Demographic Expansion Continues to Outpace Residential Supply Delivery

APN ANALYSIS: A-260324-AUS138602

Executive Summary

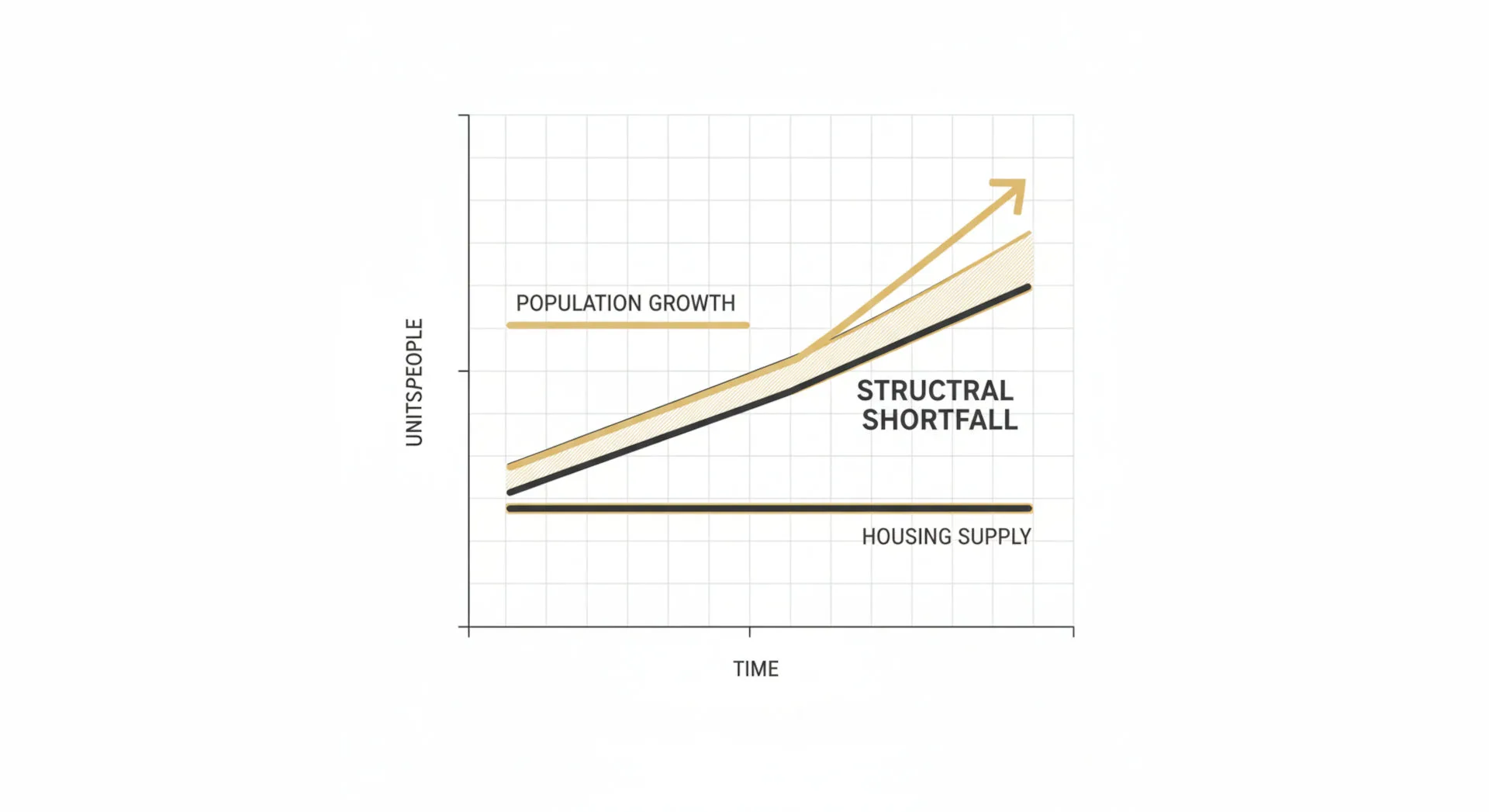

Empirical analysis of official data confirms that while the rate of net overseas migration has moderated from its recent peak, Australia’s absolute population expansion remains at historically elevated levels. For the year ending September 2025, the national population grew by 423,600 individuals, a volume that constitutes a greater than two standard deviation event against the pre-2020 baseline. This sustained demographic load is occurring concurrently with a material contraction in the physical delivery of new housing, with completions declining 1.2 per cent in the September 2025 quarter. This widening structural deficit between human capital intake and habitable dwelling output is the primary driver of sustained housing stress and systemic demographic displacement.

For property professionals, this analysis validates that the fundamental market imbalance is structural, not cyclical. The persistent shortfall in new supply provides a strong price floor for existing, well-located residential assets and ensures rental yields will face continued upward pressure. However, it also signals elevated execution risk for developers due to entrenched supply chain frictions and project viability constraints. For financiers, the data highlights accumulating serviceability risks within mortgage portfolios, necessitating a more granular assessment of household balance sheet resilience in an environment of sustained shelter cost inflation.

Background & Strategic Context

This analysis validates and calibrates APN’s core macro-thesis of Structural Supply Constraints. The research demonstrates that government housing targets and theoretical zoning changes are insufficient to overcome the entrenched logistical and financial frictions that govern the physical delivery of new dwellings. The data confirms that the mathematical reality of a +2σ demographic load converging with a constrained construction pipeline is the dominant force shaping the Australian property market, overriding policy intent and creating predictable points of systemic stress.

The Empirical Anchor (Population Growth & Distribution (21410)): The analysis is anchored in the official demographic data, which quantifies the precise volume of human capital being integrated into the domestic economy. The sustained high volume of population expansion, despite a statistical moderation in net overseas migration, establishes the baseline demand pressure that all other supply-side metrics must be measured against. The unequal geographic distribution of this intake further concentrates this demand into specific metropolitan corridors.

The Human Consequence (APN Acute Vulnerability Index™): This proprietary index is informed by the measurable outcomes of the supply-demand imbalance. The analysis tracks the transmission of macroeconomic pressure into localised housing stress, as evidenced by institutional data showing 1.26 million low-income households in financial distress and 44.5 per cent of all mortgage holders allocating over 30 per cent of their income to housing costs. This validates the index’s function as a measure of systemic demographic displacement.

The Delivery Bottleneck (APN Supply Chain Strain Index™): The failure of the construction sector to scale output is not a matter of intent but of capacity. This index tracks the underlying frictions, including a documented 18 per cent degradation in productivity, a structural deficit of 90,000 skilled workers, and a 47 per cent increase in base construction costs since 2020. These constraints form a structural barrier to converting development approvals into completed, habitable dwellings at the required velocity.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of official data from the Australian Bureau of Statistics (ABS), the Australian Institute of Health and Welfare (AIHW), and key industry bodies. The key facts are:

- Elevated Population Growth: Australia’s population expanded by 423,600 individuals in the year to 30 September 2025, an annualised growth rate of 1.6 per cent. Net overseas migration accounted for 311,000 of this total.

- Statistically Significant Anomaly: The 423,600 growth figure is a greater than two standard deviation (+2σ) event when benchmarked against the 2015-2019 pre-pandemic annual average of 371,828, confirming the intake volume is structurally abnormal.

- Contracting Supply Completions: Despite a quarterly rise in theoretical approvals and commencements, the number of dwellings achieving practical completion fell by 1.2 per cent in the September 2025 quarter to 44,242 units.

- Projected Structural Deficit: The construction sector is on track to deliver approximately 180,200 fewer homes than the 1.2 million target set by the National Housing Accord over its five-year term, based on current delivery friction.

- Widespread Housing Stress: An estimated 1.26 million low-income households are in housing stress. Across the entire market, the proportion of mortgage-holding households paying over 30 per cent of their income on housing costs has escalated from 24 per cent in 2021 to 44.5 per cent in 2025.

Critical Analysis & Balanced View

The analysis reveals a structural paradox in the current policy environment. While sovereign policymakers have achieved a statistical moderation in net overseas migration—a 14.9 per cent contraction from the post-pandemic peak—the resulting absolute intake of 423,600 people remains a +2σ event that the physical economy cannot absorb. This demonstrates that the nation’s historical baseline capacity for infrastructure and housing delivery is the primary limiting factor, not the marginal velocity of migration. The data suggests that even with ‘successful’ migration management, the structural housing deficit will continue to compound until demographic intake is calibrated to the measured, physical capacity of the construction sector, or until the sector’s productivity constraints are fundamentally resolved.

Furthermore, the data exposes a deepening bifurcation of the property market. The convergence of a +2σ demographic load and a constrained supply pipeline creates a Replacement Cost Moat and a Residual Land Value Gap, thereby establishing a high price floor for existing assets and rendering the construction of new, affordable housing commercially unviable for many developers. This process mathematically insulates outright asset owners from market pressures while concentrating the structural consequences of the adjustment among renters and leveraged mortgage holders. Unverified sentiment indicating a retreat into multi-generational living arrangements suggests a suppression of official household formation statistics, masking the true depth of the underlying demand and structural housing deficit.

Strategic Implications for Property Professionals

- For Investors: The persistent, structural undersupply of new dwellings provides a strong fundamental underpinning for capital values of existing, well-located residential assets. Expect continued low vacancy rates and sustained upward pressure on rental yields as demand consistently outpaces delivery.

- For Developers: The analysis confirms that securing a development approval is not a guarantee of project success. Elevated execution risk persists due to labour shortages, cost inflation, and financing constraints. Viability hinges on meticulous cost management and securing sites where the Residual Land Value equation remains favourable, potentially outside the most contested metropolitan cores.

- For Lenders & Financiers: The finding that 44.5 per cent of mortgage holders are in a state of housing stress signals accumulating serviceability risk across loan portfolios. This warrants a more conservative assessment of new lending, particularly to cohorts with limited capital buffers, and a proactive approach to managing stress within existing books.

- For Property Managers: The market dynamics guarantee a high-friction rental environment. Tenant demand will remain elevated, but the capacity of tenants to absorb further rent increases is finite. The need for tenants to deploy advanced capital to secure leases indicates a market where robust vetting and managing tenant financial stability are critical operational priorities.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Acute Vulnerability Index™ (24126) by empirically linking a +2σ demographic load directly to deteriorating institutional metrics of housing stress and observable demographic displacement.

- Index Calibration: The APN Supply Chain Strain Index™ (24430) is calibrated to reflect the confirmed 18 per cent productivity degradation and the 90,000-worker structural deficit, increasing its weighting in the overall development feasibility model.

- Data Capture: This triggers a new data capture mandate for the APN Residual Land Value (RLV) Gap™ (24410) to monitor the divergence between residential building approval values and the value of actual work done, quantifying the rate of project attrition between approval and commencement.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.