Federal Budget’s $1.6B Housing Intervention: A Targeted Policy Adjustment on the RLV Gap and Regulatory Sustained Friction

APN ANALYSIS: A-251115-AUS130488

Executive Summary

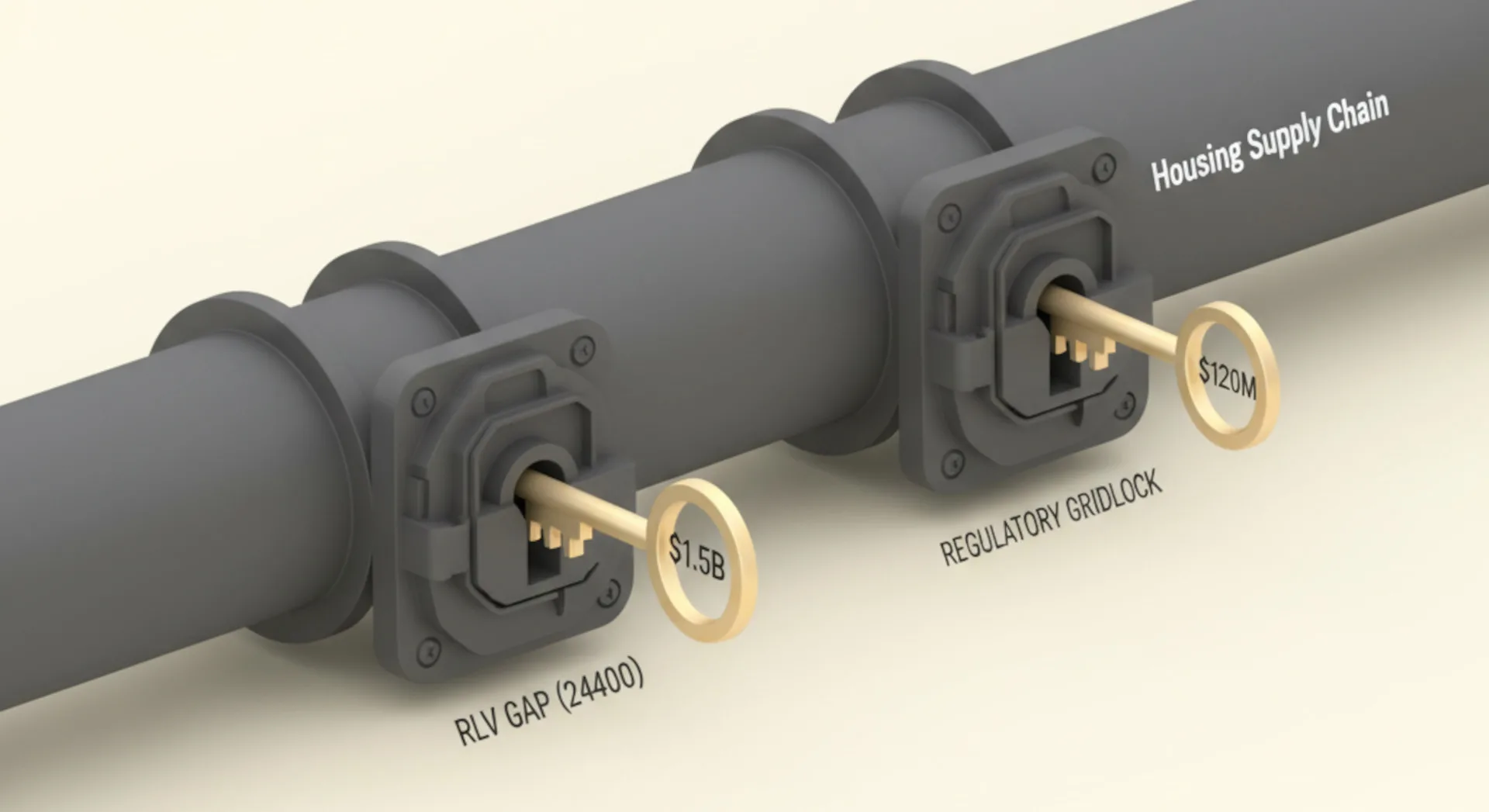

The Federal Budget 2025-26 has deployed two highly targeted financial interventions: the $1.5 billion Housing Support Program and a $120 million allocation from the National Productivity Fund. APN analysis confirms these are not general stimulus measures, but targeted policy tools designed to unlock two of the most elevated structural constraints in Australia’s housing supply chain. The $1.5B fund directly addresses the Residual Land Value (RLV) Gap by providing capital for the enabling infrastructure and planning capacity that currently renders zoned land financially unviable for development. Concurrently, the $120M fund acts as a financial incentive to accelerate the Regulatory Velocity Multiplier, incentivising states to remove the regulatory friction that prevents the at-scale adoption of Modern Methods of Construction (MMC).

For property professionals, this represents a fundamental shift in the development landscape. The government is no longer just a regulator; it is now an active financial partner in de-risking the front end of the development cycle. These interventions signal where future supply will be unlocked, creating new opportunities in locations previously sidelined by prohibitive infrastructure costs and regulatory friction. Developers, investors, and consultants must now factor this direct government underwriting of viability and speed into their strategic planning and site acquisition models.

Background & Strategic Context

This Federal Budget intervention is a direct validation of APN’s core APN Sovereign Policy Composite Index™ (SPCI, 24800) thesis, which posits that direct state action is the primary force shaping property market boundaries and outcomes. Rather than broad-based stimulus, the government has opted for targeted policy adjustments on systemic blockages, demonstrating a sophisticated understanding of the supply chain’s mechanics. These actions are designed as the enabling keys to unlock the potential of the much larger $33 billion national housing plan.

A Targeted Intervention (APN Sovereign Policy Composite Index™ (SPCI, 24800)): The combined $1.62 billion of these two programs is strategically disproportionate to its dollar value. Within a multi-billion-dollar national housing strategy, these funds act as the critical ‘plumbing and permits’. They are not designed to fund houses directly, but to unblock the financial and regulatory pathways that the larger pools of public and private capital must flow through, confirming their function as precise APN Sovereign Policy Composite Index™ (SPCI, 24800) interventions.

Closing the Viability Gap (Future Development Pipeline Index™): The $1.5 billion Housing Support Program is a direct measure to address the Residual Land Value (RLV) Gap. By funding last-mile infrastructure (roads, water, power) and council planning capacity, it absorbs the prohibitive upfront costs that prevent development feasibility. This mechanism is designed to convert what APN defines as ‘Paper Rezonings’, economically unviable zoned land, into genuine, shovel-ready opportunities, a core function tracked by our Future Development Pipeline Index™.

Accelerating the Pace (Regulatory Velocity Multiplier): The $120 million MMC fund is a financial lever designed to increase the Regulatory Velocity Multiplier. It pays states to harmonise building codes and remove the ‘regulatory friction’ blocking the use of prefabricated and modular construction. This is a classic federal manoeuvre to alleviate state-level regulatory sustained friction, directly targeting the ‘time cost’ of development, a key metric within our APN Risk & Compliance Index™ (24200) risk framework.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the Federal Budget 2025-26 papers, associated ministerial statements, and corroborating industry submissions. The key facts are:

- The RLV Gap Intervention: A $1.5 billion Housing Support Program is confirmed, explicitly designed to fund state, territory, and local governments for “enabling infrastructure such as roads, water and power” and to “improve planning capability.”

- The Regulatory Velocity Intervention: A $120 million allocation from the National Productivity Fund is confirmed, with the express purpose to “incentivise states and territories to remove regulatory friction preventing the uptake of modern methods of construction (MMC)” and help homes be built faster.

- The Dual-Action Mechanism: The $1.5B fund addresses both ‘hard’ infrastructure costs (validated by a $27.2 million grant for a sewage plant upgrade in Marulan) and ‘soft’ planning bottlenecks (validated by a $1.5 million grant to Blacktown City Council for housing capacity studies), confirming a sophisticated, dual-pronged approach to closing the RLV Gap.

- The Multi-Pronged MMC Strategy: The $120M incentive is the financial ‘leverage’ in a wider federal strategy. It is supported by a $4.7M allocation to the Australian Building Codes Board (ABCB) to create a national MMC standard (the ‘technical fix’) and a $49.3M fund to help states scale up existing MMC projects (the ‘pump-primer’).

- Industry Validation: Peak industry bodies have confirmed these interventions target the correct barriers. The Urban Development Institute of Australia (UDIA) directly lobbied for an “enabling infrastructure fund” to solve the RLV Gap, while the Housing Industry Association (HIA) and Master Builders have consistently cited regulatory fragmentation as the key obstacle to MMC adoption.

Critical Analysis & Balanced View

The strategic nature of these interventions lies in their asymmetry; their market impact will be far greater than their relatively modest monetary value suggests. They function as catalysts, designed to unlock tens of billions in otherwise stalled public and private development capital. However, this approach is not without complexity or risk. The policy represents a significant centralisation of power, with the Federal Government using its financial might to directly influence local planning and state-based building regulations, a classic APN Sovereign Policy Composite Index™ (SPCI, 24800) manoeuvre that could create significant federal-state friction if not managed carefully.

Furthermore, a key risk is scale. While the interventions are precisely targeted, the $1.5 billion allocated for infrastructure may prove insufficient against the backdrop of a nationwide deficit estimated to be many times that figure. The UDIA’s original ask was for $5 billion, suggesting the current program may function as a pilot. Its success will be measured by its ability to create replicable models for de-risking development, but it may initially only create isolated pockets of viability rather than a systemic, nationwide solution.

An additional opportunity exists within the MMC intervention. By driving the creation and adoption of a national standard, the government is not just encouraging faster building; it is structuring the industrialisation of the Australian construction sector. This will inevitably favour large, sophisticated firms capable of leveraging standardisation and scale, potentially reshaping the competitive landscape and accelerating market consolidation.

Strategic Implications for Property Professionals

- For Developers: The $1.5B Housing Support Program is a direct subsidy for your feasibility studies. Immediately identify land parcels previously deemed unviable due to servicing costs or council planning delays. Proactively engage with local and state governments to co-develop applications for this fund, effectively using public money to de-risk your front-end development costs and unlock your pipeline.

- For Investors & Fund Managers: Re-weight portfolio analysis towards regions and development partners positioned to capture these subsidies. The government is explicitly signalling where growth will be unlocked. Identify and prioritise developers with established MMC capabilities, as they are set to benefit from regulatory tailwinds and will likely deliver projects faster and with greater cost certainty.

- For Planners & Consultants: A new, federally funded revenue stream has opened. Position your services to assist local councils in applying for the ‘planning capability’ stream of the Housing Support Program. There is a clear mandate and funding for the strategic planning, capacity studies, and DA process optimisation that many councils lack the resources to undertake themselves.

- For Construction & Building Materials Suppliers: The multi-pronged MMC intervention is an unambiguous signal to industrialise. The creation of a national certification scheme via the ABCB de-risks investment in prefabrication, modular systems, and digital design. This is the moment to pivot business models and supply chains towards a national, standardised market, moving MMC from a niche solution to a mainstream, government-backed methodology.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation (APN Sovereign Policy Composite Index™ (SPCI, 24800)): This analysis provides validation of the APN Sovereign Policy Composite Index™ (SPCI, 24800) thesis, demonstrating direct, top-down federal intervention designed to alter market conditions in a targeted manner at elevated structural constraints in the housing supply chain.

- Index Calibration (Future Development Pipeline Index™ 24400): The Residual Land Value (RLV) Gap metric is recalibrated. The $1.5B Housing Support Program now acts as a direct negative input on the ‘Infrastructure Cost’ variable for specific LGAs that receive funding. This will turn previously negative RLV calculations positive, moving sites from ‘Paper Rezoning’ to ‘Genuine Opportunity’ status within the index.

- Index Calibration (APN Risk & Compliance Index™ (24200)): The Regulatory Velocity Multiplier is now calibrated to track state-level adoption of the forthcoming national MMC standard. States that adopt the harmonised codes will see their Multiplier rating increase, reflecting a lower ‘time cost’ of development, while non-compliant states will be flagged for higher regulatory friction and risk.

- Data Capture Mandate: This analysis triggers a new data capture mandate to track all grant allocations under the $1.5B Housing Support Program and the $120M National Productivity Fund. This data will be mapped geographically to recalibrate the Future Development Pipeline Index™ (24400) at the LGA level, providing granular insight into newly viable development precincts.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24500) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.