Australian Housing Supply Pipeline Exhibits Material Divergent Stress as Delivery Costs Escalate

APN ANALYSIS: A-260423-AUS138989

Executive Summary

The Australian residential housing supply pipeline exhibited a state of material divergent stress at the close of 2025, a condition that remains structurally intact at the time of this analysis. A detailed analysis of the APN Housing Supply Pipeline (21500 Series) reveals a structural decoupling between the approval of new dwellings and the capacity of the construction sector to physically commence and complete them. Despite a high volume of development approvals, physical commencements are contracting, and the financial cost to complete the existing pipeline of work has escalated to a multi-year high. This divergence signifies a material bottleneck in the conversion of theoretical supply into tangible housing stock, driven by a combination of structural inflation in the supply chain and elevated rates of corporate insolvency within the construction sector.

For property professionals, this analysis signals a period of heightened execution risk and a fundamental shift in project viability. Developers must now factor in materially higher contingency budgets and extended delivery timelines. Investors and financiers must apply intensified due diligence, looking beyond headline approvals to assess the financial solvency of construction partners and the true, inflation-adjusted cost of project completion. The widening gap between the cost of new builds and the value of existing properties establishes a structural price floor for completed assets, while simultaneously increasing the risk profile for off-the-plan and yet-to-be-commenced projects.

Background & Strategic Context

This analysis validates and calibrates APN’s core macro-thesis that structural supply-side constraints are a primary determinant of long-term asset values in the Australian property market. The significance of this research lies in its multi-dimensional quantification of the supply pipeline’s operational state, moving beyond simplistic, first-order metrics like dwelling approvals. By synthesising data on statutory intent, physical pipeline volume, and financial capacity, the framework provides an empirical explanation for why the housing supply is failing to respond elastically to persistent demographic demand, thereby creating a structural underpinning for asset prices.

Intent-to-Execution Failure — Building Approvals & Commencements (21510): The widening spread between the number of dwellings approved and the number physically commenced indicates a material failure in the initial phase of the supply pipeline. This suggests that while statutory authorities and developers are signalling intent to build, economic or operational barriers are preventing projects from breaking ground at a rate consistent with historical norms.

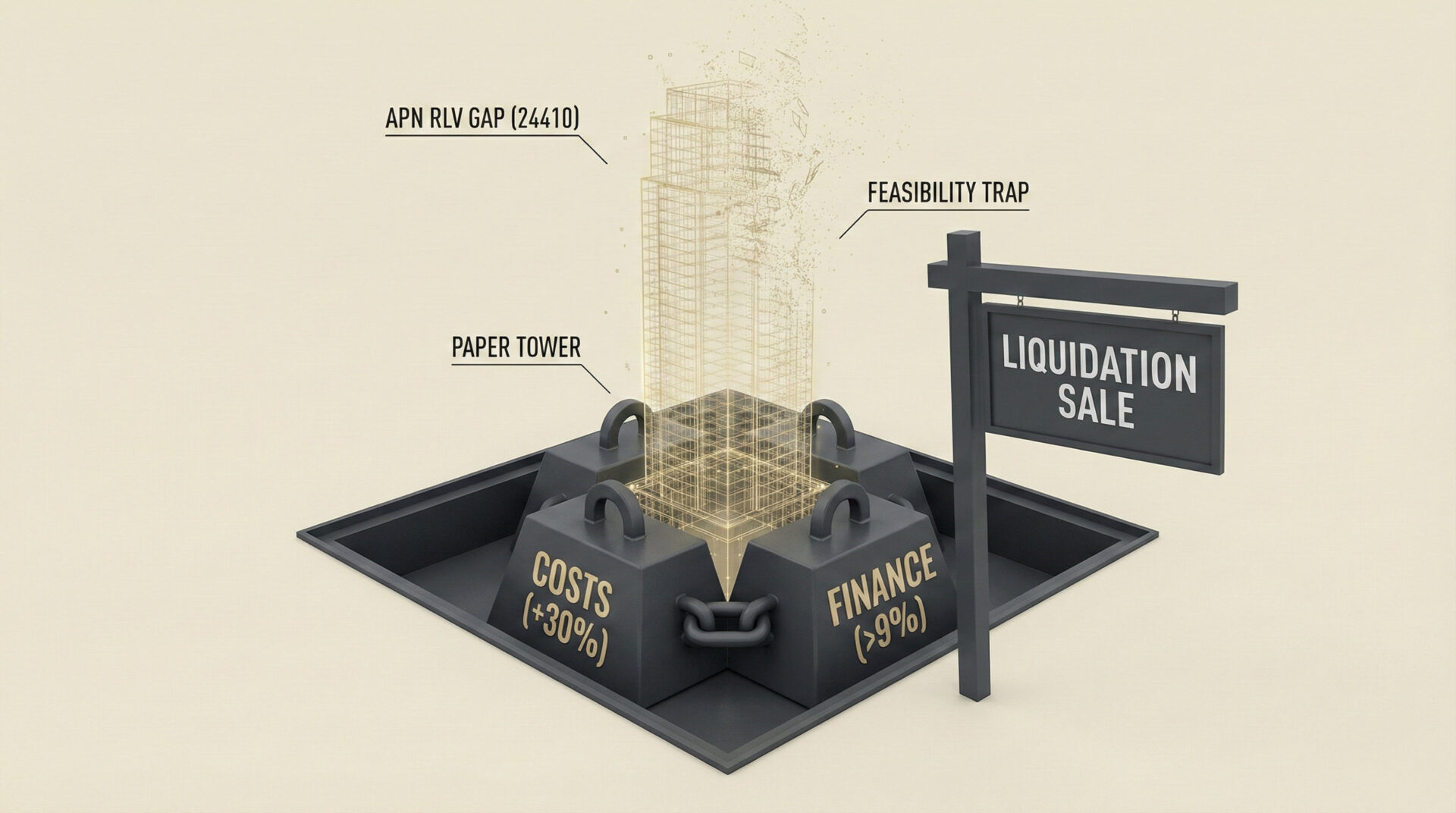

Structural Pipeline Inflation — New Housing Supply Forecasts (21520): The pronounced decoupling between the number of dwellings under construction and the financial value of work yet to be done provides a quantitative measure of material cost inflation. The sector is spending significantly more capital to complete a comparatively static volume of physical work, indicating that labour and materials costs are eroding project viability and constraining delivery capacity.

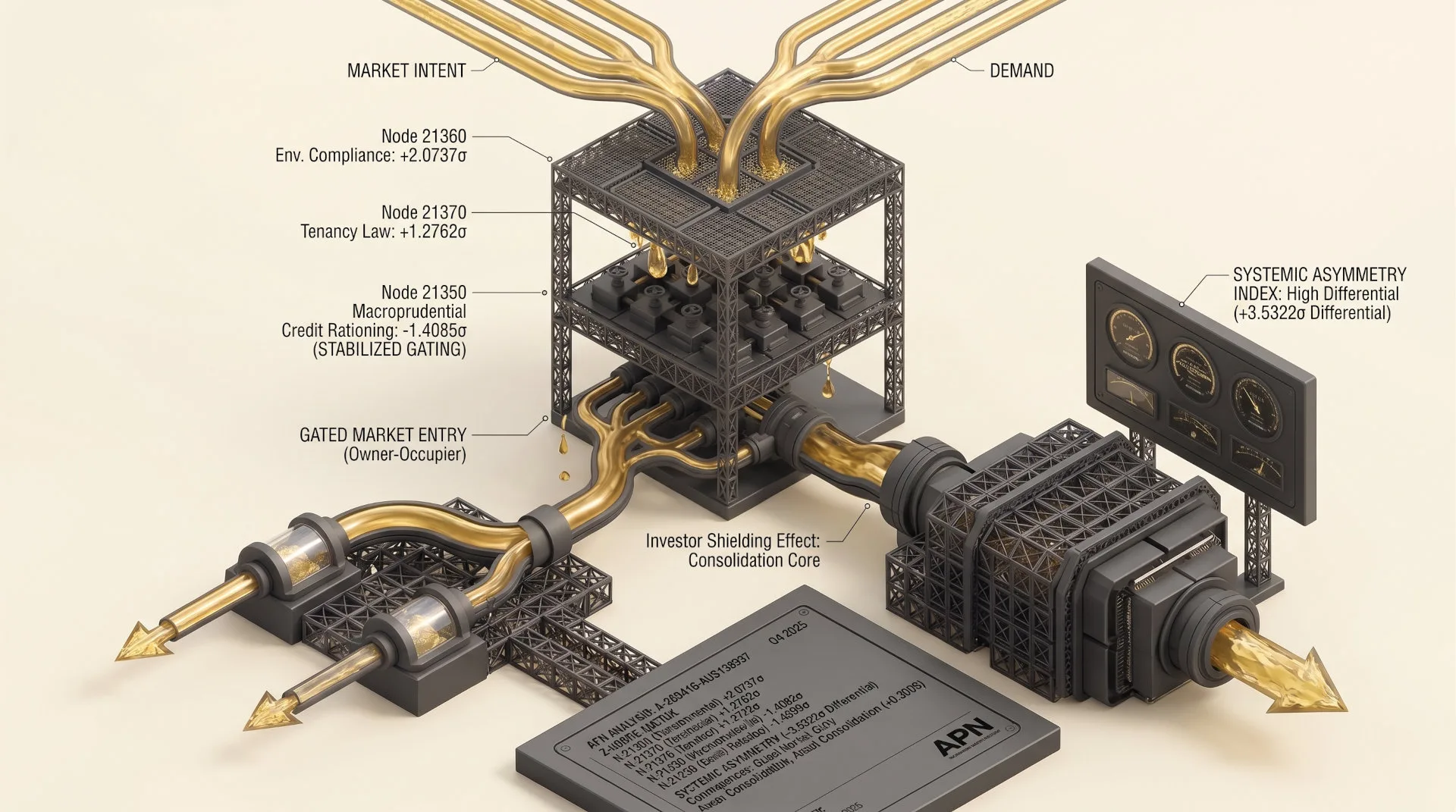

Masked Financial Distress — Construction Finance & Capacity (21530): A superficially positive reading on sector financial capacity masks a more complex reality. The metric is artificially elevated due to a structural lag in the reporting of construction company insolvencies. This creates a significant hidden risk, where available institutional credit is not translating into market activity because the corporate entities required to execute the work are facing material financial distress.

Deconstruction of the Source Event

This deconstruction is based on APN’s analysis of the terminal state of the Australian residential supply pipeline at Q4 2025, synthesising data from the Australian Bureau of Statistics (ABS), the Australian Prudential Regulation Authority (APRA), and the Australian Securities and Investments Commission (ASIC). The key facts are:

Elevated Conversion Constraint: The spread between dwelling approvals and commencements registered at \(+1.5885\sigma\) above the 15-year mean. This divergence is driven by approvals running above the mean (\(+1.0843\sigma\)) while commencements are materially suppressed below it (\(-1.0483\sigma\)), confirming a significant bottleneck in project activation.

Structural Cost Escalation: The financial value of work yet to be done on active projects reached \(+2.2819\sigma\), materially outpacing the physical volume of dwellings under construction (\(+1.0553\sigma\)). This mathematical delta quantifies a state of structural inflation within the construction pipeline.

Misleading Capacity Signal: The composite index for construction finance and capacity registered a high \(+2.1333\sigma\). However, this figure is a result of a mandatory data substitution for lagged insolvency statistics, which computationally neutralises a key distress signal that was otherwise registering at multi-year highs in preceding quarters.

Critical Analysis & Balanced View

The analysis reveals a structural paradox at the heart of the Australian construction sector: the co-existence of high institutional credit availability and record-high corporate distress. The terminal reading from Construction Finance & Capacity (21530) shows that APRA-regulated credit limits are not the primary constraint. Instead, the structural inflation quantified in New Housing Supply Forecasts (21520) is the active mechanism driving sector attrition. Escalating costs for labour and materials are rendering previously viable projects unprofitable, leading to a wave of corporate insolvencies. This means that even where wholesale funding is available, the pool of solvent, capable construction firms able to deploy it is contracting, effectively severing the link between financial capacity and physical delivery.

Furthermore, the current state of Divergent Stress can be understood as a direct consequence of the policy-induced Artificial Inflation observed during the 2020–2022 pandemic period. Stimulus measures including HomeBuilder and temporary insolvency protections pulled forward demand and masked underlying financial vulnerabilities. This created a synthetic surge in commencements that overwhelmed supply chains, seeding the latent cost pressures that are now manifest. The subsequent removal of these sovereign supports did not create the current distress but rather allowed the pre-existing, masked conditions to resolve into the observed wave of insolvencies and project delays. The current market dislocation is therefore not a new phenomenon, but the system’s lagged structural re-normalisation to economic reality.

Strategic Implications for Property Professionals

For Developers: Project feasibility models require immediate recalibration to account for elevated construction cost inflation and extended delivery timelines. Securing fixed-price contracts and financially robust construction partners is now a material risk mitigation strategy, as the headline availability of institutional credit does not guarantee project-level execution.

For Financiers & Lenders: Underwriting processes must evolve beyond assessing headline credit limits. Enhanced due diligence is required to probe the solvency of individual construction firms and the real-world cost pressures on specific projects. The high composite capacity score should be viewed as a lagging indicator that masks significant forward-looking risk.

For Investors: A clear distinction must be made between approved projects and genuinely deliverable ones. Due diligence on off-the-plan assets must now prioritise the financial health and track record of the builder. The risk of project delays, rescissions, or outright failure is materially elevated across the sector.

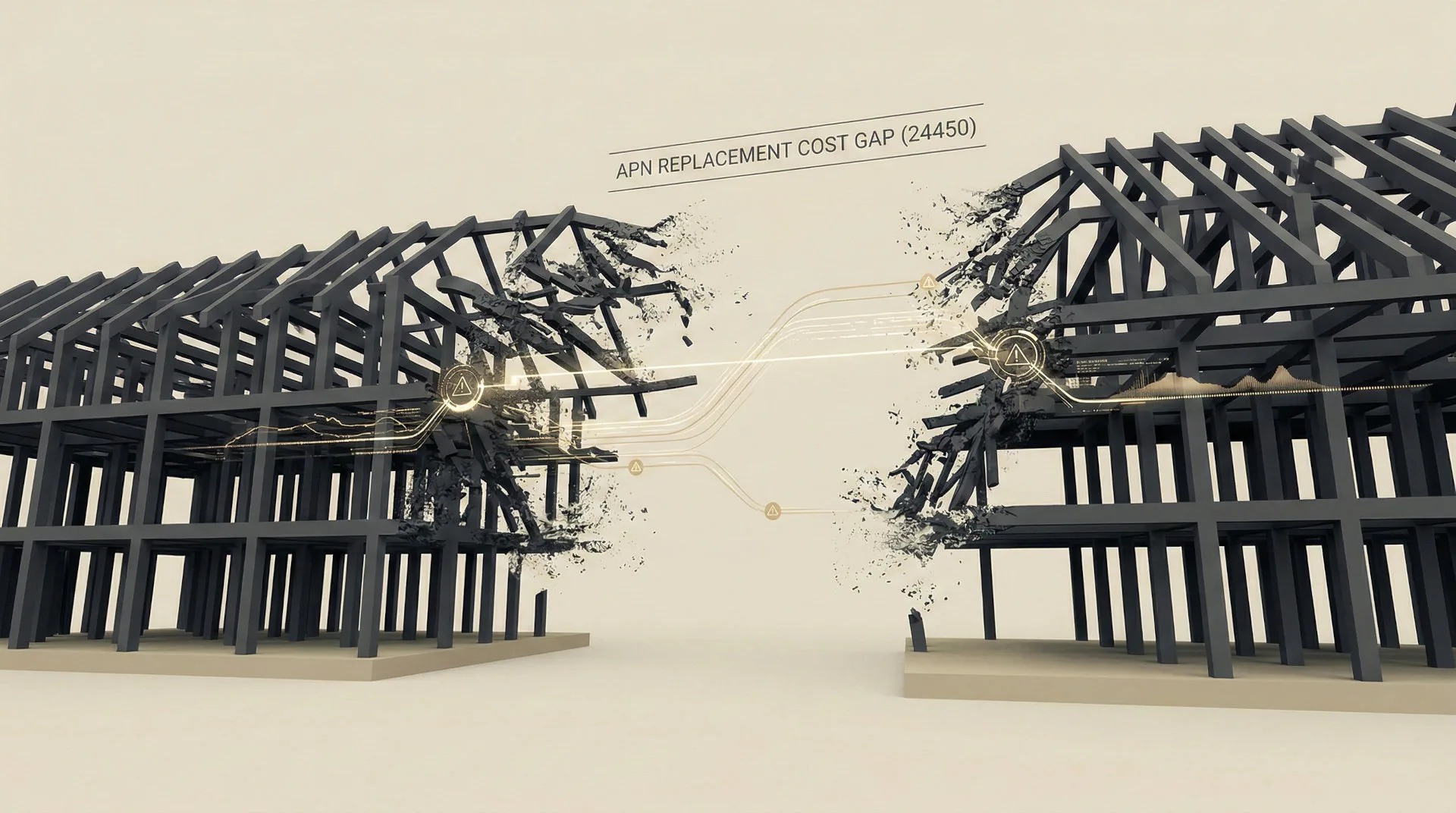

For Valuers: The structural gap between the escalating cost of new construction and the value of existing properties provides a firm valuation floor for completed assets. This replacement cost gap is widening, supporting the values of established stock while simultaneously making new development less viable without higher end-prices.

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

Validation: This analysis validates the APN Future Development Pipeline Index™ (24400) by empirically demonstrating how financial capacity (Node 21530) and execution costs (Node 21520) act as material filters on theoretical approvals (Node 21510), creating the observed divergence between development intent and physical delivery.

Validation: This analysis validates the APN Replacement Cost Gap™ (24450), using the quantified decoupling of financial value (WYTBD_t) from physical volume (DUC_t) in Node 21520 to measure the rising per-dwelling completion cost that supports the valuation of existing assets.

Index Calibration: The APN Supply Chain Strain Index™ (24430) has been calibrated to incorporate the documented lag in official corporate insolvency data (Node 21530), assigning a higher weight to leading indicators of distress to correct for the artificially elevated composite reading.

Index Calibration: The APN Sovereign Policy Composite Index™ (24800) has been calibrated to model the rebound effects of major policy interventions, specifically quantifying the lagged increase in corporate insolvencies following the cessation of temporary pandemic-era support measures.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.