Climate Safety Plan Mandates Two-Tier Property Market via Resilience-Linked Insurance Discount

APN ANALYSIS: A-251110-AUS002

Executive Summary

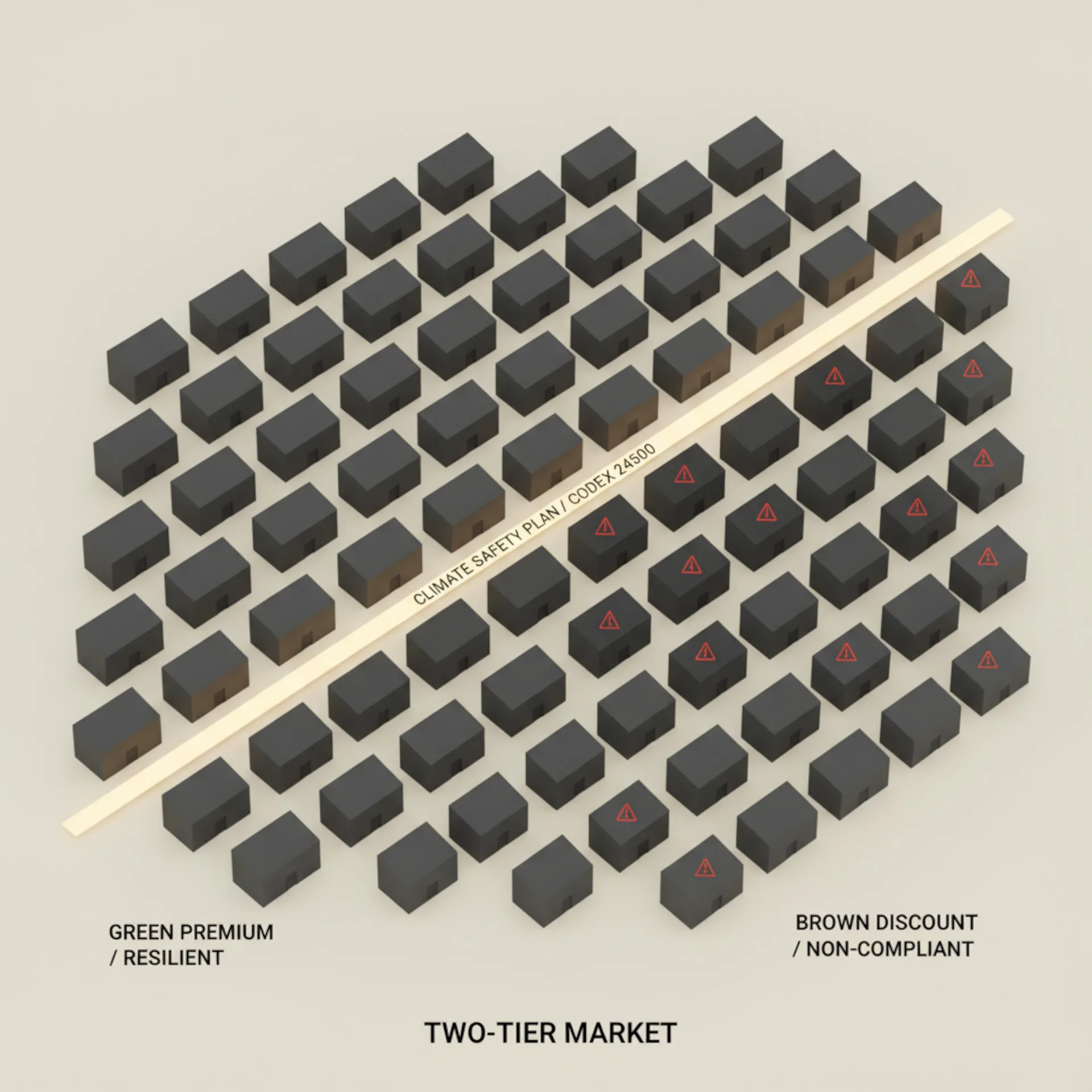

The “Climate Safety Plan,” launched by a systemic political bloc of 80+ organisations, including the ACTU and primary social services, provides the explicit blueprint for a policy-driven, two-tier property market. The plan’s central demand, to “mandate discounted insurance” for resilient homes, is the financial mechanism that operationalises the APN Climate-Risk Asset Devaluation Index™ (24500), creating a quantifiable “Green Premium” while forcing a “Brown Discount” onto non-adapted assets.

This plan shifts climate risk from a long-term, latent threat to an immediate financial and legal liability. For property professionals, it signals the arrival of forced capital expenditure to meet new minimum rental standards and provides a direct, non-market input for asset valuation. Non-compliant properties now face a binary outcome: a total loss of rental income or exposure to “unaffordable,” non-discounted market insurance.

Background & Strategic Context

This research provides the primary legal and financial mechanisms required to fully operationalise the APN Climate-Risk Asset Devaluation Index™ (24500). The plan moves the concept of a climate-driven two-tier market from a theoretical, market-led repricing event to an imminent, policy-driven mandate.

- APN Climate-Risk Asset Devaluation Index™ (24500): This is the core framework. APN Research provides the two key triggers for quantifying devaluation.

- The Financial Mechanism (Green Premium): The “mandated discounted insurance” creates a specific, quantifiable value for resilience (the value of the discount).

- The Legal Trigger (Brown Discount): The demand for “minimum standards for rental properties” provides the legal lever to crystallise devaluation, rendering non-compliant assets unable to legally generate income.

- Political Reframing (Systemic Risk): The plan’s strategic brilliance lies in its coalition. By bringing in labour (ACTU), health (ANMF), and social services (Uniting), it successfully reframes climate adaptation from an “environmental” issue to a mandatory “economic and health & safety” issue, dramatically increasing its political velocity and probability of adoption.

- Hyper-Local Risk (Codex 24500): The plan’s call for a new “LGA Adaptation Fund” confirms the 24500 thesis that climate risk devaluation will be hyper-local. Asset risk will be fragmented and determined on a council-by-council basis, depending on how local governments implement the compliance and funding mandates.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing. The key facts are:

- The “Climate Safety Plan” (CSP) was launched on November 8, 2025, in direct response to the government’s National Climate Risk Assessment (NCRA).

- The coalition consists of “80+ organisations,” including the peak union body (ACTU), Australia’s largest union (ANMF), and major social service providers (Uniting).

- Financial Mandate: The plan’s core demand is to “mandate discounted insurance in exchange” for government-funded resilience upgrades.

- Legal Mandate: The plan demands “urgent updates to the National Construction Code” and the implementation of “minimum standards for rental properties.”

- Funding Mechanism: It calls for “$4 billion over 5 years” to be allocated via the Disaster Ready Fund and a new LGA Adaptation Fund.

- Industry Response: The Insurance, Property, and Banking sectors have maintained a “structured silence” post-launch, signalling high-level concern.

Critical Analysis & Balanced View

The “real story” is the political sophistication of this plan, which has created a pincer movement. The government’s own National Climate Risk Assessment (NCRA) identified a systemic problem but offered no solution, creating a political vacuum. The 80+ organisation coalition has now filled that vacuum with the only comprehensive, politically-backed plan on the table. The “structured silence” from the finance and property sectors confirms this plan is being treated as a serious policy threat, not a fringe ambit claim.

The plan’s true impact comes from its two-pronged financial and legal mechanism. The “mandated discounted insurance” bypasses slow, market-led repricing and imposes a “Green Premium” by policy fiat. This simultaneously isolates non-resilient assets, forcing them to bear the full, “unaffordable” market risk, thereby creating a “Brown Discount.” The demand for minimum rental standards is the legal trigger that crystallises this latent risk into an explicit financial liability. An investor in a non-compliant rental asset will no longer face a risk of devaluation; they will face a certainty of zero rental income or forced, non-negotiable capital expenditure. This makes the devaluation immediate and quantifiable.

On the surface, this is a progressive policy proposal. However, the analysis reveals it as a direct blueprint for operationalising the APN Climate-Risk Asset Devaluation Index™ (24500). It provides the exact triggers, policy-driven insurance pricing and legal rental compliance that will bifurcate the property market. The risk is now hyper-local, hinging on the compliance and funding regimes implemented at the LGA level.

Strategic Implications for Property Professionals

- For Investors (Rental): You must immediately factor in a significant, forced CapEx liability to meet looming minimum rental standards. Non-compliance will shift from a minor issue to a primary driver of asset devaluation, resulting in a 100% loss of rental income.

- For Valuers: The “Brown Discount” is no longer theoretical. Valuations for non-resilient assets, particularly in at-risk LGAs, must be qualified by this new, policy-driven compliance risk. The value of the mandated insurance discount will provide the first quantifiable benchmark for the “Green Premium.”

- For Developers: Prepare for urgent updates to the National Construction Code. Feasibility models must be recalibrated to account for higher mandatory resilience standards, which will impact project costs and the APN Future Development Pipeline Index™ (24400) RLV Gap.

- For Lenders & Insurers: The “structured silence” is untenable. The sector must prepare a unified counteroffer or compromise. The baseline assumption must now be that a non-market, policy-based intervention in risk pricing is imminent.

- For APN Index Management: The APN Climate-Risk Asset Devaluation Index™ (24500) must be immediately updated to model: (1) The value of mandated insurance discounts, (2) LGA-level policy implementation velocity, and (3) The financial impact of rental non-compliance.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty regarding their accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.