Systemic Risk Evaluation: Structural Vulnerabilities within the $12.4 Trillion Equity Moat

APN EL: Level 5 – Source: APN CODEX: 21200 RISK MATRIX AUDIT – Subject: Multi-Nodal Convergence, Structural Rigidity, and the Economics of Synthetic Expansion

Note: In accordance with APN Cortex II Clean Room protocols, this analysis has been mathematically reframed to reflect structural and hierarchical aggregation pathways rather than speculative sentiment.

Executive Abstract

Current telemetry derived from the APN 21200 Risk Matrix indicates a profound structural realignment within the national housing sector. The $12.4 Trillion Equity Moat has decoupled from foundational economic capacity, transitioning into a phase of Synthetic Expansion. This sustained appreciation phase is not supported by organic income metrics or productivity, but is instead mathematically reliant upon systemic supply constraints and the rapid migration of speculative debt.

This systemic critique evaluates the interplay among holding-cost erosion, localised liquidity contractions, and capital momentum to assess the broader macroprudential risks currently embedded in the financial system.

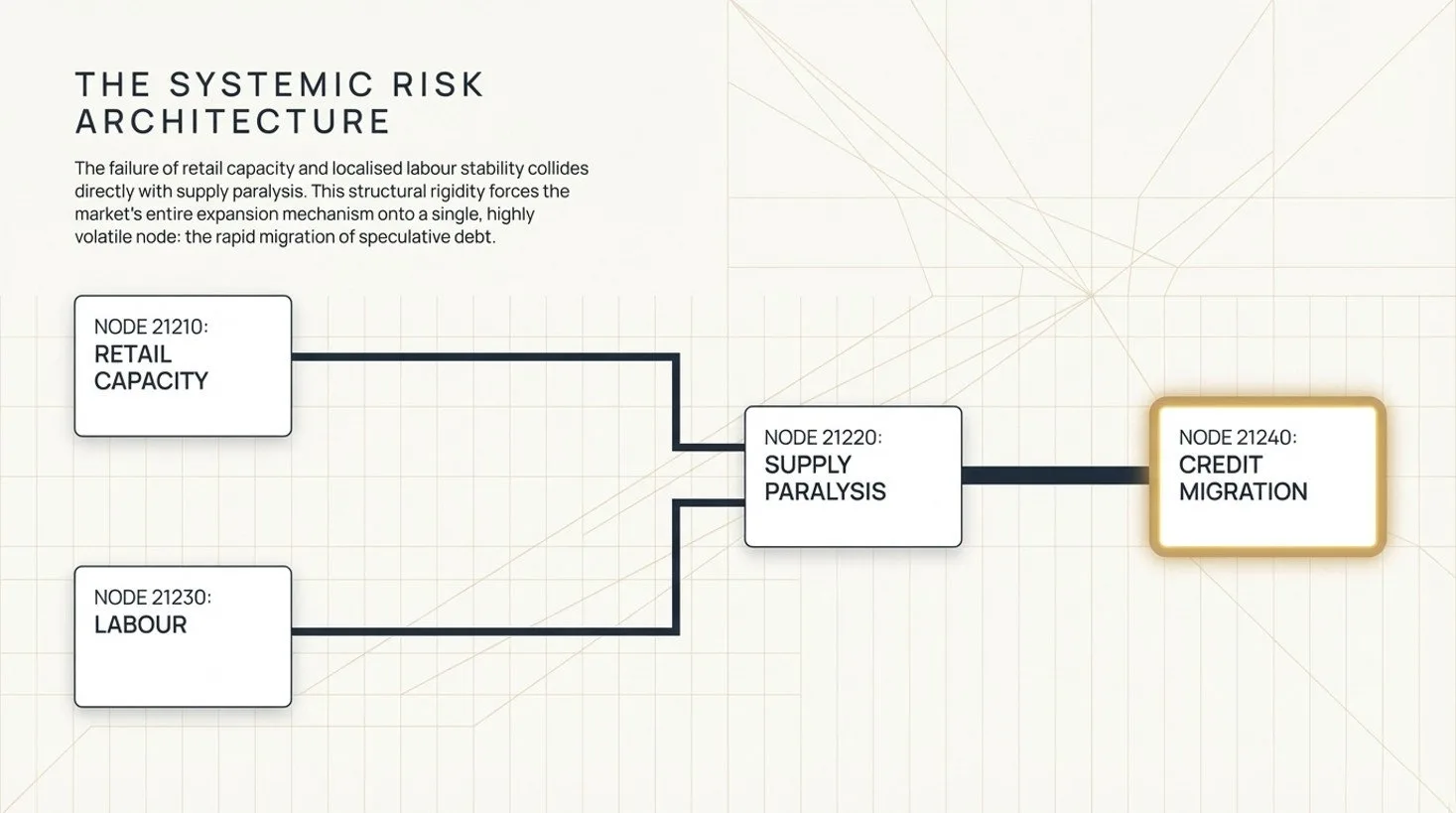

1. The Erosion of Macroeconomic Buffers and Policy Transmission

Evaluating Nodes 21210 & 21240 (Institutional Baselines)

The primary mechanism for organic market expansion—the capacity of retail participants to accrue and service new debt—is currently experiencing severe structural degradation. This presents a critical limitation to the efficacy of traditional monetary policy transmission.

- The Discretionary Inversion: Historically, the spread between Discretionary and Non-Discretionary spending growth operates at a mean of \(\mu = -53.51\) bps. Recent APN telemetry records a violent positive inversion, reaching \(+304.69\) bps (\(Z = +0.64\)). Non-discretionary CPI components (utilities, insurance, taxation) are rapidly depleting household capital buffers.

- Serviceability Capacity Limit (SCL) Breach: The prevailing 3.85% cash rate, combined with the mandatory 3% APRA buffer, has mathematically breached the SCL for median-income deciles.

Systemic Implication: The traditional asset accumulation trajectory for wage-earning demographics is structurally blocked. Because the standard credit risk models utilised by tier-one institutions rely on historical discretionary capacity that has now been fundamentally negated, current institutional risk weighting may be significantly under-calculating baseline portfolio vulnerability.

2. The Labour Paradox and Systemic Liquidity Contractions

Evaluating Node 21230 (Hyper-Localised Serviceability)

Macroeconomic indicators are currently projecting a false stabilisation regarding employment. The national unemployment baseline (\(\mu = 5.14%\)) is statistically insufficient for accurate macroprudential risk modelling, as it masks acute, concentrated downward variance at the micro-level.

The APN Labour Paradox Divisor (\(D_{paradox}\)) reveals multi-sigma negative deviations in critical SA4 regional corridors:

- Hobart (SA4 601): \(Z = -7.19\sigma\)

- Ballarat (SA4 201): \(Z = -3.19\sigma\)

- Sydney – Ryde (SA4 126): \(Z = -2.83\sigma\)

Systemic Implication: Regulators and risk directors must transition from national employment aggregates to SA4-level vulnerability indexing. The intersection of these extreme employment deviations with elevated holding costs creates highly concentrated zones of structural vulnerability. These specific corridors present a high mathematical probability of localised systemic liquidity contractions, which precede accelerated downward variance in underlying asset values.

3. Capital Misallocation and Structural Rigidity

Evaluating Node 21220 (Residual Land Value Constraints)

The market is currently demonstrating extreme structural rigidity, effectively neutralising the market’s organic ability to de-leverage via the delivery of new physical inventory.

- PPI Variance: The Producer Price Index (PPI) construction matrices report an extreme variance (\(\sigma = 25.43\)) against a historically elevated mean (\(\mu = 127.82\)).

- RLV Negation: Applying the APN Residual Land Value equation (\(RLV = GRV – [C_c + M_d + H_c]\)) demonstrates that the concurrent escalation of construction input costs (\(C_c\)) and capital holding costs (\(H_c\)) has functionally negated required developer margins (\(M_d\)).

Systemic Implication: The inability to achieve mathematical viability on physical supply delivery guarantees sustained artificial scarcity. For economic policymakers, this represents a severe capital misallocation dilemma: investment capital is being absorbed by the appreciation of existing, non-productive assets due to supply paralysis, rather than being deployed into new housing infrastructure or broader economic productivity.

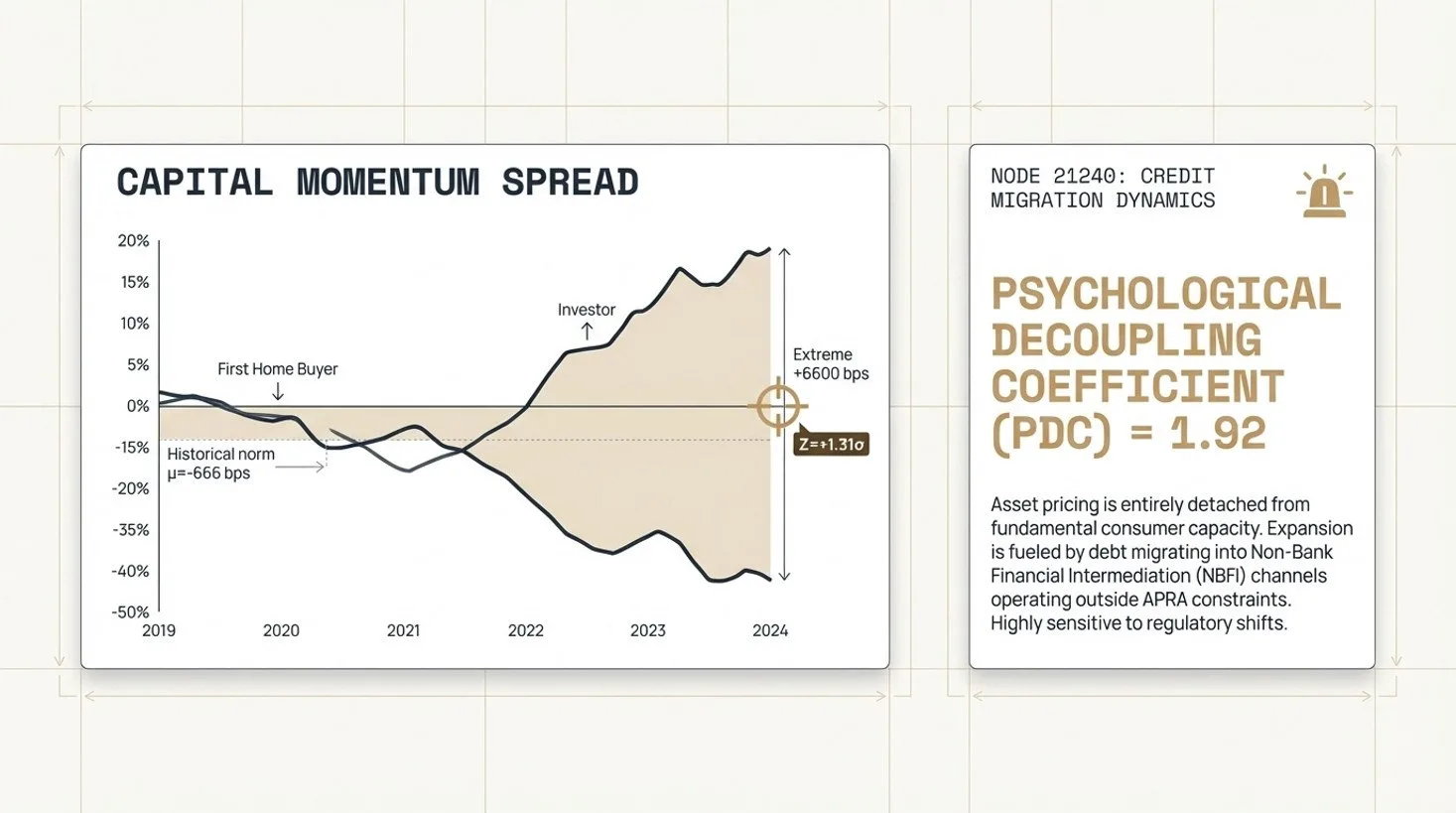

4. Credit Migration and the Psychological Decoupling Coefficient

Evaluating Node 21240 (Capital Momentum)

Given the structural degradation of retail capacity (Node 21210) and the paralysis of supply channels (Node 21220), the continued expansion of the Equity Moat is mathematically dependent on the rapid deployment of existing leverage.

- Capital Momentum Spread: The spread between Investor and First Home Buyer YoY growth has experienced a multi-nodal convergence, diverging from a historical norm of \(\mu = -666\) bps to an extreme \(+6600\) bps (\(Z = +1.31\sigma\)).

- The PDC Metric: The Psychological Decoupling Coefficient (PDC) has formalised at 1.92.

Systemic Implication: Asset pricing is now entirely detached from fundamental consumer capacity (\(S_{base}\)). This Synthetic Expansion is being fuelled predominantly by the migration of debt into Non-Bank Financial Intermediation (NBFI) channels, which operate outside traditional APRA constraints. A PDC of 1.92 denotes a high-risk node; the market is highly sensitive to regulatory shifts in NBFI compliance and taxation structures, carrying an elevated risk of a coordinated systemic shift if capital momentum is disrupted.

Macroprudential Policy Recommendations

The $12.4 Trillion Equity Moat is operating with profound structural vulnerability. To mitigate the probability of severe, cascading systemic liquidity contractions, macroprudential regulators should consider:

- Targeted NBFI Regulation: Instituting stricter capital controls on Non-Bank Financial Intermediation channels, driving the current speculative debt migration.

- SA4-Weighted Capital Buffers: Requiring institutions to adjust their capital reserve buffers based on localised \(D_{paradox}\) metrics rather than national macro-stability baselines.

- Redefining Serviceability: Updating the standard SCL to accurately reflect the permanent upward shift in non-discretionary CPI components relative to stagnant real wage growth.

Disclaimer: APN Cortex II Alpha Testing

The analysis and information contained in this deconstruction are the result of APN Cortex II alpha testing. They are provided for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice.

The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor. This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness.

Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events. All frameworks (Codex 21200–24800) and the APN Cortex II architecture are proprietary to APN.

Property values and market conditions are subject to structural variance. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.