APRA Signals Preparation for Regulatory Intervention on High-Risk Investor Lending as Banks Breach Key Thresholds

APN ANALYSIS: A-251125-AUS131092

Executive Summary

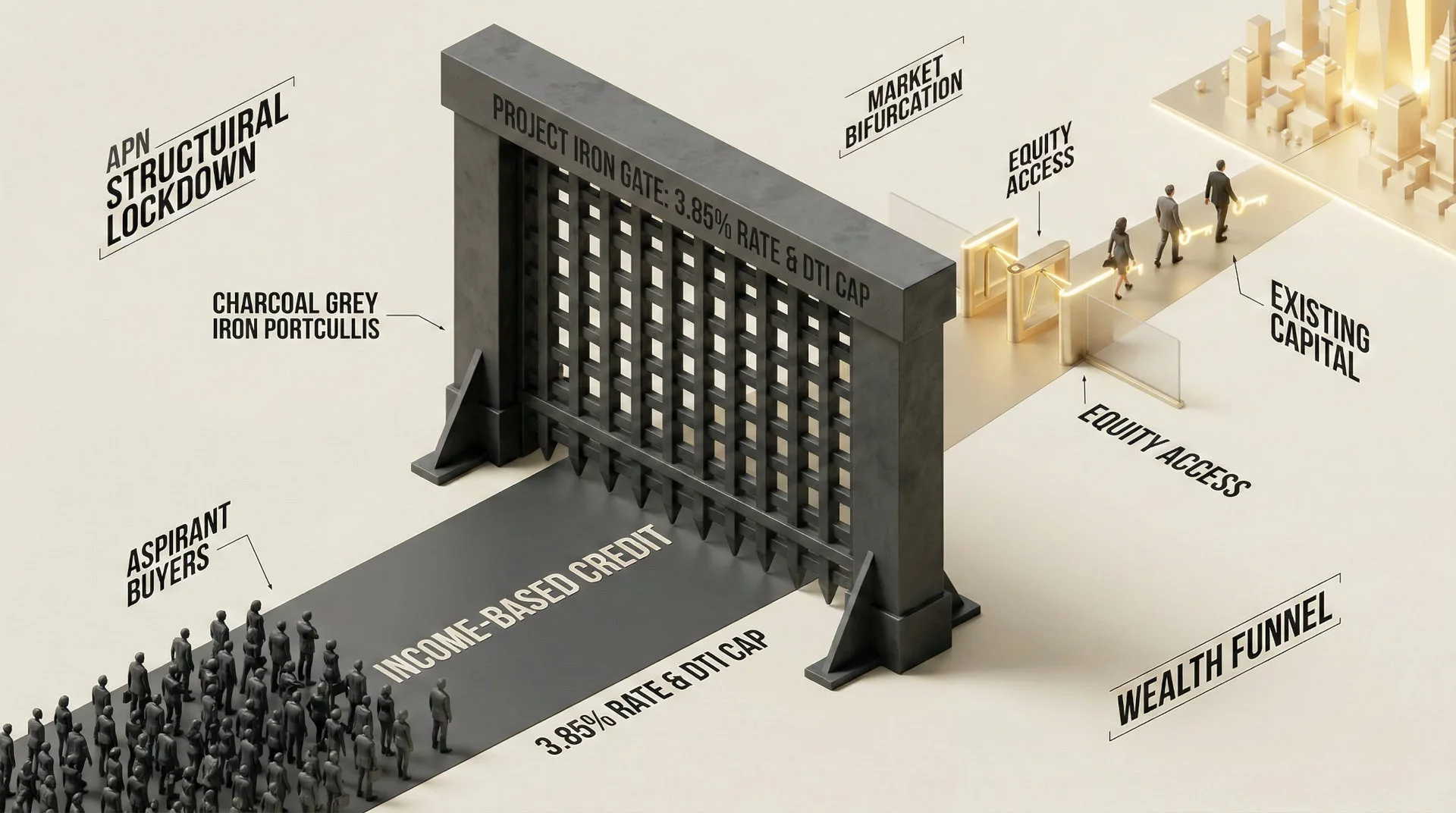

The Australian Prudential Regulation Authority (APRA) has issued a notable warning to the banking sector, signalling a shift from passive monitoring to active preparation for macroprudential intervention. An APN analysis of APRA’s November 2025 System Risk Outlook and associated lending data confirms that banks, driven by intense competition, are rapidly expanding high-Debt-to-Income (DTI) lending to property investors. New lending where debt is six times or more than income has breached the regulator’s informal 5% threshold, rising to 5.5%. This behaviour, facilitated by a record volume of serviceability waivers, has occurred despite prudential guidance and a high interest rate environment, triggering a high-velocity regulatory response that mirrors the pre-intervention conditions of 2014 and 2017.

For property professionals, this signals a diminishing opportunity for high-leverage investor financing. The market is approaching a material credit tightening event, likely to be formalised in the first half of 2026. Professionals must immediately advise clients that borrowing capacity is set to contract, particularly for the investor cohort. This regulatory intervention will moderate investor-led demand, potentially easing competition for A-grade assets and creating tactical opportunities for less-leveraged buyers and those with strong equity positions.

Background & Strategic Context

This development validates APN’s core macro-theses, demonstrating how state-level actors dictate market boundaries and risk parameters. The regulator’s explicit focus on a specific market segment (investors) and lending practice (high-DTI) is a direct application of state power to manage systemic risk, directly confirming the principles of the APN Sovereign Policy Composite Index™ (SPCI, 24800) and the APN Risk & Compliance Index™ (24200).

Regulatory Dominance (APN Sovereign Policy Composite Index™ (SPCI, 24800)): This event confirms that regulatory action, not just market sentiment, is the primary force shaping credit availability and risk appetite in the Australian property market. APRA’s explicit warnings and preparation for intervention demonstrate the state’s power to override commercial expansion and enforce prudential discipline.

Regulatory Velocity (APN Regulatory Velocity Multiplier™ – 24210): The shift in APRA’s language from passive monitoring to active preparation for intervention represents a significant acceleration in regulatory velocity. This moves the market from a ‘Warning Shot’ phase to an ‘Imminent Intervention’ footing, activating the APN RVM™ as a key indicator of impending policy change.

Risk Concentration: The analysis confirms the risk is not evenly distributed but is concentrated within the investor cohort, a group that has disproportionately benefited from prior credit cycles. APRA’s targeted focus on ‘high debt-to-income borrowing by investors’ is a direct attempt to manage the accelerator effect associated with this segment.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Australian Prudential Regulation Authority’s (APRA) November 2025 ‘System Risk Outlook’ and the associated ‘Quarterly ADI Property Exposures’ statistics for the June 2025 quarter. The key facts are:

- High-DTI Breach: New lending with a Debt-to-Income (DTI) ratio of six times or more has risen to 5.5% of all new loans, exceeding APRA’s informal 5% prudential threshold.

- Investor-Specific Risk: APRA explicitly attributes the rise in ‘higher risk lending’ to ‘high debt-to-income borrowing by investors’, isolating this cohort as the primary source of emerging systemic vulnerability.

- Intense Competition as a Driver: The regulator directly links the loosening of standards to ‘heightened competition’ among banks seeking to increase market share, confirming a competitive dynamic is overriding prudential caution.

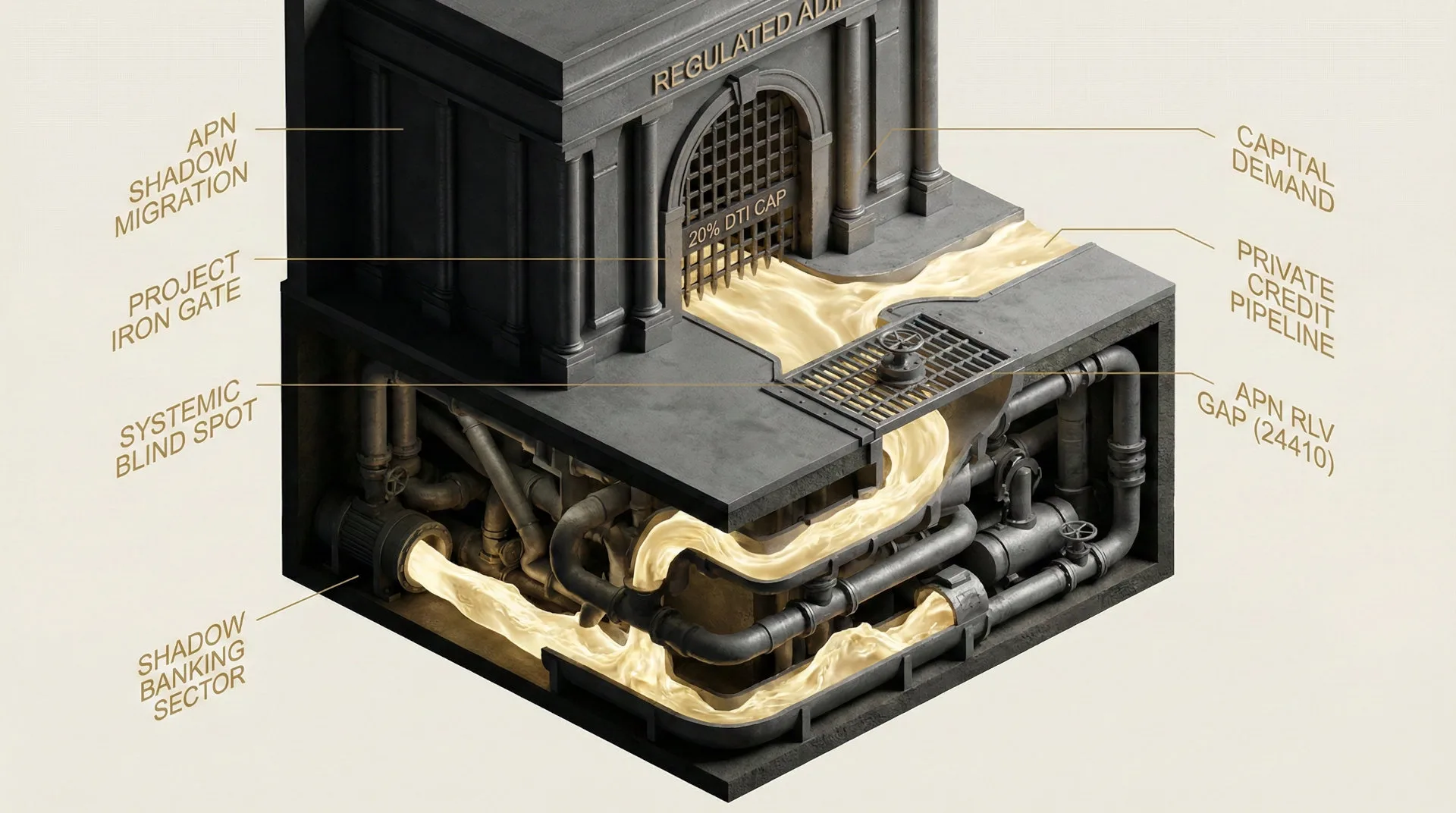

- Mechanism Identified: The increase in high-DTI lending is being mechanically facilitated by the record use of serviceability exceptions and waivers, which reached a combined total of over $13 billion, effectively bypassing the standard 3% serviceability buffer.

- Regulatory Posture Shift: APRA Chair John Lonsdale has moved from previous public statements to explicit warnings, stating the regulator is ‘prepared to implement additional macroprudential tools’, signalling a high probability of intervention.

Critical Analysis & Balanced View

The central analytical point of this event is why banks are expanding their risk appetite in a high interest rate environment, a time when serviceability constraints should naturally compress leverage. The evidence suggests this is not irrational behaviour but a calculated risk amid intense competition for market share. With modest overall credit growth, major banks are competing for volume by loosening underwriting standards for the investor segment, which they deem ‘attractive’. They are trading DTI risk for market share, likely rationalising the decision based on the perceived strength of their existing loan books and an assumption of continued asset price inflation to offset the risk.

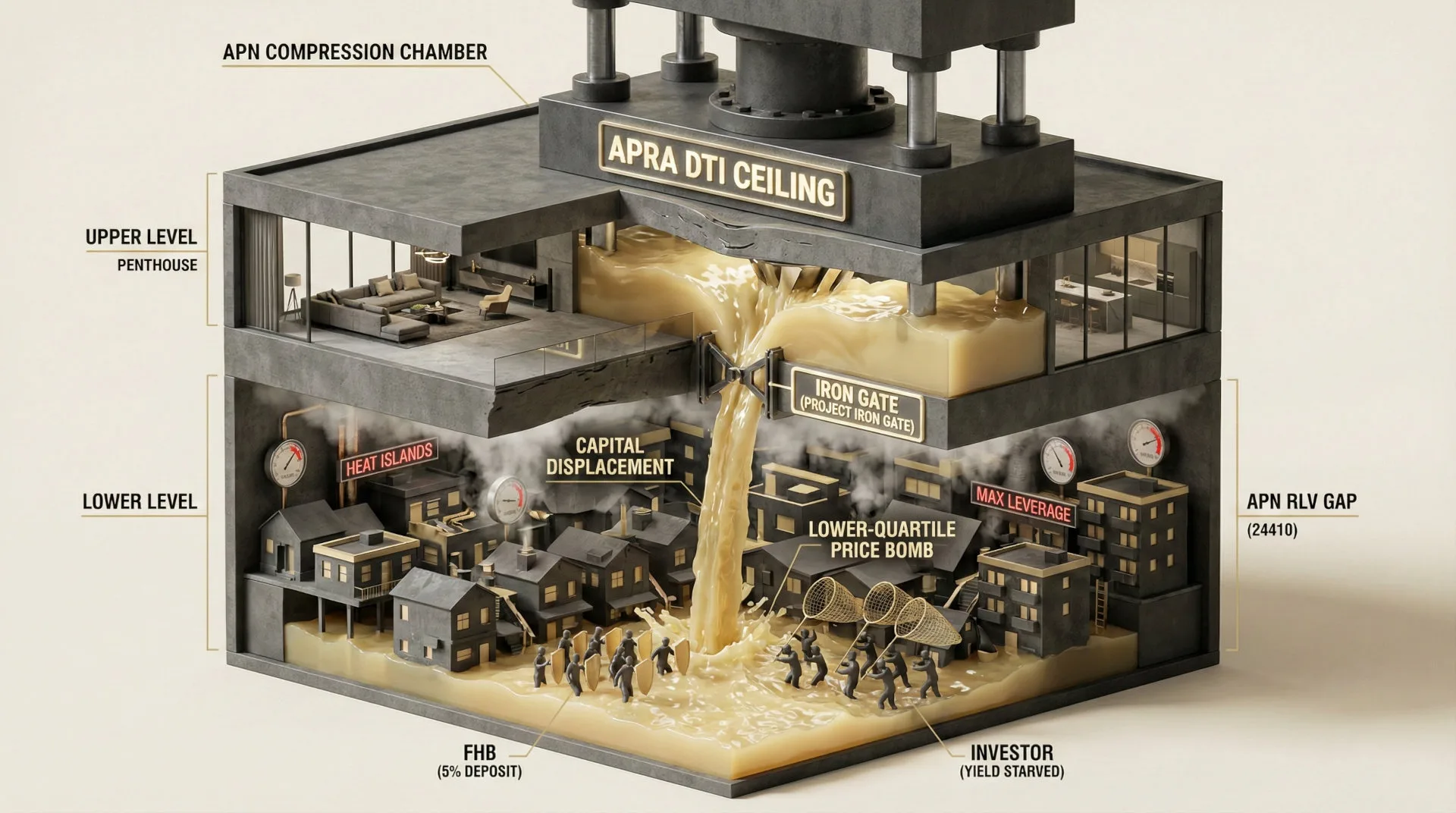

This creates a dual-front expansion of leverage, elevating systemic risk. At one end, highly leveraged investors are driving up DTI ratios. At the other, government initiatives like the expanded 5% Deposit Scheme are enabling higher Loan-to-Valuation (LVR) lending for first-home buyers. While APRA’s focus is currently on the investor-driven DTI risk, this dual-front expansion of leverage reduces systemic resilience. The urgency of APRA’s response is heightened by the deteriorating global geopolitical environment; the regulator cannot afford domestic structural vulnerabilities when the risk of an external shock is elevated. The regulator appears to be proactively reducing domestic systemic vulnerabilities in anticipation of potential external macroeconomic pressures.

Strategic Implications for Property Professionals

- For Mortgage Brokers & Lenders: Immediately prepare for a material contraction in credit policy. The period of widespread serviceability exceptions is ending. Your value proposition must shift from maximising loan size to strategic structuring and risk mitigation. Expect increased scrutiny and potential clawbacks on deals that may fail to meet incoming DTI caps.

- For Buyers’ Agents & Agents: The accelerated growth in investor activity is facing material regulatory constraints. Advise clients that borrowing capacity assessments from even a month ago may now be no longer valid. This will disproportionately impact highly leveraged investors, potentially reducing competition for A-grade stock and creating a tactical advantage for cash or low-leverage buyers.

- For Developers: The investor pre-sale market is about to tighten materially. Projects reliant on highly leveraged, off-the-plan investor sales face an elevated risk of settlement failure. Re-evaluate funding structures and target markets towards owner-occupiers or investors with stronger equity positions.

- For Property Valuers: Be prepared for increased scrutiny from lenders on valuations for investment properties, particularly in markets that have seen rapid price growth fuelled by investor demand. Lenders will be de-risking their balance sheets, and valuation conservatism will be their primary risk mitigation measure.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core thesis of the APN Sovereign Policy Composite Index™ (SPCI, 24800), confirming that regulatory bodies are the ultimate arbiters of market boundaries. It also provides a direct case study for the APN Risk & Compliance Index™ (24200), demonstrating a rapid shift in regulatory posture from monitoring to intervention.

- Index Calibration (APN RVM™ – 24210): The APN Regulatory Velocity Multiplier™ is calibrated to HIGH. The combination of a quantitative breach (DTI > 5%), specific attribution (investors), and forward-looking statements (‘preparing tools’) confirms a shift from passive monitoring to active intervention preparation.

- Data Capture (Symbiotic Intelligence Network™ – 24310): This analysis triggers a new data capture mandate within the APN Symbiotic Intelligence Network™. The focus is to monitor ADI policy changes regarding serviceability exceptions and investor-specific interest rate pricing on a weekly basis to provide a leading indicator of market retraction ahead of official APRA announcements.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.