The Energisation Constraint: How a Global Transformer Shortage Has Immobilised $4.2 Billion in Australian Housing Stock

APN ANALYSIS: A-260120-AUS134937

Executive Summary

A fundamental decoupling of civil completion from electrical energisation has created a structurally adverse new class of ‘immobilised assets’ across Australia’s residential land market. APN analysis confirms that a conservative baseline of 12,000 physically completed housing lots are currently withheld from settlement, rendered legally uninhabitable due to material constraints in power infrastructure. This represents a capital lockout of approximately $4.2 billion held in a state of indefinite suspension. The structural pressure point is not a transient logistical hiccup; it is the manifestation of a global supply chain structural adjustment in essential grid components, specifically distribution transformers, intersecting with an inflexible domestic regulatory framework and elevated demand from the AI and EV sectors.

For property professionals, this ‘Energisation Constraint’ represents a permanent structural shift in development timelines and feasibility. The historical 12-week lead time for transformers has been materially altered, replaced by a new reality of 14 to 18 months. This structurally disrupts traditional development models that rely on the rapid recycling of capital post-completion, introducing elevated holding costs, escalating insolvency risk in the civil construction sector, and creating a ‘phantom supply’ of land that exists on paper but is undeliverable. This is now the primary constraint on achieving national housing supply targets.

Background & Strategic Context

This event validates and calibrates APN’s core macro-thesis, APN Sovereign Policy Composite Index™ (SPCI, 24800), demonstrating how global supply chain structural adjustments, when filtered through inflexible domestic regulatory frameworks, become the primary force shaping market boundaries and resulting in capital impairment. This dynamic results in a capital lockout and the creation of ‘commercially unviable’ land assets, whereby developers with deep capital reserves can sustain the extended holding period while smaller entities face insolvency, leading to a concentration of market power.

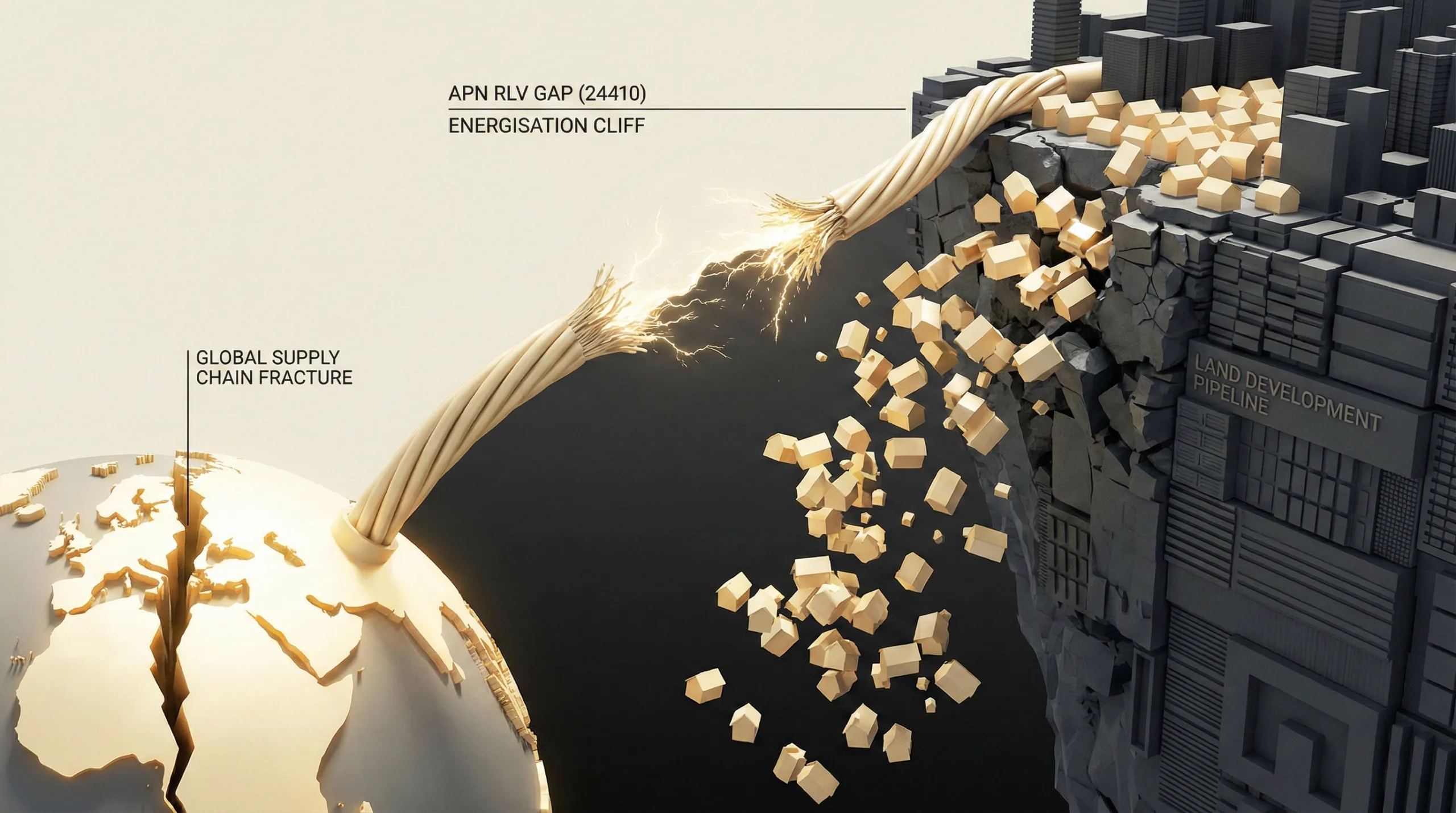

The APN Residual Land Value (RLV) Gap™: The 14-18 month energisation lag creates a material APN Residual Land Value (RLV) Gap™. The holding costs, land taxes, and interest accrued during this ‘dead time’ erode project profitability to the point of unviability, transforming thousands of zoned lots from ‘Genuine Opportunities’ into ‘Paper Rezonings’.

Regulatory Delivery Friction Point (APN Risk & Compliance Index™ (24200)): The structural pressure point is exacerbated by regulatory inertia. The inability of utilities like Western Power and Endeavour Energy to adapt their connection processes, and the slow pace of ‘Works in Kind’ (WIK) agreement negotiations in NSW, exemplify a low APN Regulatory Velocity Multiplier™. The system is too slow and rigid to respond to the external supply shock.

Social Capital Structural Adjustment (APN Social Capital Index™ (24100)): The emergence of ‘Dark Estates’ and ‘Ghost Suburbs’ in places like Donnybrook and Ripley Valley represents a structurally significant failure of the APN Agora™ (Amenity & Access Index). The absence of the most basic utility—power—renders all other amenities useless, eroding social cohesion (APN Bedrock™) and creating a cohort of financially distressed buyers constrained in a state of limbo.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing, ‘DarkEstates’, which synthesised data from the UDIA, CCF, Energy Networks Australia, and global supply chain intelligence. The key facts are:

- Immobilised Inventory Volume: A conservative baseline of 12,000 residential lots are physically complete but cannot be settled due to power connection failures. The true figure, including rezoned but unserviced land in NSW, likely exceeds 24,000 lots nationally.

- Capital Lockout Value: Based on a blended average land value of $350,000, the 12,000 immobilised lots represent $4.2 billion in immobilised capital, accruing holding costs while generating zero revenue.

- Lead-Time Escalation: The procurement lead time for essential distribution transformers has materially escalated from a historical 12-16 weeks to a current 52-80 weeks (14-18 months). Large Power Transformers (LPTs) face delays of up to 48 months.

- Primary Cause: The shortage is driven by a global scarcity of Grain-Oriented Electrical Steel (GOES), exacerbated by elevated competing demand from the Electric Vehicle (EV) and Artificial Intelligence (AI) data centre sectors, which are absorbing manufacturing capacity.

- Primary Affected Localities: The structural pressure point is most concentrated in Melbourne’s Northern Corridor (Donnybrook/Mickleham), SEQ’s Ripley Valley, and Perth’s growth corridors, where ‘Dark Estates’ are a physical reality.

- Identified Workaround: The ‘Diesel Solution’: A ‘Diesel Solution’ has emerged, where developers use industrial generators to power estates, creating a secondary source of risk from environmental non-compliance, regulatory fines, and material reputational damage.

Critical Analysis & Balanced View

The analysis reveals a structural paradox: Australia’s push to become a digital economy leader is directly constraining its ability to house its population. The ‘AI arms race’ is not a virtual phenomenon; it is a physical one, with hyperscale data centres outbidding the entire residential sector for the same critical grid components. This creates a direct, zero-sum conflict between housing supply and digital infrastructure growth, a dynamic we term the ‘AI Vampire’ effect.

Furthermore, the industry’s pivot to a ‘Diesel Solution’ exposes an elevated vulnerability in the ESG narrative of major developers. Marketing 7-star, all-electric, ‘green’ homes while powering the estate’s early stages with diesel generators is a clear instance of unverified ESG claims. This is not just a reputational risk; it is a regulatory one, as EPA Victoria’s enforcement actions demonstrate. This ‘Fake Green’ paradox presents a risk of devaluing the ESG credentials developers have spent years building.

Finally, the structural pressure point creates ‘phantom supply’ in official housing data. The 24,000+ lots in NSW’s Wilton and Appin growth areas are counted in long-term pipelines but are functionally non-existent for the short-to-medium term. This provides a dataset that does not adequately reflect the underlying supply constraint for policymakers and capital markets, masking the true materiality of the supply deficit. The problem is not a lack of zoned land, but a lack of serviceable land.

Strategic Implications for Property Professionals

- For Developers & Financiers: Immediately recalibrate all project feasibilities and delivery timelines. The primary determining factor is no longer civil completion but transformer procurement. Capital must be allocated for ordering electrical infrastructure at the Development Application stage, not the civil tender stage, to hedge against the 18-month lead time. Projects without a confirmed transformer delivery slot carry an elevated risk of failure.

- For Valuers & Risk Assessors: ‘Practical completion’ is no longer a reliable milestone for valuation. A new risk category, ‘Energisation Status,’ must be applied to all greenfield subdivision projects. Assets without a confirmed grid connection date must be devalued to account for indefinite holding costs, potential financing breaches, and market illiquidity.

- For Civil Contractors: The viability of linear ‘dig and deliver’ project models is diminished. Pivot to integrated project models that account for ‘stop-start’ workflows caused by component delays. Diversify service offerings to include temporary power solutions (BESS, not just diesel) and asset relocation services to capture revenue from the delivery friction points themselves. The ‘lineworker gap’ also presents an opportunity for firms that can attract and retain specialised electrical talent.

- For Agents & Buyers’ Agents: Exercise elevated due diligence on off-the-plan land sales in new estates, particularly in the identified ‘Ghost Suburb’ watch zones (Donnybrook, Ripley, Wilton). Demand evidence of the energisation schedule and Statement of Compliance timeline from the developer. Advise clients of the material risk of extended settlement delays and the associated financial distress of paying a mortgage on an uninhabitable property.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides empirical validation for the APN Future Development Pipeline Index™ (24400), confirming that infrastructure deficits create a significant APN Residual Land Value (RLV) Gap™ that renders structurally static tens of thousands of ‘zoned’ lots. It also validates the APN Agora™ (24140) framework, demonstrating that a failure in a single core utility can cause a material contraction in a location’s entire amenity score.

- Index Calibration: The APN Future Development Pipeline Index™ (24400) will be recalibrated to include ‘Transformer Lead Time’ as a primary economic friction filter. A new sub-metric, ‘Energisation Certainty,’ will be added to differentiate between theoretically viable and practically deliverable land supply.

- Data Capture: This analysis triggers a new data capture mandate for the APN Symbiotic Intelligence Network™ (24310). We will now actively track transformer lead times from manufacturers, utility connection backlogs (SoC requests), and reported instances of ‘Diesel Solution’ deployment as leading indicators for settlement risk within the APN Professional Sentiment Index™ (24300).

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.