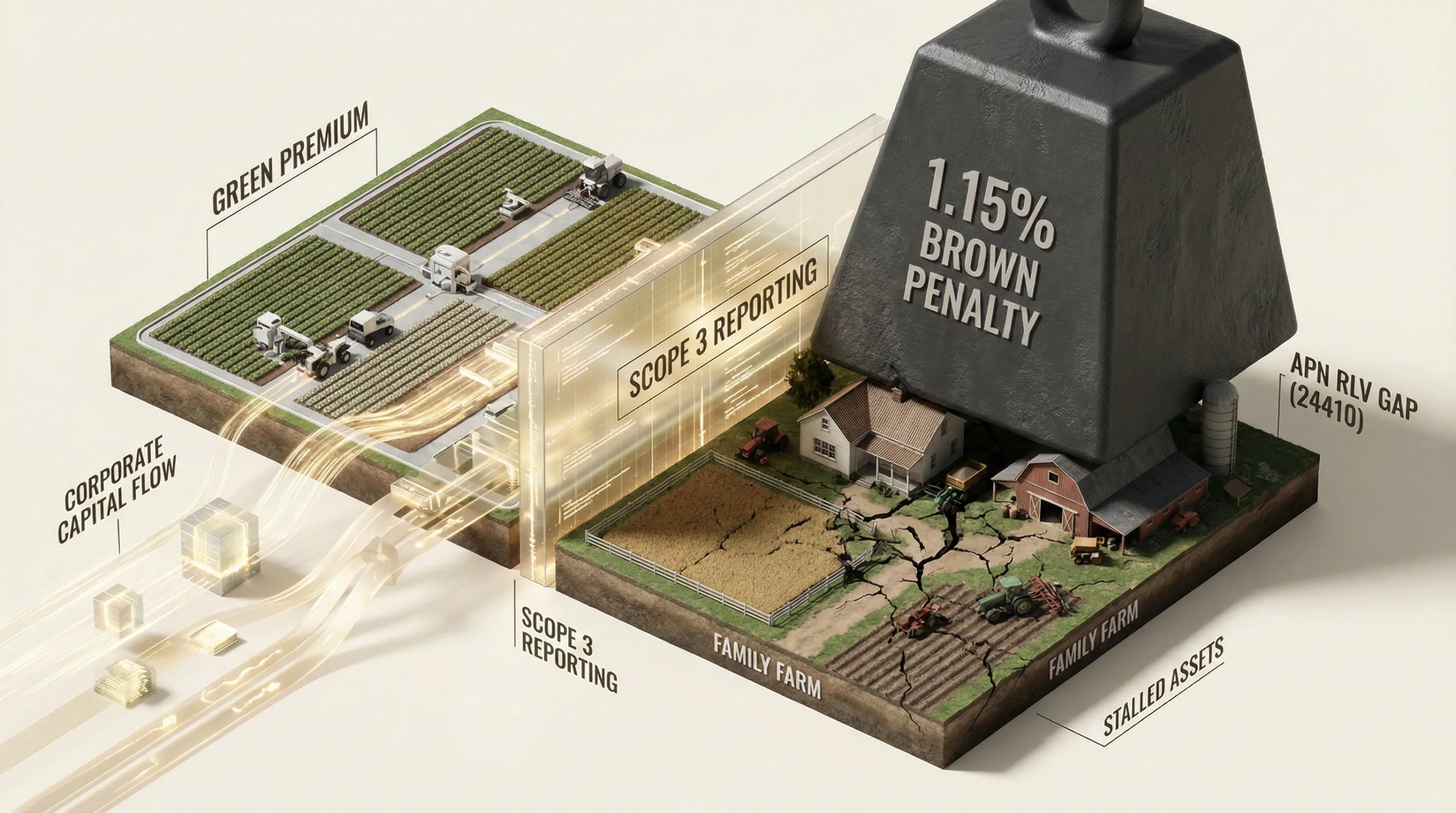

Validated: ‘Data-Driven Asset Reallocation’ Confirmed as Scope 3 Reporting Creates a 1.15% ‘Brown Penalty’ in Agribusiness Lending

APN ANALYSIS: A-251127-AUS131227

Executive Summary

A definitive stress-test of the Australian agribusiness sector confirms that mandatory Scope 3 emissions reporting has created a bifurcated credit market, structurally disadvantaging family farms. The core mechanism is a ‘Sustainability Risk Premium’—effectively a ‘Brown Penalty’—imposing a cost-of-capital differential of between 0.65% and 1.15% on operators unable to meet the new, data-intensive compliance demands of their lenders. This is not an anomalous market outcome; it is a direct consequence of Tier 1 banks transferring their own regulatory compliance obligations for reporting ‘financed emissions’ to their borrowers.

For property professionals, this represents a fundamental recalibration of asset valuation in the rural sector. The emergence of a ‘Brown Discount’ on data-poor land and a corresponding ‘Green Premium’ on compliant assets is creating a two-speed market defined by data-readiness. Understanding an asset’s capacity to generate audit-grade environmental data is now as critical as assessing soil quality or water rights, directly impacting valuation methodology, transaction viability, and strategic client advisory.

Background & Strategic Context

This event validates and calibrates APN’s core macro-theses, specifically the ‘Wealth Funnel’ and the APN Sovereign Policy Composite Index™ (SPCI, 24800). The regulatory shift (APN Sovereign Policy Composite Index™ (SPCI, 24800)) in the form of the Australian Sustainability Reporting Standards (ASRS) has created a market mechanism that structurally channels assets from one class of owner (data-poor family farms) to another (data-rich corporate aggregators), illustrating the Wealth Funnel in operation.

The Regulatory Catalyst (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The domestication of ISSB standards into Australian law is a state-level intervention that has redefined ‘creditworthiness’ to include ‘climate data availability’. Banks, as regulated entities, are now compelled to enforce these standards on their loan books, making them de facto regulators of the agricultural sector and initiating the entire asset reallocation mechanism.

Quantifying the Value Shift (APN Climate-Risk Asset Devaluation Index™): The emergence of the 0.65%-1.15% ‘Sustainability Risk Premium’ is the first hard quantification of the APN Regional Brown Discount™ (24520). It demonstrates that climate transition risk is no longer a theoretical ESG concept but a direct, measurable financial penalty impacting asset viability and market valuation.

The Social Capital Erosion (APN Bedrock™): The accelerated consolidation of family farms by corporate entities represents a direct risk to the social cohesion measured by the APN Bedrock™ (24110) index. The diminished presence of family-run operations weakens local institutions, reduces resident stability, and affects the social fabric of regional communities, posing a long-term risk to regional resilience and value.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing, synthesising analysis of banking covenants, land transaction data, and regulatory filings from late 2025. The key facts are:

- The ‘Sustainability Risk Premium’: Lenders have established a quantifiable cost-of-capital differential based on ESG data. This ranges from a 0.65% discount on CEFC-backed green loans to a 1.15% incentive from NAB for verifiable emissions reduction activities.

- The ‘Brown Penalty’ Rate: Family farms unable to provide the required data are pushed onto standard variable rates, such as NAB’s ‘Farmer’s Choice Variable Rate’ at 8.97%, while compliant corporates can access rates as low as 6.5%. This creates an ‘asset reallocation differential’ of up to 2.47%.

- The Regulatory Driver: Mandatory Scope 3 emissions reporting under the Australian Sustainability Reporting Standards (ASRS) forces Tier 1 banks to calculate the ‘financed emissions’ of their loan books, effectively outsourcing the data compliance burden to their borrowers.

- The ‘Brown Discount’ on Collateral: Property valuers are now incorporating a ‘brown discount’ for land that lacks environmental baselining, reducing the valuation of the primary asset of data-poor farms and further restricting their access to capital.

- Accelerated Corporate Consolidation: Transaction data from 2025 shows a ‘flight to scale,’ with corporate aggregators like PSP Investments and Hewitt acquiring vast land portfolios in consolidation hotspots like the Queensland grazing belts and the NSW Wheatbelt, leveraging their access to more competitive green finance.

- Insufficient Government Support: Federal ‘Transition Support’ programs, such as the $17.5 million Carbon Farming Outreach Program, are fiscally immaterial, representing just 0.017% of the total rural debt pool and insufficient to cover the capital expenditure required for on-farm data infrastructure.

Critical Analysis & Balanced View

The ‘Green Credit Squeeze’ is not a conspiratorial action but the logical, emergent outcome of misaligned incentives. For banks, pricing data-opacity as credit risk is a rational response to their own regulatory obligations under ASRS. They are not explicitly identifying family farms as targets; they are de-risking their balance sheets. The asset reallocation is a second-order effect of a top-down regulatory framework that did not adequately account for the substantial disparity in data-readiness across the agricultural sector.

The central paradox is that the policy intended to promote environmental sustainability is materially affecting the social sustainability of rural communities. By favouring capital-intensive, data-rich corporate models, the framework inadvertently penalises the smaller, often more locally-invested, family operations that form the bedrock of regional economies. This creates a future where Australia’s agricultural landscape may be ‘greener’ on paper but structurally depopulated.

The unquantified risk for the corporate aggregators is reputational and regulatory repercussions. As the ‘Wealth Funnel’ effect becomes more pronounced, the political narrative could shift, leading to inquiries, levies on foreign ownership, or changes to the ASRS framework. The opportunity lies for second-tier lenders, ag-tech firms, and advisory services that can create a ‘compliance-as-a-service’ model, offering scalable, low-cost data solutions to help family farms bridge the data gap and access more competitive financing.

Strategic Implications for Property Professionals

- For Valuers & Rural Agents: Your valuation methodology must now include a ‘Data-Readiness’ assessment. An asset’s ability to generate ISSB-compliant emissions data is a direct driver of its value and liquidity. Develop a checklist to score assets on their data infrastructure (e.g., precision ag systems, digital mapping, carbon baselining) to justify the application of a Green Premium or Brown Discount.

- For Agribusiness Finance Brokers: The key value proposition is no longer just sourcing the lowest rate, but navigating the data compliance maze. Specialise in structuring ‘transition finance’ packages that bundle the cost of data infrastructure CAPEX into the loan facility, demonstrating a clear ROI to the lender through the unlocked interest rate discount.

- For Institutional Investors & Fund Managers: The arbitrage opportunity is clear, but the ESG risk is evolving. While acquiring ‘brown’ assets and converting them to ‘green’ offers significant uplift, portfolio strategy must now include a political risk buffer. Monitor government and public sentiment (APN Social Capital Index™) towards corporate farm ownership to anticipate potential regulatory headwinds.

- For Buyers’ Agents & Family Office Advisors: When advising on agricultural acquisitions, the due diligence process must extend beyond soil and water to a full ‘digital and compliance audit’. Prioritise assets that either have existing data systems or a clear, cost-effective pathway to compliance. For clients looking to exit, creating a ‘data prospectus’ that pre-emptively baselines the farm’s emissions profile can significantly increase the sale price and attract a wider pool of buyers.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides definitive validation for the APN Climate-Risk Asset Devaluation Index™ (24500), confirming that climate transition risk is being explicitly priced into credit markets.

- Index Calibration: The APN Regional Brown Discount™ (24520) is now calibrated with a baseline financial penalty of 0.65% to 1.15% on the cost of capital for data-poor agricultural assets in key consolidation zones like the Queensland grazing belts and NSW Wheatbelt.

- Index Calibration: The APN Bedrock™ (24110) index for these regions will be adjusted downwards to reflect the negative impact of accelerated corporate consolidation on social cohesion and local economic diversity.

- Data Capture: This triggers a new data capture mandate for the APN Symbiotic Intelligence Network™ (24310) to track the specific ‘compliance-as-a-service’ solutions emerging in the ag-tech market, as these will become leading indicators of market adaptation.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.