RBA Policy Inflection: Wealth Funnel Failure Forces End to Easing Cycle Amid Stagflation Risk

APN ANALYSIS: A-251106-AUS56

Executive Summary

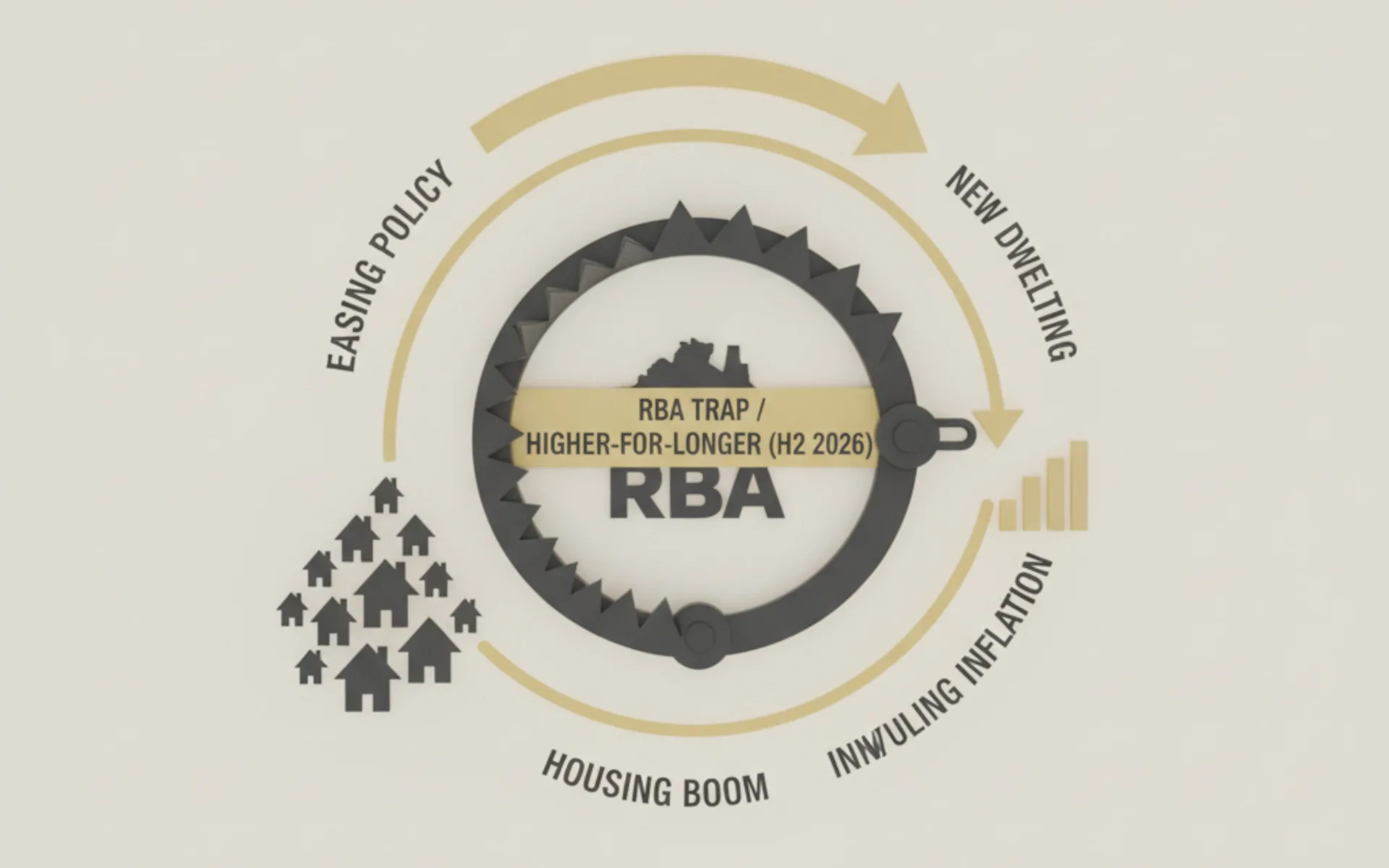

The Reserve Bank of Australia’s (RBA) November 4, 2025, hold at 3.60% is a forced policy inflection that terminates the 2025 easing cycle. The pivot was compelled by an admission that underlying inflation (3.0%) was “materially higher than expected,” confirming the RBA’s own rate cuts were causing rising housing and construction costs.

This admission is a direct validation of The Wealth Funnel thesis. The RBA’s policy has been exposed as a domestic driver of the inflation it is fighting, locking in a “higher-for-longer” rate environment and triggering a “Stagflation Risk” that will cripple new housing supply.

Background & Strategic Context

This forced policy pivot has validated our core thesis on asset inflation and has profound implications for the market, which are best understood through our core intelligence frameworks:

Wealth Funnel Mechanism Validation (The Wealth Funnel): This is a definitive validation of The Wealth Funnel. The RBA’s own statement provides the explicit causal chain: RBA easing ~ stronger housing market ~ rising construction costs ~ persistent inflation. This confirms that monetary policy is a primary domestic driver of the asset inflation that benefits incumbents at the expense of broader economic stability.

Stagflation Trap (APN Future Development Pipeline Index™ (24400)): This pivot creates a structural “Stagflation Trap” for the APN Future Development Pipeline Index™ (24400). The high construction costs, stimulated by the failed easing cycle, make new development challenging. This leads to persistent housing undersupply, which in turn feeds housing-related inflation, thereby preventing the future rate cuts needed to restore developer feasibility.

Negative Sentiment (APN Professional Sentiment Index™ (24300)): The negative inflection is quantified by developer-focused peak bodies, which confirm “project feasibility remains challenging.” This “subdued developer sentiment” is a direct negative vector into the APN Professional Sentiment Index™ (24300), which is now expected to be structural and protracted, not a short-term reaction.

Deconstruction of the Source Event

This deconstruction is based on an internal APN intelligence briefing. The key facts are:

- The Reserve Bank of Australia (RBA) terminated the 2025 easing cycle on November 4, 2025, holding the cash rate at 3.60%.

- The decision was forced by underlying (trimmed mean) inflation reaching 3.0% over the year, breaching the 2-3% target band.

- The RBA explicitly admitted that its “recent interest rate reductions are having an effect” on the housing market, causing “Housing prices are rising” and “dwelling construction costs… to increase again”.

- The market immediately “wiped out market hopes of a 2025 rate cut,” and the RBA Governor confirmed the Board “Did not consider cutting rates.”

- This inflection introduced the “risk of another hike” if price pressures worsen.

Critical Analysis & Balanced View

The “real” story here is the “Forced Policy Admission.” The 3.0% underlying inflation print was a decisive, documented failure of the RBA’s 2025 forecast guidance, compelling a non-discretionary policy pivot to prioritise its inflation mandate.

- Terminal Rate Re-evaluation: The unanimous pivot by major bank economists and the Governor’s verbal guidance signals that 3.60% is now the new terminal cash rate for the cycle. This invalidates all developer funding models that were predicated on a lower floor.

- Contradictory Mandate Risk: The RBA is trapped in a policy conflict. Any future rate cut needed to alleviate developer feasibility challenges will directly re-accelerate inflation via the validated “Wealth Funnel” mechanism, ensuring continued volatility.

- Structural Inflationary Channel: The persistent high costs of rents and new home construction are now entrenched as a structural inflationary channel, guaranteeing high underlying inflation for the next year.

Balanced View: On the surface, this is a central bank holding rates steady. However, the analysis reveals it as a forced admission that the RBA’s 2025 easing cycle was a policy failure. By stimulating asset prices, the RBA’s own actions have become a primary driver of the inflation it is now forced to fight, validating The Wealth Funnel and locking in a “higher-for-longer” rate environment that threatens to create stagflation for the development sector.

Strategic Implications for Property Professionals

- For Developers & Lenders: You must immediately reassess project feasibility against a terminal cash rate of 3.60% or higher. The market consensus on further easing has collapsed, and the “risk of another hike” must now be included in high-risk financial modelling.

- For Risk & Sentiment Analysts: The negative sentiment impacting developer confidence (Codex 24300) must be treated as structural and protracted, not a short-term reaction. The “Stagflation Risk” is now the primary negative driver for the APN Future Development Pipeline Index™ (24400).

- For Investors: The persistent high costs of rents and new home construction are now entrenched as a structural inflationary channel. This further solidifies the investment case for existing assets, as the “higher-for-longer” rate environment will cripple the delivery of new, competing supply.

- For Government & Policy: The RBA is trapped in a policy conflict. Any future rate cut to support the housing supply mandate will directly re-accelerate inflation. This confirms that monetary policy cannot solve the supply crisis and places the burden squarely on supply-side reform.

Disclaimer

The analysis and information contained in this analysis are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on internal APN intelligence, data, and information believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events. Property values and market conditions can go down as well as up.

Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.