Editor’s Note: This is Part 2 of the APN Insight series, “The Anatomy of a Crisis.” The series was prompted by a viral video from MacroBusiness economist Leith van Onselen, which crystallised the scale of the nation’s housing shortfall. In Part 1, we dissect the foundational numbers. In Part 2, we investigate the structural reasons why we can’t build faster. And in Part 3, we explore the controversial demand-side factors to ask: is it the whole story?

For a full breakdown of the data and sources, you can access the complete consolidated APN Research Report here.

From Blueprint to Backlog: Why Australia Can’t Build Homes Fast Enough

The number has become infamous in property circles: 177,000. That’s the approximate number of new homes Australia’s construction industry is managing to complete annually. In a nation crying out for far more to meet population growth and internal demand, this figure isn’t just a statistic; it’s the epicentre of our housing crisis. It represents a system at its limit, a pipeline choked by deep, structural blockages.

The narrative of a lazy or unambitious building sector is a dangerous oversimplification. The reality, as any developer or builder on the ground will attest, is far more complex. The 177,000-home ceiling is a symptom, not the disease. To understand why we can’t build faster, we must move past the headline number and dissect the interconnected constraints crippling the industry from the ground up.

The Labour Crisis: A Scarcity of Skills

The most fundamental input for any construction project is skilled labour, and right now, the tank is running on empty. Master Builders Australia estimates the industry needs half a million new workers by 2029 just to keep pace. We are critically low on electricians, plumbers, bricklayers, and project managers. This scarcity stems from a perfect storm: an ageing workforce, a vocational training system that has failed to produce enough new talent, and intense competition for labour from massive public infrastructure projects. The on-the-ground consequence is twofold. Firstly, project timelines blow out. Secondly, labour costs soar, contributing to higher home prices.

The Material Squeeze: Volatile Costs and Broken Chains

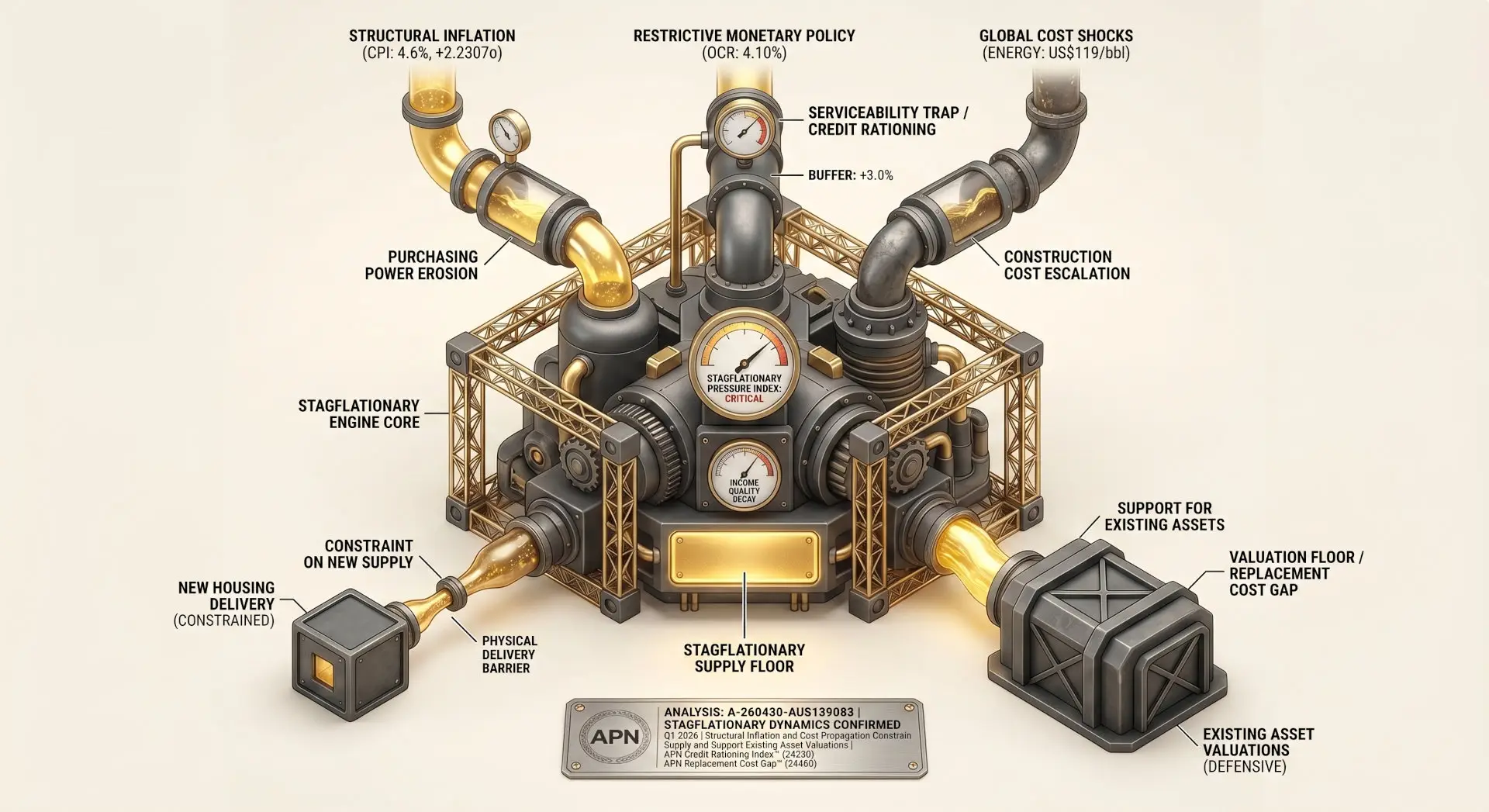

If you can find the workers, the next challenge is getting the materials. The post-COVID era left a legacy of fractured supply chains. Key materials like structural timber, steel, and concrete are subject to wild price fluctuations and unpredictable delivery schedules. The days of locking in a fixed-price contract with any degree of confidence are over. Builders are now forced to include significant cost escalation clauses, which in turn makes securing finance more difficult and spooks potential homebuyers. This isn’t just inflation; it’s a fundamental breakdown in the predictability that the construction industry relies upon.

The Red Tape Tangle: Planning and Regulatory Bottlenecks

Even with a full crew and a stockpile of materials, a project can be stopped dead for months, or even years, by Australia’s notoriously inefficient planning and approval systems. A recent Productivity Commission report laid bare the staggering cost of these delays. Research by the RBA has sought to quantify this “zoning effect,” estimating that as of 2016, planning restrictions had raised the price of an average detached house by 73% in Sydney and 69% in Melbourne above its marginal cost of supply. These delays aren’t just frustrating; they are incredibly expensive, and the costs are inevitably baked into the final price of the dwelling.

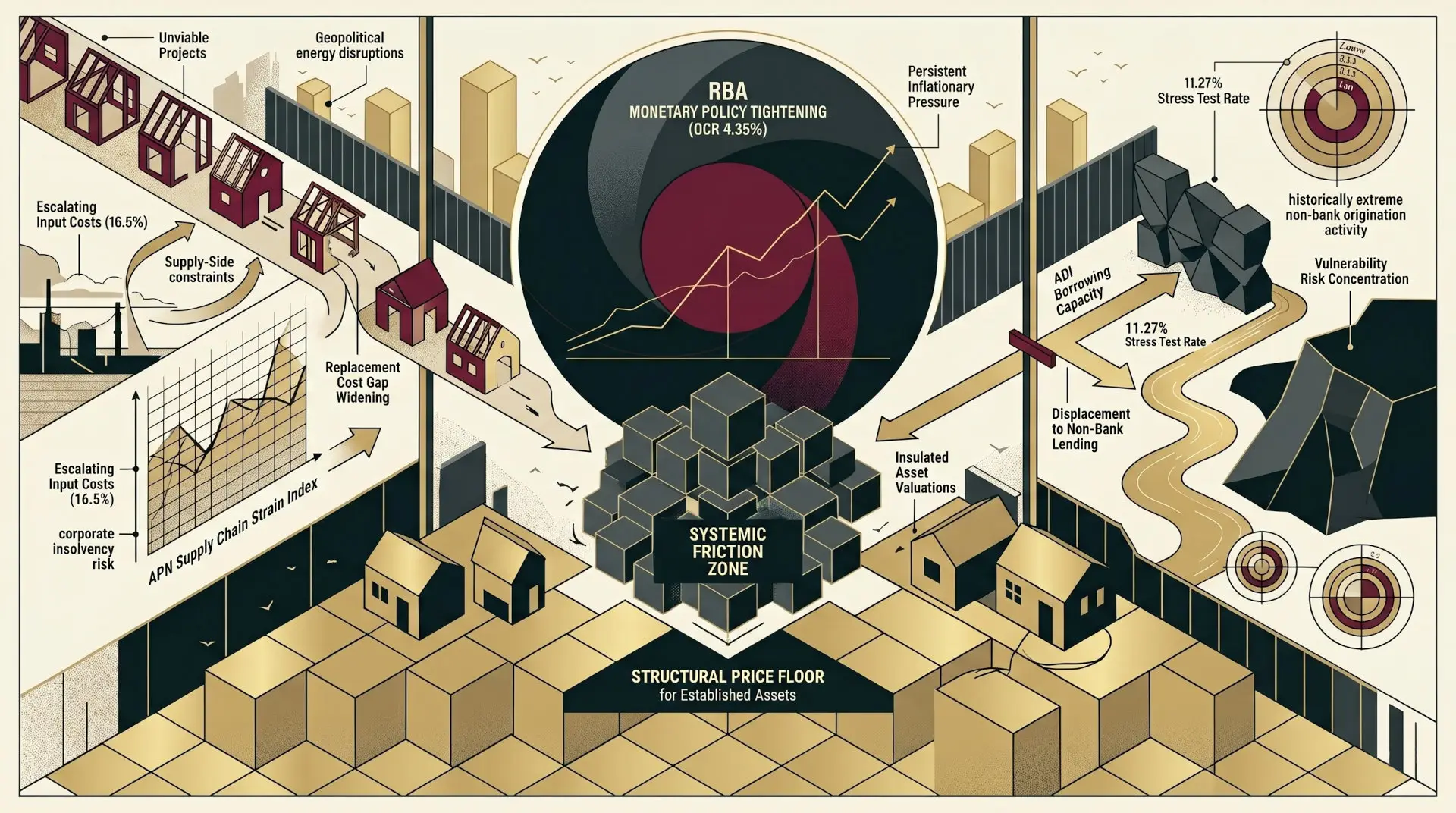

The Financial Headwinds: Securing Project Capital

The final hurdle is financing. The Reserve Bank’s aggressive campaign to curb inflation via interest rate hikes has had a chilling effect on construction finance. It’s a classic catch-22: the high cost of building makes projects riskier, and this perceived risk makes lenders more cautious. Developers are now facing a trifecta of challenges: higher borrowing costs, stricter lending criteria, and a wave of projects that are now simply financially unviable. As a result, a significant number of much-needed housing projects are being shelved, not for lack of demand, but for lack of capital.

The Policy Disconnect: A Chasm Between Targets and Reality

This brings us to the stark disconnect between political ambition and industrial reality. The Federal Government’s National Housing Accord targets the construction of 1.2 million new homes in five years, an average of 240,000 homes annually. It’s a laudable goal, but it is entirely detached from the industry’s capacity.

There is an overwhelming consensus among industry bodies that this target is unachievable.

- The Housing Industry Association (HIA) forecasts a shortfall of more than 250,000 dwellings.

- The Property Council of Australia projects a similar deficit, estimating a shortfall of 262,000 homes.

- Master Builders Australia provides an even more pessimistic outlook, warning that the shortfall could exceed 400,000 homes.

How can a sector struggling to produce 177,000 homes suddenly ramp up to 240,000? Without a concrete plan to address the core constraints of labour, materials, planning, and finance, such targets are not a strategy; they are a wish list. The blueprint for our housing future will remain permanently stuck in the backlog.

Disclaimer

The information contained in this article is for general informational purposes only and does not constitute financial, investment, or legal advice. The Australian Property Network (APN) is not a licensed financial advisor. The content is based on data from third-party sources and is provided without any warranty as to its accuracy, currency, or completeness. Property values can go down as well as up. Before making any property or investment decisions, you should conduct your own research and consider seeking independent professional advice tailored to your specific circumstances.