The Refinance Wall: How New Valuation Standards Are Constraining High-Density Apartment Owners

APN ANALYSIS: A-260202-AUS136355

Executive Summary

A structural realignment in Australia’s property valuation framework has erected a ‘Refinance Wall’ for owners of high-density, inner-city apartments. APN analysis confirms that a combination of revised professional standards from the Australian Property Institute (API) and corresponding bank credit policies has created a systemic ‘Valuation Standoff’. The core mechanism is the elevation of high-density assets to a Level 4 (Medium to High) risk profile, which automatically triggers restrictive Loan-to-Value Ratio (LVR) caps from lenders. Compounding this, valuers are now professionally obligated to disregard real-time distressed auction results as ‘non-market’ evidence, forcing them to rely on historical settled sales. This creates a ‘Valuation Lag’, where official values remain artificially high while the real market deteriorates, constraining borrowers in their existing loans.

For property professionals, this systemic friction creates a ‘Liquidity Lock’. It means official valuations no longer reflect real-time market-clearing prices, creating significant risk for agents pricing assets, developers assessing project viability, and financiers underwriting new loans. Understanding the mechanics of this ‘Valuation Standoff’, where an asset has a high paper value but zero practical liquidity for refinancing, is now of elevated importance for navigating the high-density market and managing client expectations.

Background & Strategic Context

This event validates and calibrates APN’s core macro-thesis, the APN Sovereign Policy Composite Index™ (SPCI, 24800), which posits that state and quasi-regulatory intervention is the dominant force shaping property market outcomes. The API’s actions, while not legislative, function as a significant market control, demonstrating how professional bodies can architect market boundaries and create significant economic friction. This ‘Valuation Standoff’ is not a market accident but a structured, system-level response to manage liability and credit risk.

An APN Sovereign Policy Composite Index™ (SPCI, 24800) Event: The API’s recalibration of its Professional Standards framework, specifically the guidance on ‘Forced Sales’ (ANZVGP 103) and the PropertyPRO Risk Rating Matrix, is a clear example of an APN Sovereign Policy Composite Index™ (SPCI, 24800) event. It represents a non-legislative, quasi-regulatory action that fundamentally alters the rules of capital access for a specific asset class, effectively creating a ‘Refinance Wall’ that contains risk with secondary consequences for individual asset owners’ liquidity.

A Liability Shield Dynamic (APN Risk & Compliance Index™): The tightening of professional standards is a direct response to a tightening Professional Indemnity (PI) insurance market. By creating strict, conservative protocols for evidence selection and risk rating, the API provides a liability shield for its members. This is a classic APN Risk & Compliance Index™ (24200) dynamic, where the architecture of compliance is reinforced, resulting in a protective effect for the profession, with the downstream effect of tightening credit availability for consumers.

A Structural Constraint on Sentiment (APN Professional Sentiment Index™): The new guidance forces valuers into a defensive, risk-averse position, overriding individual professional judgment with mandated protocols. This structurally constrains the discretionary professional sentiment of the valuation profession, a key input for the APN Professional Sentiment Index™ (24300). The index must now be calibrated to account for this top-down pressure, which decouples valuer sentiment from pure market dynamics in the high-density segment.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing that stress-tested the ‘Valuation Standoff’ thesis. The key facts are:

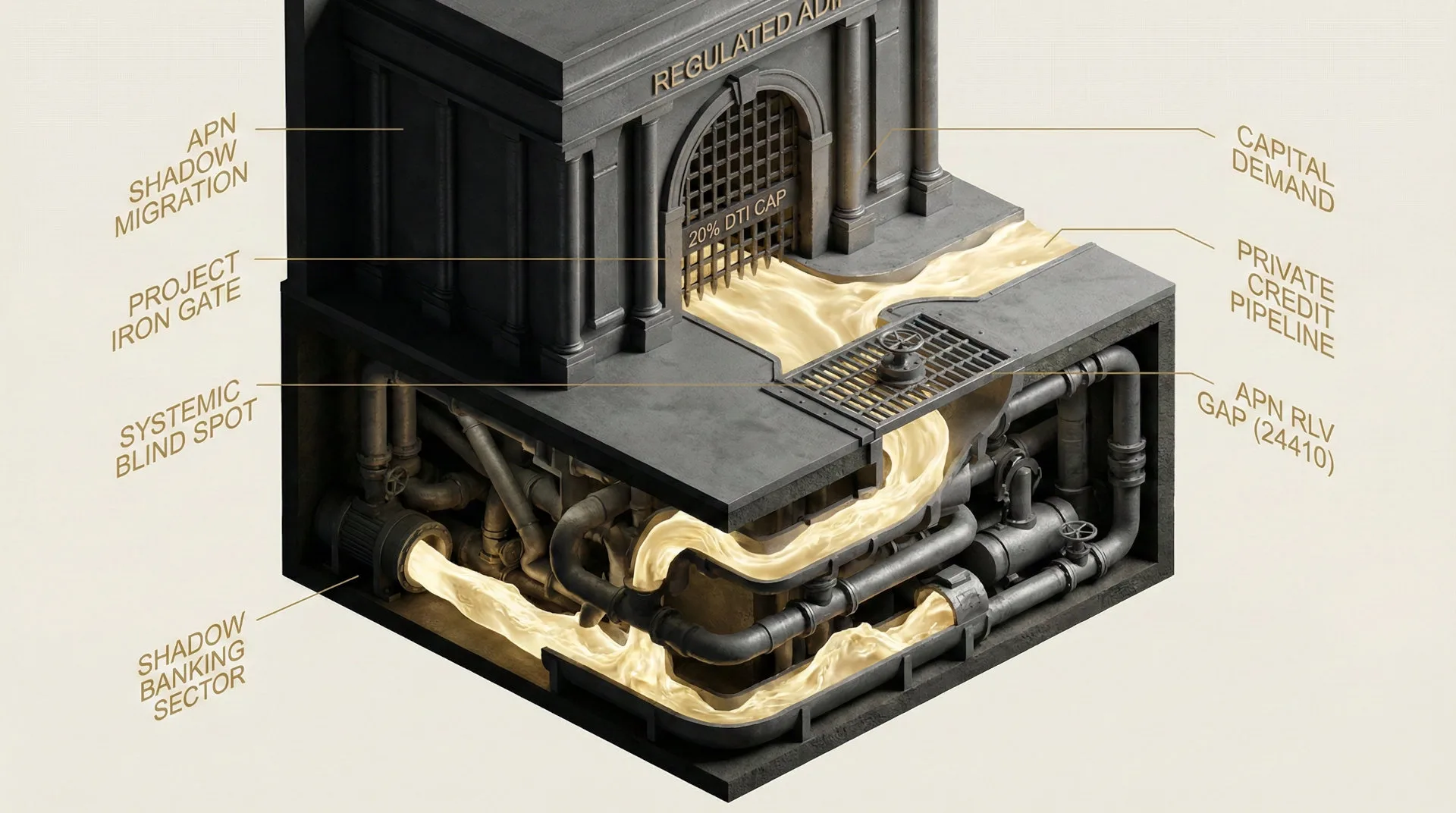

- The ‘Forced Sale’ Prohibition: Under guidance paper ANZVGP 103, valuers are professionally obligated to disregard or heavily discount distressed auction results. Because these sales involve ‘undue compulsion’ and fail the ‘willing seller’ test of the International Valuation Standards (IVS) definition of Market Value, they are treated as ‘non-market’ evidence.

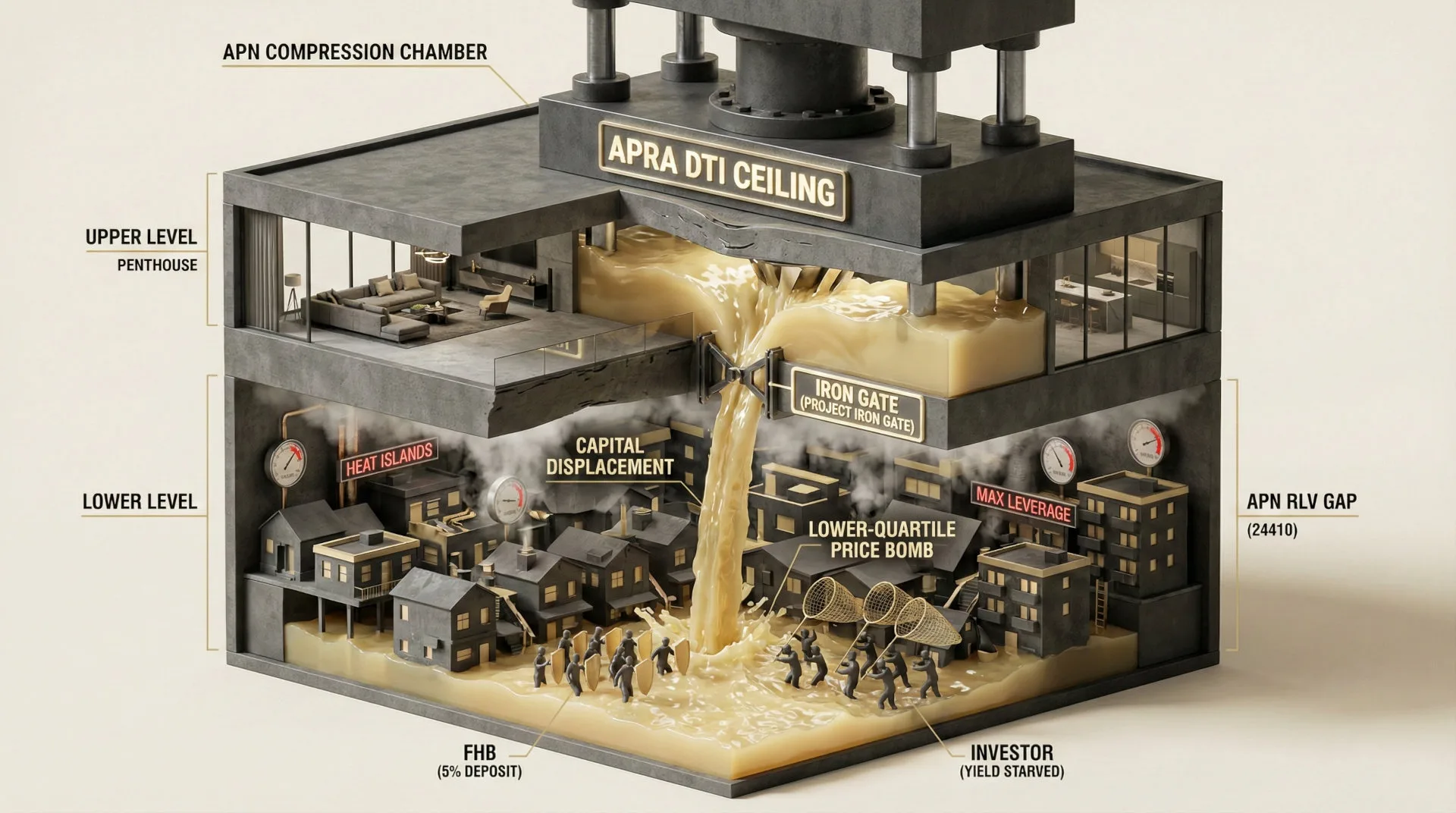

- The Risk Rating Recalibration: High-density inner-city assets (typically buildings over three storeys) are now systematically assigned a minimum Risk Rating of 4 (Medium to High) within the mandatory PropertyPRO report. This is triggered by a combination of factors, including market volatility, potential oversupply, low transaction volumes, and perceived structural risks like combustible cladding.

- The Automatic LVR Cap Trigger: A Risk Rating of 4 or 5 acts as a kinetic trigger in bank lending systems. Major lenders like Macquarie Bank explicitly cap LVRs at 70-80% for assets with a Risk Rating of 4. This materially restricts most existing borrowers from refinancing without a significant cash injection, creating the ‘Refinance Wall’.

- The ‘Valuation Lag’ Mechanism: The exclusion of real-time auction data, combined with the banking requirement for three settled comparable sales within the last six months, forces valuers to rely on historical data. This creates a ‘Valuation Lag’ of 3-6 months, where the official valuation remains anchored to past prices, obscuring the true, lower clearing price in the current market.

Critical Analysis & Balanced View

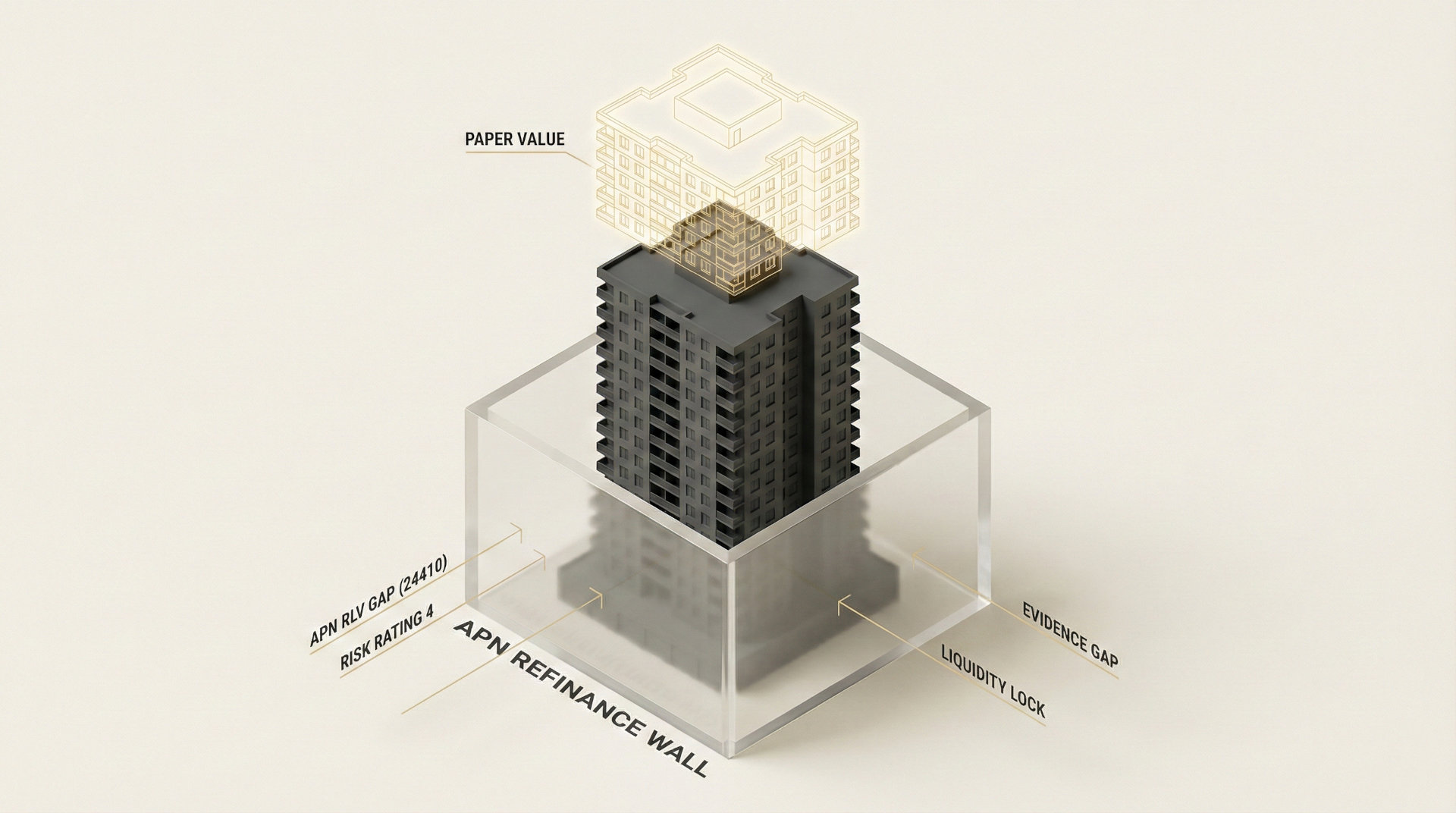

The ‘Valuation Standoff’ is not a bug in the system; it is the system functioning precisely as structured, which has the effect of protecting the balance sheets of lenders and the professional indemnity of valuers. The central paradox is that in its quest to manufacture stability and mitigate risk, the framework systematically results in a material reduction of liquidity for the asset owner. The system provides structural stability for institutions, with a secondary consequence of constraining the individual’s ability to transact or refinance.

This creates an ‘Evidence Gap’, a divergence between the ‘Official Valuation’ recorded on paper and the ‘Real Market’ price at which an asset can actually be sold or financed today. The API’s guidance on auction reliability becomes a self-fulfilling prophecy: a volatile market leads to distressed auctions, which are then discarded as unreliable evidence, which in turn forces valuations to rely on older, more stable data, thus widening the gap between the perceived value and the achievable price. The banking requirement for ‘Three Settled Sales’ cements this disconnect, especially in a low-volume market where finding recent, compliant comparables becomes structurally challenging, necessitating even greater reliance on outdated evidence.

Strategic Implications for Property Professionals

- For Valuers: The professional obligation is clear: adhere strictly to API guidance on ‘forced sales’ and risk ratings to mitigate liability, even if it creates a disconnect with real-time market prices. Documenting the rationale for evidence selection and the justification for the assigned risk rating is now a primary risk management activity.

- For Agents & Buyers’ Agents: Client education is of elevated importance. You must manage vendor and buyer expectations by explaining the ‘Valuation Standoff’. A high auction bid that fails to meet reserve is not a valuation failure; it is a market reality that official valuations cannot yet recognise. Price guidance must now account for the ‘Refinance Wall’ impacting buyer depth.

- For Mortgage Brokers & Financiers: Pre-qualifying clients now requires a ‘security-first’ assessment. Before running serviceability calculations, identify if the target asset falls into a high-density, Risk Rating 4 category. Proactively model scenarios with 70-80% LVRs to avoid last-minute failures at the valuation stage and identify potential borrowers who are structurally excluded from refinancing.

- For Developers: The ‘Refinance Wall’ directly elevates settlement risk for off-the-plan sales. Existing project feasibilities must be re-stressed assuming a percentage of buyers will fail to secure finance at previously assumed LVRs. Future project design should prioritise features that mitigate a ‘High Density’ risk rating where possible to improve purchaser access to finance.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core thesis of the APN Sovereign Policy Composite Index™ (SPCI, 24800), demonstrating how a quasi-regulatory body (the API) can architect market outcomes with the same force as legislation. It also validates the ‘liability shield’ dynamic tracked by the APN Risk & Compliance Index™ (24200), where compliance architecture is tightened to provide a protective framework for industry participants.

- Index Calibration: The APN Professional Sentiment Index™ (24300) is calibrated to recognise that valuer sentiment in the high-density segment is now structurally constrained by API guidance, decoupling it from pure market observation. The index will now weigh professional liability factors more heavily when assessing this asset class.

- Data Capture: This triggers a new data capture mandate for the APN Symbiotic Intelligence Network™ (24310): to track and quantify the ‘Evidence Gap’ by measuring the real-time delta between average settled sale prices and average ‘passed-in’ auction bid prices in high-risk postcodes.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.