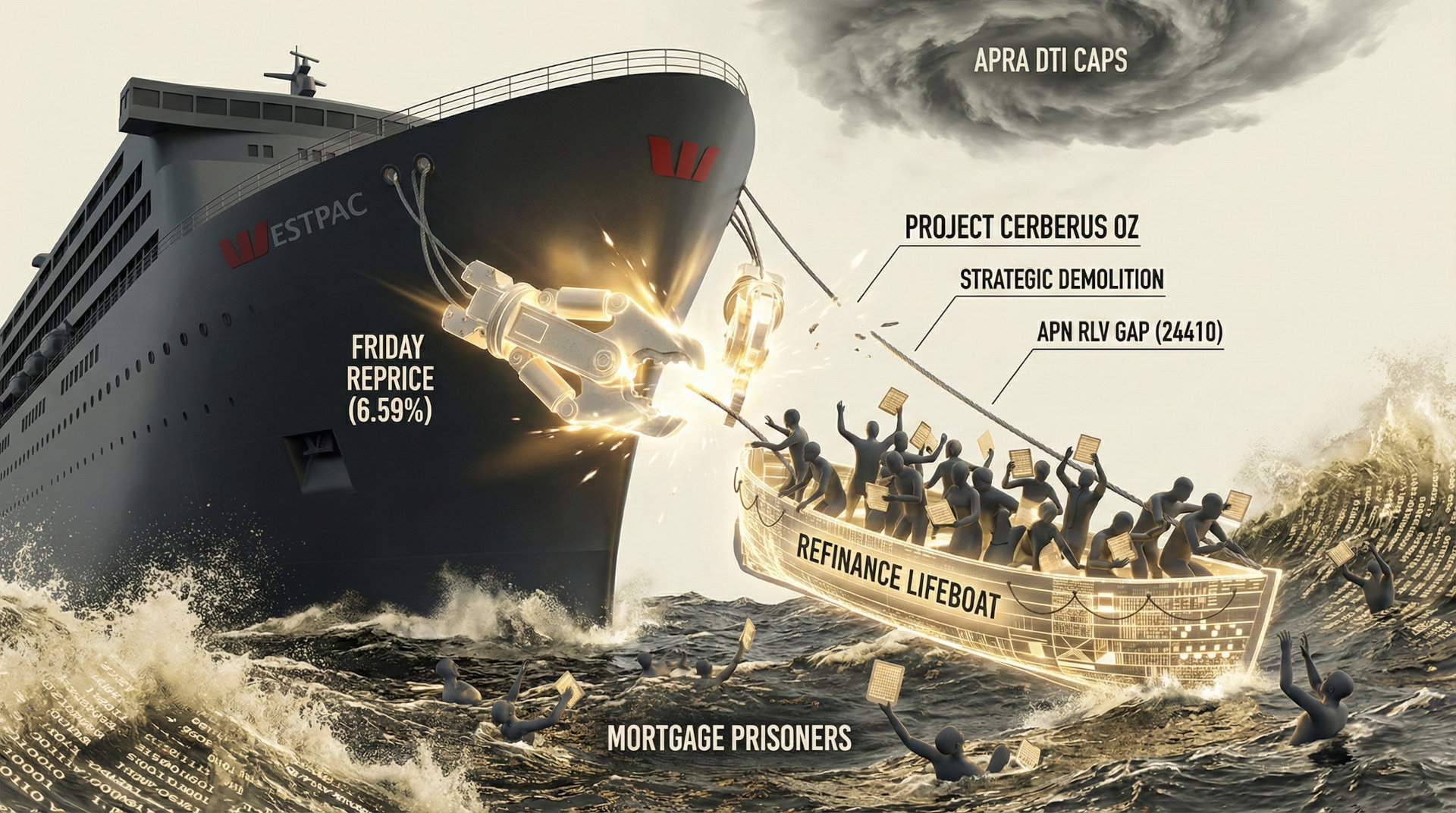

Westpac’s ‘Friday Reprice’: A Structural Reduction in Refinance Pathways

APN ANALYSIS: A-260130-AUS135989

Executive Summary

Westpac Group has executed a strategic repricing event, hiking key fixed interest rates by 40 basis points to 6.59% effective 2 February 2026. The notification, issued just 48 hours before new APRA lending restrictions take effect, is not a standard reaction to rising funding costs. APN analysis confirms this is a deliberate “Volume Control” manoeuvre designed to throttle application inflows, particularly from property investors, and de-risk its balance sheet ahead of the new Debt-to-Income (DTI) regulatory regime. By pushing the serviceability assessment rate to 9.59%, Westpac has effectively negated the refinance pathway for thousands of borrowers rolling off fixed rates from the 2021-2023 period, creating a new cohort of “structurally constrained mortgage holders”.

For property professionals, this event signals a structural break in credit availability and the end of the low-friction refinance exit for highly leveraged clients. Westpac, one of the ‘Big 4’ pillars of the market, is actively de-marketing to entire borrower segments, signalling its internal risk models anticipate a material deterioration in credit quality. This will directly impact transaction volumes, force a recalibration of valuation assumptions for investor-grade stock, and necessitate an immediate pivot in finance strategies for clients approaching the fixed-rate maturity horizon.

Background & Strategic Context

This event validates and calibrates several of APN’s core macro-theses, demonstrating how top-down regulatory intervention directly forces commercial reactions that reshape market access and outcomes. Westpac’s repricing is not an isolated treasury decision; it is a calculated response to a confluence of regulatory pressure and deteriorating risk outlook, confirming the primacy of state-level actors in defining the boundaries of the property market.

The Primacy of State Intervention (APN SPCI, 24800): The timing and targeting of Westpac’s rate hike are inextricably linked to APRA’s activation of strict Debt-to-Income (DTI) limits on 1 February 2026. This is a textbook example of our SPCI framework, where a regulator’s action becomes the primary causal force, compelling a major bank to fundamentally alter its risk appetite and pricing structure to ensure compliance.

The Operationalisation of Regulatory Risk (APN Risk & Compliance Index™ (24200)): Westpac’s move is a direct commercial response to the compliance risk posed by the new DTI caps. The bank is acting pre-emptively to avoid breaching the regulatory limit on high-DTI lending. This defensive manoeuvre is a clear manifestation of the risk quantified by our APN Risk & Compliance Index™ (24200), where the potential for regulatory enforcement action forces a bank to sacrifice market share for compliance.

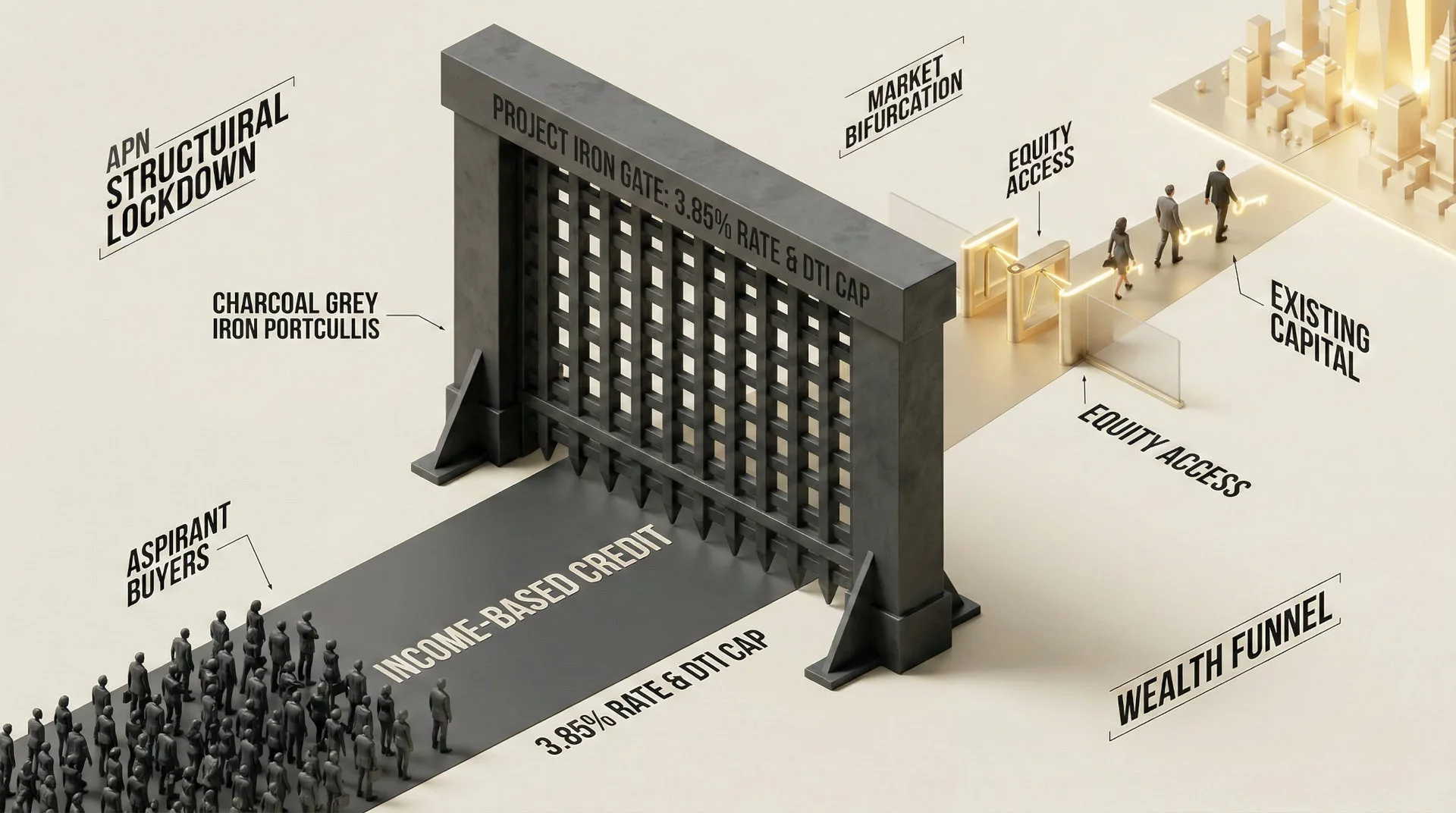

The Acceleration of Market Bifurcation: By setting a structurally constraining rate of 6.59%, Westpac creates a two-tiered market. Low-leverage, high-income borrowers can still transact, while those with higher debt levels are constrained. This action accelerates the division between unencumbered and leveraged cohorts, a structural condition where market adjustments disproportionately affect those with reduced financial capacity, constraining them within their existing financial arrangements.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the broker alert communication chain, competitor pricing data, and wholesale market data from 30 January 2026. The key facts are:

- The Rate Adjustment: Westpac Group, including subsidiaries St George and Bank of Melbourne, repriced its 3-Year and 5-Year fixed rates to 6.59% for specific high-risk cohorts, notably Investor and Interest-Only (IO) loans, effective 2 February 2026.

- The Strategic Timing: The repricing alert was issued at 14:00 on Friday, 30 January 2026. This created a structurally disruptive 48-hour window before APRA’s new DTI limits became effective on Sunday, 1 February, a move designed to clear the application pipeline and throttle last-minute high-risk applications.

- The Asymmetric Targeting: The 6.59% rate is applied directly to the borrower segments most exposed to the new DTI caps. Critically, Owner Occupier IO loans were also hiked to parity with Investor loans, removing a traditional relief valve for financially constrained borrowers and signalling a substantive “risk-off” stance.

- The Expanded Margin Outlier: The 6.59% rate establishes a gross margin of ~235 basis points over the 3-Year Swap Rate (4.24%). This is significantly above the industry norm of 180-200bps and places Westpac ~55-95bps above its major competitors, confirming the move is a deliberate “de-marketing” strategy, not a simple pass-through of funding costs.

Critical Analysis & Balanced View

The narrative that this repricing is solely driven by the market-driven increase in wholesale funding costs is an incomplete explanation. While swap rates rose ~16bps, this accounts for less than half of Westpac’s +40bps hike. The remaining premium is a deliberate expansion of the bank’s Net Interest Margin (NIM), confirming a strategic shift from volume acquisition to risk pricing. The 55bps margin disparity with its closest peer, CBA, is the key indicator confirming Westpac is intentionally positioning itself out of the market for specific loan types.

This is “Risk Pricing” in its purest form. By widening the spread to an elevated 235bps, Westpac is accumulating income today to provision against an anticipated increase in arrears and defaults tomorrow. The bank is signalling that its internal models forecast a significant deterioration in credit quality as the volume of fixed-rate mortgages reaching maturity materialises throughout 2026. They are choosing to sacrifice market share to strengthen their balance sheet against this incoming structural pressure.

This action is best understood as a “First Mover Disadvantage”. Westpac has likely acted first and most substantively because its balance sheet has the highest exposure to the new DTI limits. By making its products uncompetitive, it effectively transfers its regulatory pressure to peers like NAB and ANZ, who appear to have more headroom under the cap. Westpac is absorbing the reputational and commercial consequences of being the market outlier to solve an urgent internal compliance pressure point.

Strategic Implications for Property Professionals

- For Mortgage Brokers & Finance Strategists: The refinance exit for high-DTI and investor clients is closing at an accelerated rate. Immediately prioritise and assess your client pipeline; any applications targeting Westpac for these products are now likely unviable. Your strategic value lies in identifying the lenders with remaining DTI headroom, but you must advise clients that this window may also close without notice.

- For Agents & Buyers’ Agents: Investor and highly-leveraged buyer capacity has been structurally reduced in a short timeframe. Pre-approvals issued even last week may no longer be honoured or may be subject to reassessment. You must re-qualify buyers on their actual borrowing capacity in this new environment, not on outdated assumptions. Expect a cooling of demand and longer days on market in investor-heavy postcodes.

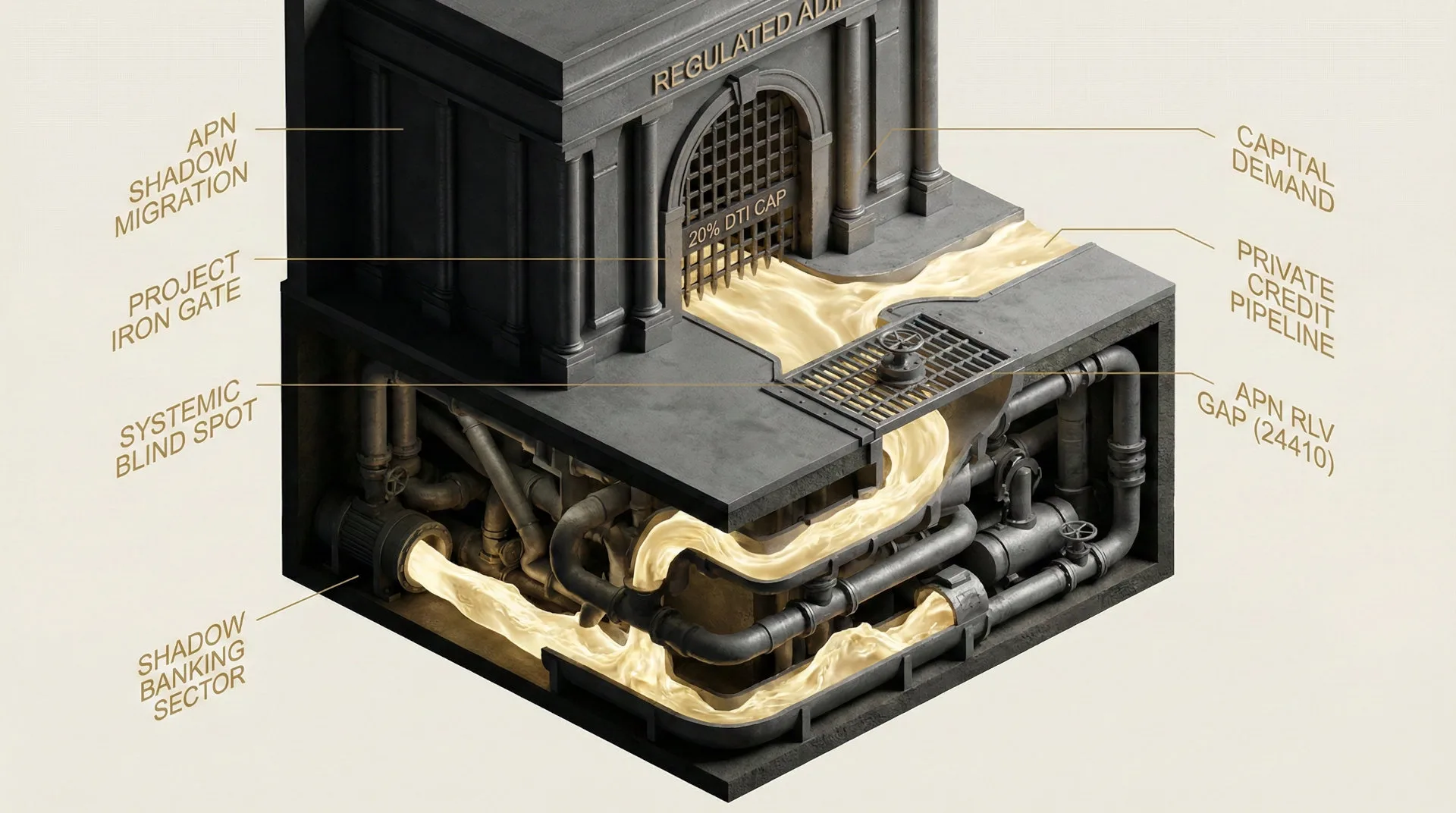

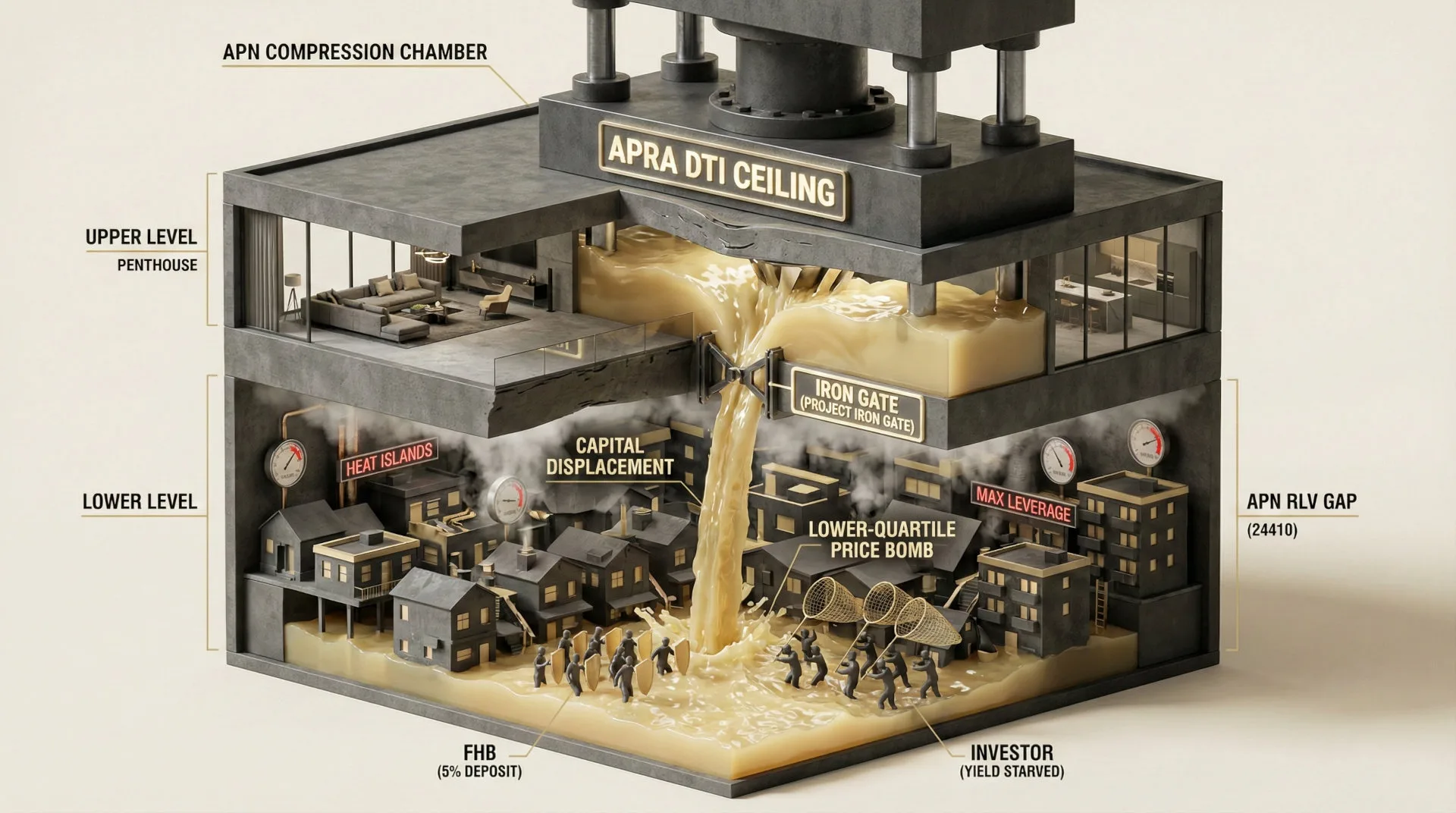

- For Developers & Valuers: This is a direct signal of reduced credit availability, which will impact end-purchaser demand and therefore project feasibility. Valuations for off-the-plan stock, particularly apartments targeted at investors, must now factor in a higher probability of settlement failure. The APN Residual Land Value (RLV) Gap™ (24410) will widen for any project reliant on a high-leverage investor cohort.

- For Asset & Fund Managers: The emergence of “structurally constrained mortgage holders” will materially impact the performance of Residential Mortgage-Backed Securities (RMBS). Expect lower prepayment speeds (as borrowers cannot refinance) and higher default probabilities on tranches with high exposure to 2022-vintage, high-LVR loans. It is time to re-assess portfolio weightings based on individual lender exposure to this newly constrained cohort.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This event provides high-confidence validation for the APN Risk & Compliance Index™ (24200), demonstrating a direct and immediate commercial reaction to a regulatory trigger. The repricing action is a textbook example of the risk quantified by the APN Regulatory Velocity Multiplier™ (24210), where the velocity of the approaching deadline forces a pre-emptive, market-altering response.

- Index Calibration: The APN Professional Sentiment Index™ (24300) will be calibrated to capture the immediate negative sentiment adjustment among mortgage brokers regarding credit availability. Data flowing through the APN Symbiotic Intelligence Network™ (24310) will be monitored for an increase in reports categorised under “lender risk appetite” and “deal viability”.

- Data Capture: This event triggers a new data capture mandate to track the pricing delta between the ‘Big 4’ banks on high-risk products (Investor/IO). This spread will be integrated as a new input into the APN Risk & Compliance Index™ (24200), serving as a real-time proxy for individual bank balance sheet stress and regulatory pressure.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.