The Financial Quantification of Climate: Deconstructing the New CRFD Valuation Mandate

APN ANALYSIS: A-251020-AUS04

Executive Summary

The Climate-Related Financial Disclosure (CRFD) regime is now in effect, compelling Australia’s largest developers, funds, and asset managers (Group 1 entities) to enter their first financial year of mandatory climate reporting. This structural change legally requires them to quantify and disclose the financial impacts of climate change, including both physical and transition risks, in their standard financial reports.

This legislation moves climate risk from a hypothetical, public-relations issue to a mandatory, auditable financial metric. The strategic implication is that this is the core regulatory trigger for the APN Climate-Risk Asset Devaluation Index™. The law forces companies to publicly disclose their resilience to specific scenarios (a 1.5°C and a greater than 2°C pathway), providing the exact, legally mandated data APN requires to model and calculate the “Financial Climate Sensitivity” of Australian property assets.

Background & Strategic Context

This new law is a profound state-level intervention, and its strategic impact is best understood through our core intelligence frameworks.

A State-Mandated Valuation Standard (Project Overlord): This is a textbook Project Overlord event. The state is intervening directly in capital markets to create and enforce a new valuation standard. By compelling disclosure under the Corporations Act, the government is forcing climate risk onto the balance sheet. This act of regulatory power compels boards and financial markets to quantify, price, and act on a risk that many had previously been able to ignore.

The Regulatory Trigger for a New APN Index (APN Climate-Risk Asset Devaluation Index™): This legislation is the specific regulatory trigger that operationalises our index. The law provides the exact risk bandwidth for our models by mandating scenario analysis for two distinct futures: a 1.5°C pathway (testing maximum transition risk) and a pathway “well exceeding 2°C” (testing maximum physical risk). We can now use this publicly mandated, high-integrity data to calculate and offer our “Financial Climate Sensitivity” metric.

Deconstruction of the Source Event

The internal research confirms the following verifiable details of the new CRFD regime:

- Core Event: The assent of the Treasury Laws Amendment Bill, which mandates Climate-Related Financial Disclosure (CRFD).

- Affected Entities: Group 1 entities, defined as those with consolidated assets of $1 Billion or more or consolidated revenue of $500 Million or more.

- Commencement Date: The mandate applies to financial years commencing on or after January 1, 2025.

- Core Requirement: In-scope entities must prepare an annual “sustainability report” that complies with the new Australian Sustainability Reporting Standards (ASRS), specifically AASB S2: Climate-related Disclosures.

- Mandatory Scenario Analysis: The Corporations Act (via new Subsection 296D(2B)) legally mandates scenario analysis for at least two specific pathways:

- A 1.5C pathway (high transition risk, low physical risk).

- A pathway “well exceeding 2°C” (e.g., 2.5°C or higher, representing high physical risk).

- Financial Impact: AASB S2 requires entities to quantify the financial effects of these risks on their financial position (balance sheet) and performance (P&L), including explicit impacts on asset valuations and impairments.

- Modified Liability: A three-year “safe harbour” (modified liability) is in place for forward-looking statements (like scenario analysis) to protect companies from private litigation, but ASIC retains full enforcement power against misleading conduct.

Critical Analysis & Balanced View

The source data confirms a new, complex reporting standard. The critical insights lie in its financial, not just environmental, implications.

The “Real” Story: This Isn’t an ESG Report; It’s an Accounting Mandate. The most critical insight is that this is not an “environmental, social, and governance (ESG)” reporting exercise. By anchoring the law in the Corporations Act and the Australian Accounting Standards Board (AASB), the state has transformed climate risk into a core financial accounting problem. Asset valuations on the balance sheet must now be justified against the assumptions in the mandated climate scenarios.

Strategic Paradox: The “Safe Harbour” Confirms the Permanent Liability. The 3-year “safe harbour” for scenario analysis is a strategic paradox. While it offers temporary protection from private lawsuits, its very existence confirms the massive, unprecedented legal liability these disclosures will create after mid-2027. It is a temporary shield to allow companies to build the models for a new class of permanent, litigable financial liability.

Challenged Assumption: “Climate Risk is a Future Problem.” This legislation definitively ends that assumption. From 2025, Group 1 entities must quantify the financial impact of climate change on their current balance sheets. The mandated greater than 2°C scenario forces them to put a dollar value on the physical risks (floods, fires, extreme weather) to their assets, making devaluation a present-tense financial calculation, not a future-tense hypothetical.

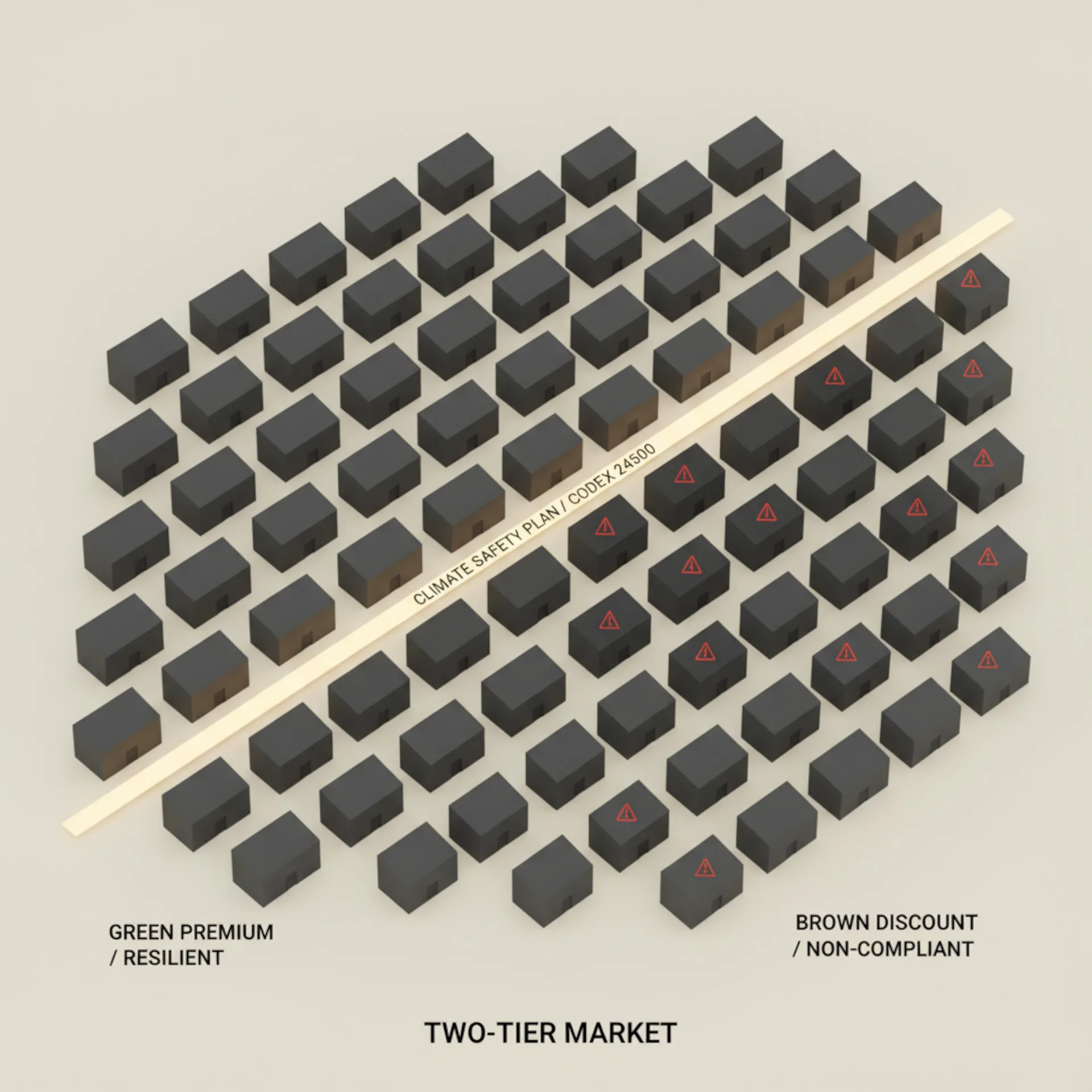

Balanced View: This legislation is the most significant change to corporate reporting in a generation. It moves climate risk from a qualitative, PR-managed issue to a mandatory, auditable, and quantifiable financial metric. By forcing the disclosure of scenario-based asset valuations, the state has provided the exact, high-integrity data needed for the APN Climate-Risk Asset Devaluation Index™ to calculate and expose the “devaluation gap” across the entire Australian property sector.

Strategic Implications for Property Professionals

- For Developers & Fund Managers (Group 1): You are now legally required to quantify your assets’ vulnerability. Your cost of capital and insurance premiums will be directly tied to your disclosed performance under the two mandated scenarios (1.5°C and greater than 2°C). “Greenwashing” has moved from a reputational risk to a direct directors’ duties liability.

- For Valuers & Lenders: The valuation profession must immediately develop a new standard for integrating CRFD data. A valuation that ignores an asset’s vulnerability under the mandated greater than 2°C scenario is now arguably incomplete and legally indefensible. Lenders will begin pricing risk and allocating capital based on these new public disclosures.

- For Investors & REITs: This is a new tool for arbitrage. For the first time, you can directly compare the “Financial Climate Sensitivity” of different asset portfolios. The APN Climate-Risk Asset Devaluation Index™ will use this data to identify which funds are most exposed to physical risk and which are most exposed to transition risk.

- For Agents & Brokers (Non-Group 1): The standards set for Group 1 will “trickle down” and become the new best practice. Expect finance and insurance partners to begin demanding climate-risk data on smaller assets as this becomes the new standard for professional due diligence.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

Property values and market conditions can go down as well as up.

Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.