Media Amplification Asymmetry Skews Perception of 2026-27 Federal Budget Housing Measures

APN ANALYSIS: A-260514-AUS139254

This analysis is produced by Australian Property Network, an independent property intelligence platform now in its tenth year of development, with no commercial affiliations, no advertiser relationships, and no industry body funding. Findings are derived from seven independent research streams across twelve outlet categories, anchored to the AUS-151-1 factual baseline of twenty-five confirmed budget measures and assessed against certified APN Codex node telemetry. The full research brief for this analysis is published at APN Research.

Executive Summary

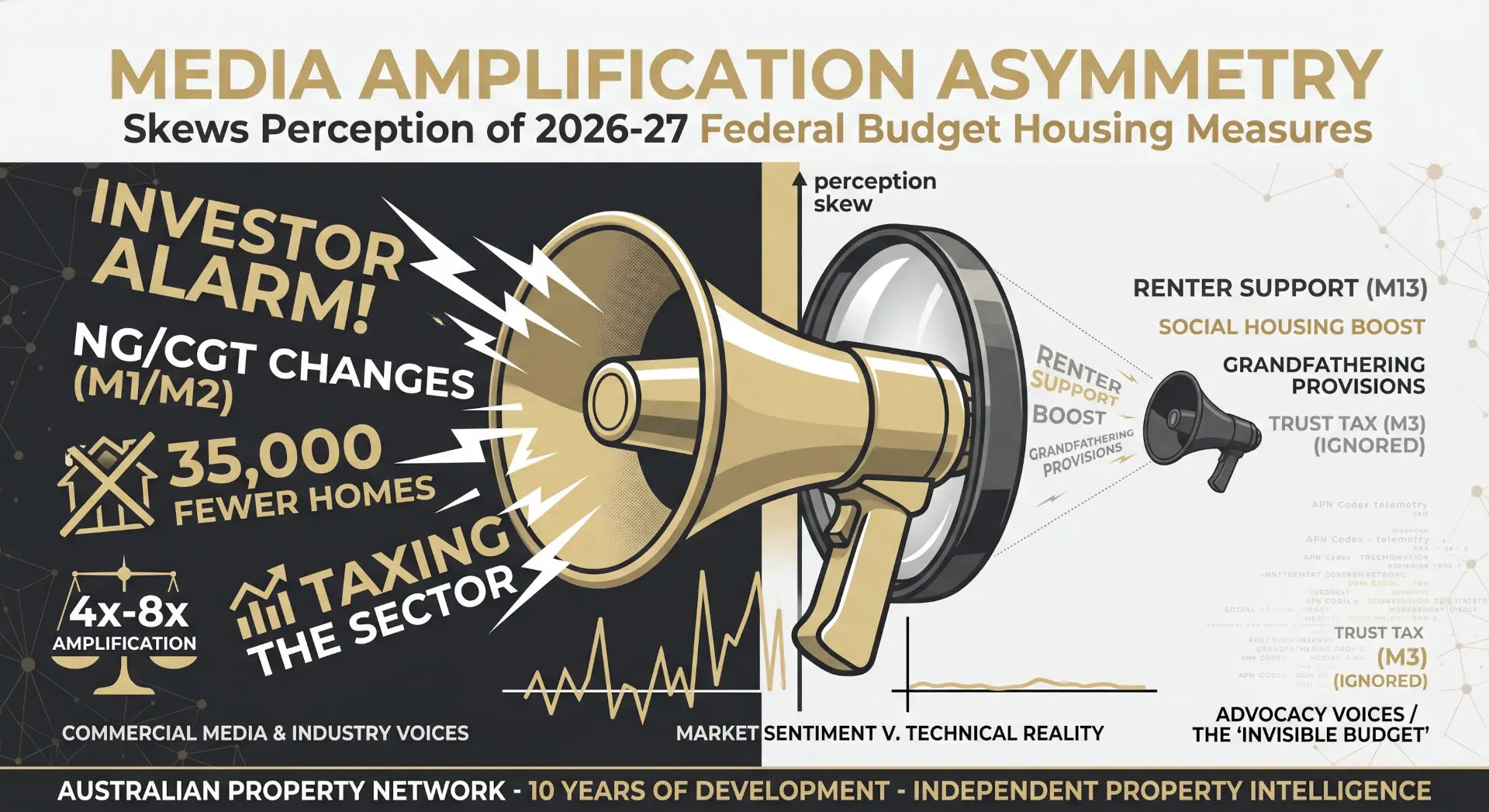

The Australian media’s coverage of the 2026–27 Federal Budget housing measures was characterised by a structural imbalance that amplified investor-centric narratives while systematically omitting key policy details. APN analysis of twelve outlet categories confirms that commercial and industry voices received approximately four times the media amplification of advocacy voices. This resulted in a narrow focus on changes to negative gearing (M1) and capital gains tax (M2), often framed with a high degree of political characterisation and without adequate explanation of critical grandfathering provisions. This selective coverage has created a material perception gap between the policy’s technical reality and the public narrative, constituting a material negative sentiment input that is misaligned with the measures’ phased implementation timeline, which does not commence until July 2027.

For property professionals, this media-driven distortion presents both a risk and an opportunity. The primary risk is that clients may make premature portfolio decisions based on a sentiment-driven and incomplete understanding of the reforms. The opportunity lies in providing clinical, evidence-based advice. By focusing on the actual policy mechanics, the 14-month implementation window, and the material but under-reported measures constituting the “Invisible Budget”—notably the new tax on discretionary trusts (M3) and major changes to tenancy law (M13)—informed professionals can guide client strategy, mitigate portfolio risk, and demonstrate significant advisory value.

Background & Strategic Context

This analysis validates and calibrates the APN Sovereign Policy Composite Index™ (SPCI) (24800), which measures policy risk arising from competing or contradictory sovereign mandates. The budget coverage demonstrates how a highly concentrated media ecosystem can function as a structural force operating outside the policy’s legislative intent, creating a narrative environment that diverges from a government’s stated policy direction. The resulting information asymmetry generates material market friction and sentiment risk, which this analysis seeks to quantify.

Inaugural Media Sentiment Baseline (Media & Narrative Sentiment Index (21680)): This analysis constitutes the foundational empirical instrument for this newly activated node. It establishes a replicable baseline for measuring media bias by documenting how commercial ownership structures, historical conflict frames (the 2019 election), and source amplification asymmetry converged to shape the public narrative of a major policy event.

Structural Taxation Realignment (Taxation & Revenue Policy (21310)): The budget measures represent the most significant structural realignment of residential property taxation since 1999. The combined effect of restricting negative gearing to new builds (M1), replacing the CGT discount with an inflation-indexed model (M2), and imposing a minimum tax on discretionary trusts (M3) alters the after-tax viability calculus for retail investors, with the media’s disproportionate focus on M1/M2 obscuring the material financial impact of M3.

Media-Driven Sentiment Input (Market Psychology & Herd Behaviour (21620)): The dominant alarm register in commercial media, combined with the suppression of the grandfathering nuance and the decontextualised use of the “35,000 fewer homes” figure, constitutes a material negative sentiment input. This is likely to influence retail-investor disposal activity and first-home-buyer behaviour in the 14-month window before the policy’s July 2027 implementation, potentially diverging from Treasury’s behavioural assumptions.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Australian media coverage of the 2026–27 Federal Budget’s housing measures, as documented in research brief AUS-151. The key facts are:

Amplification Asymmetry: Across the aggregate media landscape, commercial and industry voices (REIA, HIA, Property Council) achieved approximately four times the media amplification of renter and welfare advocacy voices (ACOSS, National Shelter). This ratio increased to 8:1 in News Corp print outlets.

Systematic Omission of Renter-Focused Policy: Measures representing a multi-billion-dollar commitment to renters, including the Commonwealth Rent Assistance boost (M12) and the ‘A Better Deal for Renters’ framework (M13), were consistently absent from commercial property and specialist financial media coverage.

The ‘Invisible’ Revenue Measure: Measure 3, a 30% minimum tax on discretionary trusts and the largest single revenue-generating mechanism in the housing package (+$4.47bn), was clinically covered by the AFR but largely omitted from specialist property media, leaving the affected retail-investor demographic largely unaware of a material future tax liability.

Decontextualised Data Deployment: The “35,000 fewer homes” figure, derived from government Treasury modelling, was reproduced across commercial media as a dominant counter-narrative, frequently without the offsetting context of the M1 new-build carve-out or other supply-side measures.

Structural Conflict of Interest: A 100% conflict-of-interest disclosure failure rate was documented across the assessed specialist property media, where outlets with revenue models dependent on property transaction volumes reported on measures directly affecting that activity.

Critical Analysis & Balanced View

The analysis reveals a pattern of systematic omission that extends beyond individual measures to entire policy domains, creating what can be termed “the Invisible Budget”. Measures primarily benefiting non-transacting market participants—renters (M12, M13), social housing tenants (M5, M6), and lower-income graduates (M20)—were rendered invisible by a commercial media ecosystem that structurally defines “the housing market” as the private, transactional property market. This creates a material information asymmetry with material consequences: a pre-legislative risk window for tenants regarding M13, and a latent tax liability for unaware investors using trust structures under M3.

Furthermore, the fiscal conservatism anomaly within News Corp coverage represents a material structural finding. The absence of positive fiscal framing for a budget that delivered a +$6.1bn net positive to the underlying cash balance is a marked deviation from the organisation’s conventional editorial posture. The dominance of negative fiscal (Frame 1) and class-based (Frame 3) characterisations suggests that for this policy set, the historical conflict frame from the 2019 election and underlying commercial property interests were more powerful drivers of editorial direction than a core commitment to fiscal discipline. This indicates the media narrative was an output shaped by identifiable commercial and ideological structural conditions rather than a neutral reflection of policy.

Strategic Implications for Property Professionals

For Financial Planners & Accountants: Proactively audit client portfolios for discretionary trust structures. The widespread media omission of Measure 3 (Minimum Tax on Discretionary Trusts) creates a material advisory window to guide clients on restructuring ahead of the 1 July 2028 implementation and its three-year CGT rollover relief provision.

For Buyer’s Agents & Mortgage Brokers: Advise clients against sentiment-driven decisions based on the media alarm surrounding M1/M2. Emphasise that the grandfathering provisions protect existing investments and the measures do not commence until July 2027. Conversely, the under-reported impact of Measure 20 (HELP Debt Settings) on borrowing capacity presents a tangible opportunity for qualifying first home buyers.

For Property Managers & Landlords: The universal media omission of Measure 13 (A Better Deal for Renters) creates a pre-legislative information vacuum. Professionals should prepare for the crystallisation of new tenancy frameworks at the state level and advise landlord clients on future compliance to mitigate regulatory risk, rather than reacting to potential friction.

For Developers & Institutional Investors: The media’s focus on M1/M2 has displaced coverage of supply-side incentives, including the M1 new-build carve-out and Build-to-Rent exemptions. This creates a positioning opportunity for capital that can clearly articulate its alignment with the new policy direction.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

Validation: This analysis validates the APN Sovereign Policy Composite Index™ (SPCI) (24800) by providing an empirical case study of how media narrative can function as a structural force operating in divergence from legislative intent, creating a policy environment that generates material market friction.

Index Calibration: The Media & Narrative Sentiment Index (21680) is calibrated with its inaugural baseline reading from this analysis. The ten-vector bias matrix and seven-frame political characterisation taxonomy are now established as core metrics for future assessments.

Data Capture: This triggers a new data capture mandate for the APN Risk & Compliance Index™ (24200) to track the information asymmetry gap created by the omission of Measure 13 (A Better Deal for Renters) and Measure 3 (Minimum Tax on Discretionary Trusts), quantifying the pre-legislative risk for tenants and the latent liability risk for unaware investors.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.