Divergent Regulatory Trajectories Structurally Constrain New Housing Supply While Gating Market Entry

APN ANALYSIS: A-260416-AUS138937

Executive Summary

Terminal analysis of the APN Codex 21300 Series at Q4 2025 reveals a material compositional shift in the regulatory environment governing Australian residential property. The data indicates that sovereign policy friction is no longer moving in a uniform direction. Instead, supply-side constraints, particularly those related to environmental compliance and tenancy law, are escalating at a statistically significant rate. Concurrently, demand-side constraints, primarily macroprudential credit controls, have stabilised at a highly restrictive level relative to the 15-year historical mean. This divergence creates a complex equilibrium where the cost to build and manage housing is rising, while the capacity for new entrants to acquire it remains structurally suppressed.

For property professionals, this asymmetrical regulatory landscape requires a recalibration of analytical assumptions. The escalating, non-negotiable cost floor imposed by environmental building codes must be treated as a permanent feature in development feasibility studies. For investors, the rising operational burden of tenancy laws favours scaled operators with the capacity to absorb compliance costs, potentially displacing smaller asset holders. The combination of a constrained credit pathway for purchasers and a diminishing social housing sector points to sustained structural demand in the private rental market, creating distinct risks and opportunities for well-capitalised participants prepared for a higher-friction operating environment.

Background & Strategic Context

This analysis validates and calibrates APN’s core macro-thesis regarding compounding sovereign risk. The findings demonstrate that uncoordinated, multi-jurisdictional policy interventions create a complex and structurally divergent friction environment that is not adequately captured by simplistic measures of aggregate regulatory burden. By quantifying the divergent trajectories of discrete regulatory vectors—such as Commonwealth macroprudential directives versus state-based building codes—this analysis provides a granular, mathematically-grounded view of the structural forces shaping the Australian residential asset base. The significance lies in moving beyond a binary tighter-or-looser assessment to a more sophisticated understanding of regulatory composition and its market impact.

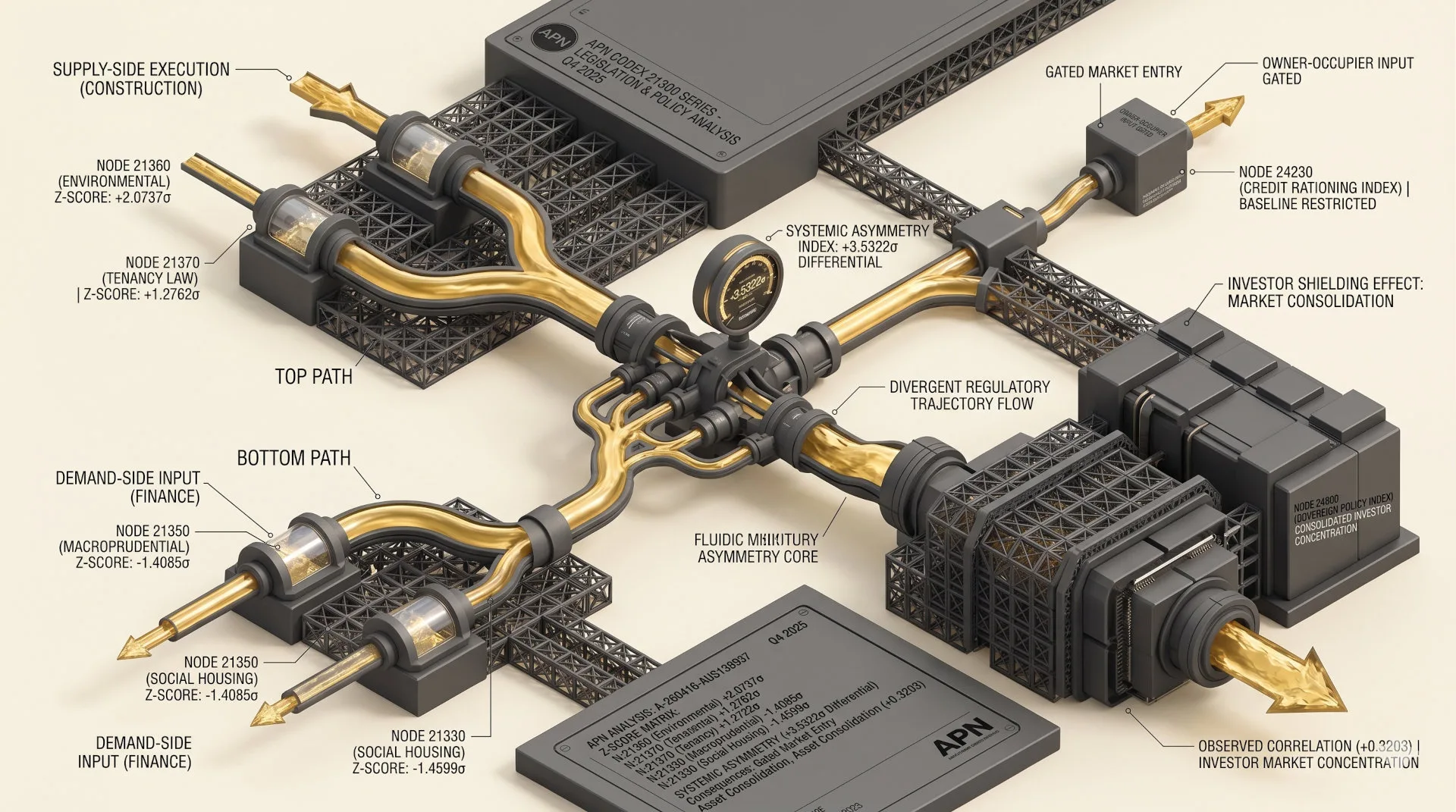

Escalating Construction Cost Floors (APN Replacement Cost Gap™ (24450)): The dominant friction vector identified is the +2.0737σ reading for Node 21360 (Environmental Compliance). Driven by the National Construction Code 2022 step-change, this establishes a structurally higher capital expenditure requirement for all new housing delivery, directly elevating the cost side of the development feasibility equation.

Rising Operational Friction (APN Sovereign Policy Composite Index™ (24800)): The sustained tightening trajectory of Node 21370 (Tenancy & Consumer Protection Law), with a terminal reading of +1.2762σ, quantifies the increasing compliance burden on landlords. This elevates the ongoing operational costs and legal risks associated with holding residential investment assets, particularly impacting smaller, under-capitalised market participants.

Stabilised Credit Rationing (APN Credit Rationing Index™ (24230)): The terminal reading of -1.4085σ for Node 21350 (Macroprudential Lending Regulation) indicates that macroprudential constraints on borrower capacity have stabilised at a materially restrictive level. While the velocity of new interventions has slowed, the existing framework continues to act as a significant gate on market entry for wage-reliant purchasing cohorts.

Eroding Alternative Supply (APN Sovereign Policy Composite Index™ (24800)): The structurally significant -1.4599σ reading for Node 21330 (Social Housing Policy) confirms a material decline in the proportional share of social and affordable housing. This erosion of non-market alternatives concentrates demand from lower-income cohorts directly into the private rental sector, compounding existing demand pressures.

Deconstruction of the Source Event

This deconstruction is based on APN’s terminal analysis of the Codex 21300 Series — Legislation & Policy Analysis — at Q4 2025, synthesising data across a 60-quarter observation period. The key facts are:

- Elevated Supply-Side Friction: Node 21360 (Environmental Compliance) and Node 21370 (Tenancy & Consumer Protection Law) recorded terminal Z-Scores of +2.0737σ and +1.2762σ respectively, indicating statistically significant increases in the structural cost to build and manage residential assets relative to the 15-year mean.

- Restrictive Demand-Side Conditions: Node 21350 (Macroprudential Lending Regulation) recorded a Z-Score of -1.4085σ, confirming that macroprudential settings remain a material constraint on borrower purchasing capacity, keeping access to credit significantly tighter than the long-term historical average.

- Contracting Social Housing Share: Node 21330 (Social Housing Policy) registered a Z-Score of -1.4599σ, identifying a sustained structural decline in the proportional delivery of state-supported housing relative to total dwelling stock growth.

- Divergent Regulatory Trajectories: The analysis reveals a compositional shift, not a uniform tightening. Supply-side execution costs are escalating while demand-side financial constraints have stabilised at a restrictive level, creating an asymmetrical friction environment.

- Near-Mean Planning & Taxation Friction: Node 21320 (Planning & Zoning Policy) at +0.1883σ and the substantive analytical signal for Node 21310 (Taxation & Revenue Policy) at -0.8528σ indicate these domains are currently operating close to their long-run historical averages.

Critical Analysis & Balanced View

The data reveals a critical second-order dynamic APN documents as the Investor Shielding Effect. This is a paradoxical outcome where escalating environmental compliance costs (21360), which increase capital expenditure, inadvertently favour well-capitalised investors over prospective owner-occupiers. While higher construction costs price out income-constrained buyers—who are simultaneously limited by restrictive credit access (21350)—investors relying on existing equity reserves can more readily absorb these premiums. The analysis identifies a positive correlation (+0.3203) between cumulative policy friction and investor market concentration, demonstrating how regulations designed to improve building standards can concurrently consolidate capital asymmetry within the market.

Furthermore, the synthesis of three separate nodes exposes a compounding pressure on the private rental market. Firstly, credit constraints (21350) prevent a cohort of prospective buyers from leaving the rental market. Secondly, the contracting share of social housing (21330) channels demand from vulnerable cohorts into the same private market. This dual-sided demand pressure occurs while landlords face escalating operational and compliance costs under tightening tenancy laws (21370). This convergence of elevated demand and rising operational friction creates a structural environment that favours scaled, institutional operators who possess the capital and administrative frameworks to manage the compounding compliance burden, progressively displacing smaller, margin-constrained investors.

Strategic Implications for Property Professionals

- For Developers & Builders: Feasibility assessments must now treat the elevated capital expenditure premiums from environmental compliance (21360) as a structural, non-negotiable cost floor, rather than a cyclical variable. The divergence in state-level adoption of the NCC 2022 necessitates a jurisdictional-specific approach to project costing and supply chain management.

- For Residential Investors & Asset Managers: The compounding effect of rising compliance costs (21370) and capital expenditure requirements (21360) structurally favours operators with scale. Smaller investors must critically assess their capacity to absorb these escalating operational frictions, while institutional investors can leverage this environment to consolidate market share.

- For Lenders & Mortgage Brokers: The stabilised but restrictive credit environment (21350) establishes a structurally persistent constraint on purchasing capacity for wage-reliant borrowers. This indicates that market access will continue to be gated by deposit size and equity, favouring established asset holders over first-time buyers, particularly for new construction.

- For Policy Analysts & Planners: The data demonstrates that permissive zoning (21320) does not automatically translate to increased housing supply when intersecting with high construction cost floors (21360). Policy effectiveness now depends on addressing the commercial viability gap between approval and delivery, as tracked by the APN Residual Land Value Gap™ (24410).

APN Index Management

The APN Codex 24000 Series is a proprietary set of indices that translates complex market forces into measurable metrics. This section outlines how the preceding analysis is validated against, and informs the calibration of, these frameworks.

- Validation: This analysis validates the APN Sovereign Policy Composite Index™ (SPCI) (24800) by demonstrating how divergent sovereign policy vectors (e.g., environmental, macroprudential, tenancy) create compounding and structurally divergent market frictions, rather than a single, uniform regulatory burden.

- Validation: The findings empirically validate the mechanism underpinning the APN Replacement Cost Gap™ (24450), confirming that regulatory mandates from Node 21360 (Environmental Compliance) directly elevate the structural cost of delivering new assets.

- Index Calibration: The APN Credit Rationing Index™ (24230) is calibrated to reflect the stabilised but structurally restrictive state of macroprudential policy, with the terminal Z-Score of -1.4085σ from Node 21350 establishing a new baseline for constrained credit access.

- Data Capture: This triggers a new data capture mandate for the APN Residual Land Value (RLV) Gap™ (24410) to more granularly track the commercial viability of approved projects in jurisdictions with high environmental compliance costs (Node 21360) versus those with deferred adoption.

Disclaimer

The analysis and information contained in this deconstruction are for general informational and strategic purposes only and do not constitute financial, investment, legal, or any other form of professional advice. The Australian Property Network (APN) is a strategic intelligence organisation and is not a licensed financial advisor.

This analysis is based on data and information from third-party sources believed to be reliable; however, APN provides no warranty as to its accuracy, currency, or completeness. Images used in this analysis are for illustrative and conceptual purposes only and may not represent real persons, properties, or events.

All frameworks (Codex 24100-24800) are proprietary to APN.

Property values and market conditions can go up or down. Before making any property or investment decisions, you must conduct your own thorough research and seek independent professional advice tailored to your specific circumstances.