation under the Just Terms Act and commercial sign-on incentives.

- The “Amenity-Affected Property” Discount: Neighbouring properties receive zero compensation for amenity loss. Stakeholder sentiment and agent advice suggest potential devaluations of 30-40% in lifestyle markets. Empirically, even a stagnant sale price in a market growing at over 12% constitutes a material relative discount and loss of opportunity cost.

- The Legislative Cause: The bifurcation is structurally enforced. SBP guidelines strictly limit payments to properties hosting an easement. Furthermore, the Land Acquisition (Just Terms Compensation) Act 1991 provides no mechanism for neighbours to claim for “injurious affection” or loss of amenity value caused by infrastructure on adjacent land.

Critical Analysis & Balanced View

The “Volt-Split Structural Adjustment” represents more than a simple valuation gap; it signals the emergence of “Energy Gentrification” in rural Australia. The analysis reveals that the core driver of the premium for “Power Hosts” is not just the quantum of the annuity, but its quality. A government-backed, inflation-indexed income stream carries a significantly lower risk profile than volatile agricultural income. Consequently, investors will apply a lower capitalisation rate (a higher valuation multiplier) to this portion of the income, permanently re-rating the asset class. A Power Host property is no longer a farm; it is a hybrid utility asset with an agricultural overlay.

Conversely, the situation for “Amenity-Affected Properties” is a paradox within a strongly appreciating market. Their loss is not necessarily a nominal fall in value from their purchase price, but a structurally significant loss of opportunity cost relative to their unencumbered peers. A property in the Mudgee region that fails to achieve significant capital growth between 2023 and 2025 has, in effect, suffered a material real-term devaluation. This is compounded by a material liquidity drag, as the pool of buyers for properties with compromised amenity shrinks materially. The legislative framework, by failing to provide any financial bridge for this loss, makes the state a direct participant in creating this two-tier market, prioritising the speed of infrastructure delivery over equitable economic outcomes for all affected landowners.

Strategic Implications for Property Professionals

- For Valuers: The standard methodology for rural valuation based on productive capacity or comparable sales is now insufficient in the REZ. Valuations for “Power Host” properties must incorporate a discounted cash flow (DCF) analysis of the indexed Energy Annuity, applying a lower, infrastructure-grade capitalisation rate. For “Amenity-Affected Properties,” a significant discount factor for stigma, amenity loss, and reduced liquidity must be quantified and applied, benchmarked against the rapid growth of the local baseline market.

- For Agents & Buyers’ Agents: Full and frank disclosure of a property’s proximity to planned REZ infrastructure is now an elevated risk management imperative. For vendors of impacted properties, managing price expectations is paramount; the key metric is not the historical purchase price but the value relative to unencumbered neighbours. For buyers, the long-term visual and market impact of the infrastructure must be a central part of due diligence, particularly in high-amenity lifestyle markets.

- For Investors & Fund Managers: “Power Host” properties represent a new, hybrid asset class combining agricultural yield with a low-risk, government-backed annuity. These assets offer portfolio diversification and inflation hedging, and should be assessed on a yield basis comparable to commercial or infrastructure assets, not just pure agricultural land. Identifying and acquiring these properties pre-construction offers the greatest potential for capitalising on the valuation uplift.

- For Developers & Land Bankers: The REZ is creating concentrated secondary impacts, such as the housing supply constraint in service hubs like Dubbo. This creates opportunities in residential and short-term accommodation development. Furthermore, understanding the land acquisition process and compensation mechanisms is vital for any party looking to assemble land parcels within the REZ footprint, as “Power Host” status fundamentally alters a landowner’s price expectations and negotiating position.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core thesis of the APN Sovereign Policy Composite Index™ (SPCI, 24800), demonstrating direct state intervention as the primary cause of market bifurcation. It provides a clear case study for the APN Infrastructure Uplift Multiplier™ (24420), quantifying the premium for Hosts, and validates the sensitivity of the APN Agora™ Amenity & Access Index (24140) to the negative shock of industrial infrastructure in lifestyle markets.

- Index Calibration: The APN Infrastructure Uplift Multiplier™ (24420) will be calibrated to specifically model the capitalisation of indexed, long-term energy annuities as a distinct value driver. The weighting of the “view shed” and “acoustic amenity” components within the APN Agora™ Index (24140) will be increased for postcodes identified as high-value “lifestyle” markets.

- Data Capture: This analysis triggers a new data capture mandate via the APN Symbiotic Intelligence Network™ (24310). The mandate is to actively track and differentiate sales data for properties directly adjoining REZ easements versus unencumbered properties in the same locality. This will allow for the empirical quantification of the “Amenity-Affected Property” discount over time, moving beyond sentiment to hard market evidence.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.