Sovereign Risk Premium in Residential Property: Divergent State and Federal Policy Settings and Their Effect on Investment Viability

APN ANALYSIS: A-260322-AUS138458

Executive Summary

The Australian residential property market is experiencing a measurable structural shift, driven by the interaction of two opposing policy mandates. State governments, led by the ACT, are legislating housing as a human right, introducing administrative complexity and legal risk for property owners. Simultaneously, the Reserve Bank of Australia is maintaining a restrictive monetary policy, with a 4.10% cash rate constraining household borrowing capacity and debt-servicing ability. APN analysis indicates this misalignment between social policy objectives and capital feasibility has generated a sovereign risk premium for residential assets. The effect is a deterioration in the viability of investment models, reduced new supply, and a migration of capital toward the unlisted private credit sector.

For property professionals, the primary determinants of market outcomes have shifted. Regulatory architecture and the friction between competing government objectives now define the market’s effective boundaries more than conventional supply and demand metrics. Competency in jurisdictional policy risk assessment, administrative friction quantification, and capital bifurcation analysis has become operationally necessary. Project and investment viability now depends on correctly pricing this sovereign risk premium.

Background & Strategic Context

This analysis validates and calibrates APN’s core macro-thesis that state-led intervention has become a primary determinant of asset liquidity and valuation, operating alongside rather than simply displacing traditional market forces. The interaction between legislative mandates and macroprudential policy creates systemic friction that requires a multi-dimensional measurement framework.

The State Intervention Framework (APN Sovereign Policy Composite Index™): The 24800 APN Sovereign Policy Composite Index™ (SPCI) is designed to measure this exact phenomenon. The divergence between the RBA’s mandate to suppress demand and the ACT’s mandate to provide housing irrespective of commercial viability produces a negative reading on the SPCI, indicating a high degree of policy-induced market friction.

The Regulatory Friction Matrix (APN Risk & Compliance Index™): The 24200 APN Risk & Compliance Index™ quantifies the operational drag created by these interventions. The introduction of human rights criteria into tenancy law, coupled with APRA’s DTI lending caps, increases administrative complexity and compliance costs, effectively rationing credit and excluding marginal capital from the regulated market.

The Social Licence Framework (APN Social Capital Index™): The 24100 APN Social Capital Index™ provides the lens to measure the qualitative impacts. The policy divergence tends to sharpen the adversarial framing of the landlord-tenant relationship in public discourse, eroding the social licence for property investment. This is captured as a negative calibration in the APN Sentinel™ (Safety & Sentiment Index), as reputational and sentiment risk become material financial considerations.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of concurrent legislative, monetary, and macroprudential policy shifts occurring throughout 2025 and early 2026. The key facts are:

- Restrictive Monetary Policy: On 17 March 2026, the Reserve Bank of Australia raised the official cash rate to 4.10%, the second consecutive hike of the year, citing persistent inflationary pressures and a tight labour market. This directly increases capital costs and constrains household borrowing capacity.

- Legislative Entrenchment of Housing Rights: In 2025, the ACT Legislative Assembly passed the Human Rights (Housing) Amendment Bill, making it the first Australian jurisdiction to formalise a statutory right to adequate housing. This introduces new legal considerations for landlords, particularly regarding evictions and tenancy management.

- Household Fiscal Pressure: Roy Morgan projects that a 4.10% cash rate will place 26.6% of mortgage holders (1.319 million households) in the ‘At Risk’ category. This represents a greater than two standard deviation event from historical averages, indicating limited capacity within the consumer base to absorb higher rents or prices.

- Institutional Loan Book Stability: Despite household pressure, APRA data for December 2025 shows non-performing loans in the regulated banking sector at a historically low 0.99%. This reflects the operation of macroprudential exclusion mechanisms rather than an absence of underlying stress.

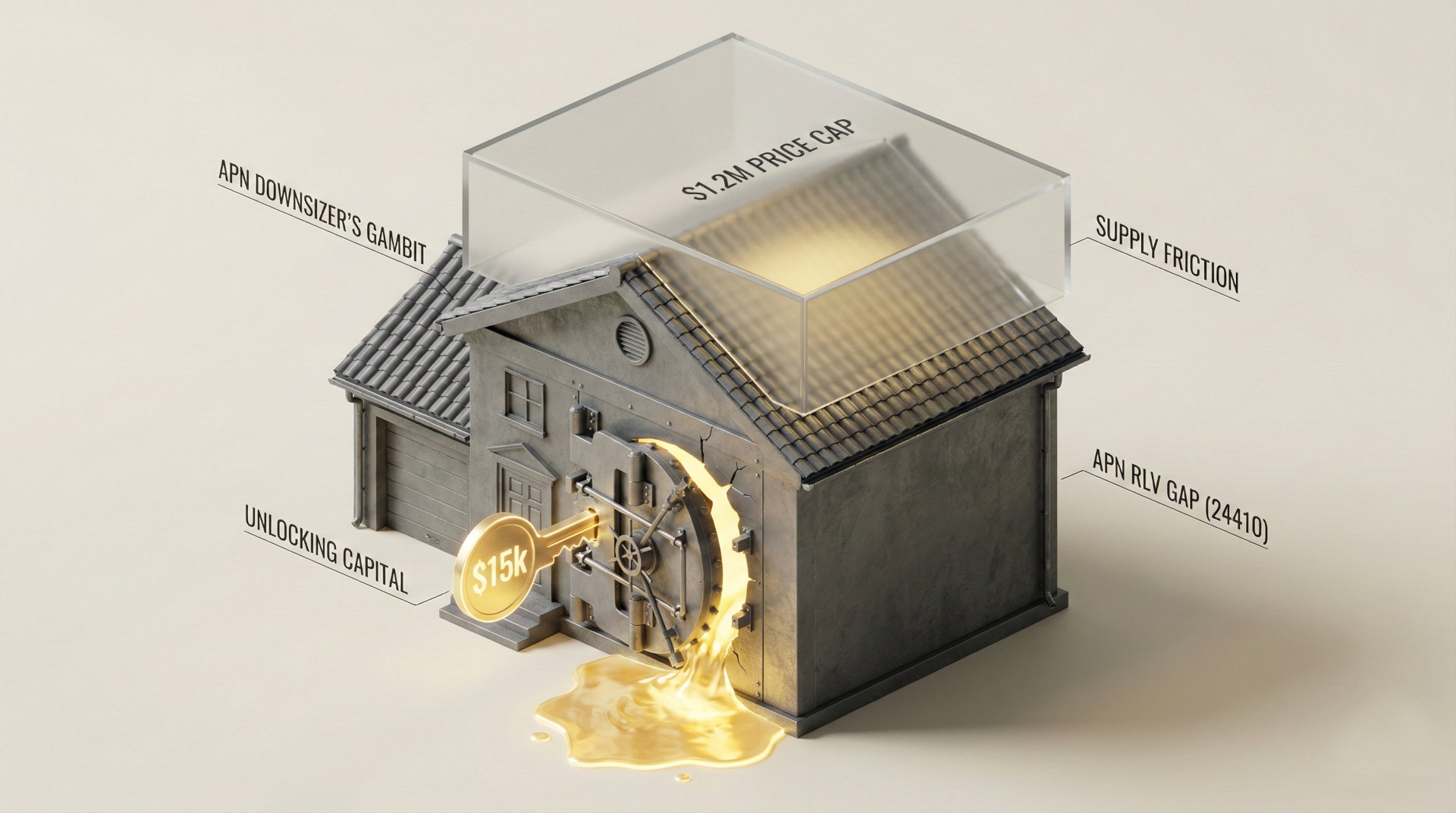

- Capital Migration to Private Credit: Capital excluded from the regulated banking system by APRA’s DTI limits is migrating to the unlisted private credit sector. This market, valued at over $224 billion, has become the primary funding mechanism for higher-risk development projects, with pricing that reflects the sovereign risk premium through wider interest rate spreads.

Critical Analysis & Balanced View

The central analytical tension in the current market is the gap between household fiscal pressure and institutional default rates. Roy Morgan’s data indicates a consumer base operating near its debt-servicing limits; APRA’s non-performing loan statistics simultaneously indicate stability within the banking system. These are not contradictory readings; they are the intended outcome of macroprudential policy design.

The APN Credit Rationing Index™ (24230) demonstrates that APRA’s DTI limits and serviceability buffers are functioning as designed: they prevent high-risk borrowers from entering the regulated system, protecting bank balance sheets while constraining marginal capital availability. The underlying stress has not been resolved; it has been displaced. Risk moves out of the transparent, lower-cost ADI sector and into the unlisted, higher-cost NBFI and private credit markets.

The Null Hypothesis — that capital risk is being successfully contained — is therefore only partially correct. Systemic bank failure is not the immediate concern. The cost of this stability is the parallel development of an unlisted, less-regulated liquidity system operating at a significant interest rate premium. That premium, paid by developers and complex borrowers accessing private credit, is the direct quantitative expression of the sovereign risk premium: the price of navigating the friction between the state’s social housing objectives and the central bank’s financial stability mandate.

Strategic Implications for Property Professionals

- For Developers: The APN Residual Land Value (RLV) Gap™ is the most critical viability metric in the current environment. Project feasibility models should assume debt financing from higher-cost private credit sources rather than traditional ADI lending. Extended time and cost contingencies for compliance navigation should be factored in, particularly in jurisdictions with expanded tenancy legislation.

- For Investors & Landlords: Jurisdictional risk analysis is now a standard pre-acquisition step. The risk-adjusted return premium required to invest in the ACT, given its human rights legislative framework, has increased measurably. Acquisition models that do not quantify administrative and legal risk should be treated as incomplete. Capital allocation toward jurisdictions with more commercially stable tenancy frameworks warrants consideration.

- For Agents & Buyers’ Agents: Client education should address the market’s bifurcation. Preference for established housing with a strong replacement cost position is a rational response to completion and quality risk in the off-the-plan sector. Articulating the relative stability of existing assets against new-build uncertainty is a substantive value proposition.

- For Lenders & Brokers: The credit market has bifurcated structurally. ADIs will increasingly concentrate on low-DTI, prime owner-occupier lending, a competitive but narrowing segment. The growth segment lies in structuring transactions for the NBFI and private credit sector, which requires a higher degree of specialisation in complex commercial and development finance.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides empirical validation for the 24800 APN Sovereign Policy Composite Index™ (SPCI), demonstrating how opposing sovereign mandates, federal monetary policy versus state legislative housing rights, generate a measurable, negative market outcome.

- Index Calibration: The 24200 APN Risk & Compliance Index™ is recalibrated to assign higher weighting to legislative interventions that alter fundamental property rights, such as the ACT’s housing amendment. This is classified as a high-impact event within the APN System Friction Index™ sub-component.

- Index Calibration: The APN Sentinel™ (Safety & Sentiment Index) is adjusted to reflect measurable shifts in public discourse relating to property investment. Adverse sentiment and reputational risk are formally weighted as material investment considerations.

- Data Capture: This analysis triggers a new data capture mandate to systematically track and compare advertised interest rate spreads between ADI-funded development loans and those offered by the unlisted private credit sector. This spread will serve as a direct quantitative proxy for the sovereign risk premium over time.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All APN proprietary indices referenced in this analysis are the intellectual property of Australian Property Network.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.