The Unbankable Wall: Credit Veto Structurally Constrains 42% of Housing Pipeline, Structurally Impedes National Accord

APN ANALYSIS: A-260211-AUS137262

Executive Summary

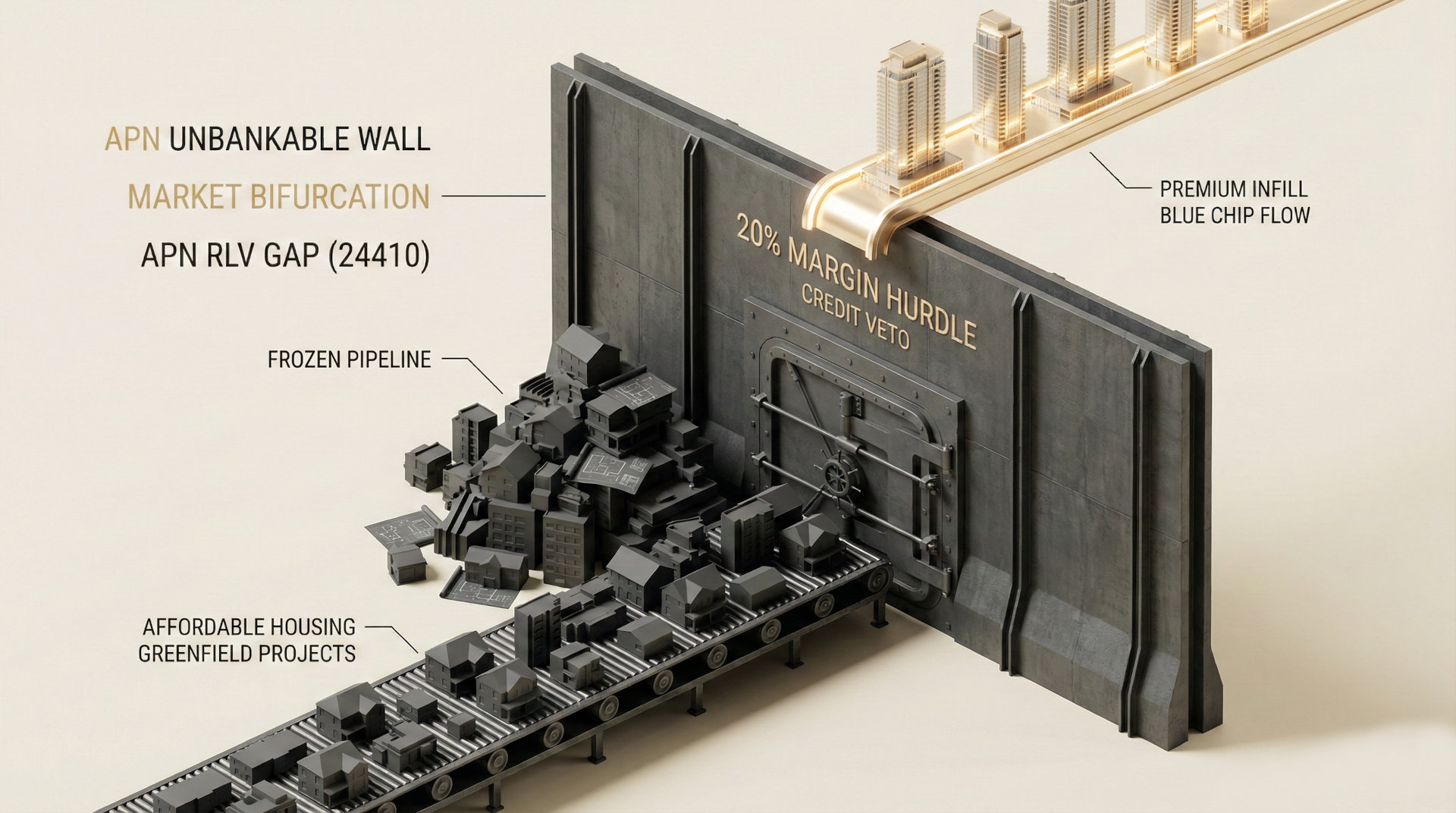

The Australian housing supply pipeline is not empty; it is structurally static. A structurally significant 29.8% contraction in private sector apartment approvals in December 2025 has confirmed the market has hit an ‘Unbankable Wall’. This is not a failure of planning but a structural adjustment in capital markets. APN analysis validates that a ‘Credit Veto’, exercised by Tier 1 lenders through a newly enforced 20% net margin hurdle, has rendered an estimated 42% of the viable greenfield and outer-metro development pipeline ‘Credit-Negative’. This recalibration of risk, driven by regulatory pressure and a higher cost of capital, is actively ‘de-zoning’ vast tracts of land intended for affordable housing, as capital bypasses these projects for ‘Blue Chip’ infill opportunities.

For property professionals, this represents a fundamental market bifurcation. The ‘Credit Veto’ mechanism means that ‘Zoned Capacity’ is now a measure that does not adequately reflect underlying structural constraint; the only pipeline that matters is the ‘Bankable Pipeline’. This creates a ‘Yield Fortress’ around existing, well-located stock by materially restricting new supply, particularly at affordable price points. Developers must pivot strategies towards projects that can absorb higher capital costs, while investors and agents must recognise that the supply constraints in the mass market are now structural, not cyclical, profoundly impacting asset selection and price growth trajectories for the foreseeable future.

Background & Strategic Context

This approvals contraction is the direct outcome of macro-financial and regulatory forces that APN has been tracking. The event validates and calibrates our core theses, demonstrating how state-level intervention physically reshapes market viability. The ‘Unbankable Wall’ is the operational manifestation of a system where capital access is no longer guaranteed by project merit alone, but is rationed according to strict, centrally-determined risk parameters.

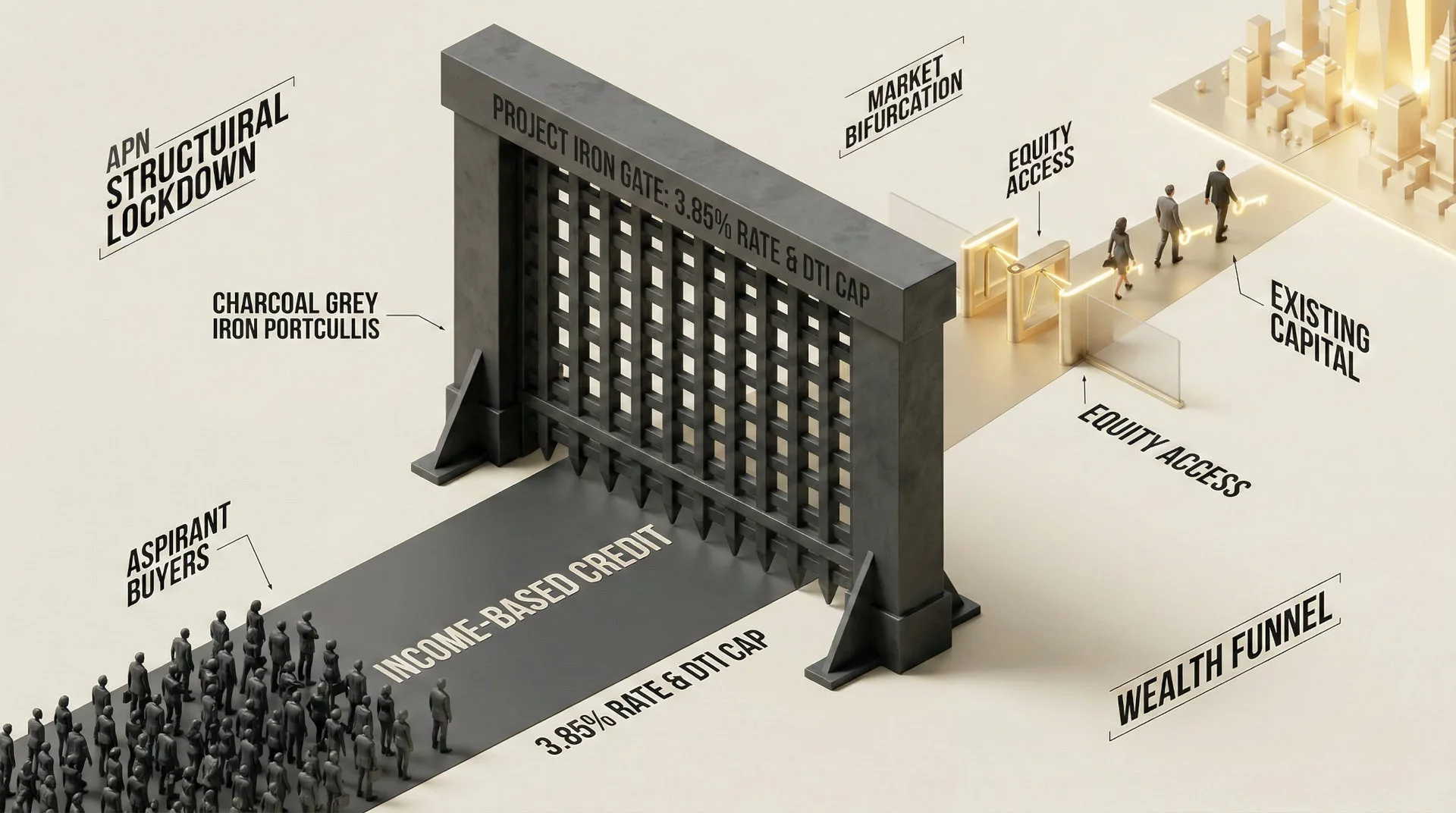

APN Sovereign Policy Composite Index™ (SPCI, 24800): The RBA’s decision to lift the cash rate to 3.85% was a material state-level intervention. While seemingly incremental, this action reset the ‘risk-free’ floor for all investment, acting as a force multiplier that immediately tightened credit conditions and pushed the required return on complex development projects beyond the reach of the affordable housing sector.

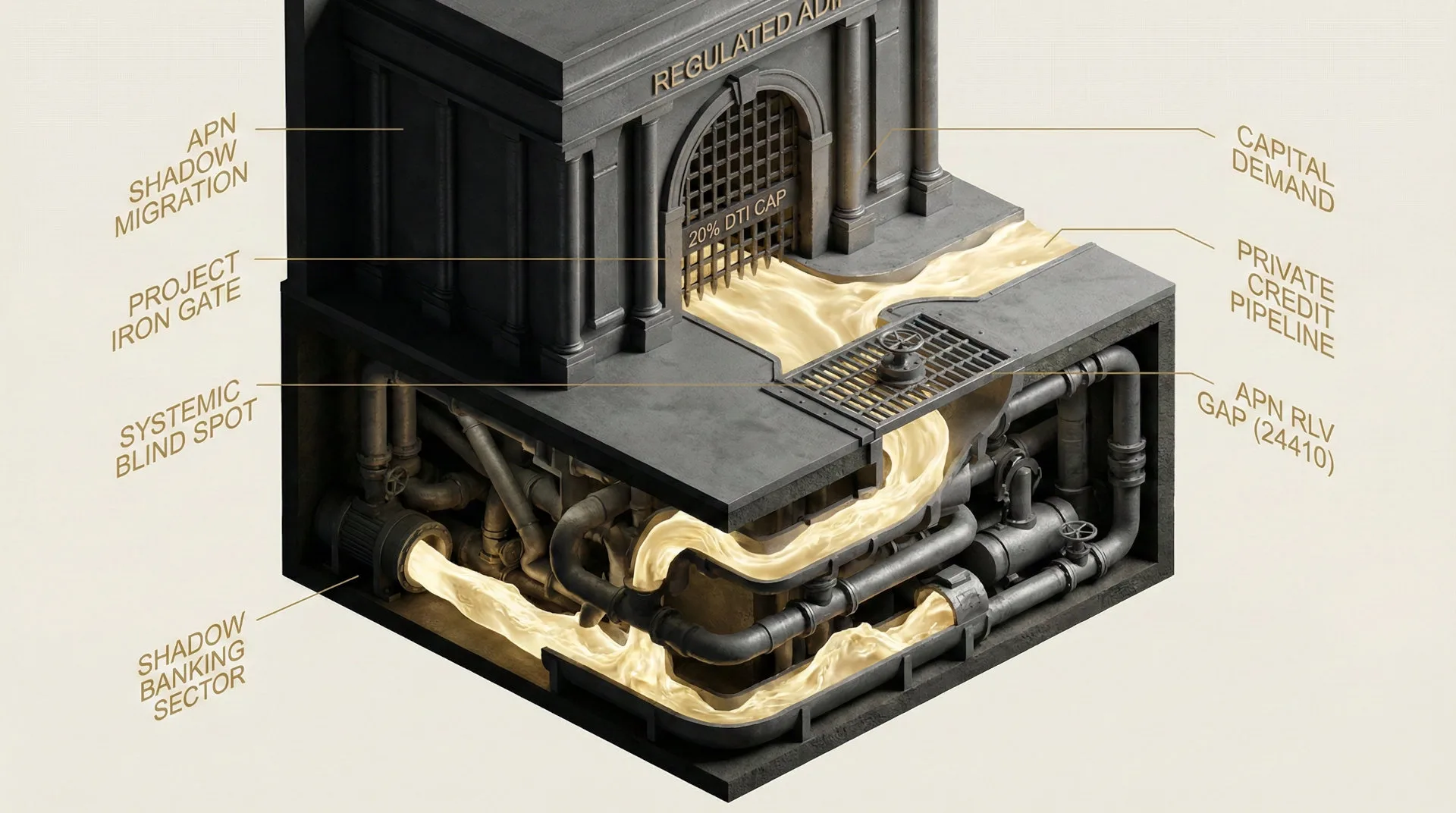

Credit Rationing Mechanism: The full implementation of Basel III and APRA’s stricter risk-weighting for commercial real estate has reinforced the credit constraint mechanism for development finance. By requiring banks to hold more capital against construction loans, regulators have induced a structural retreat from the sector, creating a material liquidity constraint. This is the core mechanism of the APN Credit Rationing Index™, where capital is allocated not to the most needed projects, but to the lowest risk.

The Viability Filter (APN Future Development Pipeline Index™): The reallocation of capital from the outer-ring to ‘Blue Chip’ infill projects is a real-world demonstration of our pipeline index. The 20% margin hurdle acts as a materially adverse economic friction filter, removing thousands of theoretically ‘zoned’ dwellings from the ‘Genuine Opportunities’ pipeline and reclassifying them as ‘Paper Rezonings’.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Australian Bureau of Statistics (ABS) Building Approvals data for December 2025, released in February 2026. The data provides validation of a systemic pressure point at the final investment decision gate for high-density housing. The key facts are:

- High-Density Contraction: Approvals for ‘Private sector dwellings excluding houses’ (apartments and townhouses) materially contracted by 29.8% in a single month. This represents the primary component of housing supply and density targets.

- Detached House Resilience: By contrast, approvals for private sector houses remained stable, rising by 0.4%. This decoupling confirms the ‘Credit Veto’ is specifically targeting high-density projects reliant on institutional finance.

- Total Pipeline Contraction: The contraction in the unit sector dragged total dwelling approvals down by 14.9%, reducing a significant portion of the forward supply pipeline in just 30 days.

- Reduction in Approved Value: The value of total residential building approved fell by 16.0%, a more pronounced decline than the volume of dwellings. This indicates a mix shift away from higher-value apartment projects towards lower-value housing.

- Geographic Concentration: The decline was led by Victoria, suggesting markets with higher construction cost escalation and existing supply overhangs are the first to hit the ‘Unbankable Wall’.

Critical Analysis & Balanced View

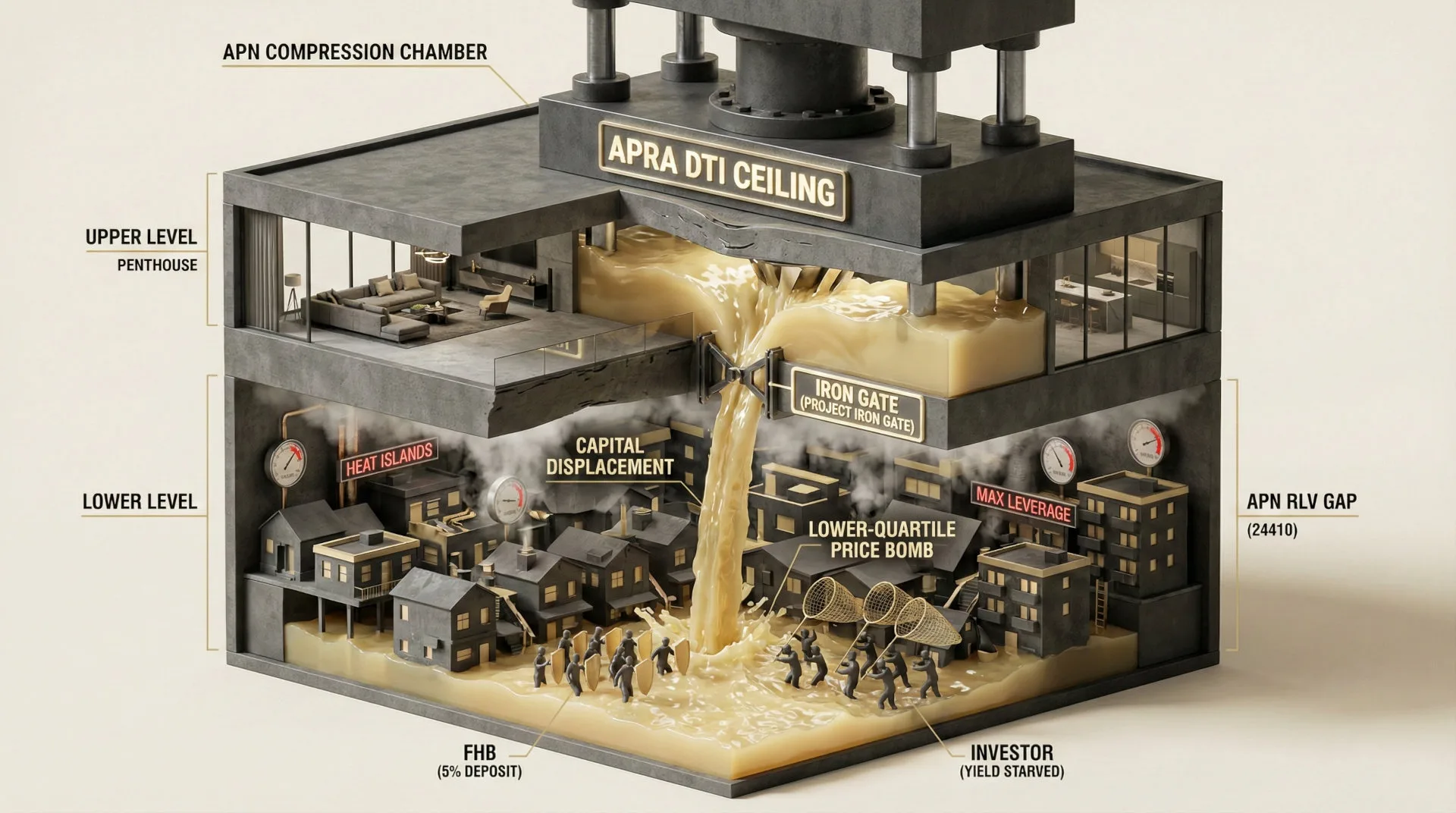

The 29.8% contraction is not a statistical anomaly but the direct consequence of a ‘Feasibility Disconnect’. The government’s focus on ‘Zoned Capacity’ has become a less material focus, obscuring the condition that land is being financially ‘de-zoned’ by banking regulation. The 500-basis-point increase in the required development margin, from 15% to 20%, has rendered unviable a significant cohort of projects designed for the affordable market, as they cannot generate the elevated profit margins now required to secure Tier 1 finance.

The alternative view that non-bank lenders will fill this gap is not supported by the data for the mass market. While private credit is available, its cost—at 12-14% per annum—is structurally adverse for affordable housing feasibility. This capital is not a viable alternative; it is a catalyst for premium projects, reinforcing the market adjustment. It funds luxury infill and Build-to-Rent, while the greenfield lots needed for first-home buyers remain undeveloped. This dynamic is compounded by the ‘Infrastructure Trap’, where a lack of project commencements means developer levies are not collected, which in turn means the trunk infrastructure required to service new land is not funded, creating a self-reinforcing structural condition of non-delivery.

Strategic Implications for Property Professionals

- For Developers: The 20% net margin hurdle is the new operating environment. Feasibilities for greenfield and outer-suburban projects must be stress-tested against this benchmark. Strategy must pivot towards ‘Blue Chip’ infill sites, joint ventures with government to de-risk infrastructure, or alternative models like Build-to-Rent that attract a different class of capital. The model of relying on 75% LTC from a major bank for a 15% margin project is no longer broadly viable.

- For Investors & Fund Managers: Capital allocation must recognise the market bifurcation. The ‘Unbankable Wall’ creates a ‘Yield Fortress’ around existing, well-located residential assets by materially constraining new competition. Focus on assets insulated from the development freeze. Opportunities exist in private credit, but only for high-yield projects capable of servicing the higher interest rates.

- For Agents & Buyers’ Agents: The projection of an impending elevated volume of new, affordable supply is not supported by current data. This structural constraint will put a structural floor under the price of established houses and units in middle and inner-ring suburbs. Advise clients that the path to asset accumulation in growth corridors has been significantly delayed, increasing demand for existing stock.

- For Planners & Government: The National Housing Accord targets are not achievable under current credit conditions. Focusing on ‘Zoned Capacity’ is less effective. Policy intervention should be reoriented from planning to finance, addressing either the capital-adequacy requirements for residential development loans (APRA) or directly funding the enabling infrastructure that is sterilising the pipeline.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides primary validation for the ‘Unbankable Wall’ thesis, which is the core premise of the APN Future Development Pipeline Index™ (24400). It confirms the operational impact of the cashflow-based rationing tracked by the APN Credit Rationing Index™ (24230).

- Index Calibration: The APN Credit Rationing Index™ (24230) is recalibrated to codify the 20% Net Margin and 65% Loan-to-Cost ratio as the new ‘Credit Veto’ floor for Tier 1 development finance. The APN Residual Land Value (RLV) Gap™ (24410) is widened for all greenfield and outer-metro sub-markets to reflect the higher hurdle rate.

- Data Capture: This analysis triggers a new data capture mandate for the APN Future Development Pipeline Index™ (24400). The mandate is to track the spread between Tier 1 bank and private credit interest rates for development finance, quantifying the ‘Cost of Capital Chasm’ as a key input for project viability filtering.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.