Sovereign Scale Asset Formation: The Role of 8MW Turbines and State-Backed Transmission in Concentrating NEM Investment

APN ANALYSIS: A-251127-AUS131254

Executive Summary

Equis, backed by sovereign wealth funds including the Abu Dhabi Investment Authority (ADIA) and Ontario Teachers’ Pension Plan (OTPP), has lodged plans for the Wanganella Wind Farm, an 840MW project in the NSW Riverina. This project is defined by its use of 8-megawatt turbines, a scale not previously deployed in the Australian market, creating a new ‘Sovereign Scale’ asset class entirely dependent on the future state-built Victoria-New South Wales Interconnector West (VNI West). This event validates the hypothesis that Australia’s energy transition is no longer about organic renewable development; it is a structural adjustment that facilitates a concentration of private asset creation. Publicly funded, nation-building infrastructure is now the primary catalyst for private asset creation, with technical and capital barriers so high that only the world’s largest institutional investors can participate, effectively concentrating market access.

For property professionals, this signals a substantive and sustained shift in the valuation of rural land. The economic driver of freehold land in strategic corridors is no longer agricultural yield but has become a direct derivative of its geospatial proximity to state-planned energy infrastructure. This bifurcation creates a two-tiered market where ‘strategic’ land becomes a high-yield financial instrument for a limited number of participants, while adjacent properties face potential value sterilisation from the industrial scale of the new infrastructure. Understanding the maps of these emerging energy corridors is now a critical component of due diligence and advisory.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses, demonstrating how state-level intervention is the primary force reshaping market boundaries and creating exclusive investment classes. The Wanganella project is a direct example of the interplay between state action, capital concentration, and regulatory triggers, confirming that the next phase of the National Electricity Market (NEM) will be dominated by a new class of geopolitical asset.

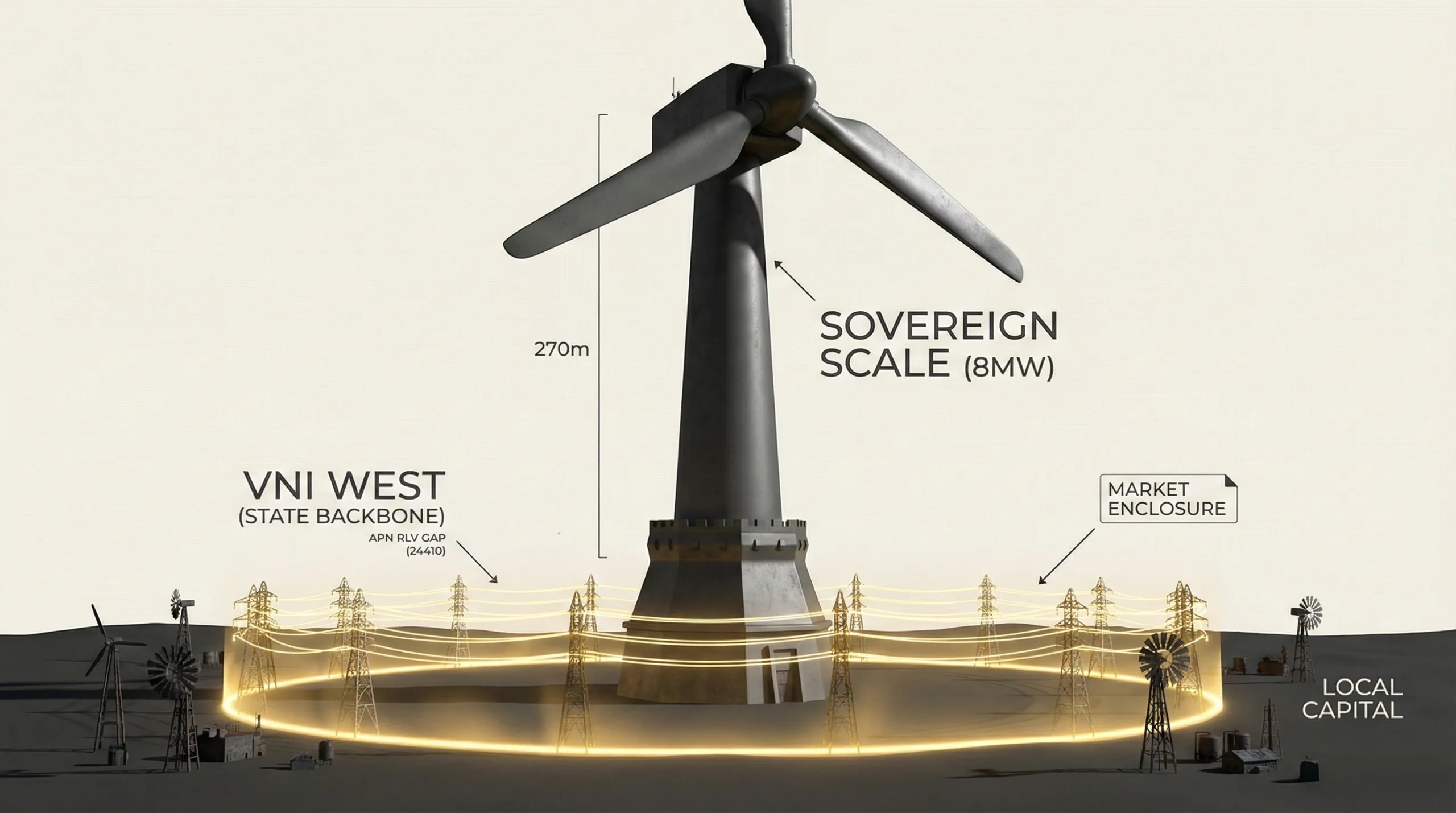

The State as Prime Mover (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The viability of the circa $2 billion Wanganella project is predicated on the NSW and Victorian governments delivering the 500kV VNI West transmission line. This confirms that state infrastructure planning is no longer just a market influence but the primary determinant of asset creation and value capture in the energy sector.

The Capital Filtration Mechanism: The shift to 8MW turbines and gigawatt-scale projects creates a material capital and logistical barrier. The substantial CAPEX and, importantly, the ability to absorb a potential two-year revenue gap—the ‘Stranded Asset’ risk—restricts participation to sovereign-scale balance sheets like ADIA and OTPP, reallocating the returns from public infrastructure to a specific cohort of global capital investors.

The Value Catalyst (APN Infrastructure Uplift Multiplier™): The land’s value is no longer based on its intrinsic agricultural utility but is derived almost entirely from its geospatial relationship to the VNI West corridor. The project is a physical manifestation of the APN IUM™, where the state’s infrastructure decision creates a significant, localised land value uplift captured by the entity positioned to benefit from the value uplift.

The Trigger Point (APN Regulatory Velocity Multiplier™): The investment was not speculative but programmatic. Equis lodged its EPBC referral just four months after Transgrid confirmed the VNI West route and timeline. This precise timing demonstrates a strategy driven by ‘Regulatory Velocity,’ where capital is deployed only after state action de-risks the core investment thesis.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Wanganella Wind Farm EPBC Act Referral 2025/10359 and associated state infrastructure planning documents. The key facts are:

- Project Scale & Technology: The proposal is for an 840MW wind farm comprising 105 turbines, each with a nameplate capacity of approximately 8MW. This represents a 33-60% increase in per-unit capacity compared to the 4-6MW turbines that are standard in the Australian market.

- Change to Land Use and Zoning: The turbines have a maximum tip height of 270 metres. This vertical scale materially changes the land use to be consistent with an industrial zone and effectively precludes the immediate area for activities like aerial agriculture due to physical collision risk and significant wake turbulence.

- Critical Grid Dependency: The project is explicitly designed to connect to the proposed 500kV VNI West transmission line, with the referral noting the ‘co-location’ as a key feature. The 840MW injection capacity makes the project technically and financially unviable on the existing regional network.

- Firming & Storage Capacity: The project includes a 600MW / 2400MWh Battery Energy Storage System (BESS), a 4-hour duration system designed for energy arbitrage and firming. This large-scale storage component, representing over $1 billion AUD in CAPEX, is essential to manage price cannibalisation in the modern NEM.

- Sovereign Ownership: The proponent, Equis Wind Australia, is majority-controlled by the Abu Dhabi Investment Authority (ADIA) and the Ontario Teachers’ Pension Plan (OTPP), entities with capital depth measured in the hundreds of billions of dollars, enabling them to absorb the project’s substantial scale and risk profile.

Critical Analysis & Balanced View

The most notable insight is the paradox of the ‘Stranded Asset’ risk. A notable 18-24 month gap exists between the wind farm’s target commissioning date (2027) and the transmission line’s earliest availability (2029). For a typical ASX-listed developer, this pre-revenue phase would be financially unviable; the carrying costs on a non-revenue-generating $2 billion asset would trigger insolvency. However, for sovereign capital, this structural impediment serves as a competitive advantage. The ability to absorb this multi-year delay acts as the final capital filter, a competitive ‘moat’ that ensures only entities with substantial, long-duration balance sheets can participate. This temporal misalignment, coupled with the highly competitive Renewable Energy Zone (REZ) access auctions, is not an unintended consequence but a structural characteristic of the market design, ensuring market participation is limited to the largest entities. The project is not just resilient to regulatory lag; it is structured to deploy it as a barrier to entry.

Strategic Implications for Property Professionals

- For Valuers & Agribusiness Consultants: Rural land valuation models require substantive recalibration. Properties within designated REZ corridors or near proposed transmission lines must be assessed not just on agricultural productivity but on their ‘energy yield’ potential. This introduces a new ‘highest and best use’ consideration, creating a significant valuation gap between strategic and non-strategic holdings.

- For Developers & Strategic Land Acquirers: The opportunity for mid-scale renewable development is contracting. Future opportunities lie in either servicing the ‘Sovereign Scale’ giants (e.g., providing ancillary services, logistics, accommodation) or identifying smaller, niche grid connection points that fall below the 500kV threshold. Attempting to compete on a like-for-like basis is now a material challenge for entities with smaller balance sheets.

- For Agents & Buyers’ Agents: A new due diligence layer is essential for all rural and peri-urban transactions. Proximity to energy infrastructure can have divergent outcomes. While it can signal material uplift for a few landholders, for surrounding properties it can mean value sterilisation due to visual amenity loss, construction disruption, and operational constraints. Mapping these energy corridors is no longer optional.

- For Institutional Investors & Funds: The Wanganella project provides the model for the next wave of Australian infrastructure investment. The model is clear: partner with state-sponsored infrastructure, leverage elevated scale to create structural barriers to entry based on capital requirements, and structure assets to withstand the regulatory and construction delays that would render smaller competitors commercially unviable. The primary risk is no longer market demand, but securing exclusive access to the grid.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides validation for the thesis of concentrated capital allocation and the primary causal role of the APN Sovereign Policy Composite Index™ (SPCI, 24800). It confirms that state-led infrastructure (VNI West) is the primary catalyst creating a new, exclusive asset class accessible only to sovereign-grade capital.

- Index Calibration (APN IUM™ 24420): The Wanganella project serves as a new benchmark for the APN Infrastructure Uplift Multiplier™. The index will be calibrated to model the elevated value differential between rural land with and without direct access to 500kV transmission corridors.

- Index Calibration (APN RVM™ 24210): The four-month lag between the VNI West EIS release and the Wanganella referral provides a key data point for the APN Regulatory Velocity Multiplier™, quantifying the ‘Asset Mobilisation Window’ for sovereign-grade capital.

- Data Capture (APN Substrate™ 24150): The change in land use in the Riverina landscape and the effective preclusion of land for certain agricultural uses triggers a data capture mandate. APN Substrate™ will now track the ‘land use conversion’ impact of large-scale renewable projects as a factor in regional adaptive capacity and economic resilience.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.