Brisbane’s ‘Rental Ratchet’: How the 2026 Rate Wall and Infrastructure Delays are Driving a ‘Yield Flip’ to Units

APN ANALYSIS: A-260202-AUS136409

Executive Summary

The Queensland metropolitan property market, specifically Brisbane’s northern corridor, is undergoing a significant structural realignment. The convergence of a likely February 2026 RBA rate hike (the ‘Rate Wall’), new Debt-to-Income (DTI) lending caps, and a verified three-year delay to the Cross River Rail project is catalysing a ‘Yield Flip’. This phenomenon marks the end of the historical outperformance of detached house capital growth, which is now being superseded by high-amenity, transit-oriented unit markets in key suburbs like Chermside and Wavell Heights.

For property professionals, this is not a cyclical fluctuation but a fundamental recalibration of asset performance. The data confirms that unit markets are already outperforming houses by a significant margin—over 7% in Wavell Heights. Capital allocation must now pivot towards assets that are serviceable under new lending constraints and benefit from a ‘Scarcity Premium’ created by infrastructure delays. The period for acquiring these high-yield, high-growth assets is contracting as the market fully prices in this new structural condition.

Background & Strategic Context

This market dynamic validates and calibrates APN’s core macro-theses, particularly the APN Sovereign Policy Composite Index™ (SPCI, 24800). The confluence of RBA monetary policy, APRA’s macro-prudential rules, and the State Government’s management of the Cross River Rail project demonstrates how state-level interventions are the primary force defining market boundaries and funnelling capital towards specific asset classes.

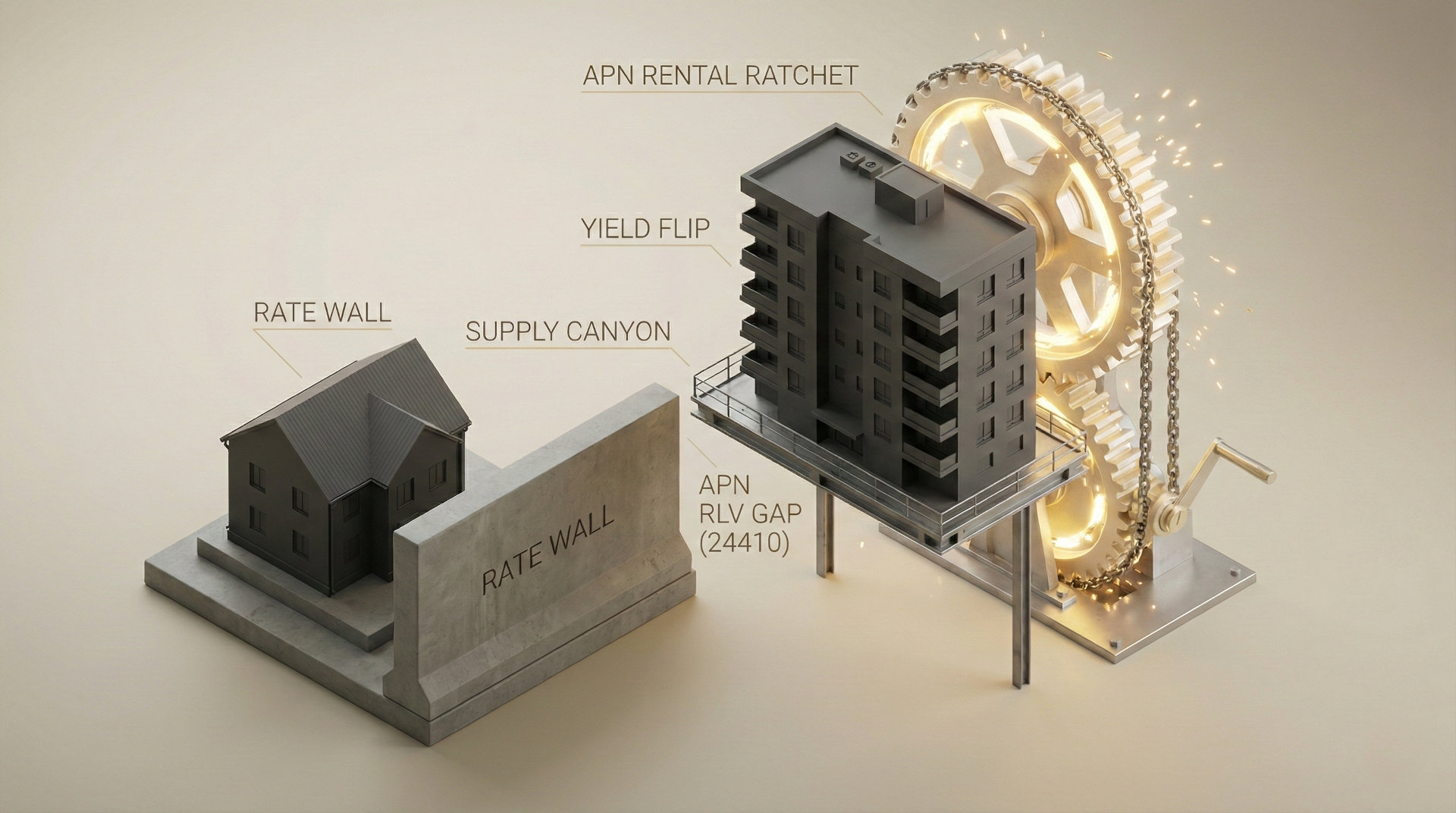

The State as Prime Mover (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The combined actions of the RBA (rate hikes), APRA (DTI caps), and the Queensland Government (infrastructure delays) are not isolated events. They are a material confluence of state-level interventions that are structurally reshaping buyer capacity and asset desirability, driving a structural shift away from detached housing in middle-ring suburbs.

Quantifying Connectivity’s Value (APN Agora™): The three-year delay of the Cross River Rail project creates a ‘Delay Premium’ for assets near existing, high-frequency transit. The APN Agora™ (Amenity & Access Index) reading for suburbs like Chermside, serviced by the reliable Northern Busway, is now significantly hardened, as their connectivity advantage is sustained until at least 2029, insulating them from disruption affecting the rail network.

The Viability Filter (APN Future Development Pipeline Index™): The ‘Supply Canyon’ thesis is confirmed by applying the APN Future Development Pipeline Index™ (24400). Despite high building approvals, rising costs and financing challenges create a significant APN Residual Land Value (RLV) Gap™, preventing approvals from converting to completions. This ensures the sustained undersupply of new units, countering the ‘Supply Flood’ counter-narrative.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing analysing the convergence of monetary, regulatory, and infrastructure vectors in Brisbane’s northern corridor. The key facts are:

- The ‘Rate Wall’: ASX 30-Day Interbank Cash Rate Futures imply a ~70% probability of a 25-basis point RBA cash rate hike to 3.85% in February 2026, creating a significant affordability barrier for high-debt borrowing.

- Macro-Prudential Tightening: New lending rules effective 1 February 2026 cap new loans with a Debt-to-Income (DTI) ratio of 6x or higher to just 20% of a bank’s new loan book, materially restricting borrowing capacity for high-value detached houses.

- The ‘Yield-to-Growth Flip’: In Wavell Heights, 12-month unit capital growth (19.53%) has surpassed house growth (12.31%) by 7.22%, exceeding the 5% threshold required to confirm a market ‘Structural adjustment’.

- Infrastructure Delay Premium: The operational launch of the Cross River Rail project has been delayed from 2026 to 2029, extending a ‘monopoly’ on high-frequency transit to existing hubs like the Chermside Interchange.

- The ‘Supply Canyon’: Brisbane’s apartment delivery is forecast at only 4,600 per year against demand for 16,000. In Chermside, the population-to-approval ratio is 10.5 people for every new dwelling approved, confirming a sustained supply deficit, not an elevated volume.

Critical Analysis & Balanced View

The ‘Rental Ratchet’ is a self-reinforcing structural condition, not a series of isolated events. The ‘Rate Wall’ and DTI caps force would-be house buyers into the unit market. This accelerated growth in demand, intersecting with the ‘Supply Canyon’, drives up both unit prices and rents. The resulting strong yields and capital growth then attract investors who are simultaneously being pushed out of the negatively geared detached house market by rising holding costs. This cycle creates a material, self-reinforcing escalation for unit values in the short to medium term.

The primary counter-risk, tracked under the APN Risk & Compliance Index™ (24200), is that the very success of this market segment could attract future government intervention—such as rent controls or inclusionary zoning—if affordability deteriorates too rapidly. Furthermore, while the Cross River Rail delay creates a premium now, it also creates a future ‘supply cliff’ circa 2029 when a new wave of transit-connected stock finally comes online. This future event must be priced into any long-term hold strategy formulated today.

Strategic Implications for Property Professionals

- For Agents & Buyers’ Agents: Re-orient clients away from the ‘house and land’ growth narrative. Focus acquisition strategies on 2-bedroom units in high-amenity, transit-connected hubs like Wavell Heights and Chermside. Emphasise serviceability under the new DTI rules and the superior rental yield as a buffer against interest rate risk.

- For Developers: The ‘Supply Canyon’ represents a significant opportunity, but the APN RLV Gap™ is a material constraint. Projects must be de-risked through efficient design, robust pre-sales, and a clear focus on delivering product (e.g., 2-bedroom units) that aligns with the new borrowing capacity of the target market. The ‘Delay Premium’ provides a 3-year window to deliver product before Cross River Rail changes the landscape.

- For Valuers & Lenders: Traditional valuation models based on historical house-vs-unit growth differentials are no longer structurally viable in this corridor. Valuations must be recalibrated to account for the ‘Yield-to-Growth Flip’ and the tangible premium attached to existing, reliable transit access. Serviceability assessments must rigorously apply the new DTI caps, which will disqualify many aspiring house buyers.

- For Property Managers: While Chermside’s vacancy rate of 0.83% (HtAG, Feb 2026) is technically higher than the 0.7% Brisbane-wide record low, it represents an Elevated Convergence. This rate has compressed from 1.6% in 2024 to 0.83% in 2026—a 48% reduction in availability. This velocity confirms that Chermside is no longer a ‘buffer’ suburb; it is a primary site of the ‘Rental Ratchet’ where high churn is being materially reduced by long-term tenure demand from the medical and retail sectors.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Infrastructure Uplift Multiplier™ (24420), demonstrating how a project delay, rather than completion, can create a quantifiable ‘Delay Premium’ for existing assets.

- Index Calibration: The APN Agora™ (Amenity & Access Index) (24140) for the northern Brisbane corridor is recalibrated to reflect the increased value of non-rail, high-frequency bus transit due to the confirmed Cross River Rail delay and ongoing rail network disruptions.

- Data Capture: This briefing triggers a new data capture mandate under the APN Future Development Pipeline Index™ (24400) to track the approval-to-completion attrition rate in middle-ring Brisbane, quantifying the structural impact of the APN Residual Land Value (RLV) Gap™.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.