Research Preface

Australian Property Network operates as an independent property intelligence platform, now in its tenth year of development. The platform is self-funded and editorially independent, with no commercial affiliations, advertiser relationships, or political affiliations of any kind. This research brief does not constitute financial advice. APN’s analytical work is structured to provide informed observers with a clinical, evidence-anchored account of the property market environment; it is not a recommendation to buy, sell, or hold any asset, nor a prediction of market direction.

The APN Codex operates as a chart of accounts for macroeconomic and property risk data. The 21000 Series captures objective institutional data inputs from the Reserve Bank of Australia, the Australian Bureau of Statistics, the Australian Prudential Regulation Authority, the Australian Securities and Investments Commission, and the Australian Energy Market Operator. The 24000 Series captures proprietary derived indices. This research brief operates at the level of media-environment analysis adjacent to the 21000 Series.

The variable operative nodes engaged by this brief are: 21310 (Taxation & Revenue Policy), 21320 (Planning Regulations & Zoning), 21330 (Housing Policy), 21370 (Tenancy & Consumer Protection Law), 21620 (Market Psychology & Herd Behaviour), 21640 (Measured Consumer & Business Sentiment), and 21680 (Media & Narrative Sentiment Index — activated 14 May 2026; AUS-151 constitutes the inaugural empirical research instrument for this node).

Abstract

This brief analyses the Australian media coverage of the housing and property measures contained in the 2026–27 Federal Budget. Seven independent research streams documented the coverage architecture, structural conflicts, voice amplification, omission patterns, representational equity, and political-register characteristics across twelve outlet categories. Convergent findings establish that commercial and industry voices achieved materially greater amplification than advocacy voices for the identical budget event; that renter-focused measures (notably Measure 12 Commonwealth Rent Assistance and Measure 13 A Better Deal for Renters) were consistently omitted from commercial property and specialist financial media; that the grandfathering provisions in Measures 1 and 2 were inconsistently explained across the ownership groups; and that the “35,000 fewer homes” figure derived from government Treasury modelling was reproduced across commercial media as the dominant counter-narrative without consistent contextualisation against the offsetting modelled effects. The brief identifies the five measures constituting “the Invisible Budget,” documents the activation patterns of the 2019 historical-conflict frame, and flags the time-sensitive sentiment implications for the 21620 node ahead of the policy’s July 2027 implementation.

Section 1 — The Budget as a Media Event

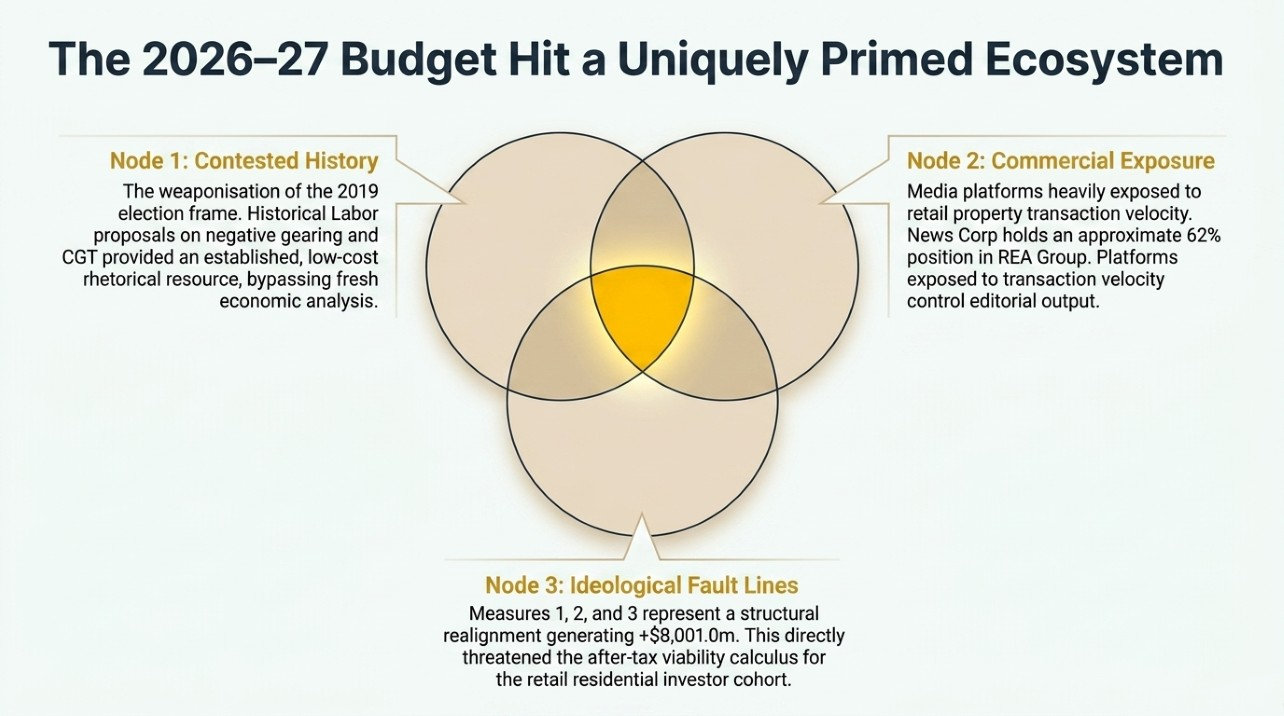

The 2026–27 Federal Budget arrived in a media ecosystem with three structural conditions that elevated its coverage intensity to a level not observed since the 2019 election cycle. The first condition is the contested history of negative gearing reform. The Australian Labor Party’s proposed restrictions on negative gearing and the capital gains tax discount in the 2019 federal election cycle were deployed by the Coalition, by the property sector, and by News Corp mastheads as a structural threat to investor and aspirational buyer interests, and contributed to the Coalition’s electoral victory. The 2026 measures bear material structural similarity to the 2019 proposals — though with significantly different transition dates, grandfathering provisions, and a new-build carve-out — and the historical frame was therefore available as an established rhetorical resource for any commentator seeking to characterise the budget without conducting fresh economic analysis.

The second condition is the commercial exposure of dominant media ownership groups to property market conditions. News Corp Australia holds an approximately 62% ownership position in REA Group, the operator of realestate.com.au and Australia’s dominant residential property listings platform. Domain Group, the principal competitor in residential listings, was acquired by US real estate data company CoStar Group in August 2025 for approximately $3 billion, severing the longstanding commercial relationship between Nine Entertainment’s mastheads and the residential listings platform. At the time of the 2026–27 budget, Nine print mastheads therefore operated without a direct residential listings commercial interest. The 151-4 research stream documents a 100% conflict-of-interest disclosure failure rate across the assessed property specialist media, including the dominant portals and their associated data subsidiaries, the investor-focused property publications, and the mortgage and finance comparison sites. The implication is structural: platforms most exposed to changes in retail-investor transaction velocity operate adjacent to, or within the same corporate ecosystems as, a significant share of housing-related editorial output.

The third condition is the pre-existing ideological fault line activated by Measures 1, 2, and 3. The combined revenue generation of +$8,001.0m from these three taxation measures (per the AUS-151-1 factual baseline) represents the largest structural realignment of residential property taxation since the 1999 introduction of the 50% CGT discount. The measures’ core mechanics — restricting negative gearing to new residential builds while grandfathering existing investments, replacing the 50% CGT discount with an inflation-indexed model and a 30% minimum tax on real capital gains, and imposing a 30% statutory minimum tax on discretionary trusts — together alter the after-tax viability calculus for the entire retail residential investor cohort.

These three conditions produced a budget cycle in which the editorial bandwidth of the entire Australian media ecosystem converged on a narrow band of measures (M1, M2, and to a lesser extent M3) while leaving a substantial portion of the housing and property policy architecture under-reported or absent from public discourse.

Section 2 — Structural Bias Patterns

The bias matrix produced by this research organises the structural findings by ownership group. Five ownership groups dominate the coverage landscape: News Corp Australia (print, digital, and broadcast), Nine Entertainment (print and digital), Seven West Media, the public broadcasters (Australian Broadcasting Corporation and Special Broadcasting Service), and the independent/progressive sector. A sixth grouping — the specialist property media — operates as a distinct ecosystem with its own structural characteristics.

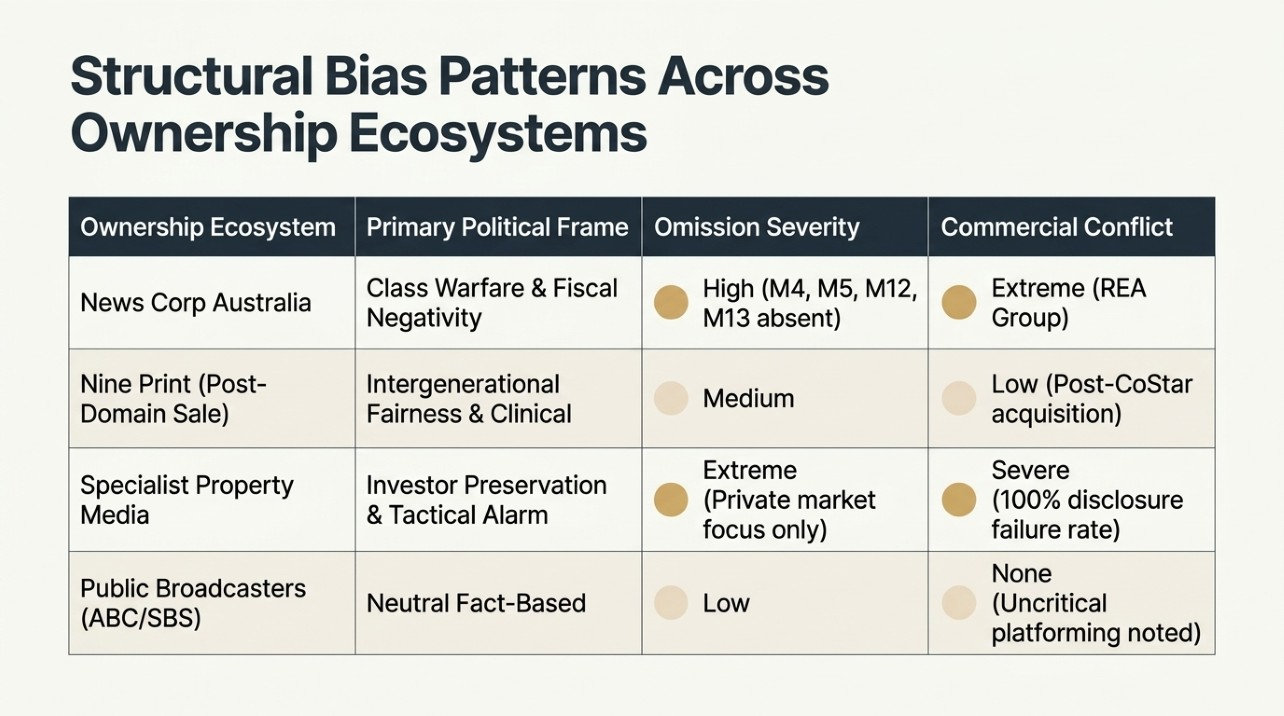

News Corp Australia. Across the print mastheads (The Australian, Herald Sun, Daily Telegraph, Courier-Mail), the coverage architecture demonstrated high within-group consistency. The 151-2 research stream documented convergent semiotic framing across state boundaries: the “Jim Reaper” motif (Herald Sun), the “communist state” framing (Daily Telegraph), the “class warfare” framing (The Australian), and the “Guide to Lying” framing (Courier-Mail). The investor cohort received approximately 65% of editorial space; the renter cohort received approximately 10% (151-7). Measures 4, 5, 6, 8, 9, 12, and 13 were absent from primary coverage. The political-register analysis in 151-8 identifies four convergent frames in operation: Frame 1 (Fiscal Negative), Frame 3 (Class Politics), Frame 4 (Electoral Motivation), and Frame 5 (Historical Conflict — the 2019 election), all in the right-conservative direction. The grandfathering provision in M1 and M2 was minimised or buried in primary coverage. The within-group findings are convergent across 151-2, 151-7, and 151-8.

The fiscal conservatism anomaly is notable: Frame 2 (positive fiscal characterisation) was absent from News Corp coverage despite the budget producing a net positive of +$6,139.2m to the underlying cash balance — a result that would conventionally attract favourable coverage from mastheads editorially committed to fiscal discipline. The digital and broadcast arms (news.com.au, Sky News Australia) operated in a format-driven variant of the same editorial line. Sky News amplified the hyper-partisan register; news.com.au tempered the print framing with pragmatic acknowledgement of the grandfathering provisions and the modelled effect on rents.

Nine Entertainment. The Nine print mastheads operated under a more clinical editorial register than the News Corp print group, with material internal divergence between the broadsheet titles (Sydney Morning Herald, The Age) and the business title (Australian Financial Review). The SMH and Age framed the budget through an intergenerational fairness lens, presenting the policy as a rebalancing rather than a punitive intervention. The AFR maintained a clinical-technical register, uniquely elevating Measure 3 (Discretionary Trusts) due to its impact on high-net-worth family office structures and providing detailed analysis of the M1 new-build carve-out and the Build-to-Rent exemption (151-2).

The Nine commercial signal is structurally distinct from the News Corp signal. Following the CoStar Group acquisition of Domain in August 2025, Nine Entertainment’s mastheads no longer operated under a direct residential listings commercial interest at the time of the budget. The SMH and Age coverage of M1/M2 through an intergenerational fairness lens is therefore more editorially independent than the research streams assumed — the framing was not commercially motivated by listings revenue. The AFR’s clinical-technical register reflects its business-title readership rather than a property portal commercial interest. The grandfathering provision was explained accurately and prominently across the Nine print group (151-7).

Seven West Media. The West Australian operated as a single-outlet group with limited national reach but high state-level salience. The 151-2 finding is that federal macroeconomic housing policy was consistently subordinated to state-level fiscal narratives, with the title focused on federal fiscal dynamics versus the WA state government’s own housing targets. The defining characteristic is parochial sovereignty rather than national political characterisation.

Public broadcasters. The 151-3 research stream documents the ABC’s coverage operated under the section 8 statutory mandate of the Australian Broadcasting Corporation Act 1983, requiring “accurate and impartial news and information.” The 151-7 representational-equity analysis records the public broadcasters demonstrated the highest representational equity across the Australian media landscape, with an approximately 1:1 investor-to-renter voice ratio.

The ABC’s coverage architecture devoted approximately 60% of editorial space to the contested tax reforms. Platform-level divergence (ABC News digital explanatory; ABC 7.30 accountability-interview register; ABC Insiders economic-orthodoxy synthesis; ABC Radio National sociological analysis) operated without contradiction on the empirical substance of the policy.

SBS uniquely framed the budget through a multicultural demographic lens, elevating Measure 21 (the Net Overseas Migration reduction to 245,000) as a housing demand variable rather than a culture-war signal, and platforming the Federation of Ethnic Communities’ Councils of Australia (FECCA) as a primary analytical source. National Indigenous Television provided exhaustive coverage of Measure 6 (First Nations Housing in Remote Communities), including community-level data — the Yarrabah Aboriginal Shire Mayor’s documentation of up to 20 people per dwelling in severely overcrowded remote-community housing — absent from all other coverage.

The 151-8 assessment is that the public broadcasters maintained first-order neutrality (the own-editorial register avoided ideological framing) but were consistently compromised at second-order neutrality: uncritical platforming of contested political claims, particularly the 35,000-homes figure deployed without immediate clinical arbitration against the M1 new-build carve-out.

Independent and progressive media. The Guardian Australia, Crikey, The Saturday Paper, and The Conversation operated as a high-internal-consistency group. The investor cohort received approximately 30% of editorial space; the renter cohort received approximately 40% (151-7). The grandfathering provision was accurately explained but criticised as inadequate. The 151-8 finding is that the progressive media produced an analytical-displacement effect analogous to — though politically opposite from — the News Corp class-political framing: the pervasive use of “housing crisis” and “housing justice” framing substituted moral characterisation for clinical mechanical analysis.

Specialist property media. The 151-4 research stream documents that the specialist property sector operates under direct commercial conflict — revenue depends on transaction volumes, listing durations, mortgage originations, and investor demand. The sector divides into five sub-groups: property portals (realestate.com.au under REA Group/News Corp majority ownership; Domain under CoStar Group ownership following the August 2025 acquisition), both deploying the grandfathering provision tactically to prevent panic-induced sell-off; property data providers (CoreLogic independent, maintaining austere macroeconomic distance; PropTrack as the REA Group analytical arm, providing tactical investor-preservation advice); investor-focused property media (PIPA, Property Update/Metropole, API Magazine, Your Investment Property, Smart Property Investment), exhibiting the lowest analytical integrity of any category audited, including commentary that diverged materially from the M1 and M2 mechanics documented in AUS-151-1; mortgage and finance media (Canstar, Mortgage Business, Finder, RateCity, Money Magazine), operating under a clinical-consumer-utility register and converting M14, M17, and M20 announcements into mortgage-origination lead-generation funnels; and industry-affiliated media (The New Daily under Industry Super Holdings/AIST), offering editorial support for retail-investor tax restrictions from which the parent industry is explicitly exempt — a structural conflict not disclosed to the readership.

Section 3 — The Omission Architecture

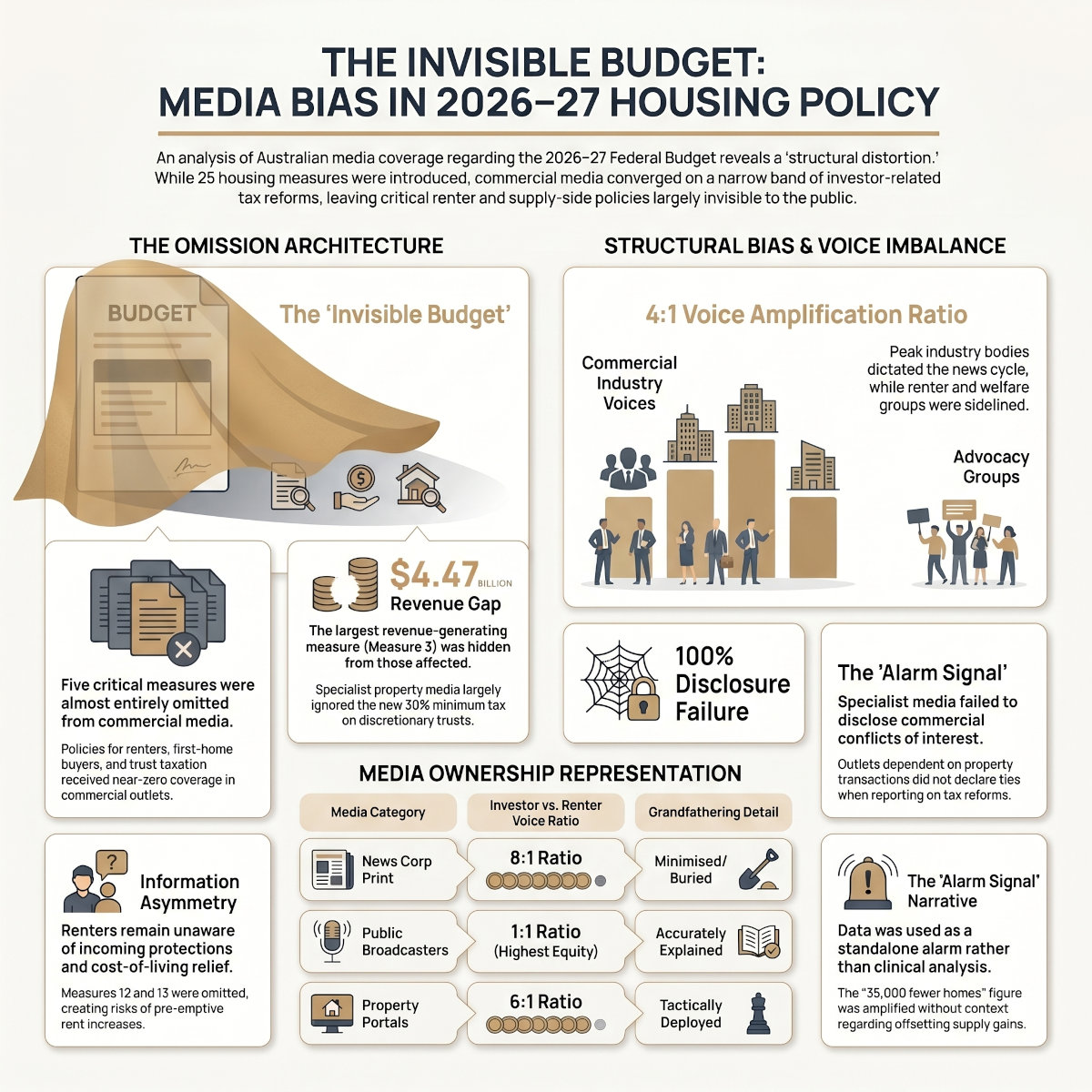

The 151-6 research stream maps coverage of all 25 budget measures across six media classifications. Only seven measures received adequate coverage (Tier 4): M1, M2, M4, M17, M18, M19, M21, and M23. Four measures were universally omitted (Tier 1): M13, M14, M16, and M24. Seven measures received Tier 2 coverage — substantive in some categories, absent in others — including M3, M5, M6, M8, M9, M12, and M22.

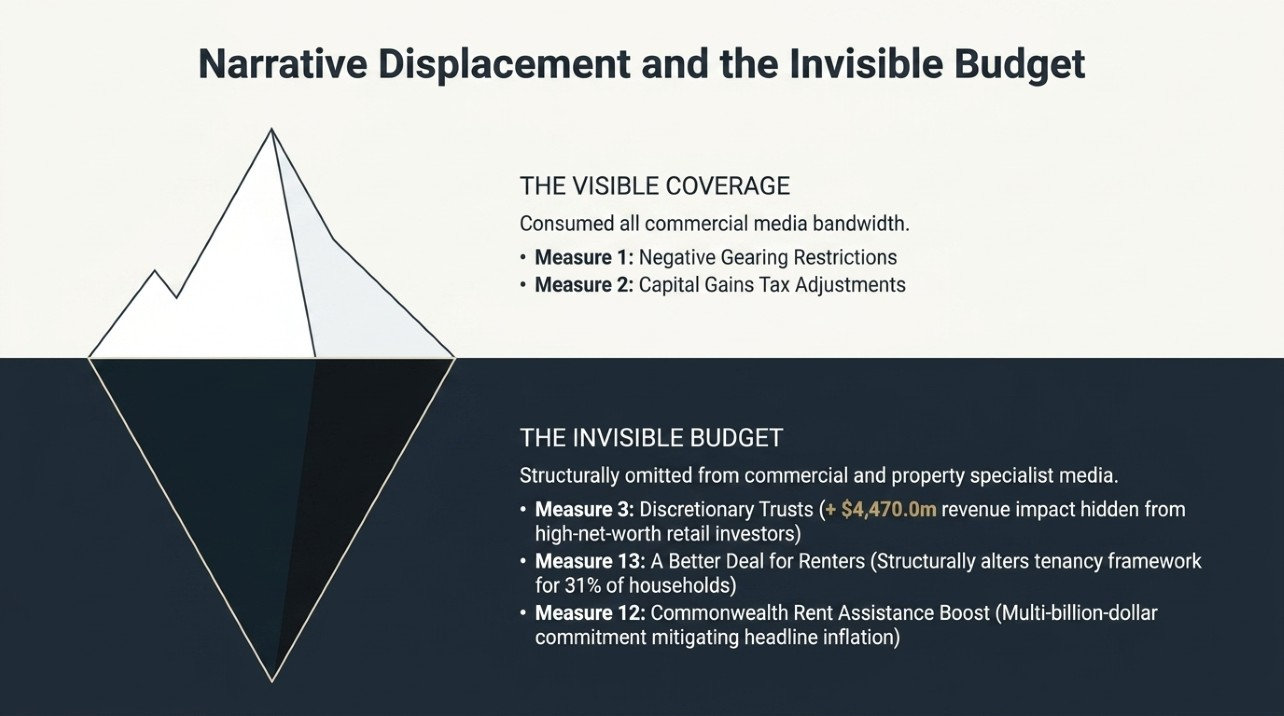

The five measures constituting “the Invisible Budget” — those representing the greatest gap between policy significance and public awareness:

Measure 3 — Minimum Tax on Discretionary Trusts (+$4,470.0m). The largest single revenue-generating mechanism in the housing measure set. Clinically covered by the AFR and progressive media but consistently absent from property specialist media and minimally referenced by industry advocacy bodies. The retail-investor demographic most affected remains largely unaware of a material tax liability on their holding structures from July 2028, including the three-year CGT rollover relief window for restructuring. The structural drivers are commercial sensitivity and ideological inconvenience: M3 directly antagonises the high-net-worth retail-investor demographic that drives the engagement and revenue metrics of the property specialist sector.

Measure 13 — A Better Deal for Renters. Structurally alters the tenancy framework for approximately 31% of Australian households. Absent from virtually all commercial coverage. The information asymmetry between landlords and tenants regarding incoming protections creates a pre-legislative window during which pre-emptive rent increases and evictions may occur before state legislation crystallises.

Measure 12 — Commonwealth Rent Assistance Boost. Multi-billion-dollar cumulative commitment supporting 1.4 million low-income renter households, with Treasury projecting a 0.5 percentage point mitigation of headline inflation. Absent from property portals and financial specialist media — the outlets least likely to be consumed by the beneficiary demographic.

Measure 20 — HELP Debt Settings. Materially elevates borrowing capacity for first home buyers under APRA serviceability buffers. Conceptually siloed as an “education” story; financial and property journalists did not run the technical calculations linking student debt relief to mortgage serviceability multipliers.

Measure 14 — Help to Buy Scheme (Status Update, +$685.0m saving). Returned $685.0m to the budget bottom line through underutilisation — a policy-design signal that has received no scrutiny from aligned or adversarial media. Aligned outlets protect the government’s housing credentials; adversarial outlets are absorbed by M1/M2.

The beneficiary omission pattern is structural rather than incidental. Measures primarily benefiting renters (M12, M13), social housing tenants (M5, M6), and lower-income graduates (M20) were consistently less covered by commercial outlets than measures affecting investors (M1, M2, M3). The 151-4 finding that specialist property media defines “the housing market” as the private, transactional property market — excluding interventions that do not generate transaction yield — captures the structural driver of this asymmetry.

Section 4 — Voice and Amplification

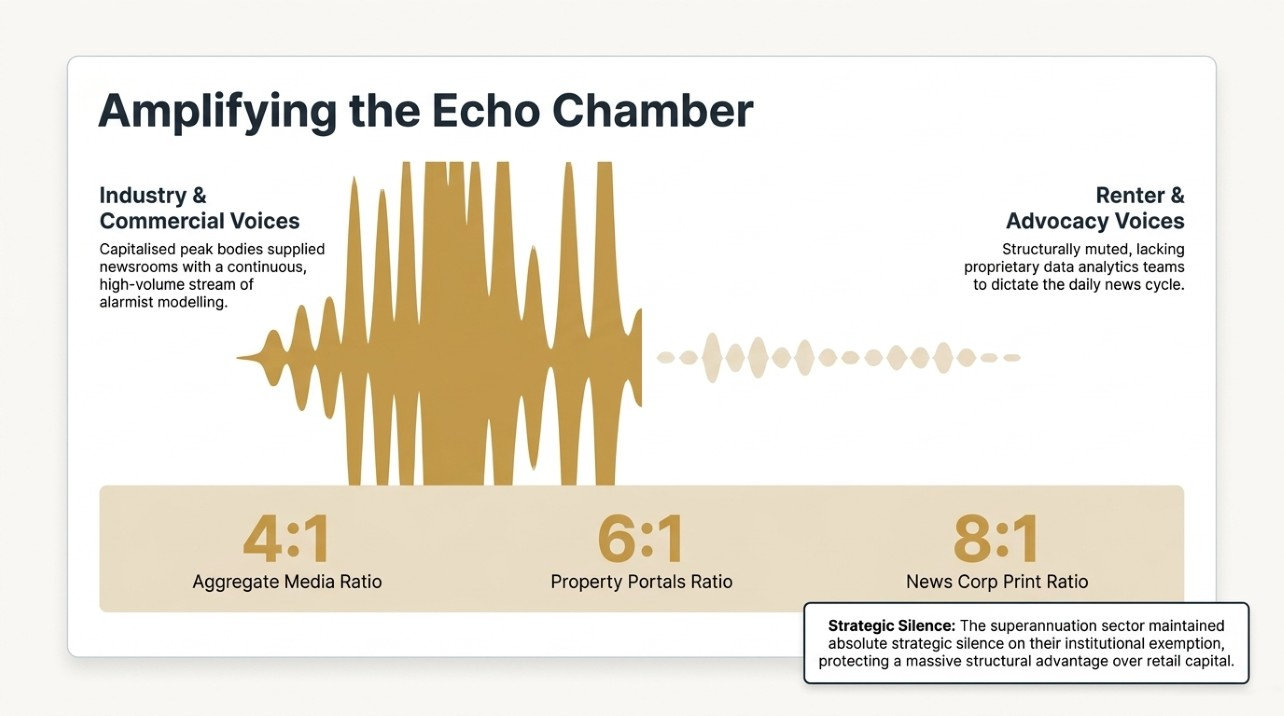

The 151-5 voice audit established that commercial and industry voices achieved materially greater media amplification than advocacy voices for the identical budget event. The asymmetry is quantified by the 151-7 stream at approximately 4:1 across the aggregate Australian media landscape, rising to 8:1 in News Corp print and 6:1 in property portals.

The structural explanation has two components. First, industry interests are represented by capitalised peak bodies (REIA, HIA, Property Council, MBA) backed by proprietary data analytics teams that provide newsrooms with a continuous stream of modelling, press releases, and available spokespeople. Renter and welfare advocacy bodies (ACOSS, National Shelter, Everybody’s Home) operate with materially smaller resourcing, limiting their capacity to dictate the daily news cycle. Second, advocacy bodies face an amplification disadvantage when a sitting government enacts their preferred policies: critique reduces to debating adequacy, which generates less editorial friction than the existential market threats deployed by industry voices.

The 35,000-homes metric illustrates the structural dynamic. The figure originated in the government’s own Treasury modelling, projecting that the M1 and M2 restrictions would result in 35,000 fewer homes being built over the next five to ten years. The REIA cited the figure continuously; the HIA used it to validate the “right hand giving and left hand taking” framing; the Master Builders Australia used it to argue that the net housing gain after M4 was only 30,000 homes. The figure was reproduced almost verbatim across News Corp print, the realestate.com.au editorial pipeline, and into ABC and SBS coverage. The contextualisation pattern divides clearly by ownership group: the public broadcasters paired the figure with the offsetting Treasury modelling (the negligible rent impact and modest house-price impact); News Corp print and the property portal editorial pipelines deployed the figure as a standalone alarm signal. The Grattan Institute provided the dominant independent modelling counter-narrative, projecting that M4’s planning reforms could unlock 60,000 additional homes annually — but the counter-narrative reached the SMH, the Age, ABC, and progressive media at materially lower amplification than the original metric reached the broader commercial ecosystem.

The three most analytically significant strategic silences identified across the research streams: the banking sector’s silence on mortgage-demographic implications of M1, M2, M3, M14, and M20; the real estate sector’s silence on the grandfathering provisions, allowing alarm framing to dominate the cycle; and the superannuation sector’s silence on the institutional exemption from M1, M2, and M3, protecting a material structural advantage over retail capital.

Section 5 — Political Register Findings

The 151-8 political-register audit identified seven characterisation frames distributed predictably across the outlet categories. The clinical baseline assessment ranks the public broadcasters and the AFR as closest to maintaining an analytical register throughout, with CoreLogic and the mortgage and finance media following. News Corp print sat at the most politically characterised end of the ranking, with investor-focused property media adjacent. The progressive media operated in an ideological register analogous to — though politically opposite from — News Corp print, producing a similar analytical-displacement effect through different framing.

The 2019 activation finding is structurally important. The Historical Conflict Frame was activated across News Corp print (directly and explicitly activated), Nine Entertainment print and the public broadcasters (implicit via the “broken promise” narrative), and progressive media (explicit as vindication). For APN purposes, the convergence interpretation is the conservative analytical claim: the 2019 frame functioned as a low-cost rhetorical resource available to any actor seeking to characterise the budget without conducting fresh economic analysis.

The fiscal conservatism anomaly is the structural absence of Frame 2 (Fiscal Positive) from News Corp coverage despite the budget producing a net positive of +$6,139.2m to the underlying cash balance. News Corp’s traditional editorial commitment to fiscal conservatism would conventionally produce coverage that praised the budget on fiscal-discipline grounds; the absence of that frame alongside the dominance of Frame 1 (Fiscal Negative) is reportable as a structural observation; it does not require inference of editorial intent to be analytically valid.

The ABC charter assessment concludes the broadcaster partially met its statutory impartiality obligation under section 8 of the Australian Broadcasting Corporation Act 1983. The own-voice register was clinically maintained, and the deployment of Treasury modelling to verify contested claims represents the most rigorous structural arbitration recorded across the research streams. The partial-compliance finding rests on the second-order neutrality failure: the uncritical platforming of Opposition claims regarding M1’s supply impact without immediate arbitration against the new-build carve-out, and the sidelining of direct stakeholder perspectives in favour of macroeconomic commentators and political proxies. The assessment is structural rather than normative.

Section 6 — Node Implications and Forward Considerations

The most time-sensitive implication of the AUS-151 findings is the 21620 sentiment vector. The dominant alarm register in commercial media around M1 and M2, combined with the suppression of the grandfathering nuance, the standalone deployment of the 35,000-homes figure, and the activation of the 2019 frame, collectively constitute a material media-driven sentiment input into the 21620 data environment. The directional effect is negative for retail investor confidence and modestly positive for first-home-buyer expectations.

The magnitude consideration is important. The M1 and M2 measures do not commence until 1 July 2027, and M3 does not commence until 1 July 2028 (per AUS-151-1). The 14-month window between budget night and M1/M2 commencement is a behavioural-response window during which retail-investor disposal activity and first-home-buyer inquiry and pre-approval activity are likely to track materially differently from the Treasury behavioural assumptions underlying the policy modelling. If sentiment-driven retail-investor disposal exceeds the Treasury assumption, the actual 21310 revenue trajectory may diverge from the projected +$3,531.0m generation, and the actual 21620 BMM reading in the established residential investor segment may register a depressed result during the H2 2026 to H1 2027 transitional window.

A secondary implication concerns the 21640 node. The cost-of-living measures (M17, M19, M23) received Tier 4 coverage but predominantly through political characterisation rather than household-finance description. The 21640 sentiment readings (the FRED OECD composite series, Westpac Consumer Sentiment, NAB Business Confidence) may therefore record a more muted upward movement in consumer confidence post-budget than the actual household-finance impact would predict, because the media framing has subordinated the cost-of-living mechanics to political character debate.

Node 21680 (Media & Narrative Sentiment Index) was activated on 14 May 2026. AUS-151 constitutes the foundational empirical content establishing the inaugural baseline reading: twelve outlet categories, a ten-vector bias matrix, and a seven-frame political characterisation taxonomy, anchored to 25 confirmed budget measures across the AUS-151-1 factual baseline. The methodology and findings are sufficient to constitute a replicable inaugural observation.

Methodological Notes

The AUS-151 research methodology consisted of seven independent deep-research outputs (AUS-151-2 through AUS-151-8) produced by a deep research agent, each using the AUS-151-1 measure inventory (APN Clinical Register version) as the factual baseline. The seven streams were run independently and without cross-contamination. The synthesis stage operates on a high-judgement analytical layer applying the APN Codex governance framework and the APN Clinical Authority Register.

The analytical significance of convergence across independent streams is structurally important. A finding documented in a single stream rests on the methodology and source selection of that stream; a finding documented in three or more independent streams represents convergent observation from independent perspectives, materially raising the confidence level. Findings are tiered accordingly: Tier 1 (convergent, three or more streams), Tier 2 (corroborated, two streams), Tier 3 (single-stream, provisional).

The methodology has known limitations. Seven research streams cannot exhaustively cover the Australian media ecosystem; smaller and regional outlets are necessarily under-represented. The 72-hour post-budget research window captures the immediate coverage cycle but not the slower analytical follow-up. The streams rely on publicly available coverage rather than direct masthead access; certain framings (particularly in subscriber-gated content) may be incompletely captured. The methodology is sufficient for the structural observation purpose of this brief, but should not be over-extended to support claims about individual journalist intent, individual masthead editorial direction, or specific corporate decision-making within media ownership groups.

The brief observes the APN Clinical Authority Register throughout. Documented source language — headlines, quoted statements, framing constructions — is reproduced as evidence of the coverage observed. The documented language is attributed to its source and is not adopted as APN voice.

Ownership correction note: The AUS-151 research streams (151-2, 151-4, 151-7) characterised Domain as a Nine Entertainment asset and analysed coverage through a Nine/Domain commercial conflict lens. This characterisation is factually incorrect as at budget night 12 May 2026: Domain Group was acquired by CoStar Group (United States) on 27 August 2025 for approximately $3 billion, with the transaction announced in February 2025. Nine Entertainment’s mastheads held no residential listings commercial interest at the time of the budget. This brief has been corrected accordingly. The primary implication for the structural analysis is that Nine print coverage (SMH, Age, AFR) is more editorially independent than the research streams assessed; the conflict-of-interest finding for Domain itself persists under CoStar ownership, given Domain’s continued dependence on property transaction volumes for listings revenue. AUS-151 — Australian Property Network — 14 May 2026 Primary node: 21680 — Media & Narrative Sentiment Index APN Experience Level 3–4 This brief does not constitute financial advice.

Research Stream Register

The following seven research streams constitute the evidential basis for AUS-151. Each was produced independently by a deep research agent using the AUS-151-1 measure inventory as the common factual baseline, without cross-contamination between streams. All seven documents are held in the APN Codex Vault under Node 21680 (Media & Narrative Sentiment Index). They are source instruments of record; the synthesis, analysis, and clinical register conversion are contained in this brief.

AUS-151-2 — Mainstream and Digital Media Coverage Sweep

Scope: 17 outlets across seven ownership groups — News Corp Australia (print: The Australian, Herald Sun, Daily Telegraph, Courier-Mail; digital/broadcast: news.com.au, Sky News Australia), Nine Entertainment (print: SMH, Age, AFR; digital: Brisbane Times, WAtoday), Seven West Media (The West Australian), independent/progressive (Guardian Australia, Crikey, Saturday Paper, The Conversation), and industry-affiliated (The New Daily).

Primary analytical variable: Commercial ownership structure and its discernible effect on editorial framing architecture, source selection, and coverage omissions.

Key findings: Documented convergent semiotic framing across News Corp print mastheads regardless of state-based readership (the “Jim Reaper,” “communist state,” “class warfare,” and “Guide to Lying” formulations). Nine Entertainment demonstrated material internal divergence between its broadsheet titles (SMH, Age) and its business title (AFR), with the AFR uniquely elevating M3. The correction note in the Methodological Notes applies: Domain was acquired by CoStar Group in August 2025, severing the Nine/Domain editorial linkage prior to the budget. The Nine print group’s editorial posture on M1/M2 is accordingly assessed as more independent than the stream assumed. Grandfathering treatment is identified as the primary factual accuracy differentiator across outlet categories. 100% conflict-of-interest disclosure failure across all commercial outlets assessed.

Convergent finding contributions: T1-1, T1-2, T1-3, T1-4, T1-5, T1-6, T1-7, T1-8, T1-9

AUS-151-3 — Public Broadcaster Framing Analysis

Scope: Australian Broadcasting Corporation (ABC News digital, ABC TV news, ABC 7.30, ABC Insiders, ABC Radio National), Special Broadcasting Service (SBS News, SBS Voices), and National Indigenous Television (NITV).

Primary analytical variable: Charter compliance against the statutory obligations of the Australian Broadcasting Corporation Act 1983 (s.8) and the Special Broadcasting Service Act 1991, with M1/M2 impartiality as the primary compliance test.

Key findings: ABC maintained first-order neutrality (own-editorial register avoided ideological framing) but was consistently compromised at second-order neutrality through uncritical platforming of Opposition supply claims against M1 without immediate arbitration against the new-build carve-out. ABC deployed Treasury modelling for verification — the most rigorous structural arbitration recorded across all seven research streams. SBS uniquely framed M21 (NOM reduction) as a housing demand variable rather than a culture-war signal, platforming FECCA as a primary source. NITV provided community-level data on M6 (up to 20 people per dwelling in Yarrabah), absent from all other coverage across all streams.

Convergent finding contributions: T1-1, T1-4; T2-2 (ABC charter partial compliance), T2-7 (SBS multicultural lens)

AUS-151-4 — Property and Financial Specialist Media Analysis

Scope: Property portals (realestate.com.au under REA Group/News Corp majority ownership; Domain under CoStar Group ownership following the August 2025 acquisition), property data providers (CoreLogic independent; PropTrack under REA Group), investor-focused publications (PIPA, Property Update/Metropole, API Magazine, Your Investment Property, Smart Property Investment), mortgage and finance media (Canstar, Mortgage Business, Finder, RateCity, Money Magazine), and general financial media (Investor Daily, The Motley Fool Australia).

Primary analytical variable: Commercial conflict of interest between outlet revenue and the budget measures being reported, and the discernible effect of that conflict on editorial framing, source selection, and factual accuracy.

Key findings: 100% conflict-of-interest disclosure failure rate across all assessed specialist media — no outlet disclosed its commercial relationship to the residential property market when covering measures directly affecting its revenue base. CoreLogic/PropTrack independence distinction produced discernibly different analytical postures: CoreLogic maintained macroeconomic distance; PropTrack provided tactical investor-preservation advice, including the explicit recommendation that most investors should not sell. PIPA commentary referenced a “two-property cap on negative gearing” and a “33 per cent capital gains tax rate with no grandfathering” — formulations that diverge materially from the M1 and M2 mechanics documented in AUS-151-1. Mortgage and finance media converted M14, M17, and M20 policy announcements into mortgage-origination lead-generation funnels.

Convergent finding contributions: T1-3, T1-8, T1-9; T3-1 (CoreLogic/PropTrack divergence), T3-3 (mortgage media lead generation)

AUS-151-5 — Industry and Advocacy Voice Audit

Scope: Six organisational groups — Group A (property/real estate industry: REIA, REIQ, REINSW, PIPA, REBAA), Group B (development/construction: Property Council, UDIA, HIA, MBA), Group C (financial services: ABA, MFAA, COBA), Group D (housing advocacy: National Shelter, Everybody’s Home, ACOSS, CHIA, Homelessness Australia, state tenant unions), Group E (research/independent: AHURI, Grattan Institute, e61 Institute, Per Capita), Group F (superannuation/institutional: Industry Super Australia, Super Members Council, AIST, FSC).

Primary analytical variable: Own-voice positions versus media-amplified positions; amplification asymmetry between commercial/industry and advocacy sectors; strategic silences on measures directly affecting each organisation’s constituency.

Key findings: REIA, HIA, and MBA achieved high media amplification; ACOSS, National Shelter, and Everybody’s Home achieved only medium amplification despite endorsing the government’s policy direction. The 35,000-homes figure (Treasury modelling) was identified as the primary industry counter-narrative, deployed by REIA and HIA as the statistical anchor for their budget response. The superannuation sector (Industry Super Australia, AIST) maintained absolute strategic silence on the institutional exemption from M1, M2, and M3 — a material structural advantage over retail capital that was not disclosed in editorial content. Property Council CEO characterised the operational environment as a “tightrope walk.” HIA characterised the budget as “right hand giving and left hand taking.” Grattan Institute provided the dominant independent modelling counter-narrative (60,000-home annual uplift from M4 planning reform).

Convergent finding contributions: T1-2, T1-5; T2-3 (institutional capital silence), T2-4 (HIA framing), T2-5 (Grattan counter-narrative)

AUS-151-6 — Framing by Omission Audit

Scope: All 25 measures from the AUS-151-1 inventory assessed across six media classifications (mainstream broadsheet/tabloid, public broadcaster, property specialist, financial specialist, independent/progressive, industry/advocacy). Each measure is assigned to one of four coverage tiers: Tier 1 (universal omission), Tier 2 (sector omission), Tier 3 (depth omission), Tier 4 (adequate coverage). Each omission was assessed against a seven-type taxonomy: commercial sensitivity, ideological inconvenience, technical complexity, audience demographics, political inconvenience, structural invisibility, and narrative displacement.

Primary analytical variable: Coverage omission patterns, their structural drivers, and the policy consequences of public unawareness of specific measures.

Key findings: Four Tier 1 universal omissions identified: M13 (A Better Deal for Renters), M14 (Help to Buy Status Update), M16 (Community and Active Transport Infrastructure), M24 (Strengthening Financial Regulation Oversight). M3 (Minimum Tax on Discretionary Trusts) was classified as a critical Tier 2 omission driven by commercial sensitivity and ideological inconvenience — the largest single revenue-generating mechanism in the housing measure set (+$4,470.0m) was largely invisible to the retail-investor audience most affected by it. M13’s universal omission creates a pre-legislative information asymmetry that may permit pre-emptive landlord activity before state legislation crystallises. M1/M2 narrative displacement is identified as a primary structural mechanism reducing coverage of supply-enabling measures (M4, M8, M9) and welfare measures (M5, M6, M12).

Convergent finding contributions: T1-1 (by omission contrast), T1-3, T1-7; T2-6 (M3 sector omission pattern)

AUS-151-7 — Investor vs Renter Axis Analysis

Scope: Representational equity assessment across all outlet categories using four measurement dimensions: (1) coverage quantum — approximate proportion of editorial space devoted to investor and renter cohort impacts; (2) register and characterisation — how each cohort was framed; (3) voice representation — which cohort’s organisational representatives were quoted; (4) implied audience construction — which cohort each outlet type implicitly addresses as its primary reader on housing issues. Two specific tests applied: the Grandfathering Coverage Test (factual accuracy and prominence of the M1/M2 grandfathering provision) and the Second-Order Renter Risk Test (whether the BTR exemption and its relationship to the renter risk from investor retreat was explained).

Primary analytical variable: Quantitative and qualitative representational equity between investor and renter cohorts across the Australian media landscape.

Key findings: Aggregate 4:1 investor-to-renter voice ratio across the Australian media landscape; News Corp print 8:1; property portals 6:1; public broadcasters approximately 1:1 (highest representational equity of any outlet category). Numerical paradox documented: Australia’s approximately 2.6 million renter households and approximately 2.2 million individual investment properties are numerically comparable constituencies — the coverage quantum does not reflect this comparability. First Home Buyer Displacement identified as a structural pattern: the FHB narrative crowded out the renter narrative in commercial media, creating a three-way imbalance where the numerically largest housing constituency received the least proportionate coverage.

Convergent finding contributions: T1-2, T1-3, T1-4, T1-8, T1-9

AUS-151-8 — Political Register Audit

Scope: Seven political characterisation frames assessed across all outlet categories: Frame 1 (Fiscal Negative), Frame 2 (Fiscal Positive), Frame 3 (Class Politics), Frame 4 (Electoral Motivation), Frame 5 (Historical Conflict — 2019 election), Frame 6 (Migration Politics), Frame 7 (Crisis Narrative). Clinical baseline ranking of outlet categories from most clinical to most politically characterised. Specific assessment of the 2019 Historical Conflict Frame activation pattern. Fiscal conservatism anomaly analysis. ABC charter impartiality assessment.

Primary analytical variable: Political characterisation patterns, their analytical displacement of clinical description, and the distribution of each frame across the outlet category spectrum.

Key findings: News Corp print maintained the highest political-contamination intensity across all assessed outlet categories. The “Jim Reaper” construction (Herald Sun), the “communist state” framing (Daily Telegraph), and the “class warfare” framing (The Australian) were identified as the most extreme instances of Frame 3 deployment across the entire research corpus. Frame 5 (Historical Conflict) was activated independently across News Corp print (as weapon), Nine Entertainment and public broadcasters (as broken promise), and progressive media (as vindication) — the same rhetorical resource serving three different purposes. Frame 2 (Fiscal Positive) was absent from News Corp coverage despite the budget’s +$6,139.2m net positive fiscal outcome. ABC assessed as partially compliant with s.8 statutory obligations. Investor-focused property media was assessed as exhibiting the lowest analytical integrity of any category, adjacent to News Corp print in the clinical baseline ranking.

Convergent finding contributions: T1-1, T1-6, T1-7; T2-1 (2019 frame activation), T2-2 (ABC charter) Research Stream Register — AUS-151 — Australian Property Network — 14 May 2026 All seven source documents held in APN Codex Vault — Node 21680 — Media & Narrative Sentiment Index