ASIC Initiates Coordinated Regulatory Intervention to Materially Constrain the Private Credit Market

APN ANALYSIS: A-251124-AUS131015

Executive Summary

In a coordinated campaign, the Australian Securities and Investments Commission (ASIC) executed a ‘maximum intensity’ enforcement spike in November 2025, focusing on the entire private credit supply chain. The regulator simultaneously launched criminal proceedings against a fraudulent asset originator, civil penalty proceedings against a key ‘gatekeeper’ research house, and litigation against major financial planning licensees. This is not a series of isolated actions; it is a kinetic manifestation of the risk framework detailed in the APN Risk & Compliance Index™ (24200), a strategic campaign designed to systematically address the opaque and asymmetrically positioned elements of the private credit sector and sever their access to Australia’s superannuation capital pool.

For property professionals, this coordinated systemic shift signals a structural realignment in the non-bank lending landscape. The resultant constraint on private credit will constrict a material source of development and investment finance, making capital more expensive and harder to secure. Developers, financiers, and consultants who rely on or service this sector must immediately reassess their funding strategies and operational risks, as the era of plausible deniability is over and the liability for inadequate due diligence has been applied as a regulatory instrument across the entire value chain.

Background & Strategic Context

This enforcement event validates and calibrates APN’s core macro-theses on the primacy of state intervention in shaping market outcomes. ASIC’s campaign is a top-down re-engineering of the risk-reward equation in a key capital market, demonstrating how regulatory action can override traditional market forces to achieve a specific policy objective: protecting the integrity of the superannuation system.

The State as Primary Actor (APN Sovereign Policy Composite Index™ (SPCI, 24800)): ASIC’s campaign is a textbook demonstration of our APN Sovereign Policy Composite Index™ (SPCI, 24800) thesis. Rather than allowing market forces to slowly correct the period of accelerated growth in private credit, a state-level actor has intervened directly to materially influence the viability of an entire asset class. This is not a market correction; it is a regulatory restructuring designed to reshape the boundaries of acceptable risk.

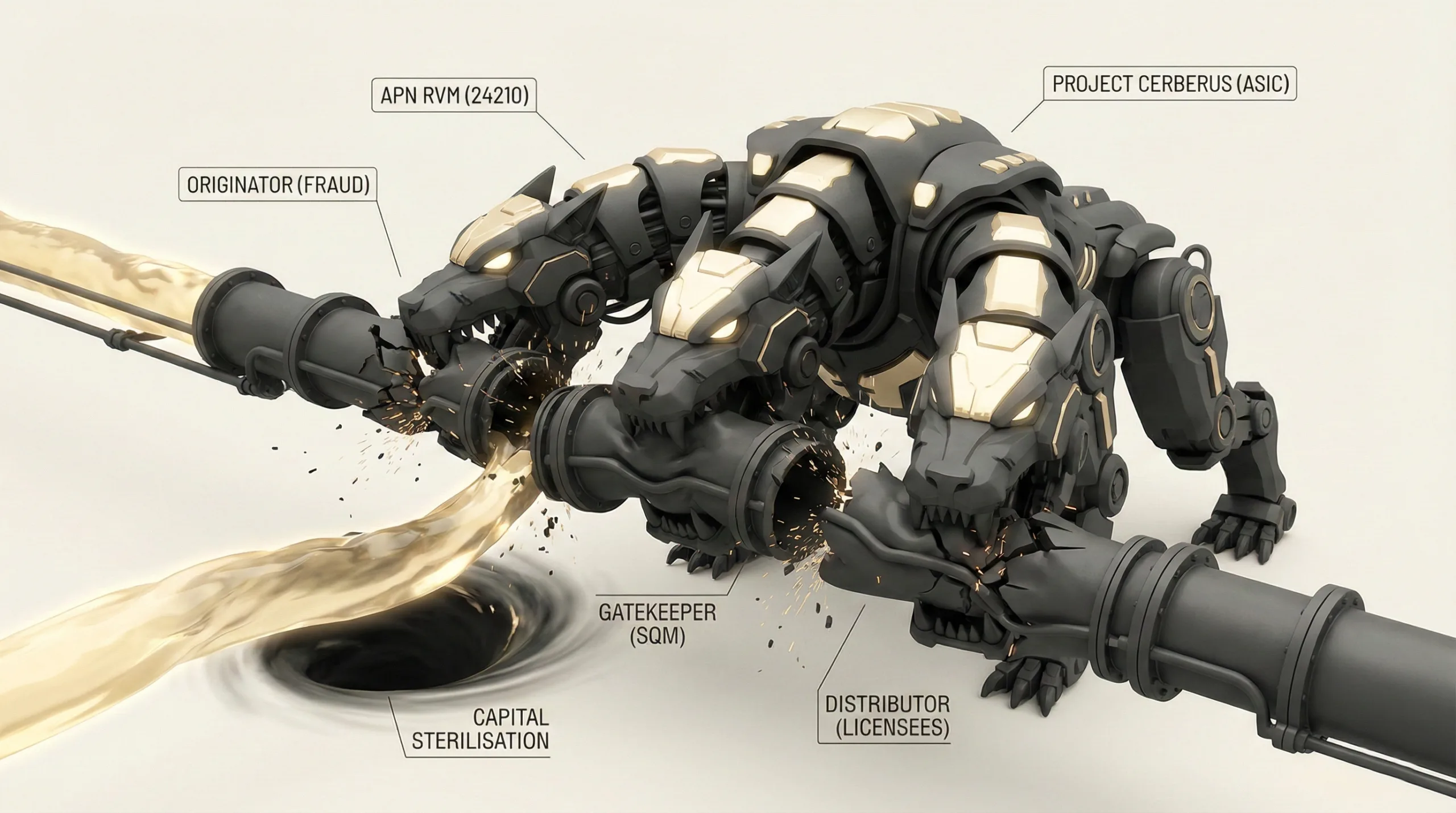

Quantifying Regulatory Intensity (APN Regulatory Velocity Multiplier™): The simultaneous, vertically integrated legal actions against an originator (Young), validator (SQM), and distributor (InterPrac) represent a material spike in the APN Regulatory Velocity Multiplier™ (APN RVM™). This multi-pronged approach moves beyond prosecuting a single entity to applying regulatory pressure to the entire ecosystem, creating a compounding deterrent effect that constrains capital flow at multiple points.

Regulatory Focus on Market Opacity (APN Risk & Compliance Index™ (24200)): The campaign’s dual focus on ‘shadow directors’ who fabricate assets and ‘gatekeepers’ who fail to verify them is the operational core of the APN Risk & Compliance Index™ (24200) framework. ASIC is addressing the systemic vulnerability that allows opaque structures to manufacture value and distribute unquantified risk to retail and superannuation investors, making it clear that opacity itself is now a primary regulatory focus.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of ASIC media releases and legal filings from November 2025. The key facts are:

- The Origination Fraud: On 21 November 2025, ASIC announced criminal charges against Mr. Brent Young, a Queensland-based ‘shadow director’. He is alleged to have orchestrated an $8.3 million debt factoring fraud by fabricating over 10,000 invoices to Bunnings Warehouse, a company with which he had no commercial relationship.

- The Gatekeeper Litigation: On 13 November 2025, ASIC initiated civil penalty proceedings against research house SQM Research. The regulator alleges SQM issued misleading ‘Favourable’ ratings on the contracted Shield Master Fund by failing to verify information and understating the fund’s material concentration in high-risk, related-party loans.

- The Distributor Liability: In parallel, ASIC sued financial planning licensees InterPrac Financial Planning and MWL Financial Services. They are accused of failing to conduct their own independent due diligence, instead relying on SQM’s research without independent verification and directing approximately $677 million of client superannuation savings into the structurally adverse funds.

- The Strategic Codification: ASIC’s 2026 Enforcement Priorities, released in November 2025, formalised the campaign by explicitly naming ‘Poor Private Credit Practices’ and ‘Holding those responsible to account for the contraction of the Shield and First Guardian Master Funds’ as top-tier priorities, signalling a sustained, long-term focus.

Critical Analysis & Balanced View

A primary insight from this campaign is the systematic elimination of ‘plausible deniability’ as a defence for market participants. ASIC has simultaneously closed the loopholes for every actor in the chain: the shadow director cannot hide behind the corporate veil; the research house cannot blame the issuer for providing faulty data; and the licensee cannot blame the research house for a flawed rating. This ‘no-excuses’ doctrine fundamentally raises the bar for professional conduct and operational diligence.

The SQM litigation, in particular, is a structurally significant test case for the investment research industry. If ASIC succeeds in establishing that a research house has a duty to forensically verify issuer-supplied data, it could render the current business model for rating complex, multi-asset funds economically unviable. The cost of such in-depth analysis would likely exceed the fees researchers can charge, potentially leading to a ‘ratings withdrawal’ from the sector.

While this regulatory action is necessary to address market integrity, the consequent constraint on market activity poses a significant risk. A material contraction in private credit availability could constrain legitimate, well-governed property developments and businesses of essential capital, potentially stifling economic activity. The challenge for the market will be to adapt to the new, higher standards without introducing material operational friction.

Strategic Implications for Property Professionals

- For Developers: Immediately stress-test your funding pipeline. Any reliance on private credit or non-bank lenders with opaque structures is now an elevated vulnerability. You must diversify your capital sources, prepare for significantly heightened due diligence from all financiers, and ensure your own governance and reporting can withstand forensic scrutiny.

- For Lenders & Financiers: Your due diligence framework is now subject to regulatory scrutiny. Reliance on third-party ratings or issuer-supplied data is now considered insufficient. You must invest in capabilities to verify not just the credit risk but the ‘existence risk’ of underlying assets, particularly in complex structures like debt factoring and related-party loans.

- For Valuers & Consultants: The liability for professional ‘opinion’ has been applied as a regulatory instrument. Your reports and assessments will be treated as critical validation services carrying significant legal weight. Ensure your disclaimers are robust, but more importantly, ensure your verification processes can withstand regulatory scrutiny. The ‘we relied on the information provided’ defence is no longer viable.

- For Financial Planners & Licensees: The practice of adopting external research for Approved Product Lists (APLs) without independent verification is now a direct source of litigation risk. The duty to perform independent due diligence is non-delegable. You must immediately review and remove from your APLs any product where you cannot independently verify the underlying assets, strategy, and governance structure.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis provides kinetic validation for the APN Risk & Compliance Index™ (24200) framework, confirming the thesis that regulatory bodies will use coordinated, multi-pronged enforcement to materially constrain high-risk market segments and protect the integrity of the broader financial system.

- Index Calibration (APN RVM™ 24210): The APN Regulatory Velocity Multiplier™ is calibrated to register a ‘maximum intensity spike’ for November 2025. The model is updated to assign a higher weighting to vertically integrated enforcement actions (targeting originators, validators, and distributors simultaneously) over isolated prosecutions, reflecting their greater systemic impact.

- Data Capture: This event triggers a new data capture mandate for the APN Risk & Compliance Index™ (24200) to systematically track civil penalty proceedings against ‘gatekeeper’ entities (research houses, auditors, valuers) as a leading indicator of a systemic de-rating of risk within a specific asset class.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.