Mortgage Broker Headcount Reaches Record High Amid Structurally Constrained Credit Environment

APN ANALYSIS: A-260701-AUS140365

Executive Summary

The Australian mortgage broking sector is experiencing a structural paradox: record intermediary headcount and market share are converging with a material decline in transactional efficiency and a contracting pool of available credit. This supply-demand asymmetry is driven by sustained macroprudential constraints, including the Australian Prudential Regulation Authority’s (APRA) 3.00 percentage point serviceability buffer and new limits on high debt-to-income (DTI) lending. While brokers now facilitate over three-quarters of all new residential mortgages, this market dominance masks a material deterioration in per-capita productivity, with declining application-to-settlement conversion rates indicating a significant increase in unremunerated labour across the sector.

For property professionals, this signals an impending phase of structural consolidation, not market collapse. The environment is transitioning from one of unconstrained volume acquisition to one where survival is predicated on operational efficiency and institutional-grade compliance. This shift will favour larger, technologically integrated, and commercially diversified brokerages capable of navigating a credit market defined by rationing, not price. The strategic imperative for the median practitioner is to protect conversion rates through stringent pre-qualification and to explore commercial diversification to offset the margin compression and volume constraints in the residential sector.

Background & Strategic Context

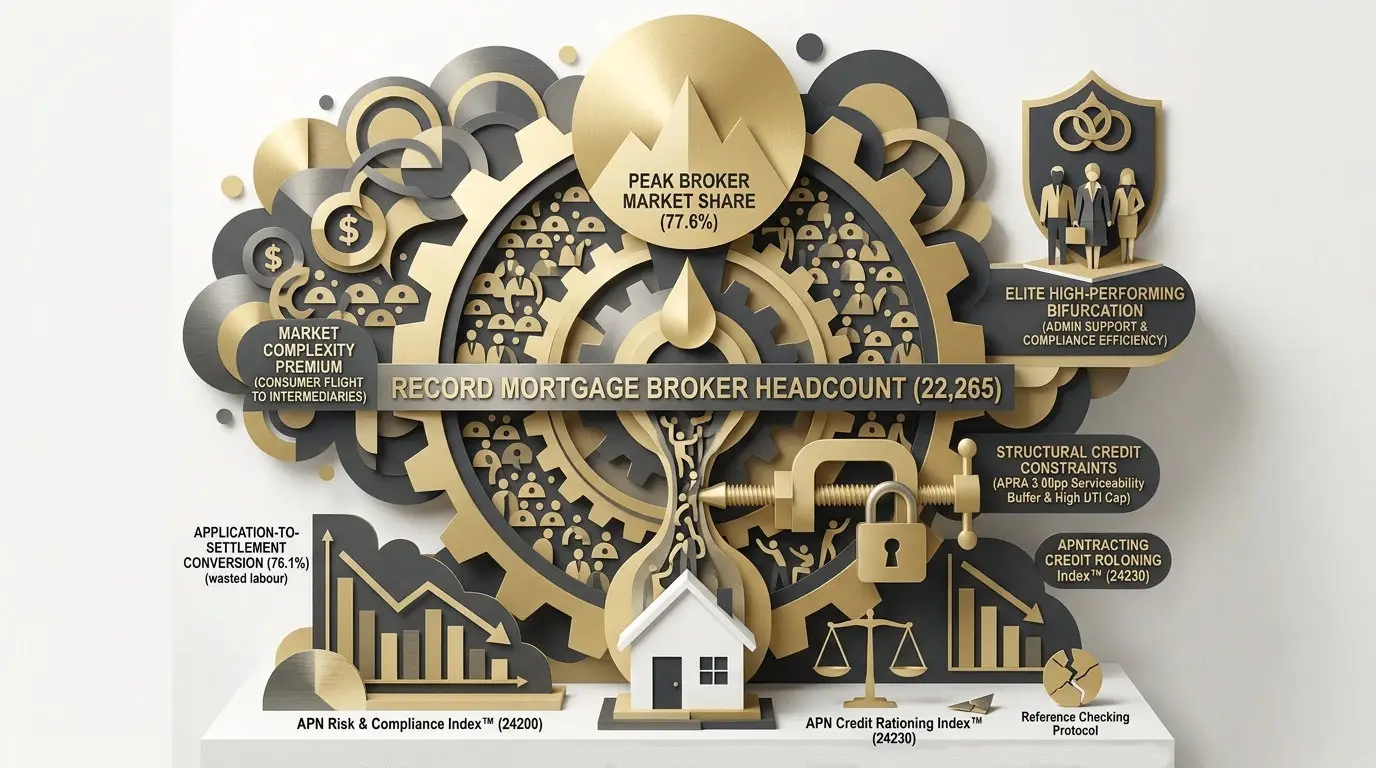

This analysis validates and calibrates APN’s core thesis on regulatory-induced market friction, specifically how sovereign policy can re-engineer capital allocation mechanisms. The mortgage broking sector provides a clear case study where macroprudential settings, designed to enhance systemic stability, create second-order effects of structural overcapacity and forced consolidation within intermediary channels. This dynamic is a key function measured by the APN Risk & Compliance Index™ (24200), quantifying the translation of policy into operational risk.

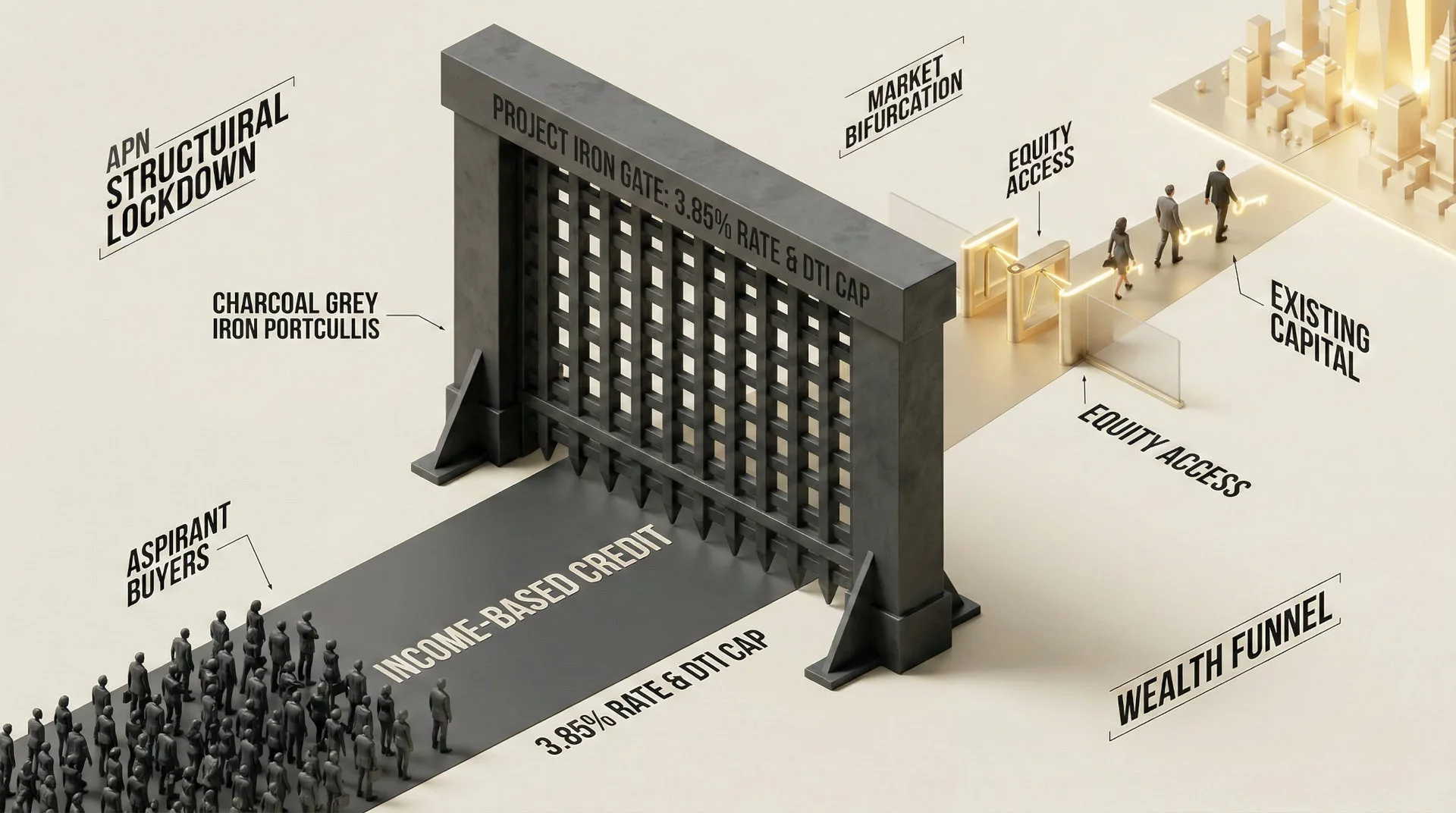

Sustained Regulatory Constraint (APN Credit Rationing Index™ (24230)): The persistence of APRA’s 3.00pp serviceability buffer and the February 2026 introduction of a hard cap on new lending at high debt-to-income ratios (≥ 6x) has shifted the market from price-based to quantity-based credit rationing. This structurally limits the total volume of convertible credit available to the market, irrespective of broker headcount or consumer demand.

Revealed Consumer Behaviour (Credit Appetite & Revealed Borrowing Behaviour (21660)): The escalation of broker market share to a peak of 77.6% is not a signal of market buoyancy but of a ‘complexity premium’. Increasing regulatory and lender policy fragmentation forces consumers into the intermediary channel to navigate the constrained credit environment, masking the underlying deterioration in per-capita productivity and profitability.

Escalating Compliance Burden (APN Risk & Compliance Index™ (24200)): The sustained decline in application-to-settlement conversion rates to 76.1% is a direct measure of systemic friction. This unremunerated labour, driven by complex Best Interests Duty (BID) obligations, fragmented lender policies, and heightened ASIC enforcement, represents a quantifiable operational risk that materially erodes profitability and viability for the median practitioner.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of data from the Mortgage and Finance Association of Australia (MFAA), the Australian Bureau of Statistics (ABS), the Australian Prudential Regulation Authority (APRA), and the Australian Securities and Investments Commission (ASIC). The key facts are:

- Record Intermediary Headcount: The number of active mortgage brokers reached a historic high of 22,265 as of September 2024, representing a 34 per cent expansion over a five-year baseline.

- Contracting Credit Volume: Total new housing loan commitments contracted by 6.2 per cent in volume and 3.8 per cent in value in the March 2026 quarter, according to ABS data.

- Peak Intermediary Market Share: The broker channel’s share of new residential lending reached a zenith of 77.6 per cent in June 2025 before a minor structural consolidation to 76.7 per cent by December 2025.

- Deteriorating Conversion Efficiency: Application-to-settlement conversion rates have steadily declined from a cyclical peak of 87.3 per cent in mid-2022 to a constrained 76.1 per cent by late 2024.

- Binding Macroprudential Constraints: APRA has maintained a 3.00 percentage point serviceability buffer and, effective February 2026, implemented a 20 per cent limit on new lending at Debt-to-Income ratios of 6x or greater.

- Emerging Consolidation Signals: The sector exhibits clear indicators of impending attrition, including a 15 per cent inactive broker cohort, sub-aggregator network exits, and heightened ASIC compliance enforcement through the new Reference Checking Protocol.

Critical Analysis & Balanced View

The primary paradox of the mortgage broking sector is that its record market share is a misleading indicator of systemic health. This dominance is a ‘complexity premium’ paid by consumers who can no longer navigate the highly fragmented and rationed credit market alone. It does not reflect a booming market, but rather one that has become too difficult for direct-to-institution navigation. This has created a highly bifurcated industry: a small cohort of elite, high-volume operators with sophisticated administrative support thrives by efficiently solving this complexity, while the vast majority of the 22,265 practitioners face diluted earnings and rising unremunerated workloads as they compete for a share of a shrinking pool of convertible credit. The aggregate market share metric, therefore, masks a material decline in per-capita productivity and viability for the median broker.

Furthermore, APRA’s DTI cap represents a structural break from previous cycles of regulatory intervention. It is not merely a cyclical tightening measure but a fundamental shift from risk-pricing to systemic credit-rationing. This change effectively terminates the historical investment model of ‘sequential equity extraction’ for leveraged investors and introduces a new, material ‘quota risk’ into the broker workflow. Brokers must now act as strategic navigators of disparate lender quotas, a skill set far removed from traditional credit advice. This exponentially increases the operational cost and uncertainty of processing high-DTI files, further eroding profitability and validating the thesis of a structurally overserved market.

Strategic Implications for Property Professionals

- For Mortgage Aggregators: The strategic imperative shifts from headcount growth to risk management and productivity enhancement. Investment must be directed towards compliance architecture and technology to identify and support high-performing brokers, while proactively managing or exiting low-volume, high-risk operators to protect the master Australian Credit Licence.

- For Individual Brokers & Brokerages: Survival and growth will depend on operational efficiency and strategic diversification. Sole operators must implement stringent pre-qualification processes to protect conversion rates, while larger brokerages should accelerate diversification into commercial lending and other less-regulated credit markets to offset residential margin compression.

- For Lenders (Banks & Non-Banks): The DTI cap creates a new competitive dynamic. Authorised Deposit-taking Institutions (ADIs) will compete on the efficiency of their quota management and processing. Non-bank lenders have a strategic window to capture high-quality, high-DTI borrowers who are rationed out of the prudentially regulated system, creating a clear arbitrage opportunity.

- For Property Investors: The era of unconstrained, high-DTI portfolio expansion using sequential equity is structurally curtailed. Future acquisitions will require higher income verification, a strategic pivot towards assets that generate higher yields to remain within DTI constraints, or a shift to lenders operating outside the direct APRA framework.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Risk & Compliance Index™ (24200) by demonstrating how sustained macroprudential policy (serviceability buffers, DTI caps) directly translates into operational friction (declining conversion rates) and structural market consolidation (broker attrition).

- Validation: The contraction in new loan commitments following the implementation of the DTI cap provides empirical validation for the APN Credit Rationing Index™ (24230), confirming its thesis that quantity-based controls are now a primary constraint on credit velocity.

- Index Calibration: The APN Regulatory Velocity Multiplier™ (24210) is calibrated to reflect the systemic impact of ASIC’s Reference Checking Protocol (INFO 257) and BID enforcement, which have accelerated the rate at which compliance risk leads to network attrition and consolidation.

- Data Capture: This triggers a new data capture mandate for the APN Risk & Compliance Index™ (24200) to monitor the quarterly DTI cap utilisation rates across major ADIs, providing a forward indicator of credit availability for high-DTI borrowers.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.