Monetary Policy Fractures High-Density Feasibility, Rendering National Housing Accord Mathematically Unachievable

APN ANALYSIS: A-260321-AUS138416

Executive Summary

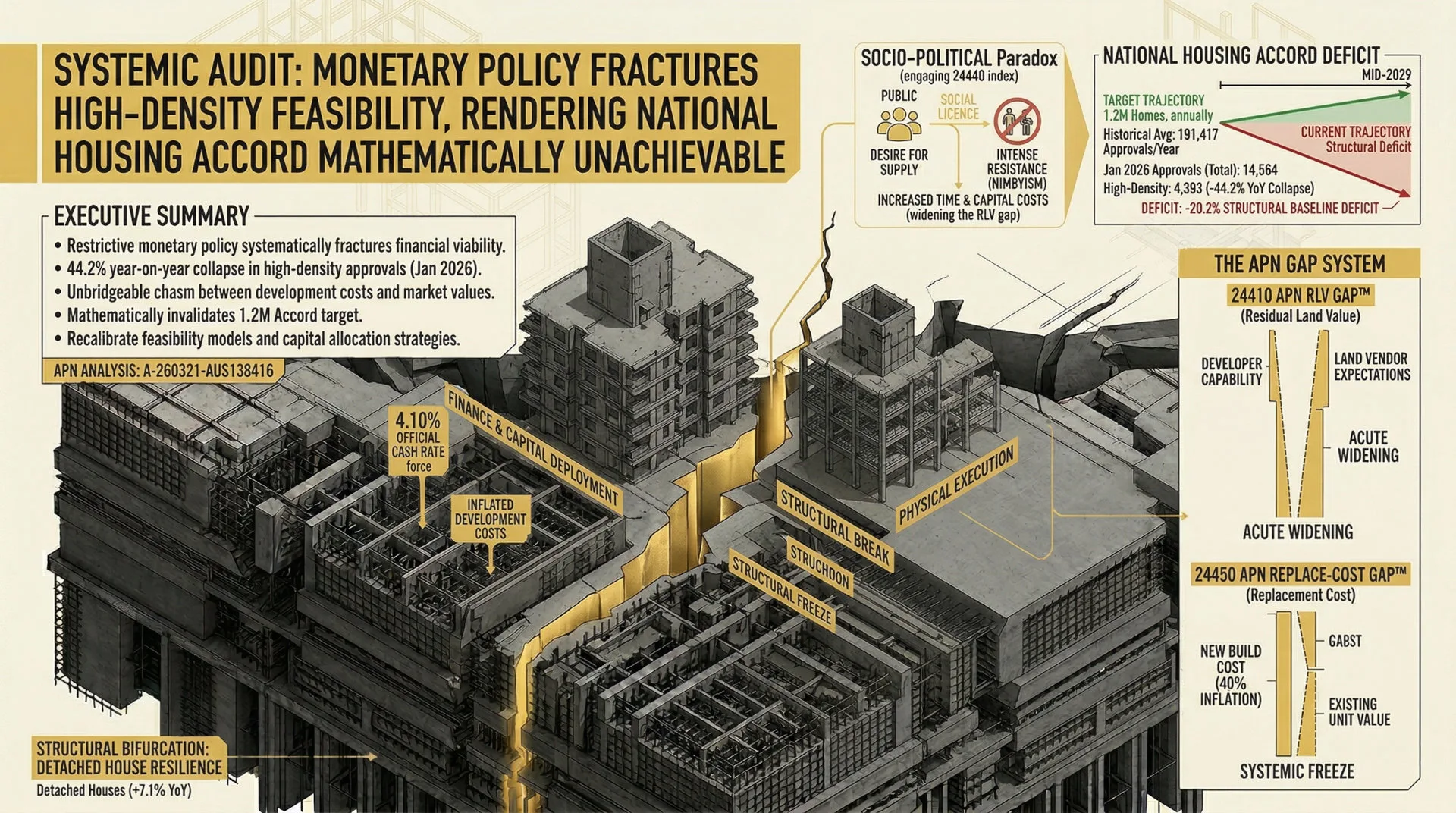

Restrictive monetary policy, anchored by the 4.10% official cash rate, has systematically fractured the financial viability of high-density residential construction across Australia. The resulting 44.2% year-on-year collapse in approvals for private-sector dwellings, excluding houses, is not a cyclical downturn but a structural break, driven by an unbridgeable chasm between inflated development costs and achievable end-market values. This mathematical impasse invalidates the operational assumptions of sovereign housing targets, rendering the National Housing Accord’s ambition to deliver 1.2 million new homes by mid-2029 unachievable under the current economic trajectory.

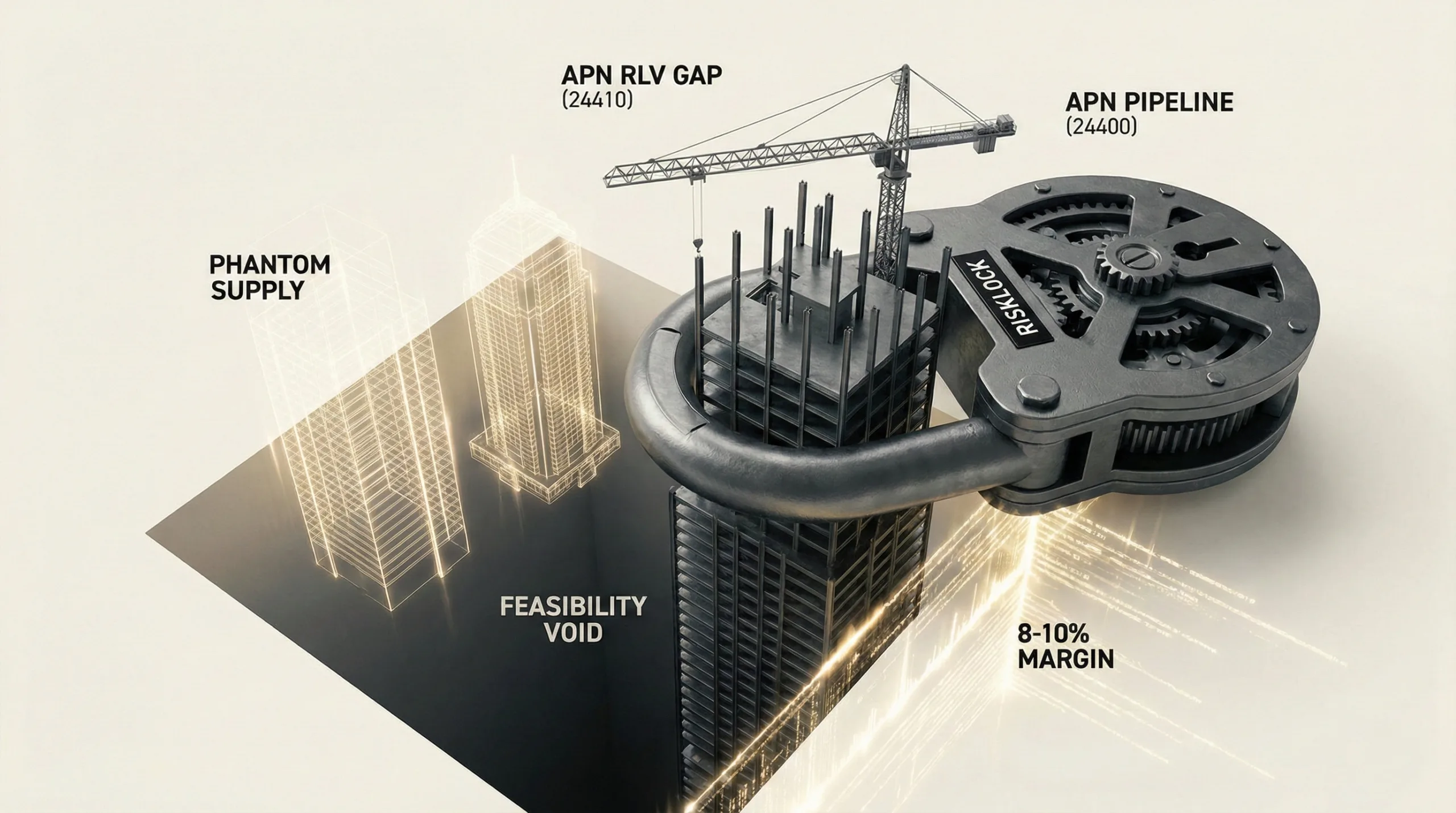

For property professionals, this environment demands a fundamental recalibration of feasibility models and capital allocation strategies. The acute widening of the 24410 APN Residual Land Value (RLV) Gap™ and the 24450 APN Replacement Cost Gap™ signals a systemic freeze in the high-density development pipeline. Strategic focus must pivot towards assets with lower cost structures and shorter delivery timelines, or capital must be held in reserve until a material correction occurs in either foundational interest rates, construction costs, or land vendor price expectations.

Background & Strategic Context

This analysis validates and calibrates the core APN macro-thesis that sovereign ambition is ultimately subordinate to mathematical and financial reality. The direct conflict between the Federal Government’s housing supply targets and the Reserve Bank’s monetary policy mandate creates a systemic friction that can only be resolved by a shift in one of the underlying variables. The current market paralysis is a direct outcome of these competing state-level interventions.

State Intervention as Primary Driver (APN Sovereign Policy Composite Index™): The current market dislocation exemplifies the core analytical function of the 24800 APN Sovereign Policy Composite Index™ — a composite measure of policy risk arising from competing or contradictory sovereign mandates operating across the property ecosystem. The RBA’s mandate to control inflation via monetary tightening is directly undermining the Federal and State governments’ mandate to increase housing supply, demonstrating how competing sovereign objectives can create systemic gridlock. The SPCI posits that state-level policy actions are frequently the dominant force shaping property market outcomes, and the current environment provides direct empirical validation of that thesis.

Supply-Side Viability Filter (APN Future Development Pipeline Index™): This analysis operationalises the 24400 APN Future Development Pipeline Index™ by moving beyond headline approval data. It applies the index’s critical economic friction filters—the 24410 APN RLV Gap™ and the 24450 APN Replacement Cost Gap™—to deconstruct the pipeline and reveal why the volume of genuinely deliverable high-density projects is contracting severely, irrespective of policy targets.

Demographic Absorption Failure (Project Carrying Capacity): The geographic bifurcation of approvals, with a collapse in the major eastern seaboard markets and marginal growth in peripheral regions, directly engages the theme of Project Carrying Capacity. Financial constraints are forcing development away from the “well-located” infill sites required to absorb population growth in primary economic centres, pushing activity towards greenfield sprawl that contradicts strategic planning objectives.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Australian Bureau of Statistics (ABS) 8731.0 Building Approvals series for January 2026 and supporting economic and industry data. The empirical data points are:

- Aggregate Approval Contraction: Seasonally adjusted total dwelling approvals fell 7.2% month-on-month and 15.7% year-on-year in January 2026, dropping to an aggregate volume of 14,564 units.

- High-Density Sector Collapse: The decline was disproportionately driven by a 24.5% monthly collapse and a severe 44.2% annual collapse in private-sector dwellings excluding houses (the statistical proxy for high-density), which fell to just 4,393 approvals.

- Low-Density Sector Divergence: In stark contrast, private-sector house approvals exhibited resilience, rising 1.1% month-on-month and 7.1% year-on-year, highlighting a profound structural bifurcation in the feasibility of different asset classes.

- National Housing Accord Deficit: The Accord requires an annual run rate of 240,000 completions. The sector’s five-year historical average for approvals is 191,417, representing a 20.2% structural deficit relative to the required baseline, a gap that is widening.

- Monetary Policy Anchor: The analysis is anchored to the Reserve Bank of Australia’s decision to increase the official cash rate to 4.10% in early 2026, which is the primary driver of inflated financing costs that render high-density projects unviable.

- Structural Cost Inflation: Construction input costs have escalated by approximately 40% over the past five years, creating a severe 24450 APN Replacement Cost Gap™ where the cost to build a new unit materially exceeds the market value of an equivalent existing property.

Critical Analysis & Balanced View

The core of this analysis is the identification of a mathematical impasse, not a cyclical downturn in sentiment. The 4.10% cash rate environment has triggered two financial circuit breakers—the 24410 APN RLV Gap™ and the 24450 APN Replacement Cost Gap™—that render the deployment of institutional capital into new high-density projects financially irrational. The RLV Gap freezes the land transaction market as vendor expectations remain anchored to a previous economic paradigm, while the Replacement Cost Gap confirms that developers cannot achieve a price point that covers costs without alienating the buyer pool, which has access to cheaper, established stock.

An examination of potential counter-narratives finds them to be analytically weak. The perceived stabilisation in construction insolvencies is a statistical artefact, a plateau at a profoundly elevated crisis level, not a recovery. The sector’s execution capacity is being structurally depleted by a toxic legacy of fixed-price contracts and impending regulatory pressures. Similarly, the marginal growth in detached housing approvals is an analytically weak counter-narrative; this sector lacks the volumetric scale and geographic alignment with infill planning policy to offset the collapse in the multi-unit pipeline. It represents a shift towards urban sprawl, which directly contradicts the Accord’s mandate for “well-located” homes.

This financial fracture is compounded by the socio-political paradox captured by the 24440 APN Social Licence & Objection Velocity™ index. A generalised public desire for more housing supply coexists with intense, localised resistance (NIMBYism) to specific high-density projects. This resistance translates into protracted planning delays, which, in a high-interest-rate environment, directly increase capital holding costs. This feedback loop actively widens the RLV Gap, turning previously marginal projects into definitively unviable ones and further entrenching the supply gridlock.

Strategic Implications for Property Professionals

- For Developers: High-density feasibility models based on pre-2025 cost of capital and construction cost assumptions are obsolete. Strategic focus must shift to projects with lower capital intensity, shorter delivery cycles, or sites where land value has been significantly recalibrated downwards to reflect the new financial reality. Engaging in protracted, high-cost rezoning applications for infill sites is financially punitive in the current rate environment.

- For Lenders & Financiers: The risk profile for high-density development finance has fundamentally increased. Underwriting must now place extreme weight on the developer’s ability to absorb extended holding costs and navigate the 24450 APN Replacement Cost Gap™. Exposure to developers reliant on legacy fixed-price contracts remains a critical and ongoing insolvency risk vector.

- For Land Vendors: Price expectations based on historical peaks or theoretical zoning uplift are now disconnected from market reality. The 24410 APN Residual Land Value (RLV) Gap™ indicates that transaction volumes for high-density development sites will remain frozen until vendors capitulate to the new, lower mathematical capacity of developers to pay for land.

- For Valuers & Consultants: The valuation of raw development sites requires a methodology heavily weighted towards a reverse-engineered feasibility based on current construction costs and finance rates, rather than comparable sales from a different economic paradigm. The concept of “highest and best use” is now constrained by immediate financial viability, not just theoretical zoning potential.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation (24410 APN RLV Gap™): The severe contraction in high-density approvals, despite explicit sovereign housing targets, provides direct empirical validation for the APN RLV Gap™ as the primary mechanism suppressing the development pipeline. It confirms the index’s thesis that financial viability, not zoning, is the ultimate gatekeeper of new supply.

- Index Calibration (24450 APN Replacement Cost Gap™): The 40% historical increase in construction costs, coupled with secondary market pricing for established apartments, mandates a recalibration of the APN Replacement Cost Gap™ index. The weighting for construction cost inputs versus established property values will be increased to reflect their dominant role in project commencement decisions.

- Data Capture (24440 APN Social Licence & Objection Velocity™): The analysis of community resistance and planning delays triggers a new structured data capture mandate. APN will begin systematically tracking council meeting minutes and planning tribunal appeal rates in key high-density corridors to quantify the time-cost impact of objection velocity, feeding this data directly into the index.

- Validation (24430 APN Supply Chain Strain Index™): Persistent construction sector insolvencies and documented labour shortages validate the index’s measurement of systemic friction. The data confirms that extended build times are a primary driver of cost overruns and financial distress, a risk that is amplified exponentially in a high-interest-rate environment.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.