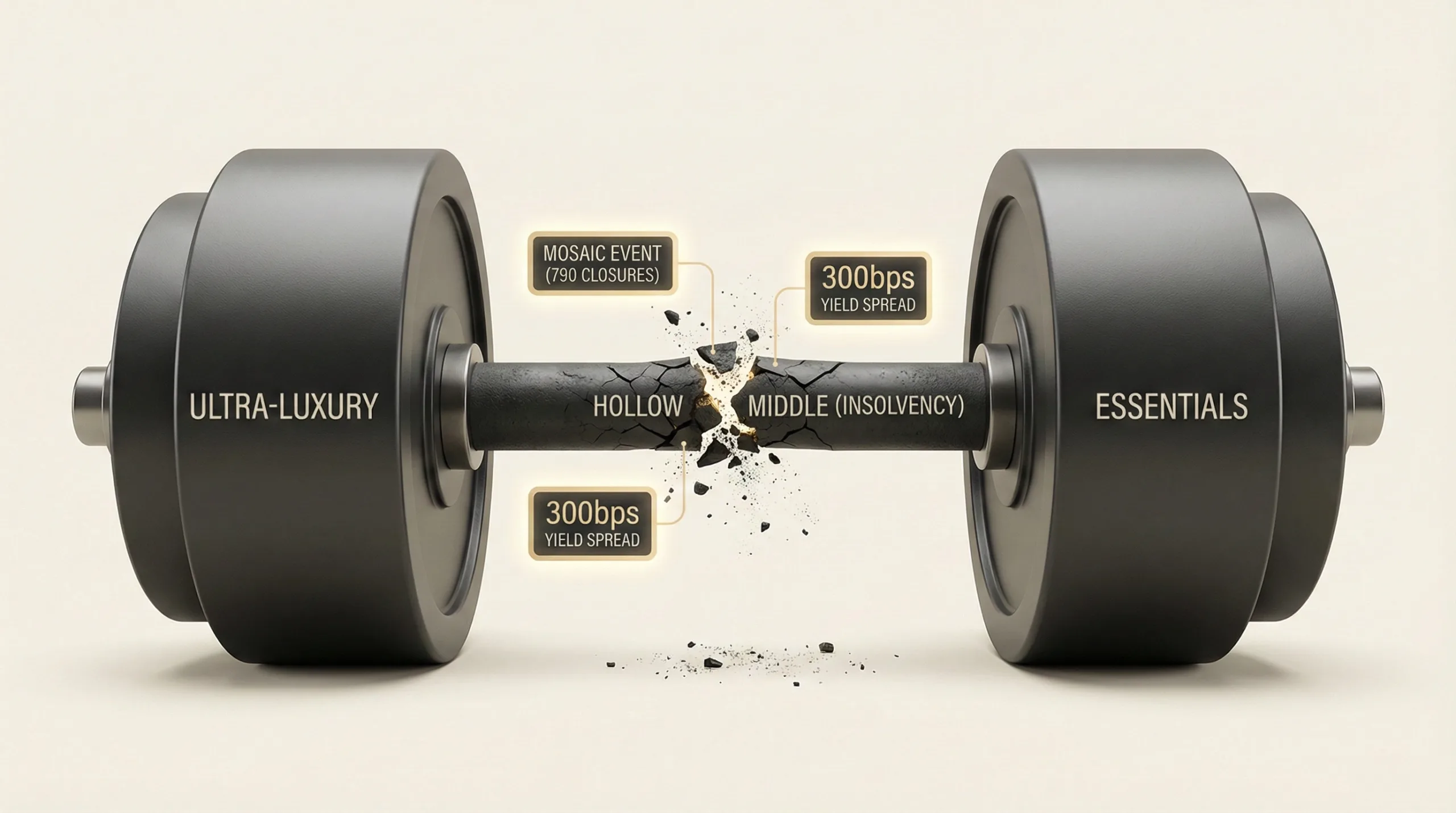

The Barbell Economy Confirmed: Australian Retail’s ‘Hollow Middle’ Is a Terminal Insolvency Event

APN ANALYSIS: A-251207-AUS131684

Executive Summary

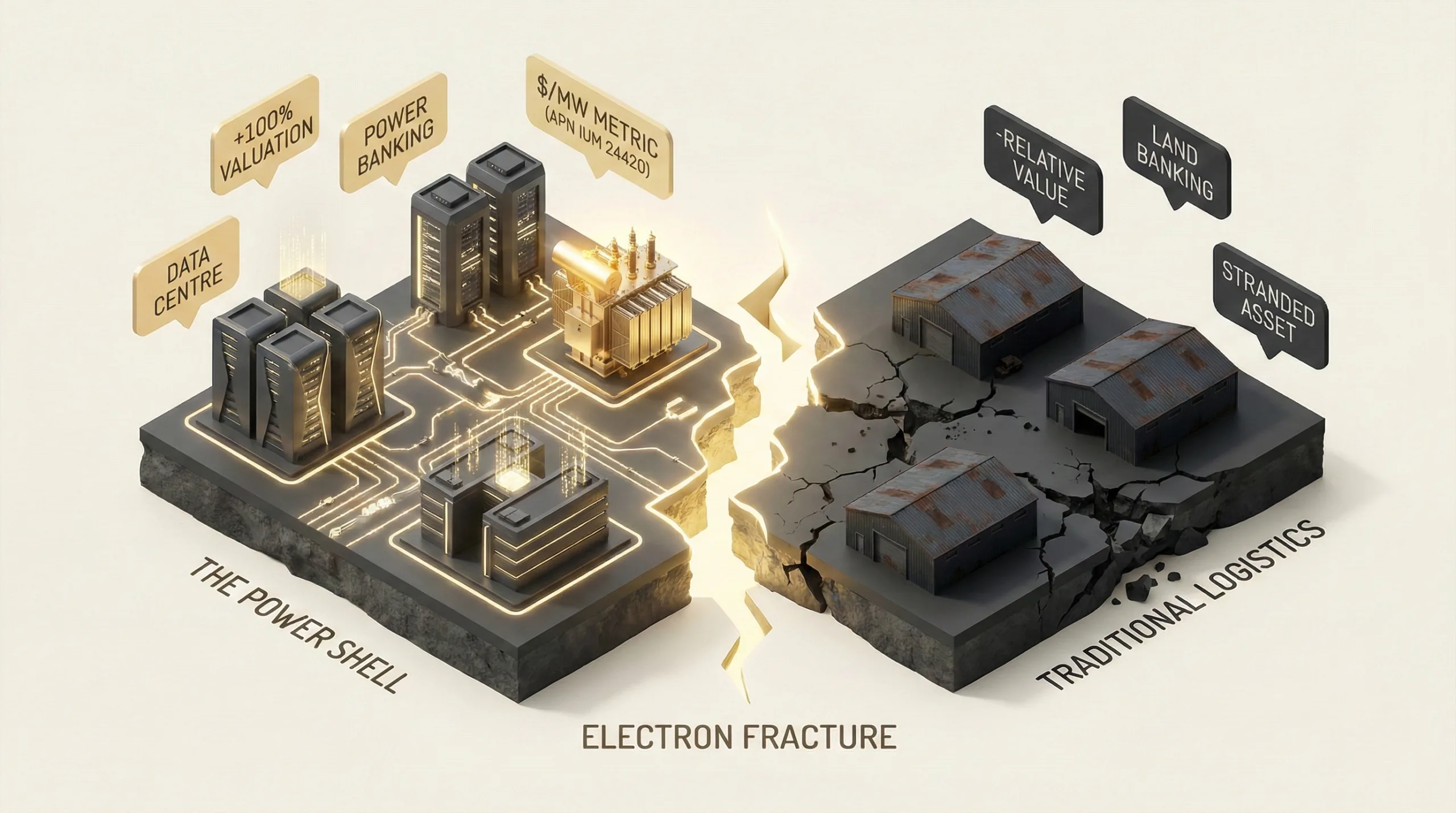

A forensic analysis of the Australian retail property landscape confirms the ‘Barbell Economy’ hypothesis with critical severity. The market has structurally fractured into two performing poles, Ultra-Luxury and Hyper-Local Essential, while the discretionary ‘Mid-Market’ is experiencing a terminal insolvency event, not a cyclical downturn. This is evidenced by the ‘Mosaic Event’, the liquidation of Mosaic Brands, which dumped approximately 700 vacancies into sub-regional centres, and a definitive 300+ basis point yield spread between secure, grocery-anchored assets (trading at ~4.6%) and distressed, discretionary-heavy malls (trading at ~7.75%). The market is no longer pricing risk; it is pricing the obsolescence of the mid-market retail model.

For property professionals, this signifies that sub-regional assets with high discretionary exposure are now ‘yield traps’. Their high income returns mask severe capital decay and imminent structural vacancy risk. The traditional model of a diversified mall is broken. Capital allocation must be decisively bifurcated, targeting the security of non-discretionary ‘fortress’ assets or the decoupled growth of the luxury ‘playground’, as the middle ground has become a leasing and investment desert.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses on market structure and capital flows. The collapse of the retail mid-market is a direct manifestation of state-level economic pressures and the subsequent concentration of wealth, proving that broad-based consumption infrastructure is no longer viable in the current economic climate.

The Bifurcation Fracture (APN Bedrock™): The social cohesion and community function of shopping centres are splitting. The APN Bedrock™ (24110) index maps this divergence, showing that while essential-anchored neighbourhood centres are strengthening their local ‘bedrock’, the sub-regional malls are suffering a catastrophic loss of their core purpose, becoming amenity-poor voids.

The Capital Flight to Safety (The Wealth Funnel): The extreme yield divergence is a textbook example of The Wealth Funnel in action. Decoupled high-net-worth wealth sustains the ‘Ultra-Luxury’ pole, while institutional capital, seeking bond-like security, floods the ‘Hyper-Local Essential’ pole. This leaves the mid-market starved of both consumer spending and investment capital.

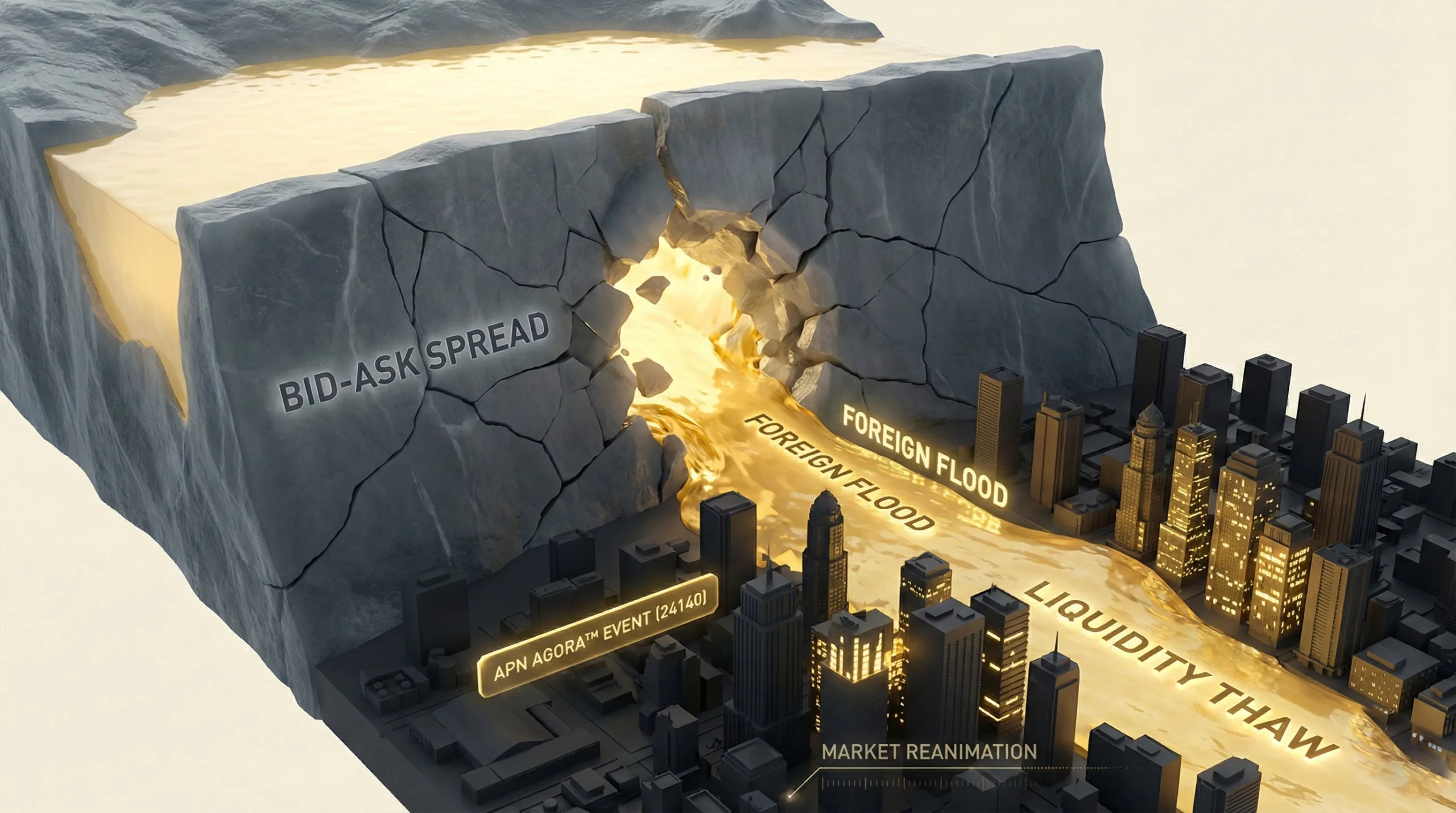

The Amenity Void (APN Agora™): The mass closure of ~800 stores from the Mosaic and Jeanswest collapses has created a critical ‘amenity void’ in sub-regional centres. The APN Agora™ (24140) index, which measures the value of a location’s amenity ecosystem, registers this as a structural downgrade, destroying the ‘cluster effect’ of fashion precincts and triggering a negative feedback loop of declining foot traffic and asset value.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of transaction data, proprietary research from Ray White Commercial, and market intelligence reports from late 2025. The key facts are:

- The ‘Mosaic Event’ Vacancy Shock: The complete liquidation of Mosaic Brands by April 2025, compounded by the collapse of Jeanswest, resulted in the closure of approximately 790 stores. This dumped an estimated 105,000-175,000 square metres of retail GLA onto the market, concentrated in the vulnerable sub-regional asset class.

- The Luxury Saturation Point: By late 2025, luxury retail stock in the Sydney CBD surged to represent 32.1% of all storefronts. This was not organic growth but a structural displacement of mid-market retailers, confirming the CBD’s transformation into a ‘sovereign luxury enclave’ decoupled from the domestic economy.

- The Yield Fracture: A definitive 316 basis point spread opened between the two poles of the market. ‘Hyper-Local Essential’ assets anchored by strong grocery covenants traded at yields as tight as 4.59% (Kurralta Village, SA), while ‘Discretionary-Distressed’ sub-regional assets required yields as high as 7.75% (Warrawong Plaza, NSW) to attract capital.

- The ‘Lipstick Effect’ Fallacy: The expansion of the ‘experience economy’ (e.g., Mecca, Sephora) is volumetrically and geographically incapable of backfilling the mid-market void. For every one new beauty store opening in 2025, approximately 40 mid-market fashion stores closed. Furthermore, these new tenants target ‘A-Grade’ fortress assets, leaving the ‘B-Grade’ sub-regional centres empty.

Critical Analysis & Balanced View

The most critical insight is the paradox of the sub-regional asset’s high total return (8.8%). This figure is a ‘false positive’ for health, driven entirely by a high income yield that is required by the market to compensate for profound capital risk and negative future growth prospects (1.9% capital growth vs 2.5% for neighbourhood centres). These assets are ‘melting ice cubes’, offering high cash flow today but are structurally impaired for tomorrow.

Similarly, the rising overall vacancy in the Sydney CBD (to 6.7%) amidst a luxury boom is not a contradiction but a confirmation of the ‘Hollow Middle’. The vacancy is not in the luxury sector; it is the footprint of the evicted or insolvent mid-tier retailers. This ‘tenant churn’ is the physical evidence of the barbell bifurcation in Australia’s premier retail precinct.

Finally, the strategy of major landlords like Vicinity Centres to ‘proactively reduce exposure’ to at-risk tenants is a portfolio management tactic, not a market solution. While it may protect their headline occupancy figures in the short term, it accelerates the hollowing out of the underlying tenant ecosystem, confirming the terminal diagnosis for the asset class as a whole.

Strategic Implications for Property Professionals

- For Asset Managers & Landlords: Immediately stress-test sub-regional portfolios for exposure to discretionary fashion and Discount Department Store (DDS) anchors. High income yields are a warning sign of capital decay, not health. Initiate strategies to pivot to non-retail uses (e.g., ‘med-tail’, last-mile logistics) or divest before the market fully prices in the structural insolvency.

- For Valuers & Financiers: Recalibrate valuation models for sub-regional assets. The 300+ basis point spread between essential and discretionary yields is the new benchmark for risk. Traditional capitalisation rate comparisons are obsolete; valuations must now factor in a ‘structural vacancy discount’ for mid-market tenancy profiles.

- For Developers & Leasing Agents: Focus acquisition and leasing mandates exclusively on the two performing poles. For luxury, target prime CBD and ‘fortress’ regional centres. For essentials, target neighbourhood centres with strong grocery anchors and ‘triple anchor’ potential. The middle ground is a leasing desert where tenant covenants are fundamentally broken.

- For Retail Strategists & Tenant Representatives: Advise clients to abandon the sub-regional mall strategy unless they operate in the non-discretionary or deep-value categories. The ‘cluster effect’ for fashion is dead. Future network planning must focus on prime high streets, fortress malls, or hyper-local convenience models that align with the bifurcated capital and consumer landscape.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides definitive validation for the APN Bedrock™ (24110) and APN Agora™ (24140) indices. The divergence in capital growth and yield between neighbourhood and sub-regional centres directly correlates with the strength of an asset’s social cohesion (Bedrock) and its amenity profile (Agora).

- Index Calibration: The APN Bedrock™ index is now calibrated to assign a significant negative weighting to centres with over 40% GLA exposure to discretionary mid-market fashion and DDS anchors, reflecting their diminished role as community hubs. The 316 bps yield spread between Kurralta Village and Warrawong Plaza will serve as the new benchmark for the risk premium calculation within the model.

- Data Capture: This analysis triggers a new data capture mandate for the APN Symbiotic Intelligence Network™ (24310) to track tenant liquidations by asset class, specifically mapping the GLA and location of vacancies from mid-market administrations to quantify the ‘Hollow Middle’ in real-time.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.