The Volatility Delta Brief: Q1 2026 Systemic Risk Assessment

APN EL: Level 5 Source: APN Codex 21200: Deterministic Delta-Analysis of the Aggregate Macro-Volatility Index Subject: Systemic Risk Evaluation of the Tripartite Exogenous Macro-Shock

Note: In accordance with APN Clean Room protocols, this analysis has been mathematically reframed to reflect structural and hierarchical aggregation pathways rather than speculative sentiment. All forward-looking risk modelling and econometric forecasting contained herein rely entirely on deterministic delta analysis.

1. Executive Abstract: Structural Drift and Non-Linear Volatility

The research paper provides an extended econometric evaluation of the APN Aggregate Macro-Volatility Index (Codex Node 21200), functioning as the definitive metric for systemic risk and liquidity friction across the Australian Residential Ecosystem. Recent audits (as of 17 March 2026) have quantified the contagion generated by a profound tripartite exogenous shock, rendering historical baseline assumptions functionally obsolete.

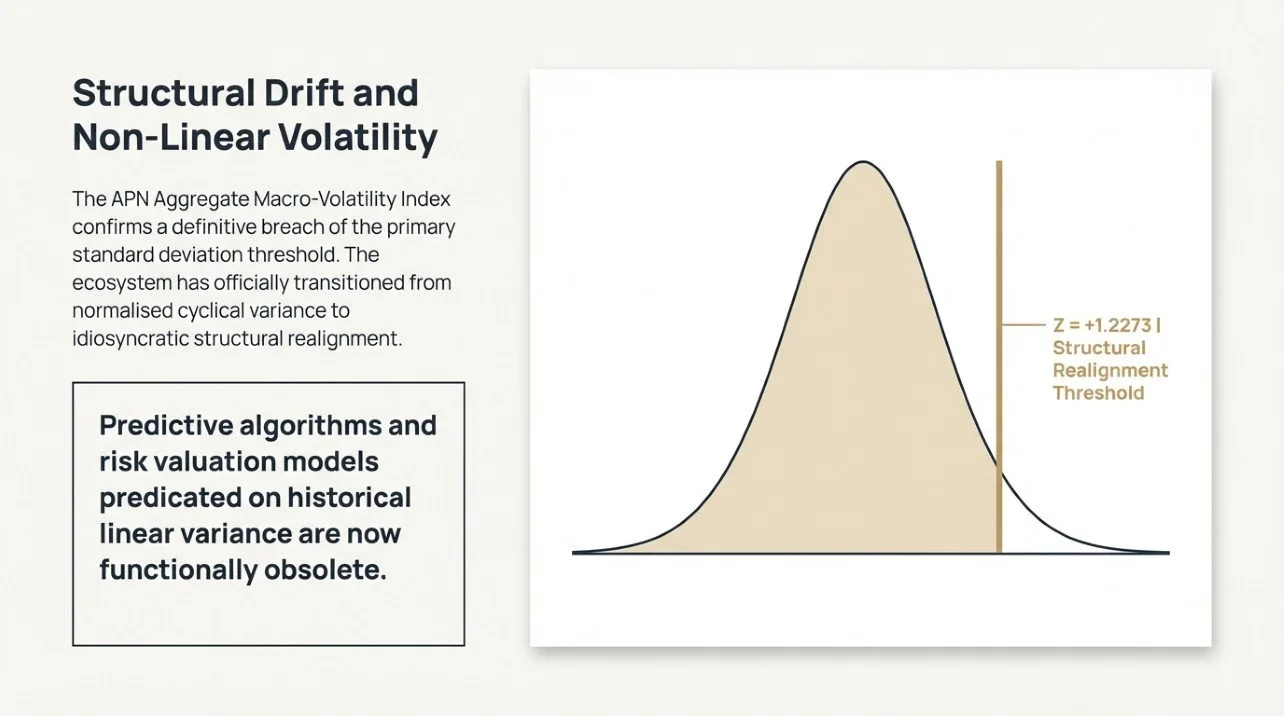

The Aggregate Macro-Volatility Index has registered a definitive structural drift, recording an aggregate Z-score of \( Z = +1.2273 \). This designates a deviation of 1.23 standard deviations (\( \sigma \)) from the fifteen-year historical baseline, signalling a pivot toward acute systemic instability. Breaching the primary standard deviation threshold indicates that the ecosystem has transitioned from normalised cyclical variance to idiosyncratic structural realignment.

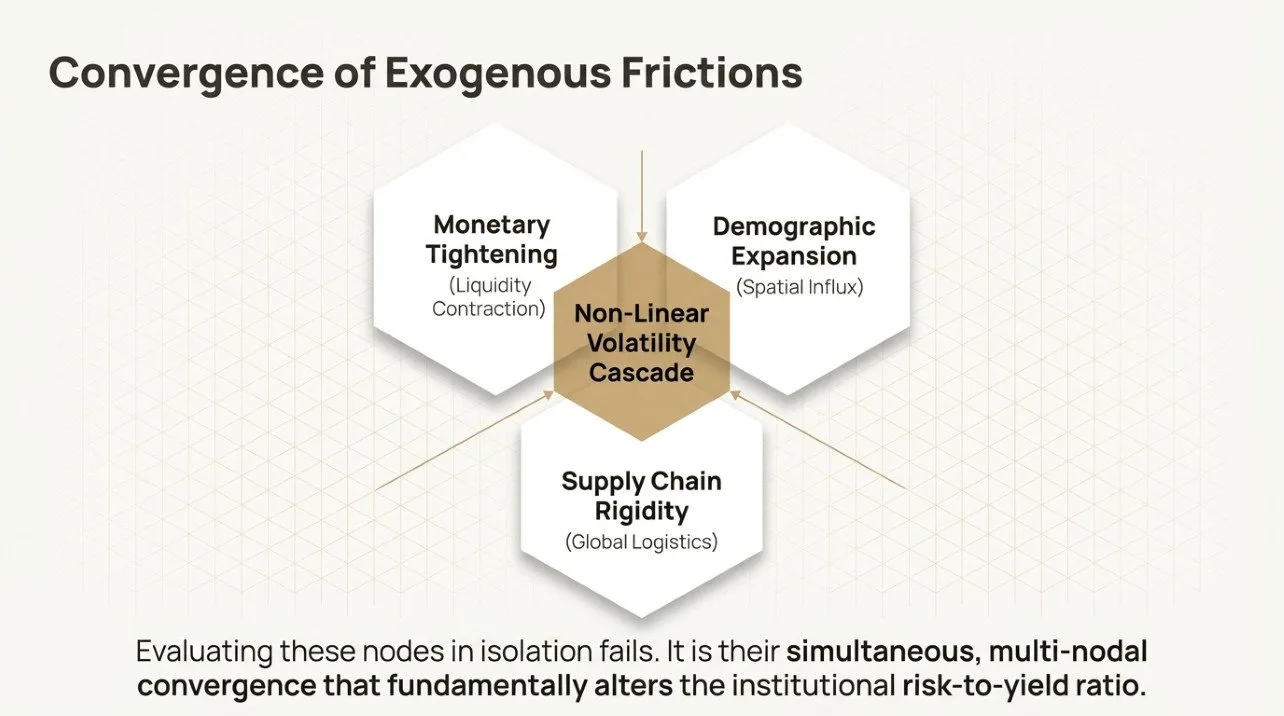

Consequently, predictive algorithms and risk valuation models predicated on historical linear variance must be immediately recalibrated. The simultaneous injection of three compounding variables—monetary tightening, demographic expansion, and supply chain contraction—has created a non-linear volatility cascade that fundamentally alters the risk-to-yield ratio for institutional capital allocation.

2. Deconstruction of the Tripartite Exogenous Shock

The current systemic vulnerability is not the result of a singular policy failure, but rather the simultaneous multi-nodal convergence of three distinct macroeconomic frictions. Evaluating these nodes in isolation fails to capture their compounding nature.

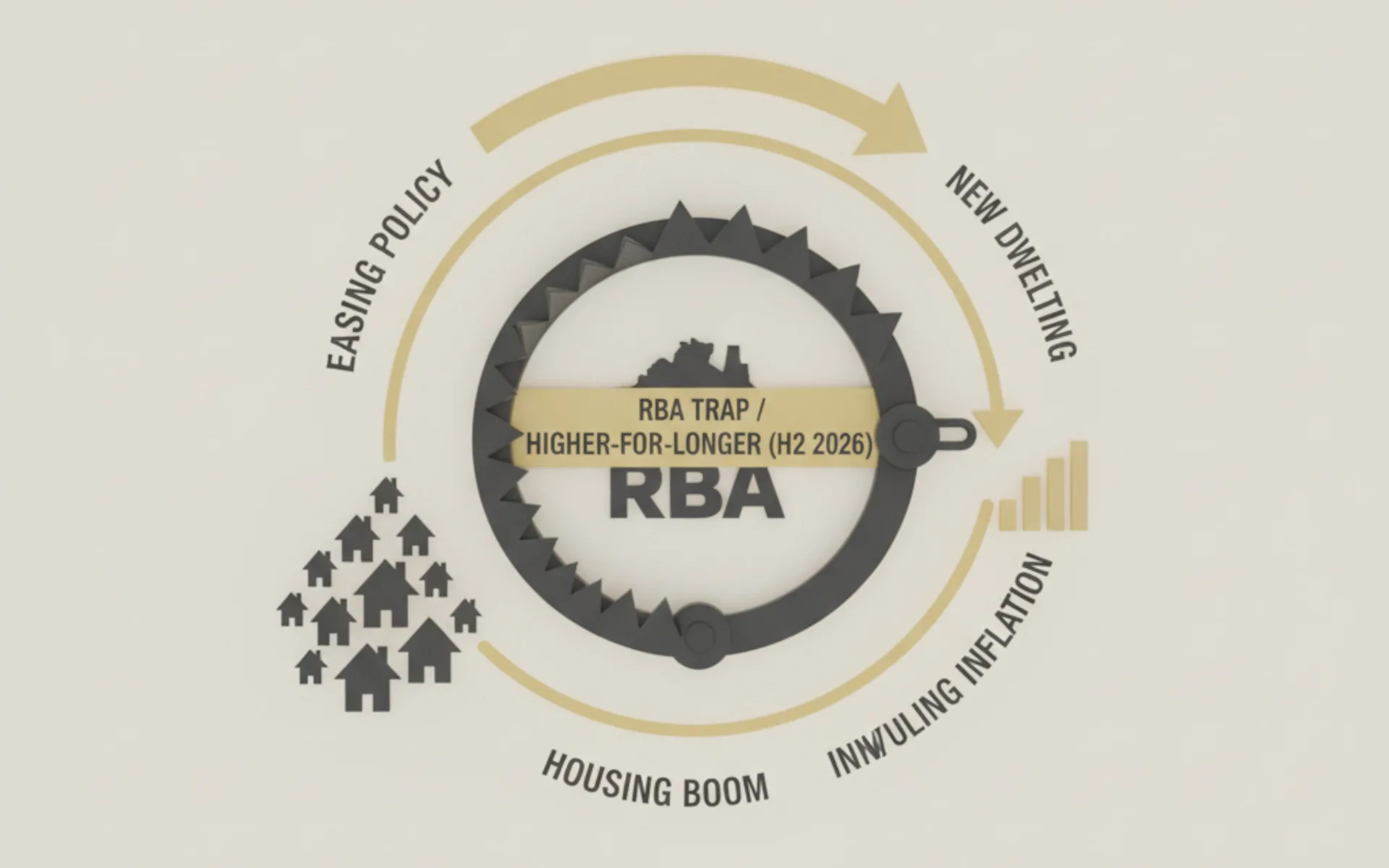

2.1. Monetary Policy Friction: Accelerated Liquidity Contraction and Serviceability Erosion

The primary variable in this deterministic delta-analysis is the acute monetary policy friction introduced by the Reserve Bank of Australia’s (RBA) Official Cash Rate (OCR) hike to 4.10% on 17 March 2026. This upward adjustment has initiated a systemic liquidity contraction across the retail lending tier, which is now transmitting into institutional funding constraints.

For macroeconomic forecasters, the immediate concern is the velocity of the asset-wage decoupling. The increased debt-servicing burden is structurally eroding aggregate purchasing power across lower- and middle-income quartiles, accelerating the decline in accessible capital for asset acquisition and retention. Furthermore, the erosion of APRA-mandated serviceability buffers makes existing highly leveraged cohorts uniquely vulnerable to negative equity transitions. As net interest margins compress and borrowing capacity contracts by an estimated 25-30% relative to the prior cyclical peak, overall market liquidity will continue its sustained depreciation phase.

2.2. Demographic and Population Influx: Spatial Concentration and Structural Rigidity

Compounding the monetary liquidity contraction is a severe population shock driven by a rapid influx of net overseas migration. In traditional linear economic models, population expansion is interpreted as an intrinsic buffer against asset devaluation. However, within the current capital-constrained environment, this influx acts as an acute systemic stressor on inherently inelastic housing supply.

Integration with APN Codex Node 21400 (Demographic Analysis) reveals intense spatial concentration of this new demand, heavily localised in primary metropolitan corridors. The resulting friction manifests as severe tightening in the rental market, pushing yields upward while underlying capital values face downward pressure due to the liquidity constraints detailed in Section 2.1. This dichotomy distorts the fundamental asset accumulation trajectory. It creates a rigid framework in which demand cannot be met by new supply due to capital constraints, thereby forcing higher density ratios and complicating traditional demand-side sovereign policy interventions.

2.3. Supply Chain Disruption: Global Logistics Friction and Pipeline Stagnation

The third compounding variable is the transmission of geopolitical friction—specifically, prevailing security complexities in the Middle East—into the domestic construction pipeline. Disruptions to global logistics networks have sharply elevated maritime freight rates, as evidenced by an immediate 8.4% increase in the Drewry World Container Index (WCI).

When hierarchically aggregated into domestic modelling (Codex Node 21260: Construction Costs & Supply Chain), this global friction translates directly into severe localised material shortages. Concurrent analysis of Codex Node 21530 (Developer Sentiment & Capacity) indicates a synchronised contraction in new project commencements. The construction sector is fundamentally unable to elastically respond to the demographic influx (Section 2.2). Elevated baseline capital costs (Section 2.1), combined with escalated material procurement expenditures, are rendering large-scale, high-density development financially unviable in the immediate term, thereby solidifying the structural vulnerability of the national supply pipeline.

3. Systemic Risk Management and Forecasting Implications

For Chief Investment Officers, fund managers, and macroeconomic regulators, the convergence of these three nodes (Monetary Tightening + Demographic Influx + Supply Chain Rigidity) renders linear forecasting methodologies invalid. The aggregate data mathematically guarantees that the Australian Residential Ecosystem has entered a sustained phase of structural realignment.

3.1 Algorithmic Recalibration Directives

The \( Z = +1.2273 \) volatility reading mandates an immediate adjustment to proprietary Automated Valuation Models (AVMs). Algorithmic weightings must shift away from historical median pricing trends and place a heavy discount on assets exposed to high-leverage retail cohorts. Predictive architecture must now incorporate localised supply pipeline deficit ratios (Node 21500) and vulnerability to sustained terminal cash rates of 4.10% or higher.

3.2 Defensive Capital Allocation Strategies

Systemic risk is currently heavily skewed toward the downside for highly leveraged retail assets, while simultaneously presenting acute supply-side inflationary pressures in the rental node. Institutional strategy must urgently pivot toward defensive capital allocation.

Recommendations for structural realignment include:

- Stress-Testing Portfolios: Executing definitive liquidity stress tests against residential mortgage-backed securities (RMBS) and development funding lines, calculating for prolonged settlement defaults.

- Yield Protection: Reallocating institutional capital toward high-density, high-yield operational assets (e.g., Build-to-Rent) that directly benefit from demographic inelasticity, thereby converting a systemic stressor into a protected yield generation mechanism.

- Risk Auditing: Liquidating exposure to mid-tier development pipelines reliant on complex global supply chains, mitigating the compounding geopolitical friction outlined in Section 2.3.

APN INSTITUTIONAL DISCLAIMER:

The data, econometric models, and analysis contained within this document are strictly for internal institutional testing, benchmarking, and policy evaluation purposes. It does not constitute personal financial advice. Please consult a qualified financial adviser before making any investment or capital allocation decisions based on this macroeconomic data.