The Land Lease ‘Super-Margin’: How Regulatory Structural Adjustments are Closing the Arbitrage Window

APN ANALYSIS: A-251208-AUS131756

Executive Summary

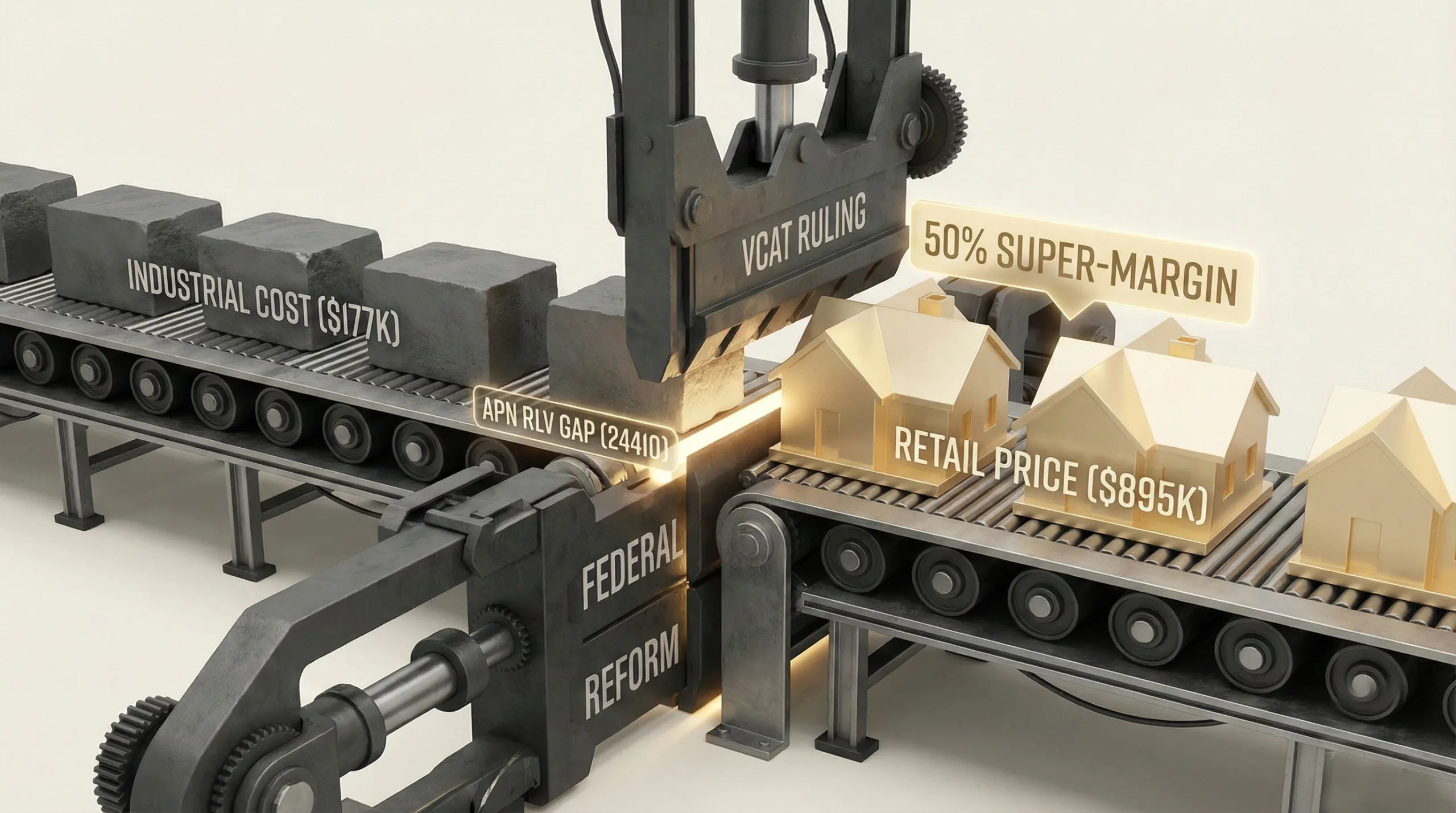

The Australian Land Lease Community (LLC) sector is experiencing a significant, but transient, ‘Super-Margin’ arbitrage event. APN analysis confirms development margins are reaching approximately 50%, a figure materially higher than the 15-20% typical for standard residential projects. This profitability stems from a structural dislocation: operators are developing sites at a wholesale industrial cost base (around $177,000 per ‘pad’) but are achieving retail sales prices of up to $895,000, effectively capturing residential land value appreciation without selling the freehold title.

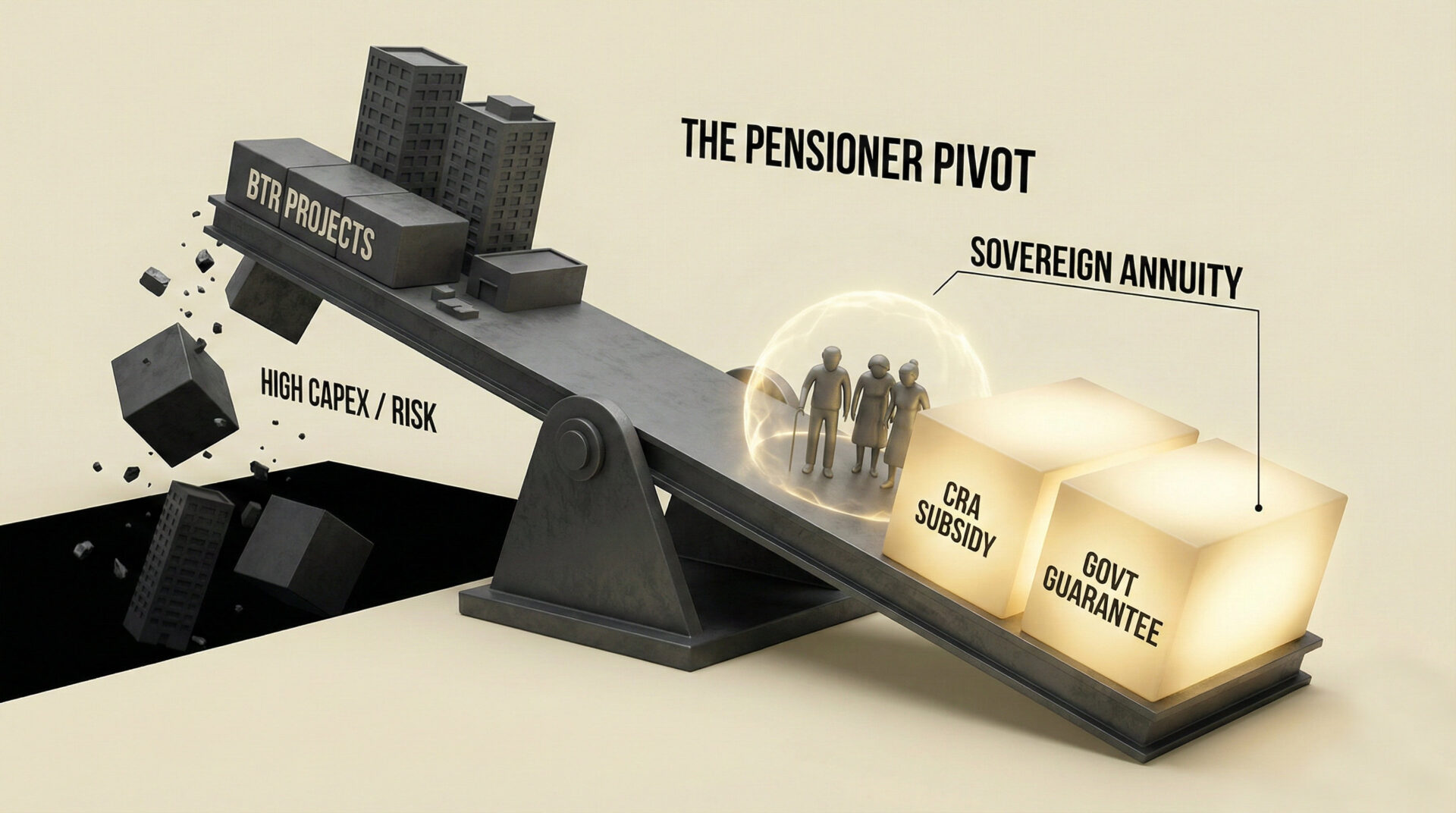

This highly lucrative arbitrage window is now closing with notable speed, subject to converging legal and regulatory interventions. The July 2025 Victorian Civil and Administrative Tribunal (VCAT) ‘Woodward’ ruling has voided the sector’s long-term annuity model by invalidating Deferred Management Fees (DMFs). Simultaneously, impending Federal ‘Support at Home’ reforms present a structural risk to the affordability narrative by creating a ‘Pensioner Trap’ and placing substantive Commonwealth Rent Assistance subsidies at risk. For property professionals, this signals a fundamental shift in the asset class, from a stable, annuity-based investment to a high-risk, high-return development play. The key risk is no longer market demand, but the velocity of sovereign and legal intervention.

Background & Strategic Context

This event validates and calibrates APN’s core macro-thesis, APN Sovereign Policy Composite Index™ (SPCI, 24800), which posits that state-level intervention is the dominant force shaping property market outcomes. The LLC sector’s ‘Super-Margin’ was created by a specific regulatory arbitrage, and its potential contraction is being driven by direct legal (VCAT) and legislative (Federal Government) actions, demonstrating the power of the state to both create and structurally degrade value structures.

The Regulatory Arbitrage (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The LLC ‘Super-Margin’ is a direct consequence of a regulatory framework that allows an industrial product (a manufactured home on leased land) to be sold at a retail residential price point, while benefiting from ‘affordable housing’ subsidies like Commonwealth Rent Assistance.

The Liquidity Paradox (APN Agora™): The elevated volume of institutional capital, exemplified by Macquarie’s $2.9 billion fund, into a sector with deteriorating fundamentals appears paradoxical. However, it reflects a strategic race to capture the peak development margin, validating the high liquidity and amenity value (APN Agora™) of these communities as a desirable product, even as the underlying financial model structurally deteriorates.

The Enforcement Shock (APN Regulatory Velocity Multiplier™): The VCAT ‘Woodward’ ruling represents a high-velocity enforcement event (APN RVM™). It did not just amend a rule; it voided a core contractual clause ab initio, triggering immediate and material asset write-downs and forcing a fundamental strategic pivot across the entire sector, demonstrating the high impact of a single legal judgment.

The Subsidy Erosion: The sector’s reliance on Commonwealth Rent Assistance for residents illustrates a structural mechanism where government subsidies intended for individuals are captured as revenue by corporate operators. The increasing political scrutiny of subsidising residents in $895,000 ‘homes’ signals an elevated risk that this subsidy mechanism will be discontinued.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Q4 2025 market conditions in the Australian Land Lease Community sector, cross-referencing institutional cost reports, legal rulings, and listed company disclosures. The key facts are:

- The ‘Super-Margin’ Confirmed: Analysis confirms a gross development margin of approximately 49% on premium LLC products. This is derived from a verified ‘Dirt-to-Door’ cost of ~$600,000 (including a ~$177,000 pad cost) against a retail price of up to $895,000.

- The Cost Basis Established: The Colliers ‘Land Lease Community Cost Per Site Report 2025’ established a benchmark civil delivery cost of ~$127,000 per site, which aggregates to a total ‘Pad-Ready’ cost of ~$177,000 when including earthworks and infrastructure charges.

- The ‘Codex Structural Adjustment’ Event: In July 2025, the VCAT ruling in Dowling v Lifestyle Management 2 Pty Ltd declared Deferred Management Fees (DMFs) calculated on future values to be void and unenforceable in Victoria, materially undermining the sector’s long-term annuity revenue model.

- The Institutional Pivot: In response to the VCAT ruling, Lifestyle Communities (LIC) announced a ‘No Exit Fee’ contract option in November 2025, forcing a pivot from a subsidised entry price model to a higher upfront cost model to maintain profitability.

- Converging Federal Policy Pressures: Impending ‘Support at Home’ reforms (effective November 2025) and potential changes to Commonwealth Rent Assistance (CRA) present a risk to the sector’s affordability narrative by creating a ‘Pensioner Trap’ and risking the removal of subsidies for residents in high-value LLC homes.

- The Elevated Capital Inflow: Macquarie Asset Management has validated the sector’s high-yield potential by launching ‘Millbray’, a $2.9 billion vertically integrated platform aiming to deliver 5,000 LLC homes, signalling a shift towards industrialised development.

Critical Analysis & Balanced View

The central paradox is the simultaneous elevated volume of institutional capital and the deterioration of the sector’s regulatory foundations. This is not irrational. Macquarie’s entry is a calculated position that it can industrialise the development margin faster than regulators can close the subsidy arbitrage. By creating a vertically integrated platform, it aims to control costs from ‘dirt to door’ and capture the ~50% development profit, making it less reliant on the structurally sensitive, long-term DMF annuity stream that smaller operators depended on.

The ‘Woodward’ Structural Adjustment is more than a financial problem; it is a structurally adverse marketing outcome. The entire LLC value proposition was built on a ‘low entry price’ subsidised by the DMF. The forced pivot to a ‘No Exit Fee’ model, which necessitates a price increase of $100,000-$150,000, negates this key point of difference. It pushes the product from an ‘affordable downsizing solution’ into direct competition with freehold townhouses, a structural contest it may not win on a pure value-for-money basis, especially given the depreciating nature of the home asset.

The ‘Pensioner Trap’ is a counter-intuitive risk. While operators are focused on the VCAT ruling, the ‘Support at Home’ reforms may represent the more structurally consequential risk. By linking aged care costs to assessable assets (i.e., the cash released from downsizing), the reforms structurally disadvantage the very liquidity event that makes moving into an LLC attractive. The liquidity event promised by downsizing becomes a liability that increases future care costs, materially undermining the customer value proposition.

Strategic Implications for Property Professionals

- For Developers & Operators: The strategic priority is to pivot from financial engineering (DMFs) to manufacturing efficiency. Future market advantage will likely accrue to vertically integrated players who can control the entire supply chain and maximise the upfront development margin. Existing operators must immediately stress-test their portfolios against a ‘No DMF’ and ‘No CRA’ scenario and consider strategic asset sales or partnerships with larger, industrialised players.

- For Valuers & Financiers: Asset valuation models for LLCs now require fundamental reassessment. Valuations based on discounted cash flows from future DMFs must be written down, as evidenced by LIC’s $135.5 million impairment. The asset class must be re-categorised from a stable, annuity-style infrastructure asset to a higher-risk residential development play. Lending criteria must be tightened to account for regulatory velocity and the risk of subsidy withdrawal.

- For Agents & Buyers’ Agents: The ‘affordability’ narrative is no longer credible for premium LLC products. Professionals must advise clients on the ‘Pensioner Trap’ risk, where the cash realised from downsizing can negatively impact future aged care costs under the ‘Support at Home’ reforms. The key selling point shifts from ‘low entry cost’ to ‘lifestyle and amenity’, but this must be weighed against the lack of capital growth on the dwelling and the new, higher upfront prices.

- For Institutional Investors: The window for acquiring smaller, legacy operators reliant on the old DMF model is closing. The opportunity lies in funding or acquiring vertically integrated platforms like Macquarie’s Millbray that focus on capturing the development ‘Super-Margin’. Due diligence must now prioritise regulatory risk modelling and exposure to federal subsidies over traditional property metrics.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the core thesis of the APN Sovereign Policy Composite Index™ (SPCI, 24800), demonstrating that direct state-level legal (VCAT) and legislative (Federal) intervention is the primary driver of structural degradation of value in the LLC sector’s business model.

- Index Calibration (APN RVM™ 24210): The APN Regulatory Velocity Multiplier™ is calibrated to register the Dowling v Lifestyle Management ruling as a high-impact, high-velocity event. The multiplier for the Victorian residential tenancy tribunal will be increased to reflect its capacity to trigger sector-wide asset re-pricing from a single judgment.

- Index Calibration (APN Agora™ 24140): The continued high demand and premium pricing for LLCs, despite underlying financial model weaknesses, validates the high weighting of amenity and community within the APN Agora™ index. The index is calibrated to reflect that a strong amenity offering can temporarily sustain pricing power even when underlying financial structures are weak.

- Data Capture (APN Symbiotic Intelligence Network™ 24310): This briefing triggers a data capture mandate via the APN Symbiotic Intelligence Network™ to survey valuers and financiers on their revised risk weighting for LLC assets post-VCAT, directly feeding the APN Professional Sentiment Index™ (24300).

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.