RBA Confirms Housing-Led Inflation Trap, Forcing ‘Higher-for-Longer’ Stance Until H2 2026

APN ANALYSIS: A-251110-AUS62

Executive Summary

The RBA’s November 2025 Statement on Monetary Policy (SMP) has officially validated the “Project Overlord / Wealth Funnel” feedback loop. The RBA confirmed its prior policy easing is “consistent with” the housing price boom, which in turn is now the primary source of “new dwelling inflation.”

This policy-induced inflation has forced the RBA into a structural trap, compelling it to adopt a “higher-for-longer” stance. The RBA’s own forecast, which stalls the return to target inflation until the second half of 2026, has vaporised market expectations for near-term rate cuts and set a new 18-month+ timeline of policy uncertainty.

Background & Strategic Context

This SMP is a watershed event that provides central bank validation for two of our core intelligence frameworks:

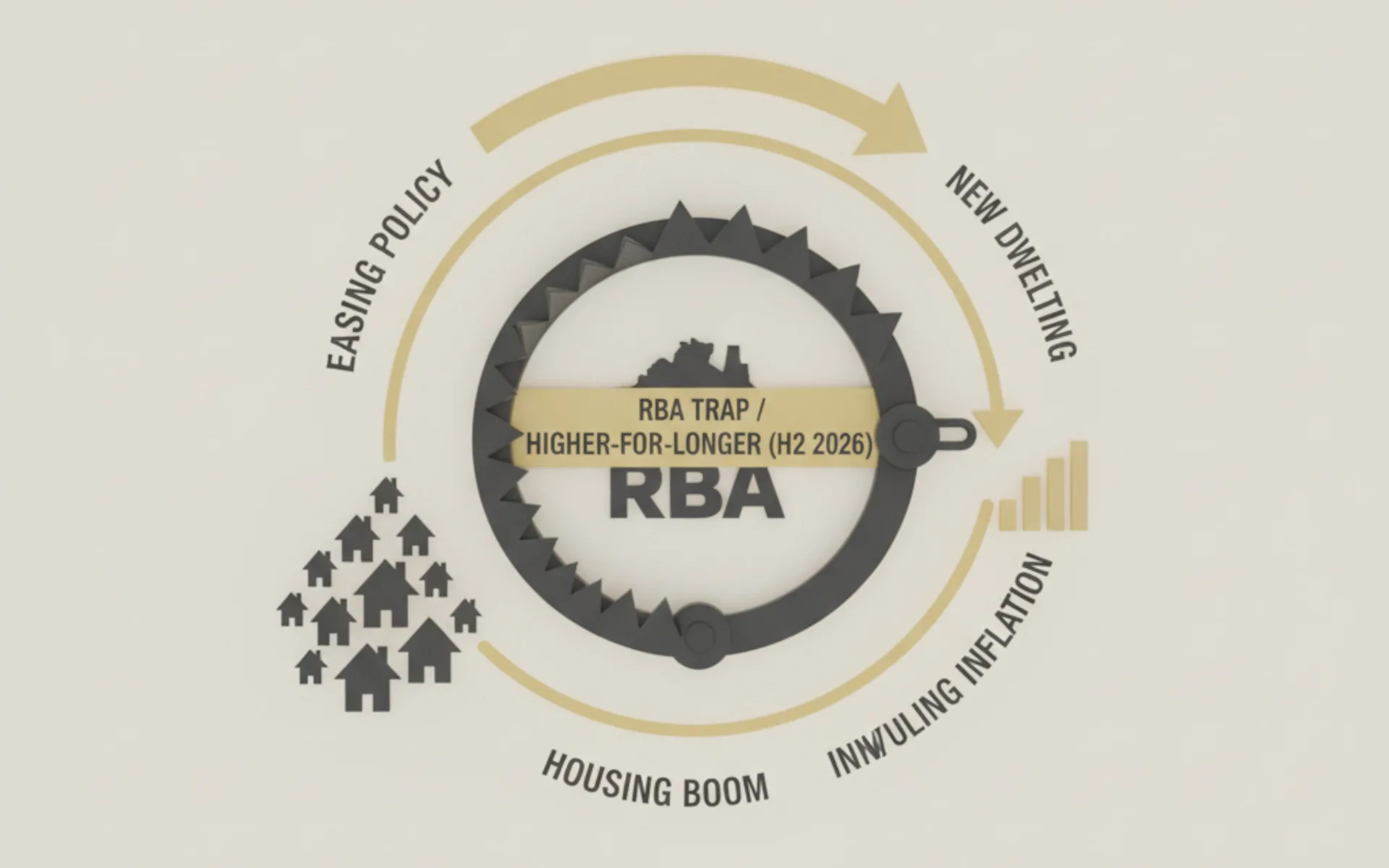

The Overlord / Wealth Funnel Feedback Loop: The RBA’s subtle admission that the housing price boom is “consistent with the easing in policy this year” is a deliberate, official acknowledgement of the policy-asset-price transmission mechanism. Synthesising the SMP’s separate sections “closes the loop,” confirming our thesis: RBA policy easing directly fuelled the housing boom, which created capacity pressures, which are now driving the “new dwelling inflation” that prevents the RBA from easing further.

APN Professional Sentiment Index™ (Codex 24300): The dominant driver for market sentiment has now shifted. It is no longer “high rates” but the “uncertainty” created by the removal of expected rate cuts. As noted by the REIA, this “extended pause” is pushing buyers “to the sidelines.” This uncertainty, driven by the RBA’s self-created policy trap, is the primary input for Codex 24300 and will suppress transaction momentum.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the RBA’s November 2025 SMP and related market commentary. The key facts are:

- Inflation Forecast: The RBA officially forecasts that underlying inflation will remain above the 2–3 per cent target band until the “second half of 2026.”

- RBA Admission: The RBA explicitly states that the “pick up” in “housing prices and housing credit” is “consistent with the easing in policy this year.”

- Inflation Driver: The upward revision to the inflation forecast is explicitly driven by “larger-than-expected price increases” in “building new homes.”

- The Mechanism: The RBA expects “new dwelling inflation to rise sharply” due to “capacity pressures in housing construction.”

- Sentiment Shift: Professional sentiment has shifted from anticipating rate cuts (CBA) to an “extended pause” (NAB forecasting May 2026).

- Market Impact: The REIA warned that the rate hold risks “pushing more buyers to the sidelines as future conditions remain uncertain.”

Critical Analysis & Balanced View

The “real” story here is the RBA’s official, if subtle, admission that it is caught in a feedback loop of its own making. The policy-asset-price transmission of “Project Overlord” is no longer a theoretical risk; it is now the active, documented source of Australia’s persistent inflation.

APN’s synthesis of the SMP sections reveals the trap in plain sight:

- Policy Easing

- Housing Growth (“consistent with”)

- Capacity Pressures

- New Dwelling Inflation (“rise sharply”)

- Higher-for-Longer Policy (H2 2026)

Balanced View: On the surface, the RBA’s decision to hold the cash rate at 3.60 per cent is a simple “extended pause.” However, APN’s analysis of the SMP document itself reveals this is a structural policy trap, not a cyclical pause. The inflationary consequence (new dwelling costs) of the policy stimulus (housing boom) is now actively constraining the RBA’s ability to act, confirming this self-created trap is a permanent feature of the new policy environment.

Strategic Implications for Property Professionals

- For Investors & Developers: The RBA’s H2 2026 timeline is the new minimum investment horizon for rate-sensitive, capital-intensive strategies. The RBA’s explicit identification of “new dwelling inflation” and “capacity pressures” validates a continued, aggressive hedging strategy against building cost escalations.

- For Sentiment & Risk Analysts: The primary input for the APN Professional Sentiment Index™ (Codex 24300) is now the REIA-articulated “uncertainty.” The stalled policy cycle, not the high rate itself, is the new source of market suppression and will reduce transaction volumes.

- For Lenders & Brokers: The confirmed “extended pause” until H2 2026 removes easing optimism and will “weigh on sentiment.” This directly increases portfolio exposure to mortgage stress in low-buffer segments and requires a full recalibration of serviceability models.

- For Economists: This event confirms the “Project Overlord” thesis. The RBA’s own documentation validates that the policy-to-asset feedback loop is no longer a risk but an active, structural constraint on monetary policy.

Disclaimer

The analysis and information contained in this analysis are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on internal APN intelligence, data, and information believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events. Property values and market conditions can go down as well as up.

Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.